Will 2019 Be the Year of King Copper?

Date Posted: February 15, 2019

Read time: 58 min

Because of its wide availability and exceptional conductivity, copper is found in everything from consumer products to automobiles to semiconductors.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

Summary

- Corporate purchasing of copper-gobbling renewable energy more than doubled from 2017 to 2018.

- Sales of electric vehicles, which use three to four times the amount of copper as traditional vehicles, are booming in China.

- Copper miners get upgraded by the big banks.

Because of its wide availability and exceptional conductivity, copper is found in everything from consumer products to automobiles to semiconductors. Last year global demand for the red metal stood at 23.6 million tons, and by 2027, it’s projected to reach just under 30 million tons, representing an average annual growth rate of about 2.6 percent.

This phenomenal growth is attributable not just to the rise of middle class consumers. It’s also thanks to our steady rotation into clean, renewable energy such as wind and solar—which is good news for copper demand going forward.

As I’ve shared with you before, renewables require many more times the amount of copper as traditional energy sources. A typical wind farm—those that blanket whole areas of West Texas, California and some other states—can contain as much as 15 million tons of the metal.

2018 Was a Record-Breaking Year for Renewables

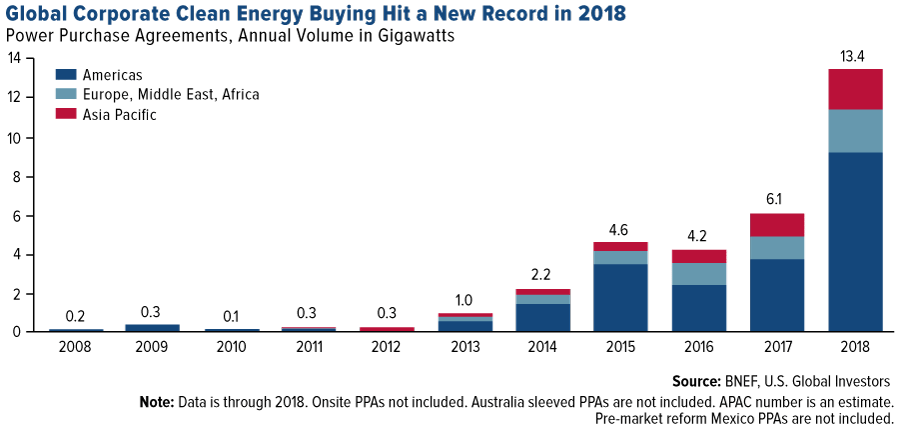

Whether you’re a believer in renewable energy or not, the tipping point may have already occurred. Among the fastest growing jobs in the U.S. right now are wind turbine service technician and solar panel installer, for whatever that’s worth. And according to a report by Bloomberg New Energy Finance (BNEF), corporate purchasing of renewable energy more than doubled from 2017 to 2018. Globally, companies bought 13.4 gigawatts (GW) last year, compared to the previous record of 6.1 gigawatts in 2017. Over 63 percent of the purchasing activity occurred right here in the U.S. Facebook alone was responsible for consuming 2.6 GW of renewables, three times as much as the next biggest corporate energy buyer, AT&T.

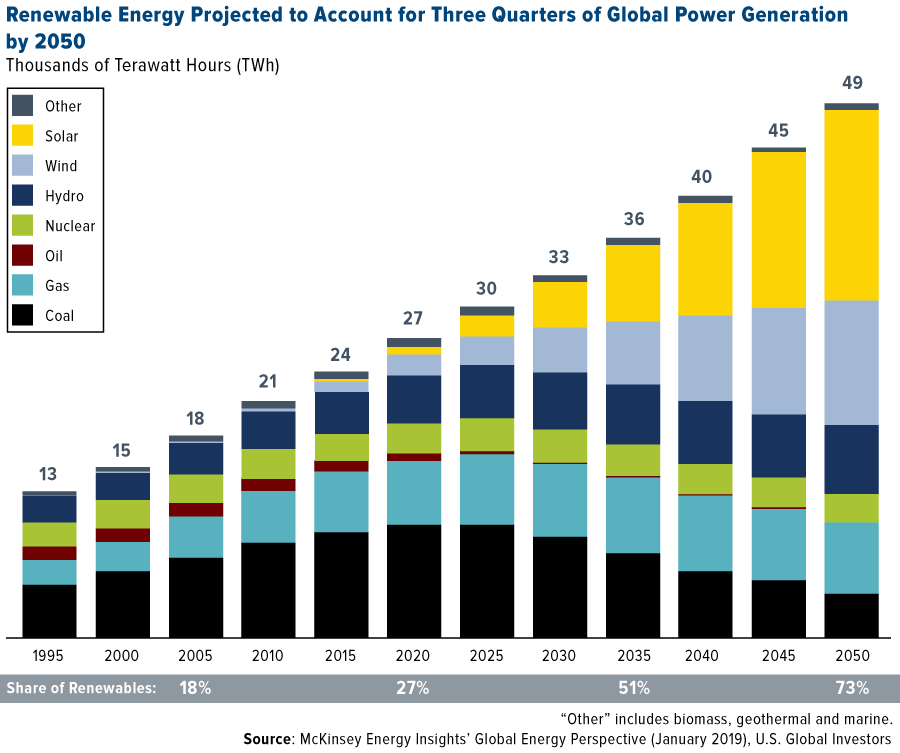

The trend toward renewables is expected to accelerate at a white-knuckle pace for years to come. Take a look at the chart below, courtesy of McKinsey’s “Global Energy Perspective 2019.” Analysts believe that, by 2035, renewable energy will account for more than half of all power generation as its price falls below that of coal and gas-generated energy. Fifteen years after that, nearly three quarters of total energy consumed around the world will be derived from renewable means, chiefly wind and solar.

