Where to Get Income in a Low-Yield World

Date Posted: February 14, 2020

Read time: 49 min

So far in 2020, the yield on the 10-year Treasury has averaged 0.01 percent when adjusted for inflation. Since the end of January, it's actually dipped below 0 percent, trading as low as negative 0.14 percent on January 31.

U.S. Global Investors Reports Financial Results for the Second Quarter of 2020 Fiscal Year

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

So far in 2020, the yield on the 10-year Treasury has averaged an anemic 0.01 percent when adjusted for inflation. Since the end of January, it’s actually dipped below 0 percent, trading as low as negative 0.14 percent on January 31.

What this means is that investors are guaranteed to lose money on the 10-year T-note if held until maturity.

It’s against this low-yield backdrop that Judy Shelton, one of President Donald Trump’s nominees for the Federal Reserve Board, went before the Senate Banking Committee this week for her confirmation hearing. A former Trump campaign advisor, Shelton is seen as an unconventional pick for the central bank role for two main reasons: 1) She’s advocated for a return to the gold standard, and 2) She has recently argued in favor of lower interest rates—which could have the effect of pushing not just inflation-adjusted yields but also nominal yields into negative territory.

Some have already speculated that, if Shelton is confirmed and Trump wins reelection this November, she may be tapped to replace Jerome Powell as Fed chair when his term ends in 2022. During his tenure, Powell has repeatedly come under fire by the president for not cutting rates fast enough—something Judy Shelton may be more willing to do.

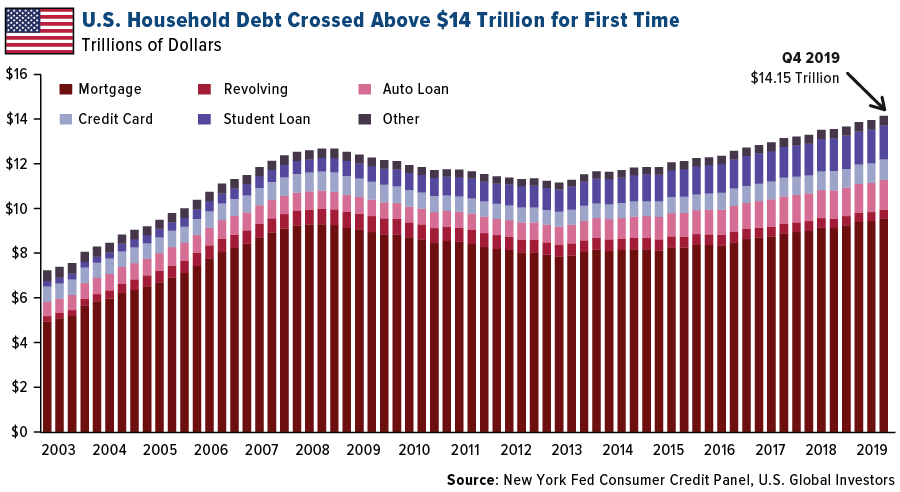

A lower-for-longer monetary environment has its benefits, to be sure. It’s great for borrowers. It makes it easier for companies and governments to service their debts. It encourages consumption. Indeed, rock-bottom borrowing costs have fueled U.S. household debt over the past decade, lifting it above $14 trillion for the first time at the end of 2019. Credit card debt alone hit a record $930 billion.

Negative Yields to Cost Investors $1 Trillion in 2020

What’s good for borrowers, though, is not always good for investors and savers. Low-to-negative rates make it challenging to generate income, and this may push investors into riskier assets such as non-investment grade and junk bonds.

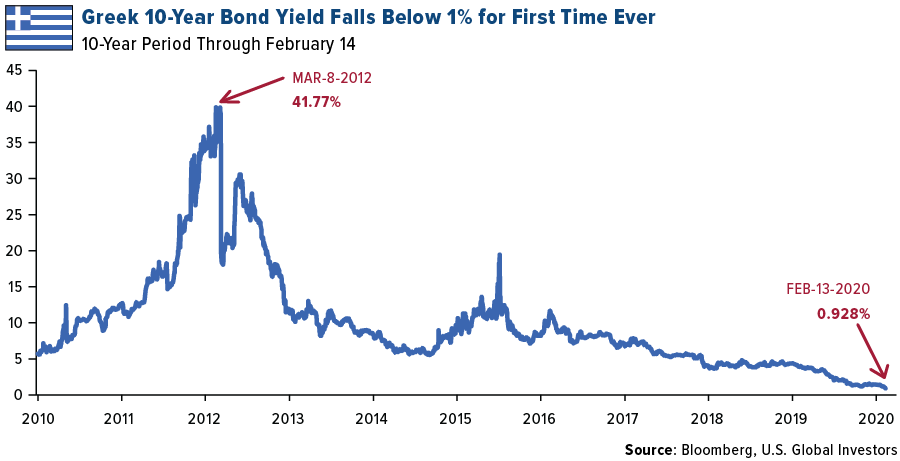

Just take a look at what’s happening in Greece right now. Never mind the Mediterranean country’s BB rated credit. A bond rally there has driven Greek 10-year yields below 1 percent for the first time ever as income-starved investors pile into one of the few eurozone debt markets to still offer a positive yield.

Can you blame them? The mountain of negative-yielding government bonds around the world, now at $13 trillion, could inadvertently cost pension funds and other institutional investors as much as $1 trillion this year, according to estimates by Daniel Tenengauzer, head of markets strategy at Bank of New York Mellon.

Check Your 401(k) for This Bond ETF

But who buys negative-yielding bonds anyway? (And here I’m talking about nominal bond yields, not inflation-adjusted yields. When adjusted for inflation, these bond yields are even more negative.)