If this is compelling at all to you, now might be an excellent time to start participating. One of the best ways, I believe, is with exposure to high-quality, well-managed copper miners as well as funds that have a large position in copper mining.

China Will Lead the Transition from Internal Combustion Engines to Electric Cars

And we haven’t even mentioned electric vehicles (EVs), which are notorious copper gobblers. As I’ve shared with you before, EVs consume between three and four times the amount of copper as traditional internal combustion engines.

China is leading the world in EV adoption and will likely continue to do so for some time. In the fourth quarter of last year, China was responsible for 60 percent of global EV sales, according to Bloomberg, which adds that the country holds half of all vehicle-charging infrastructure. By the end of last year, electric cars made up about 7 percent of total new vehicle sales in China, with a compound growth rate of 118 percent since 2011. In about a decade, the Asian country will account for nearly 40 percent of the global EV market, followed by Europe (26 percent) and the U.S. (20 percent), according to BNEF.

Not only does China have national subsidies in place, but its carmakers are also incentivized to manufacture EVs thanks to the country’s “New Energy Vehicle” credit system. The system acts as an EV quota, requiring carmakers to generate credits through the sale of electric cars. According to BNEF, this is the “single most important piece of EV policy globally and is shaping automakers’ electrification plans.”

Adding to this acceleration is the fact that China has elevated the adoption of new “Phase 6” emissions standards under its anti-pollution “Blue Sky Defense” action plan. Just as we’re seeing in parts of Europe right now, China will soon begin banning the production of the most polluting diesel engines.

Many cities in China see the writing on the wall and have already enacted restrictions on gasoline-powered vehicle sales. In 2018, Shenzhen and Shanghai collectively led the world with more than 165,000 EV sales. That’s more than Norway and Germany combined.

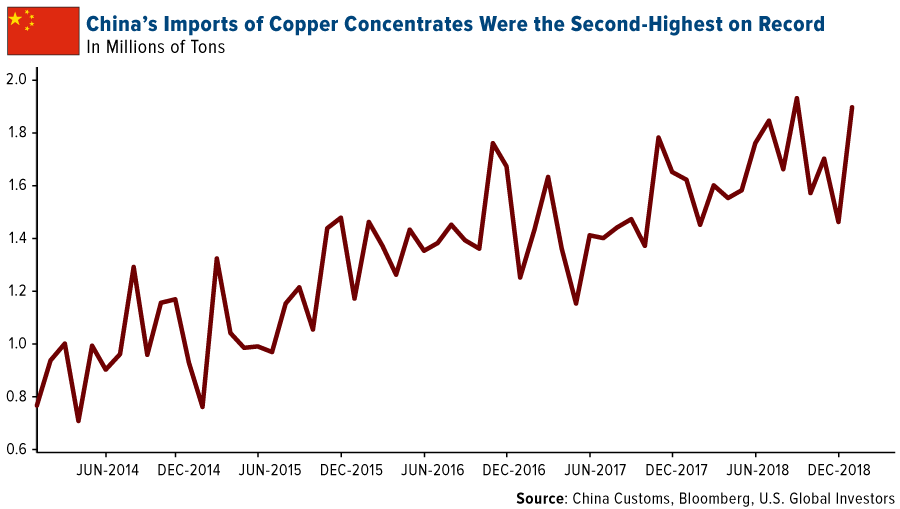

With demand for EVs so high, it’s little wonder that China’s copper imports climbed to 479,000 tonnes in January, the second-highest on record.

Morgan Stanley Bullish on Copper, Upgrades Freeport-McMoRan

All of this leads me to believe that 2019 could be not only copper’s year but also copper miners’ year. The price of the red metal is up about 6 percent so far in 2019, trading at close to $2.80 a pound. That’s about 67 percent short of the metal’s all-time high of $4.62, set in February 2011.

This week Morgan Stanley joined Citi and Goldman Sachs in making a bullish call on the metal. The investment bank projected a 14 percent upside for copper in 2019, based on a widening supply deficit and the likelihood of a resolution to the U.S.-China trade spat.

As for copper miners, Morgan Stanley upgraded Freeport-McMoRan, while Goldman Sachs recently upgraded Rio Tinto. Piyush Sood, lead analyst at Morgan Stanley, said in a note that Freeport’s “earnings sensitivity to copper is still the highest among its peers, and combined with its high trading liquidity, we believe it will emerge as the go-to large-cap stock for exposure to a copper price rally.” Shares of the Phoenix-based company’s stock jumped nearly 7 percent on the news this Wednesday.

Singapore-based DBS Bank also sees a copper shortage over the mid-term. Analysts expect supply to be in a deficit each year between now and at least 2022, when it could be at its widest since 2004.

“Copper is king for this electrification trend taking over the global economy,” Matt Gilli, CEO of Nevada Copper, told Reuters. “We see demand increasing steadily in the years ahead and, so far, supply is not keeping up.”

To meet surging demand, four U.S. copper projects are set to open by next year, the first to do so in decades, according to Reuters. And Ivanhoe Mines, founded by my friend Robert Friedland, is in the process of developing the Kamoa-Kakula copper deposit in the Democratic Republic of Congo, which Robert describes as the second-largest copper mine in the world.

“You’re going to need a telescope to see copper prices in 2021,” Robert told us when he visited our office last year.

Enjoyed what you read? Get more research and insights by subscribing to my FREE, award-winning Frank Talk CEO blog!

Gold Market

This week spot gold closed at $1,321.55, up $7.05 per ounce, or 0.54 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 0.23 percent. The S&P/TSX Venture Index came in up 0.65 percent. The U.S. Trade-Weighted Dollar rose slightly, gaining just 0.28 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Feb-13 | CPI YoY | 1.5% | 1.6% | 1.9% |

| Feb-14 | PPI Final Demand YoY | 2.1% | 2.0% | 2.5% |

| Feb-14 | Initial Jobless Claims | 225k | 239k | 235k |

| Feb-19 | Germany ZEW Survey Current Situation | 22.5 | — | 27.6 |

| Feb-19 | Germany ZEW Survey Expectations | -13.0 | — | -15.0 |

| Feb-21 | Germany CPI YoY | 1.4% | — | 1.4% |

| Feb-21 | Initial Jobless Claims | 229k | — | 239k |

| Feb-21 | Durable Goods Orders | 1.7% | — | 0.7% |

| Feb-22 | Eurozone CPI Core YoY | 1.1% | — | 1.1% |

Strengths

- The best performing metal this week was palladium, up 2.05 percent on a strong market outlook. Gold traders and analysts were split between bullish and bearish this week as gold struggles to get back up to highs seen in January, according to the weekly Bloomberg survey. However, the yellow metal remarkably gained this week even as both the U.S. dollar and equities rose on the news that U.S.-China trade talks would resume next week. Despite local prices in India trading near the highest levels in more than five years, gold imports to the world’s second largest consumer of gold rose in January, reports Bloomberg. Inbound shipments rose 64 percent last month from a year earlier to 46 tons. Gold futures 60-day volatility is at its lowest since 1997 as investors await the results of trade negotiations. Low volatility has historically been a sign of steady buying in the metal.

- China, the number one consumer of gold, added to its gold reserves for the second month in a row after a two-year dry spell. The People’s Bank of China increased its holdings to 59.94 million ounces in January, up from 59.56 in December. Russia’s gold output in 2018 rose 2.5 percent year-over-year to 314.42 tons, while silver production grew 7.2 percent to 1,119.95 tons. Russia is also taking steps to make gold investing accessible to more people. According to Bloomberg, the government is considering opening the precious metals market participation by allowing retail investors to buy bullion for their individual investment accounts.

- Agnico Eagle Mines Ltd. is forecasting record gold output as it brings two major projects in Canada into production, reports Bloomberg. CEO Sean Boyd said on Thursday in an interview that they will announce a 14 percent dividend hike, which could be even higher even if gold prices stay flat. Evolution Mining’s executive chairman Jake Klein says that the gold sector is ready for more consolidation. Klein said “we believe that the mid-tier space is the space that delivers the best return.” Harmony Gold Mining Co. Ltd’s metal output rose by 34 percent due to a new mine in Papua New Guinea and a South African project, reports Bloomberg. The company’s output rose to 751,008 in the six months to December and its free cash flow generation rose 100 percent to 1.1 billion rand.

Weaknesses

- The worst performing metal this week was silver, down 0.32 percent as new hedge funds cut bullish positions in late January. Turkey’s gold reserves fell $119 million from the previous week, according to official weekly figures from the central bank in Ankara. In Italy, the country’s populists have called on lawmakers to pass legislation allowing the government to take control over the central bank’s gold reserves, reports Bloomberg. Luckily the market has seemed to shrug off any speculation of reserve sales to fund the country’s budget. “My bill only aims at making clear that the gold belongs to the state, not to the government,” euro-skeptic lawmaker Claudio Borghi of the League said in a phone interview.

- Amid financial turmoil and the government shutdown, U.S. retail sales unexpectedly fell in December, reports Bloomberg, posting the worst drop in nine years. The value of overall sales fell 1.2 percent, missing all economist estimates in a Bloomberg survey that called for a 0.1 percent gain. This sign of slowing economic momentum boosted the haven demand for gold, sending the yellow metal higher after the announcement. Concerns from gold bulls that the Federal Reserve may hike U.S. interest rates this year were eased on the news.

- The U.S. solar job market lost around 8,000 jobs in 2018 as uncertainty surrounding President Trump’s tariffs took a toll on planned projects, reports Bloomberg. This likely lowered the demand for solar panels which contain silver. The good news is the Solar Foundation does expect project employment growth to resume in 2019, with the number of jobs increasing by 7 percent, the article continues.

Opportunities

- According to the leading maker of auto catalysts, Johnson Matthey, the palladium deficit is set to widen “dramatically” in 2019. The company wrote in a report that “our figures suggest that the market moved closer to balance, but the underlying structural deficit continues to grow.” Platinum holdings in ETFs rose to the highest level since 2015 as investors bet on better performance of the precious metal. After prices fell 19 percent in the past year, many analysts believe platinum to be undervalued relative to other precious metals.

- The investment case for copper, the red metal, is on the rise due to supply shortage. Morgan Stanley writes that after significant outperformance last year, supply disruption has returned to several mines and years of low capital expenditure means a dearth of new production is entering the market this year. However, demand has only continued to rise, largely in part due to China’s push for electric vehicles, and a big deficit could emerge.