Don’t act surprised, but chances are good that you own some in your 401(k), especially if it holds passive ETFs that track international bond markets. One of the more popular ETFs, the Vanguard Total International Bond ETF, is highly concentrated in some of the biggest issuers of debt that trades with a negative yield. As of the end of last quarter, 19 percent of the ETF was allocated to Japan, where about half of all debt carries a yield below zero. That’s followed by 12 percent in France and 9 percent in Germany, both of which also have a significant amount of money-losing bonds.

Again, you may own this ETF, and others like it, in your 401(k) or retirement account without realizing it. It’s worth checking to make sure because even JPMorgan CEO Jamie Dimon, who once said he “would never buy a negative-rate bond,” did, in fact, buy not just one but a plethora, as the investment bank had a nearly-25 percent stake in Vanguard’s international bond ETF.

Record Municipal Bond Inflows

So where can fixed-income investors go for yield today? Even the long-term 30-year Treasury isn’t paying up. According to reports, the Treasury Department this week sold as much as $19 billion of 30-year bonds at a record-low 2.061 percent yield.

One of the most attractive sources of income right now is tax-free municipal bonds. Other investors have come to the same conclusion, as a record $105.5 billion flowed into muni bond funds in 2019, according to Morningstar. That’s significantly more than the previous record of $75 billion, set in 2009.

This raises the question of how to invest. As you can see in the chart above, investors are choosing to get access to muni bonds through actively managed mutual funds over passive vehicles such as ETFs. An incredible 90 percent of all muni inflows in 2019 went into mutual funds, the remaining flows going into ETFs.

Why the scramble for munis? As I’ve already pointed out, they may offer more attractive yields than some other options. And then there’s also the fact that they provide income that’s tax-free at the federal level and often the state and local levels. This feature no doubt appealed to many investors in high income tax states—including California, New York, New Jersey and others—who had their state and local tax (SALT) deductions capped at $10,000 starting last year, thanks to the Tax Cut and Jobs Act of 2017. And it isn’t just high-net-worth families who were affected.

Now that the law is in full effect, I expect demand for actively managed muni funds to stay high for the remainder of the year and beyond.

Still need help with your 2019 taxes? Check out our Tax Help Center by clicking here!

Gold Market

This week spot gold closed at $1,584.06, up $13.62 per ounce, or 0.87 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 1.12 percent. The S&P/TSX Venture Index came in off 0.64 percent. The U.S. Trade-Weighted Dollar rose 0.48 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Feb-13 | Germany CPI YoY | 1.7% | 1.7% | 1.7% |

| Feb-13 | CPI YoY | 2.4% | 2.5% | 2.3% |

| Feb-13 | Initial Jobless Claims | 210k | 205k | 203k |

| Feb-18 | Germany ZEW Survey Expectations | 21.0 | — | 26.7 |

| Feb-18 | Germany ZEW Survey Current Situation | -11.0 | — | -9.5 |

| Feb-19 | Housing Starts | 1400k | — | 1608k |

| Feb-19 | PPI Final Demand YoY | 1.6% | — | 1.3% |

| Feb-20 | Initial Jobless Claims | 210k | — | 202k |

| Feb-21 | Eurozone CPI Core YoY | 1.1% | — | 1.1% |

Strengths

- The best performing metal this week was palladium, up 4.91 percent as hedge funds cut their bullish positions to a 17-month low. January’s 22 percent slump in China’s car sales could dampen demand short-term. Federal Reserve Chairman Jerome Powell testified before Congress this week and commented that “low rates are not really a choice anymore, they are a fact of reality.” Powell suggested large-scale asset purchases may be the tool of choice to address an aggressive downturn. Gold advanced on Thursday after the announcement of a surge in the number of coronavirus cases in China. ETFs increased holdings for the 17th straight day on Friday with total gold held by ETFs up 2.3 percent this year already, according to Bloomberg data.

- Turkey’s gold reserves rose $778 million from the previous week to now total $28.3 billion as of February 7, according to data from the central bank. South Africa’s gold output rose the most in four years in December, according to Statistics South Africa data. Production unexpectedly rose by 24.9 percent from a year earlier, compared with 4.5 percent in November. Harmony Gold Mining bought AngloGold Ashanti’s last gold mine in South Africa for $300 million. This will make Harmony the largest South African gold miner and cements AngloGold’s withdrawal from the country.

- Gold Fields raised $252 million in a share sale to fund the initial construction of a new mine in Chile, reports Bloomberg. CEO Nick Holland says the company believes it has a fully funded project. Paramount Gold Nevada announced that Rachel Goldman has been appointed chief executive and director of the company.

Weaknesses

- The worst performing metal this week was platinum, down just 0.21 percent in a muted week of trading. Agnico Eagle Mines fell sharply on Friday after reducing its guidance for 2020 gold output due to slower-than-expected ramp up at new mines in northern Canada, reports Bloomberg. Production guidance was lowered to 1.88 million ounces, down from previous projections of 1.9 to 2 million ounces with the share price off 15.63 percent by the close. Agnico has been a sector favorite for a management team that could effectively execute and create value.

- Pretium Resources announced a big shakeup in company leadership this week with lowering of guidance. The board of directors is looking for a new president and CEO. Additionally, the vice president of geology and chief geologist resigned to pursue another opportunity. Pretium’s share price fell 24.39 percent for the week. New Gold reported revenue for the fourth quarter that missed even the lowest forecasts, reports Bloomberg. The company reported revenue of $139 million, down 12 percent year-over-year, and below the lowest estimate of $140 million.

- Barrick Gold CEO Mark Bristow said in an interview this week that the company has proposed a $200 million upfront tax payment to Papua New Guinea as a way to help secure a new contract for long-term mining rights in the country. Renault’s acting CEO Clotilde Delbos said during an earnings presentation this week that the company’s main concern is palladium’s skyrocketing price. Citigroup said in January that automakers have a big incentive to find a substitution for palladium in catalysts as the metal’s rally continues.