- Newcrest Mining Co. is on the watch for smaller, tier-two assets to add to its portfolio. CEO Sandeep Biswas said in an interview with Bloomberg TV that the company is “scanning the market all the time” and that “a lot of tier-two assets, once you get in there, can be turned into tier-one assets.” Newcrest, Australia’s largest producer, wishes to have exposure to between two and four tier-two assets within the next 10 years. Pure Gold Mining Inc. announced the results of a feasibility study at its Madsen Gold Projects in the Red Lake mining district of Ontario. One highlight of the study is that it has a low initial capital requirement of $95 million including a 9 percent contingency. Paradigm Capital published a report noting that Freegold Ventures Ltd. is the most overlooked developer or explorer with remarkable exploration and torque.

Threats

- Barrick Gold Corp. said this week that its costs to produce gold will be at least 7.9 percent higher this year following its mega-merger with Randgold Resources Ltd. The company reported an all-in sustaining costs forecast of $870 to $920 per ounce, which is much higher than its forecast of $806 per ounce in 2018 pre-merger. Bloomberg writes that the company’s main project, the Veladero project in Argentina, isn’t performing like a tier-one asset. Barrick’s CEO did say that there is “plenty of interest” from other players in the space to buy some of their assets. Jefferies gave a recommendation of hold for the stock while TD Securities and Deutsche Bank downgraded it to hold from a buy.

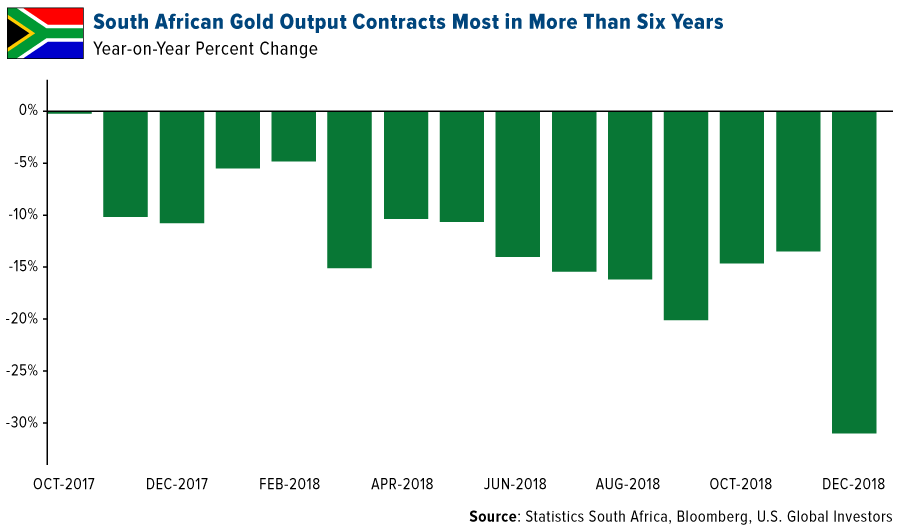

- South African gold output fell the most in six years, with production declining 31 percent from a year earlier, according to Statistics South Africa. The drop in December marks the 15th straight month of declines. Don’t forget – the nation used to be the world’s top miner of the yellow metal by a wide margin. Sibanye Gold Ltd., one of the top miners in the South Africa, said this week that it was considering shutting down unprofitable shafts and cutting jobs at its local operations. This could lead to more than 6,000 job losses.

- New Gold’s adjusted loss per share for the fourth quarter came in wider than expected. The share price fell almost 27 percent for the week. Renaud Adams, the new CEO of New Gold, joined the company last year and had positive initial news to report at the start of the year, sending the share price up around 50 percent. Sustaining those gains, however, was going to be difficult. Mr. Adams is highly respected from his prior leadership at Richmont Mines which was taken over by Alamos Gold. However New Gold gets sorted out, whether by fixing the asset or selling it, Mr. Adams will surely walk away much richer as the board at New Gold was dealing from a weak position.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 3.09 percent. The S&P 500 Stock Index rose 2.50, while the Nasdaq Composite climbed 2.39 percent. The Russell 2000 small capitalization index gained 4.17 percent this week.

- The Hang Seng Composite gained 0.02 percent this week; while Taiwan was up 1.33 percent and the KOSPI rose 0.87 percent.

- The 10-year Treasury bond yield rose 2.8 basis points to 2.66 percent.

Domestic Equity Market

Strengths

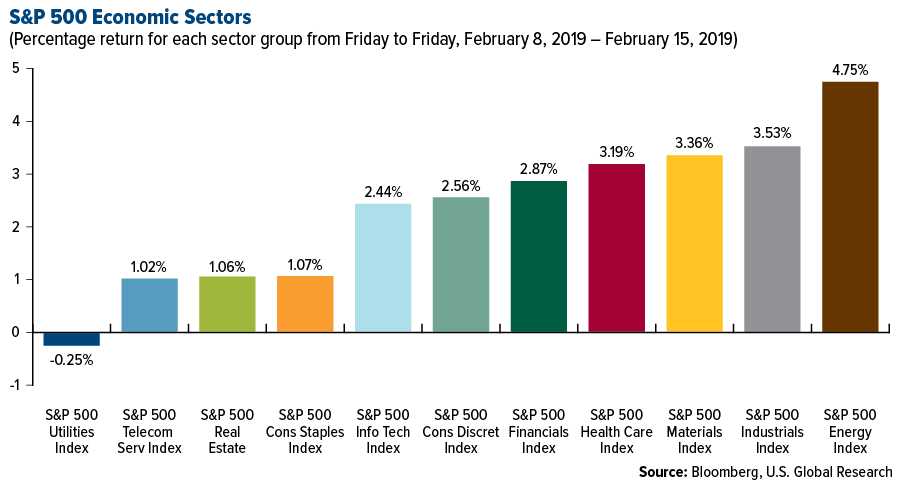

- Energy was the best performing sector of the week, increasing 4.75 percent compared to an overall increase of 2.43 percent for the S&P 500.