Opportunities

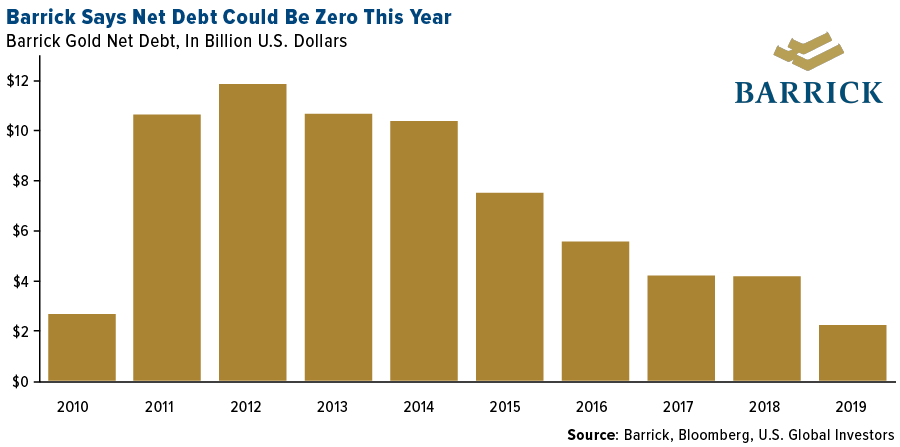

- Barrick Gold had a slate of good news this week. The company reported earnings per share that beat the highest estimate coming in at 17 cents per share. Barrick boosted its dividend by 40 percent to 7 cents per share. CEO Mark Bristow said that the company will exceed its two-year goal of selling $1.5 billion in assets by the end of 2020, reports Bloomberg. Due to asset sales, the world’s second-largest gold miner has the potential to reach zero net debt by the end of the year.

- The Russian government is looking at giving $1 billion in funding from the National Well-Being Fund to help develop the Arctic Palladium project in Siberia, reports Interfax. The project is a joint venture of Norilsk Nickel and Russia Platinum. This is part of Russia’s plan to be the world’s top platinum metals producer, reports Bloomberg. Russia’s biggest gold miner, Polyus PJSC, is focusing on smaller projects and cutting its debt ratio before starting work on Siberia’s Sukhoi Log deposit, which accounts for more than a quarter of Russian gold reserves.

- Sixth Wave Innovations, which developed disruptive molecular imprinted nanotechnology used for gold extraction, announced an agreement with Sumitomo Corporation that will greatly expand the company’s global distribution network, according to a press release. Metal Tiger is set to invest A$3.3 million into Southern Gold, an Australian and South Korean-focused gold explorer. Silver Viper announced strong drill results from its La Virginia Gold-Silver project in Mexico. High grade results provided in the press release include 196 grams per ton of gold and 984 grams per ton of silver over 0.5 meters.

Threats

- Due to severe power cuts, production by South African manufacturers fell the most in over five years in December. Statistics South Africa data shows that manufacturing output fell 5.9 percent from a year earlier. The country’s power cuts continue to hurt the economy with unemployment remaining at the highest level in at least 11 years. Harmony Gold fell after the gold producer reported first half results where production profit was 16 percent below the market estimate.

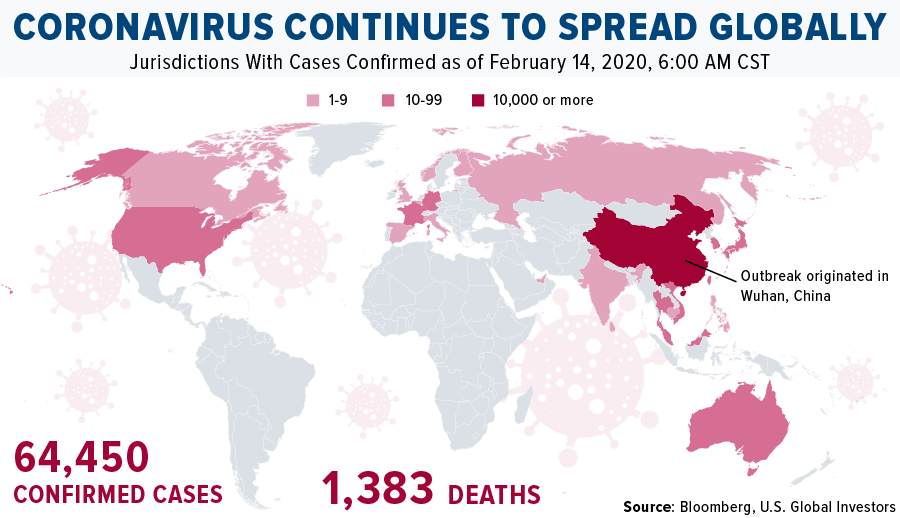

- The spread of the coronavirus continues to hit Chinese demand for jewelry. The death toll from the outbreak is now above 1,100 people and shoppers continue to stay at home as much as possible to avoid the virus. The economic impact from the global health emergency could very well send Chinese jewelry sales plummeting for the year.

- Citigroup said that it no longer has a price target for Petra Diamonds as the range of valuation outcomes for the company are too wide, reports Bloomberg. The bank downgraded the shares to neutral from buy and noted a 70 percent share price decline over 12 months.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 1.02 percent. The S&P 500 Stock Index rose 1.55 percent, while the Nasdaq Composite climbed 2.21 percent. The Russell 2000 small capitalization index gained 1.87 percent this week.

- The Hang Seng Composite gained 1.74 percent this week; while Taiwan was up 1.75 percent and the KOSPI rose 1.43 percent.

- The 10-year Treasury bond yield rose to 1.587 percent.