- Brighthouse Financial was the best performing stock for the week, increasing 18.94 percent.

- Cisco Systems on Wednesday reported second-quarter profits that beat Wall Street estimates. The company’s quarterly sales were in line with forecasts. Cisco also provided relatively bullish outlooks for profit and revenue in the coming quarter.

Weaknesses

- Utilities was the worst performing sector for the week, decreasing 0.25 percent compared to an overall increase of 2.43 percent for the S&P 500.

- Newell Brands was the worst performing stock for the week, falling 16.66 percent.

- Shares of Newell Brands tanked on Friday after the household products maker posted another disappointing round of results in its fourth-quarter earnings report. Sales slipped, and the company offered weak guidance in 2019. Consequently, the stock fell as much as 19 percent.

Opportunities

- Thanks to server sales, shares of Nvidia rallied in the extended session Thursday after the chipmaker topped Wall Street’s lowered earnings expectations for the quarter. It’s predicted that revenue will stay flat or fall slightly this year — better than analysts were forecasting.

- Nintendo detailed its heavy-hitting lineup of Switch games coming in 2019. The company showed off more than two dozen upcoming Switch games during a 36-minute "Nintendo Direct" presentation.

- Investors with $515 billion in assets under management are hoarding the most cash since the Great Recession 10 years ago, according to Bank of America Merrill Lynch. This rotation, combined with their withdrawal from the stock market, might suggest to some that sentiment is bearish. However, Bank of America’s investment strategists see the data differently. They see the development as a contrarian signal and are actually bullish on the stock market.

Threats

- Deere & Co. reported fiscal first-quarter earnings early Friday that fell well short of Wall Street estimates. "Tariffs and trade policies," Deere said, "have weighed on market sentiment and caused farmers to become more cautious about making major purchases." Trump tariffs have also raised materials costs for the farm equipment giant.

- Facebook is reportedly considering paying a record multibillion dollar fine to settle the Federal Trade Commission’s (FTC) investigation into its privacy practices. The FTC has been investigating whether the leak of data on Facebook users to Cambridge Analytica violated a previous agreement between the agency and the social network.

- In a sweeping new report on the state of venture capital, Goldman Sachs analysts revealed new findings about the performance of private and public markets. The firm found that over the last two years the biggest newly public companies would have created more value for themselves by staying private because the actual value they’ve earned in the public market has significantly lagged. In other words, it may have paid to stay private between 2017 and 2018. This dynamic is historically unusual, underscoring both a broader trend in companies staying private longer, and the importance of monitoring how this year’s slate of initial public offerings (IPO) performs. Indeed, this shift has only occurred twice in the past 25 years, both at vexing times for U.S. markets — once before the dotcom bubble burst and once before the financial crisis, the analysts said.

The Economy and Bond Market

Strengths

- U.S. consumer sentiment rebounded by more than forecast from a two-year low, suggesting recent weak retail sales will be a temporary blip after the government shutdown ended and the Federal Reserve signaled it would hold off on interest-rate hikes. The University of Michigan’s preliminary February sentiment index rose to 95.5, exceeding the median forecast in a Bloomberg survey for an increase to 93.7.

- The Empire State Manufacturing Survey rebounded in February to beat the consensus forecast, as both the general and expectations gauges indicate solid growth. The headline general business conditions index doubled from the month prior, rising 5 points to 8.8. The new orders index rose 4 points to 7.5.

- President Trump on Friday signed a spending package to avert another government shutdown. White House press secretary Sarah Huckabee Sanders told reporters that Trump approved the measure on Friday afternoon in the executive mansion.

Weaknesses

- U.S. retail sales collapsed by the most since 2009 in the month of December. Sales sank 1.2 percent to $505.8 billion, the Commerce Department said, raising suspicion among some economists that the data would eventually be revised higher.

- A record 7 million Americans have stopped paying their car loans. Most of the Americans who have recently fallen behind on their car payments have low credit scores or are younger than 30 years old.

- The number of Americans filing applications for unemployment benefits unexpectedly rose last week, pushing the four-week moving average of claims to its highest level in just over a year, suggesting some moderation in job growth. Initial claims for state unemployment benefits increased 4,000 to a seasonally adjusted 239,000 for the week ended February 9, the Labor Department said on Thursday.

Opportunities

- Investors are optimistic that progress was made during this week’s trade talks between the U.S. and China in Beijing, which are set to continue in Washington next week. Market participants appear to be hoping the two sides can come to an agreement before a March 1 deadline when tariffs on certain imported Chinese goods are set to increase from 10 percent to 25 percent.

- U.S. durable goods orders, released next Thursday, are forecast to have risen by 1.7 percent month-on-month in December, adding to the 0.7 percent gain made in November.

- Next Thursday’s release of February’s preliminary Markit U.S. Manufacturing PMI is forecast to remain in line with the previous reading.

Threats

- Chinese imports from the U.S. declined 41.1 percent in January, a record decline and the fifth straight month of contraction, according to trade data released by the customs administration. The slump partly reflects the impact of higher tariffs on U.S. goods in the course of the past year’s trade war.

- American household debt hit a new record high. Overall debt rose by $32 billion to $13.5 trillion in the fourth quarter, the Federal Reserve Bank of New York said in a report out Tuesday.

- With retail sales disappointing this week, investors will be looking at next Thursday’s release of the Leading Index for clues as to the future of the economy. While still positive, growth has been decelerating.

Energy and Natural Resources Market

Strengths

- The best performing major commodity for the week was WTI crude oil, which gained 5.69 percent, on news of production cuts. Copper advanced for a second day in a row on Thursday after a surprising gain in China’s import and export data of the metal, reports Bloomberg. China’s imports of copper concentrates were the second highest on record at 479,000 tons for the month. This is a positive signal for demand, as China is the world’s top consumer of the metal. According to Capital Economics Ltd., copper will rise more than 60 percent to around $10,000 per ton by the year 2025 due to constrained supply growth and massive demand from electric vehicles.

- The Senate could soon be voting on the Green New Deal announced last week in order to get a feel for support of the measures designed to combat climate change. Although there is disagreement between parties on the feasibility need for green initiatives, what do investors think about it? Stephen Liberatore, managing director at asset manager Nuveen, says that “Wall Street would take this seriously” because there are “more and more investors who are interested in having exposure to green projects and green debt.” According to the Forum for Sustainable and Responsible Investment, sustainable investing is a $12 trillion market in the U.S. and data from BloombergNEF shows that global issuance of green bonds rose to $600 billion in 2018.

- OPEC reduced its estimate for the amount of crude oil that the world needs to produce this year on the news that U.S. production continues to grow, reports Bloomberg. OPEC, which produces 40 percent of the world’s oil, curbed output by the most in two years last month. Oil is headed for its biggest weekly gain in a month on the heels of OPEC cuts and increasingly positive trade talks between the U.S. and China, says Bloomberg. Futures in New York rose by 0.9 percent Friday morning. Eni SpA, one of Italy’s major oil producers, reported fourth quarter results that beat estimates, with cash from operations rising 32 percent.

Weaknesses

- The worst performing major commodity for the week was coffee, which fell 4.53 percent as bumper crops continue to weigh on the market. State-run Kuwait Petroleum Corp. is re-evaluating its plan to spend $500 billion on capital projects until 2040, reports Bloomberg. The decision was made due to lower oil prices and Kuwait’s reduced output under the OPEC deal to produce less crude. The company might also decide this year to combine its eight business units into just four in order to streamline operations. PDC Energy Inc. is another oil and natural gas driller to release a 2019 spending plan below forecasts. PDC announced spending of $810 million to $870 million, which is down $150 million from last year and below the median forecast of $952.5 million.

- Bloomberg writes that the U.S.-China trade war has caused a $1 billion burn for the U.S. ethanol industry. Ethanol makers Green Plains Inc. and Archer-Daniels-Midland Co. both reported fourth quarter earnings that were below forecasts, while Valero Energy Corp said its ethanol unit had a $27 million operating loss. Since China has a 70 percent tariff on American supplies of biofuel and they’re a big consumer, profit margins have shrunk in turning corn into biofuel. Green Plains’ CEO Todd Becker says that the industry “is in a cash-burn situation.”

- The Bloomberg Industrial Metals Subindex, which tracks aluminum, copper, nickel and zinc prices, fell for eight straight days through Thursday for the longest slide since June 2017. This comes after the index posted its best month in more than a year in January. Bloomberg’s Marvin Perez writes that weaker-than-expected U.S. economic data released on Thursday coupled with demand concerns due to the U.S.-China trade war dimmed prospects for global growth.

Opportunities

- Cheniere Energy Inc. is in discussions with potential buyers of its LNG from terminals that may be built in Germany. Europe has been emerging as a hotspot for natural gas since late 2018 when mild weather sent prices falling in Asia. Lower prices made it more expensive to ship the fuel all the way to Asia, and since Europe has the capacity, it became a “natural home” for the extra volumes, writes Bloomberg. Wayne Gordon, an executive director at UBS Group AG’s wealth management unit, told Bloomberg TV in an interview this week that they now expect a 30 million ton iron ore deficit due to the Vale Brazil dam crisis. This is in contrast with expectations of a 20 million ton surplus at the beginning of the year. Gordon also said that iron ore, steel production in China is expected to rise around 1 to 2 percent in 2019.

- Bloomberg reports that Dubai is looking for partners to build its first solar-powered desalination plant in effort to diversify away from using fossil fuels to build its water supply. The Dubai Electricity and Water Authority says that the plant will have capacity to produce 120 million gallons a day of drinkable water by 2024. Shell is taking a big step to enter the household battery market. Bloomberg reports that Shell agreed to acquire 100 percent of Sonnen, a Bavarian-based home battery provider. Executive Vice President of New Energies at Shell Mark Gainsborough said that “full ownership of Sonnen will allow us to offer more choices to customers seeking reliable, affordable and cleaner energy.”

- Goldman Sachs forecasts that Brent crude oil will reach $67.50 per barrel in the second quarter of this year, driven by strong demand and supply cuts by OPEC, reports Bloomberg. Russia has already curbed output by 140,000 barrels per day. The nation’s energy minister said this week that the average February level should be at least 150,000 barrels lower than in December. Bloomberg reports that Berkshire Hathaway Inc. is moving into the Canadian energy industry by purchasing 10.8 million shares of oil-sands producer Suncor Energy Inc., valued at $300.9 million.

Threats

- According to the International Energy Agency (IEA), the crisis in Venezuela risks disrupting global crude markets because the heavy, high-sulfur crude it produces is becoming increasingly scarce. Not only is Venezuela producing less oil, but other countries are as well, due to an agreement with OPEC to cut supply in order to prevent a surplus. IEA wrote in its monthly report that crude oil “quality is another issue, and, in the context of supply in the early part of 2019, it is even more important.”