Domestic Equity Market

Strengths

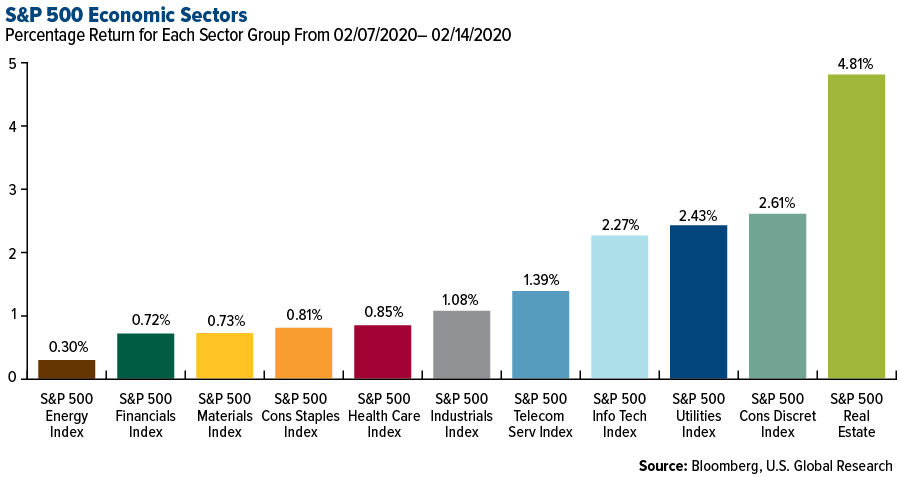

- Real estate was the best performing sector of the week, increasing by 4.81 percent versus an overall increase of 1.44 percent for the S&P 500.

- Nvidia was the best performing S&P 500 stock for the week, increasing 15.18 percent.

- Shares of mobile communications companies T-Mobile and Sprint jumped on Tuesday. T-Mobile stock was up 11 percent and shares and Sprint was up 72 percent following the news that a federal judge approved the giant merger.

Weaknesses

- Energy was the worst performing sector for the week, increasing by 0.30 percent versus an overall increase of 1.44 percent for the S&P 500.

- Under Armour was the worst performing S&P 500 stock for the week, falling 15.16 percent.

- Shares in the Japanese automaker Nissan fell almost 10 percent after it cut its annual profit forecast and ruled out a second-half dividend. The automaker is still reeling from the scandal surrounding former boss Carlos Ghosn and cut its operating profit forecast for this year by 43 percent after vehicle sales dropped.

Opportunities

- Apple added $18 billion in market value after its Chinese factories accelerated their post-coronavirus re-openings. Foxconn, which produces Apple’s iPhones and Airpods, hopes to resume 80 percent of all China production in March, according to Reuters.

- Credit Suisse posted its best profit since 2010. The Swiss bank reported a 69 percent rise in annual net profit, just days after CEO Tidjane Thiam quit over a spying scandal.

- Alibaba beat its quarterly revenue estimates. The Chinese online-shopping titan’s revenue rose 38 percent as its core e-commerce and cloud-computing businesses grew steadily.

Threats

- Angry Bird game maker Rovio saw a massive 96 percent drop in profits last quarter due to higher user acquisition costs.

- "I don’t like when investment bankers talk about EBITDA, which I call bulls— earnings," said Charlie Munger, known as Warren Buffett’s right-hand man, about Uber using the metric in its plan for becoming profitable by the end of the year.

- Google says the EU’s hardline antitrust punishments threaten internet innovation as it starts the first of three legal battles against $9 billion in EU fines.

The Economy and Bond Market

Strengths

- American consumers are increasingly optimistic about the economy despite the deadly coronavirus outbreak. The University of Michigan said its key measure of consumer sentiment jumped to 100.9 in early February from 99.8 a month earlier, near the peak of the expansion and the highest level since March 2018.

- The number of Americans who applied for unemployment benefits last week rose slightly from 203,000 to 205,000 versus expectations of 210,000. Claims remain relatively low, with no indication of major layoffs in the labor market, according to the latest data from the Labor Department.

- Retail sales rose 0.3 percent in January, a slight improvement over December, as unseasonably warm weather boosted sales at hardware stores and furniture stores. The Commerce Department said the expected January advance followed a 0.2 percent rise in sales in December.

Weaknesses

- Industrial output fell in January, driven down by unseasonably warm temperatures and weaker aircraft production at Boeing. Industrial production, a measure of factory, mining and utility output, decreased a seasonally adjusted 0.3 percent from the prior month, disappointing economists’ expectations.

- The U.S. economy is expected to expand by 1.4 percent in the first quarter of 2020, the Federal Reserve Bank of New York’s latest Nowcasting Report showed. “News from this week’s data decreased the nowcast for Q1 by 0.3 percentage point,” the NY Fed said in its publication. “Negative surprises from capacity utilization and industrial production data drove most of the decrease.”

- The junk bond market continues to deteriorate. Recoveries on defaulted loans are at their lowest levels in 30 years. This contrasts with high grade municipal bonds, where default rates remain extremely low due to their high quality and reliable cash flows.

Opportunities

- State and local governments are borrowing money for transportation projects at the fastest pace in a decade, pointing to a break in the austerity that gripped municipalities in the wake of the Great Recession. Cities and states sold $19.3 billion of bonds to raise new money for transportation projects in 2019, the most since 2010, when the post-recession Build America Bond program that provided federal subsidies was still in place. “Now that we’ve had persistent strong tax revenues for a few years, a number of states are doing things like raising their gasoline taxes and turning back to addressing capital investment in transportation infrastructure,” said Ted Hampton, a senior credit officer at Moody’s.

- The share of Americans in the labor force is the highest in nearly seven years — and the trend is led by younger women. Prime-age women 25 to 54 in the workforce is near a two-decade high, with the fastest increases among millennials and younger Gen Xers. Furthermore, 2.7 million women who weren’t in the labor force before January entered and found a job, compared with almost 2.2 million men who followed the same path, underscoring sustained demand for workers.

- Building permits are being issued at the highest rate since 2007, and housing starts in December climbed to 1.6 million units, the highest since December 2006.

Threats

- President Donald Trump’s budget proposal puts the debt held by the public at 81 percent of gross domestic product in 2021 and 66 percent in 2030. The latter goal would require a bipartisan effort, “which the lopsided nature of the deficit reduction proposed in this budget is not aimed to produce,” said Robert Bixby, executive director of the Concord Coalition, a nonprofit fiscal-advocacy group. The administration’s $4.8 trillion spending plan, released Monday, would push gross federal debt above $30 trillion over the next decade.