- The Oxford Institute for Energy Studies said in a report this week that a no-deal Brexit would put up to 40 percent of French natural gas supply at risk. Without a deal, all U.K.-based natural gas shippers will lose the right to supply France, which could create potential shortages and higher prices for French consumers. Allard Castelein, CEO of the Rotterdam Port, which is Europe’s biggest port, says that Brexit will be an “unprecedented event” and that “there will be surprises, there will be delays, there will be a loss of value and we are simply not in the position to underestimate this.” Bloomberg writes that Britain is one of the Netherlands’ biggest trading partners and that after current customs rules end, Britain will become a “third country” and customs clearance will be required.

- The Democratic Republic of Congo has grown more dominant as the world’s top source of cobalt in 2018, accounting for 72 percent of global supplies, according to Darton Commodities Ltd. The nation produced 98,300 tons last year, up from 80,800 tons in 2017. Supply growth has outpaced refiner demand, contributing to a crash in the cobalt price, which has lost more than 60 percent since last April, writes Bloomberg.

Emerging Europe

Strengths

- Romania was the best performing country this week, gaining 1.3 percent. Equities trading on the Bucharest exchange continue to rebound as the government holds budget discussions and may modify its previously proposed strategy to tax banks and energy companies.

- The Czech koruna was the best performing currency this week, gaining 30 basis points against the U.S. dollar. The central bank left its main rate unchanged at 1.75 percent, as expected. The country increased its rate five times last year and still sees room for additional increases in 2019. This will depend on the koruna exchange rate, Brexit negotiations and U.S.-China trade tensions, Governor Jiri Rusok commented.

- Communication services was the best performing sector among eastern European markets this week.

Weaknesses

- Poland was the worst performing country this week, losing 80 basis points. Jastrzebska Spolka Weglowa (JSW) and Polskie Gornictow Naftowe (PGN) declined the most, both losing about 5 percent over the past five days. These companies are expected to report weaker fourth-quarter results.

- The Russian ruble was the worst performing currency this week, losing 1.3 percent against the U.S. dollar. Days after Senate Intelligence Committee made a statement that “there is not factual evidence of collusion between the Trump campaign and Russia,” U.S. Democrats reintroduced new sanctions on Russia that may go after banks and energy companies.

- Consumer staples was the worst performing sector among eastern European markets this week.

Opportunities

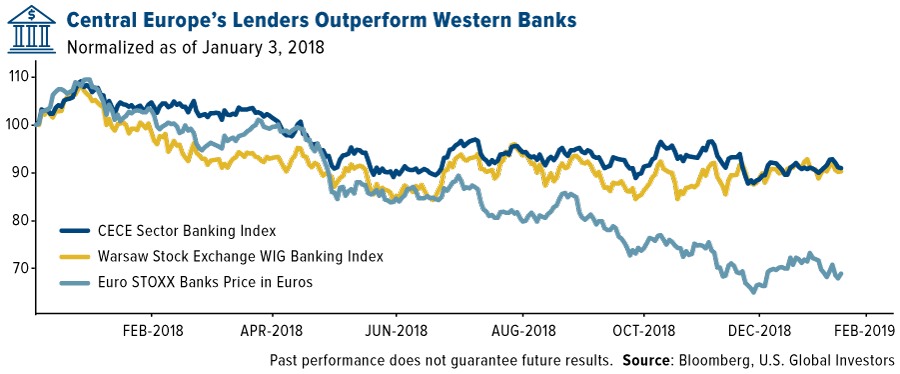

- Eastern European banks are outperforming their Western peers, supported by higher interest rates and economies that are more vibrant. Czech and Polish banks are announcing strong results as well. The four Polish lenders reporting fourth-quarter figures posted double-digit lending growth, fueled by strong demand for mortgages and consumer credit. According to Bloomberg’s article, the share of eastern European lenders does not fully reflect stronger performance.

- Romania will most likely cancel a 2 percent tax on energy companies’ revenue that the government recently proposed to boost income. This week Senate Speaker Calin Tariceana said that the tax would hinder investment and harm future development and profits. If indeed the energy tax is cancelled, the energy shares may appreciate as they trade below mid-December levels, during which the Romanian government announced tax on banks and energy companies.

- Poland’s government is working on a tax relief package for people willing to return to their homeland, taking advantage of uncertainty surrounded the U.K.’s decision to leave the European Union. Since Poland entered the bloc, about 2.6 million people have moved abroad, mainly to the U.K. This should help to ease a tight labor market in Poland and stimulate growth further. Poland’s economy has been growing around 5 percent in the past two years, but the annual growth rate is expected to slow down this year to 3.8 percent.

Threats

- Euro-area industrial output fell 0.9 percent in December from November, more than twice as much as expected. The annual decline of 4.2 percent was the steepest since 2009. Bloomberg Economics blamed Ireland and said the data may strip about 0.3 percentage points off GDP growth.

- The conflict in Eastern Europe is in danger of escalating, a United Nations official warned. This over-four-year conflict in rebel-held eastern Ukraine has claimed over 10,000 lives. Heavy fighting has eased, but a low-grade war continues along the border. Problems escalated last year when Russian forces fired on a Ukrainian warship, injuring crewmembers and capturing three vessels. The Minsk agreement signed in 2015 has failed to quell the conflict.

- According to the Russian economic minister, GDP growth could decelerate to 1.3 percent in 2019 from 2.3 percent in 2018. External risks could hamper economic growth, fiscal decisions from 2018, the OPEC agreement for oil production cuts, and weaken growth of the budget’s social expenditures. This week Morgan Stanley turned bearish on Russia over the possibility of further U.S. sanctions and doubts of the ruble rallying further. Recent reports suggest that new sanctions will be coming out in response to the capture of Ukrainian sailors by the Russian Navy in the Sea of Azov last year, near Crimea.