- The markets have used the SARS outbreak of 2003 as a guide for the impact of the coronavirus. While that epidemic resulted in a “V-shaped recovery,” the Chinese economy was growing at 10 percent to 11 percent back then, so a recovery was much easier to pull off. Today, the Chinese economy is much weaker, growing at 6 percent pre-virus, making a comeback more difficult.

- Next Friday, flash PMIs will be released and they could be a headwind for markets, especially if there is a global trend of worsening economic activity in February as a result of the coronavirus.

Energy and Natural Resources Market

Strengths

- The best performing major commodity for the week was coffee, which gained 10.80 percent as adverse weather conditions in Brazil, the largest supplier of coffee beans, may hurt crop yields. Oil is set for its biggest weekly gain in five months due to signs of the coronavirus outbreak slowing. Bloomberg reports that Chinese refiners are now buying cheap cargoes and taking traders by surprise. After weeks of production cuts, non-state owned refiners are now on a buying spree, taking advantage of a slump in prices, which is a positive sign that they are ready for an eventual rebound in demand

- Sugar is having its best start to the year in a decade with futures up 12 percent already in 2020, defying the hit that many commodities have taken due to the coronavirus. Sugar is surging largely due to a drought in Thailand, the world’s second largest exporter, which has forced crop slashing. Thai Sugar Millers Corp. reports that sugar output will likely fall 30 percent from last year.

- BP announced on Wednesday that it is pledging to offset the impact from the fuels they sell, following Shell and Equinor in making climate change a priority. The company has set a target to achieve net zero emissions from its oil and gas operations and to halve the emissions intensity of the products it sells by 2050. However, BP did not release details on how it will achieve the target. This puts growing pressure on American supermajors, such as Exxon Mobil and Chevron, to follow suit and also work toward greener practices.

Weaknesses

- The worst performing major commodity for the week was palm oil, which fell 5.44 percent as data showed India’s imports, the world’s largest buyer of palm oil, were off 20 percent in January. Commodities began to recover early in the week, but then fell again on Thursday when news broke that the number of coronavirus cases in China continues to rise by the thousands. According to the International Energy Agency, world oil consumption will fall in the first quarter for the first time in over a decade as the virus reduces economic activity and travel to China. The glut of oil not being delivered to China is forcing traders to store crude on tankers at sea. The virus is also impacting the shipping industry. According to the Baltic Exchange in London, capsize carriers that supply iron and coal to China are earning less than $2,600 a day, which is a fraction of what is needed to pay the crew and 93 percent below a 2019 peak. Bloomberg reports that BHP Group Ltd., the world’s top miner, is talking with Chinese customers about delaying shipments of copper concentrate due to the virus. Citigroup Inc. warned investors that the outbreak has “barely been priced into global commodity markets.”

- Bloomberg reports that President Trump was warned that the U.S. would struggle to produce the oil, gas and other energy products China committed to buy in the Phase One trade deal. The American Petroleum Institute (API) said last month in a meeting with the Energy Department that the deal calls for China to purchase an additional $52.4 billion in LNG, crude oil, refined products and coal over the next two years, which amounts to an additional 1 million barrels per day of crude, half a million barrels per day of refined products and 100 tankers of LNG. API said in its briefing that “even if production is available, logistical challenges remain with marine shipping and the Panama Canal.”

- Republican House leaders unveiled a plan to combat climate change, as the party begins to bow to demands that it address environmental issues. However, it has been called the “Green New Deal lite” and contains conservative principles of less regulation and an increase in domestic energy development, rather than mandated limits on greenhouse gas emissions or a carbon tax. Although it is positive news that Republican leaders are beginning to address environmental issues and they have some bipartisan support, it is a weakness that the measures likely won’t significantly combat the use of fossil fuels.

Opportunities

- Indonesia’s Energy and Mineral Resources minister announced that the government is proposing longer mine concessions for companies committed to building integrated upstream-to-downstream facilities. Bloomberg writes that Indonesia is revising its mining law to provide greater business certainty for investors. The country is one of the world’s top suppliers of nickel and coal and is trying to attract more companies to develop its resource base.

- Bill and Melinda Gates announced this week that fighting climate change and promoting gender equality will be prominent issues in their philanthropy going forward. Bloomberg writes that they are the co-founders of the world’s biggest private foundation. The foundation plans to work on technologies for lowering carbon emissions and on ways to help vulnerable populations like subsistence farmers adapt to climate change.

- Glencore announced a long-term supply agreement with Samsung SDI to supply 21,000 metric tons of cobalt contained in cobalt hydroxide between 2020 and 2024, reports Bloomberg. The company’s mining operations in the Democratic Republic of Congo will be independently audited each year to test compliance with supply-chain due-diligence standards to ensure ethical sourcing.

Threats

- Chemical companies are facing a massive plastic recycling challenge. Virgin plastic is created from crude oil and is closely linked to the global oil price, making it relatively cheaper than recycled plastic when oil prices fall. Jon Penrice, Asia-Pacific president of Dow Chemical Co., said in an interview that about 8 million tons of plastic goes into the ocean each year, which is “$100 billion worth of plastic, and that’s valuable for entrepreneurs.” According to BloombergNEF, Asia consumes nearly half of the world’s plastic packaging and global demand for recycled plastics is forecast to rise faster than supply.

- The global energy industry is suffering from the warmest winter in many years. According to Black Gold Investors chief investment officer Gary Ross, the loss in global oil demand due to mild temperatures is around 800,000 barrels a day. This past January was the hottest ever in Europe with surface temperatures 3.1 degrees Celsius warmer than average. The World Meteorological Organization says that global temperatures are already consistently breaking records, with 2016 the warmest ever followed by 2019. Warmer temperatures reduce demand for oil, gas and other fuels used to heat during the winter. According to the latest EPA inventory, Bloomberg reports that greenhouse gas emissions in the U.S. rose by 2.9 percent in 2018.

- Rystad Energy recently found that Permian Basin gas flaring is much worse than previously thought because initial research did not include gas-processing facilities. These facilities receive more gas than they can handle, so like oil producers at the wellhead, facilities burned off about 190 million cubic feet per day of gas in 2019. Bloomberg reports that this raises the total by 30 percent to roughly 810 million. Flaring is a controversial practice of burning natural gas into the air due to oversupply.

Emerging Europe

Strengths

- Greece was the best performing country this week, gaining 1.3 percent. The yield on 10-year bonds fell below 1 percent for the first time ever, allowing the country to borrow at lower rates than the U.S. government. Fitch upgraded the country’s ratings in January by one notch to a BB rating. S&P Global will conduct a review of Greece in April and Moody’s in May.

- The Russian ruble was the best relative performing currency this week, gaining 35 basis points. The ruble was supported by Russia’s positive real rates and rising oil prices. Russia lures carry traders as it offers a 3 percent real return on investments while other global markets have negative real rates. Brent crude oil gained 5.3 percent in the past five days.

- Industrials was the best performing sector among eastern European markets this week.

Weaknesses

- Turkey was the worst performing country this week, losing 1.1 basis points. Increased fighting in Northern Syria and geopolitical tension put pressure on equites trading on the Istanbul exchange. Banks underperformed as shares of Yapi Kredit declined by 7.7 percent and IsBankasi lost 6 percent.

- The Romanian leu was the worst performing currency in the region this week, losing 1 percent. Romania’s central bank lowered its inflation forecast and suggested an almost two-year freeze on interest rates is likely to be prolonged.

- Financials was the worst performing sector among eastern European markets this week.

Opportunities

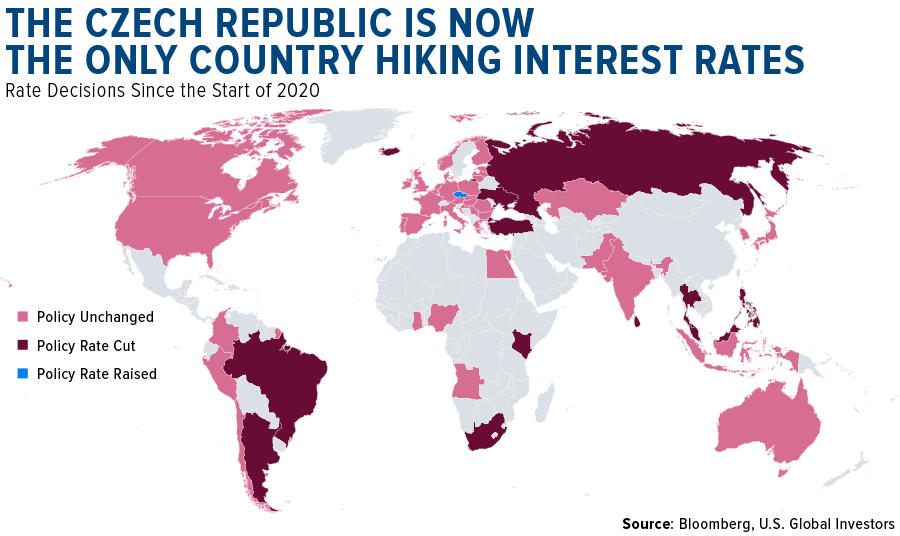

- Czech Republic, a tiny country located in Eastern Europe, has been hiking rates since June 2017, and according to the map below, it is the only country in the world with rising rates since the start of 2020. Kostas Tsigkourakos from Wood & Company commented that the country’s latest hike of 25 basis points on February 6 revealed monetary policymakers’ confidence in the domestic economy and Eurozone recovery. Rate hikes in the region should benefit the local banking sector.

- The central bank of Russia sold 50 percent plus 1 share of Sberbank to Welbeing Fund, securing a profit of around $63 billion. According to Bloomberg, about $14.3 billion from the sale will be used to finance social spending, as announced previously by President Putin. In addition to welfare programs, the new government plans to accelerate spending on a $400 billion infrastructure program. According to some estimates, extra spending could total as much as $34 billion this year.

- Despite global challenges and tensions, Turkish exports surged by 13 percent year-over-year in January, the highest level ever. Germany, Italy and the U.K. were the main recipients of Turkish exports. Record exports were possible due to the trade deal signed by the U.S. and China last month and weak lira. Additionally, optimism over a more predictable Brexit created more movement in European investments.

Threats

- Recent strength in the U.S. dollar has pushed the euro and other eastern European currencies lower. The euro to U.S. dollar exchange rate has slipped to its lowest level since 2017. Economic data for the Eurozone area weakened and with concerns over the effect of the coronavirus on global growth, the market is expecting some form of quantitative easing from the European Central Bank. Credit Suisse is predicting a 10 basis point interest rate cut in the second quarter of 2020.

- Inflation in Hungary spiked to 4.7 percent, which is well above the central bank’s tolerance band. Policymakers indicated they are ready to shift policy in order to bring inflation down from this seven-year high. Hungary has maintained one of the lowest real rates globally, and has used an array of unorthodox policy measures to boost lending and promote growth. The end of an easing cycle may halt GDP expansion.

- Eurozone industrial production fell by 2 percent in December. Germany, France, Italy and Spain all experienced a contraction in production that was larger than 2 percent. Eurozone GDP growth slowed to just 10 basis points in the fourth quarter of last year.

China Region

Strengths

- Hong Kong and Taiwan finished out the best in the region on the week, as the Hang Seng Composite (HSCI) and Taiwan Stock Exchange Index jumped 1.74 and 1.75 percent, respectively.

- Materials rose 4.71 percent for the week, the top-performing sector in the HSCI.

- You know what had a great showing this week? That’s right, you guessed it—it was Philippine exports: On a year-over-year basis, they rose 21.4 percent for the (most recent) December reading.

Weaknesses

- The Philippines’ PSE Composite Index declined by 2.98 percent for the week—the biggest loser, so to speak.

- Telecommunications was the worst-performing sector in the HSCI for the week, declining by 2.13 percent.

- In just the exact opposite way of Philippine exports having a great showing, here’s what didn’t: domestic vehicle sales in Vietnam, which, on a year-over-year basis for the January period, actually declined 52.2 percent, down from the prior decline of only 3.3 percent.

Opportunites

- Presidents Donald Trump and Xi Jinping reportedly spoke about the Wuhan coronavirus among other things in a telephone conversation this week, but one opportunity may perhaps lie in that the Phase One import levels by China of U.S. exports is supposedly still on.

- In keeping with the recent updates on the Korean Composite Stock Index (KOSPI) as a bit of a larger proxy for the region, note that it closed just over 1 percent off of its 52-week closing highs.

Threats

- Coronavirus confirmed case concerns continue.

- Reports grew this week that the fallout from the quarantine speedbumps in activity in China—especially Hubei province—may indeed slow some supply chains further or more than expected. And word has it, late on Friday, that Wuhan is actually clamping down further on quarantine restrictions even as cases reported ticked up significantly this week. Now, here’s where the threat lies and how it’s different from the one above it, generally speaking: Markets have been recovering somewhat from the initial shocks all this while, even as cases are still growing—presumably with a degree of expectation that stimulus is surely coming. And indeed, one has no doubt that it will, in various forms and around the world (see also: gold). But here’s one threat that’s different than just the actual concerns around the coronavirus and the manufacturing slowdown in China, etc.: What if forthcoming stimulus around the region is less timely or efficacious than expected? And so now the coronavirus concerns are now one thing, while the market’s anticipation and measure of responses to said concerns and admitted slowdowns are quite another. And if the responses are not sufficient, well, then we’d be left with two negatives, which of course might not exactly be a positive.

- The U.S. dollar continued its climb this week to new multi-month highs. Amid a degree of risk-off sentiment and virus concerns, it remains conceivable that could weigh on emerging markets at some point.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended February 14 was FuturoCoin, up 2,758.07 percent.

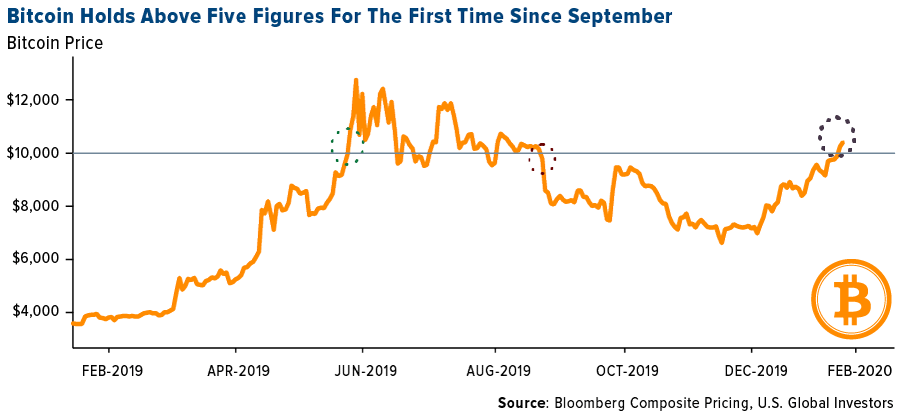

- Bitcoin appears to have decisively breached $10,000 for the first time since September, writes Bloomberg, and now traders are setting their sights on the next resistance level. On Wednesday, the longest surge for the digital coin since June brought it to as high as $10,481.

- As bitcoin surges more than 40 percent to $10,000 this year, it looks like so-called “zombie coins” – like Einsteinium and Kick that were written off long ago – are rallying, reports Bloomberg, and have even more than doubled since December. These alternative coins (or alt coins) are staying afloat and even flourishing thanks to hundreds of exchanges worldwide offering investors attractive terms to trade and capitalize on the renewal of risk taking in crypto, the article reads.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended February 14 was IFX24, down 79.75 percent.

- As the coronavirus disrupts economic activity in China, a key measure of competition among bitcoin miners has stagnated over the past two weeks, reports CoinDesk, after posting solid gains in the month of January. “Many miners have been phasing out older mining machines and buying new and more powerful models as we get closer to the halving,” Jason Wu, co-founder and CEO of DeFiner said. “The outbreak may have delayed the transition and contributed to the slow growth in mining difficulty.”

- IOTA Foundation, the nonprofit behind the IOTA distributed network, received multiple reports of fund theft and on Thursday advised users to close their Trinity wallets. CoinDesk reports that signs show it was a coordinated cyberattack that resulted in stolen funds.

Opportunities

- On Tuesday, Reuters reported that banking giant JPMorgan may be merging its blockchain project with an ethereum-focused software developer and investor known as ConsenSys. JPMorgan’s “Quorum” project was first reported in 2016, officially connecting the bank with ethereum, even if it was a private version of the tech, writes CoinDesk. In May 2019, however, staff at the bank suggested it might be spun off, though at the time it was uncertain. Quorum currently employs roughly 25 people globally, and it’s not yet clear if they would become part of ConsenSys’ team after the merger.

- On February 12 the crypto market achieved a new milestone by climbing above the $300 million market capitalization mark for the first time in six months, reports CoinTelegraph. A steady flow of funds is entering the space, showing interest in the sector continues to grow. Since the start of the new year, the crypto market cap has increased from $218.4 billion to $303.1 billion, the article continues. That is a 65.92 percent increase.

- Co-founder and CSO at blockchain and crypto analytics firm Chainalysis Jonathan Levin reiterated his stance to privacy in crypto, reports CoinTelegraph. Levin claims that full transparency of transactions might not turn out to be the best situation although in an interview with CoinTelegraph he did note that there is still a need to support the ability of regulators and businesses to monitor illicit activity related to cryptocurrency.

Threats

- According to an article this week in the Wall Street Journal, cryptocurrency scams took in over $4 billion in the year 2019. Ponzi schemes are the latest form of bitcoin fraud, the article explains, with big platforms like PlusToken drawing the most money. Seo Jin-ho, a travel-agency operator in South Korea, for example, says he invested around $86,258 in PlusToken. By June 2019, Chinese authorities concluded PlusToken was a scam.

- CEO of bitcoin media site Coin Ninja and founder of crypto wallet provider DropBit Larry Harmon, is facing federal charges related to his use of bitcoin privacy tools, writes CoinTelegraph. U.S. federal prosecutors are charging Harmon with conspiracy to launder money and operating a money transmitting business without a FinCEN license.

- In recent months, scammers have been impersonating CoinDesk reporters and editors, writes the news outlet this week, apparently promising coverage of projects in exchange for a fee. As the article makes clear, CoinDesk does not, and will never, accept payment for coverage. At least two different victims have paid hundreds of dollars in bitcoin and ether to these scammers.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| 10-Yr Treasury Bond | 1.59 | +0.00 | +0.19% |

| Oil Futures | 52.05 | +1.73 | +3.44% |

| Hang Seng Composite Index | 3,817.34 | +65.41 | +1.74% |

| S&P Basic Materials | 380.03 | +2.76 | +0.73% |

| Korean KOSPI Index | 2,243.59 | +31.64 | +1.43% |

| S&P Energy | 409.82 | +1.27 | +0.31% |

| Nasdaq | 9,731.18 | +210.66 | +2.21% |

| DJIA | 29,398.08 | +295.57 | +1.02% |

| Russell 2000 | 1,687.58 | +30.81 | +1.86% |

| S&P 500 | 3,380.16 | +52.45 | +1.58% |

| Gold Futures | 1,586.10 | +12.70 | +0.81% |

| XAU | 102.01 | +0.68 | +0.67% |

| S&P/TSX VENTURE COMP IDX | 570.49 | -3.67 | -0.64% |

| S&P/TSX Global Gold Index | 260.24 | +2.62 | +1.02% |

| Natural Gas Futures | 1.84 | -0.01 | -0.75% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Korean KOSPI Index | 2,243.59 | +12.61 | +0.57% |

| 10-Yr Treasury Bond | 1.59 | -0.20 | -11.04% |

| Gold Futures | 1,586.10 | +26.00 | +1.67% |

| S&P Basic Materials | 380.03 | +0.10 | +0.03% |

| S&P 500 | 3,380.16 | +90.87 | +2.76% |

| DJIA | 29,398.08 | +367.86 | +1.27% |

| Nasdaq | 9,731.18 | +472.48 | +5.10% |

| Oil Futures | 52.05 | -5.76 | -9.96% |

| Hang Seng Composite Index | 3,817.34 | -122.01 | -3.10% |

| S&P/TSX Global Gold Index | 260.24 | +3.02 | +1.17% |

| XAU | 102.01 | -1.39 | -1.34% |

| Russell 2000 | 1,687.58 | +5.19 | +0.31% |

| S&P Energy | 409.82 | -41.39 | -9.17% |

| S&P/TSX VENTURE COMP IDX | 570.49 | -6.52 | -1.13% |

| Natural Gas Futures | 1.84 | -0.28 | -13.02% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| XAU | 102.01 | +8.07 | +8.59% |

| S&P/TSX Global Gold Index | 260.24 | +18.48 | +7.64% |

| Gold Futures | 1,586.10 | +100.50 | +6.76% |

| DJIA | 29,398.08 | +1,616.12 | +5.82% |

| S&P 500 | 3,380.16 | +283.53 | +9.16% |

| Nasdaq | 9,731.18 | +1,252.16 | +14.77% |

| Korean KOSPI Index | 2,243.59 | +104.36 | +4.88% |

| Natural Gas Futures | 1.84 | -0.80 | -30.34% |

| S&P Basic Materials | 380.03 | +1.43 | +0.38% |

| Russell 2000 | 1,687.58 | +98.79 | +6.22% |

| Oil Futures | 52.05 | -4.72 | -8.31% |

| Hang Seng Composite Index | 3,817.34 | +243.59 | +6.82% |

| S&P/TSX VENTURE COMP IDX | 570.49 | +43.34 | +8.22% |

| S&P Energy | 409.82 | -27.68 | -6.33% |

| 10-Yr Treasury Bond | 1.59 | -0.23 | -12.80% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (12/31/2019):

Sberbank of Russia PJSC

Royal Dutch Shell PLC

Equinor ASA

BHP Group Ltd

Gold Fields Ltd

Agnico Eagle Mines Ltd

New Gold Inc

MMC Norilsk Nickel PJSC

Polyus PJSC

Sixth Wave Innovations Inc

Southern Gold Ltd

Silver Viper Minerals Corp

Harmony Gold Mining Co Ltd

AngloGold Ashanti Ltd

Boeing/The Co

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

EBITDA, or earnings before interest, taxes, depreciation, and amortization, is a measure of a company’s overall financial performance and is used as an alternative to simple earnings or net income in some circumstances. The University of Michigan Confidence Index is a survey of consumer confidence conducted by the University of Michigan. The report, released on the tenth of each month, gives a snapshot of whether or not consumers are willing to spend money. The FTSE TWSE Taiwan Index Series is a joint venture between the Taiwan Stock Exchange Corporation (TWSE) and FTSE Group (FTSE) to provide market participants with a range of tools to gain exposure to the Taiwanese market. The PSE Composite Index, commonly known previously as the PHISIX and presently as the PSEi, is a stock market index of the Philippine Stock Exchange consisting of 30 companies. The Korean Composite Stock Price Index (KOSPI) is the main tracking index in South Korea.