China Region

Strengths

- China’s Shanghai Composite reopened post-Golden Week holidays and gained 2.45 percent amid ongoing trade talks in Beijing this week, while Vietnam’s Ho Chi Minh Stock Index jumped 4.65 percent; Vietnam was also closed all last week on holiday. Singapore’s Straits Times Total Return climbed 1.18 percent.

- Consumer goods was the top performing sector in the Hang Seng Composite Index for the week, climbing 2.01 percent.

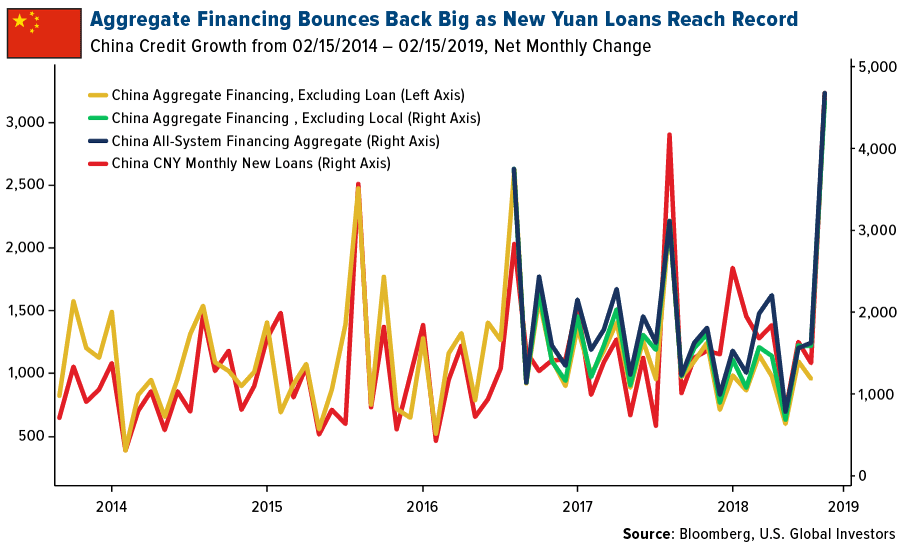

- New yuan loans in China jumped to a record 3.23 trillion yuan, as aggregate financing also came in higher than expected at 4.64 trillion yuan. Seasonally, the numbers are indeed higher at this time of year, and while monetary policy may not have shifted in any major way yet at this point we are seeing some of the results of stimulus efforts on the part of the government to spur lending.

Weaknesses

- The Philippines closed down 2.00 percent on the week, keeping Indonesia’s Jakarta Composite—which declined 2.03 percent—company as the U.S. dollar strengthened.

- Information technology was the worst performing sector in the Hang Seng Composite Index for the week, falling 1.60 percent.

- Singapore’s final fourth-quarter GDP reading missed analysts’ expectations, with quarter-over-quarter readings clocking in at 1.4 percent, shy of 1.5, and year-over-year readings at 1.9 percent, below expectations for 2.1 percent growth.

Opportunities

- Presidents Donald Trump and Xi Jinping both hailed the progress in this week’s Beijing-based trade talks, as President Xi Jinping noted the “important progress” and President Trump stated they were “going along very well,” even though the White House Press Secretary—who did note the progress—also cautioned that “much work remains.” It is a positive that President Trump indicated several times throughout the week that he may consider extending the March 1 tariff hike deadline in the event of satisfactory progress, and President Xi announced the talks will be returning to Washington next week. Reportedly the two sides were still understandably apart on reform measures and IP issues but both sides also reportedly continue to work toward finer details in a relatively comprehensive manner, bringing, one hopes, the two sides closer to a memorandum of understanding that could set the stage for a true summit between Presidents Trump and Xi on finalizing a trade deal and resolving some of the uncertainty around global trade.

- As Chinese technology giant Tencent Holdings Ltd. continues to expand its global reach, the company led a $300 million round of funding for Reddit Inc. that valued the discussion forum at $3 billion. The company is reportedly also in talks to bring the popular Apex Legends game (Electronic Arts) to China.

- Zilingo Pte., the Singapore-based startup fashion platform run by 27-year-old Ahkiti Bose, now has a valuation of almost $1 billion after raising $226 million from investors including Sequoia Capital and Temasek Holdings Pte., Bloomberg News reported this week. Of the 239 venture capital-backed startups around the world worth at least $1 billion, only 23 have a female founder. Online shopping in the region reached some $23 billion in 2018, the article continues, citing a report by Google and Temasek, and is expected to reach $100 billion by 2025.

Threats

- Although the participants in the U.S.-China trade talks continue to offer something of a measured optimism in tone, uncertainty still looms large. We have seen several positive developments recently—productive talks and remarks from both the U.S. and Chinese presidents, as well as the notion that the deadline “may” and “might” be extended. But in his Rose Garden speech today, President Donald Trump hedged some of his optimism, indicating that challenges remain.

- Following the chorus of recent concerns by several allies about Chinese technology’s reach (Huawei remains front and center, particularly after the Czech cybersecurity agency reiterated its warnings this week), Israeli security officials are also raising concerns over Chinese investment in Israeli technology companies, the Wall Street Journal reports. “U.S. and Israeli officials said they are especially concerned about stepped-up Chinese investments in Israeli companies whose products are dual-use, meaning they have both military and commercial applications, such as drones and artificial intelligence,” the article explained. “They also worry about China using Israeli companies as a way to uncover U.S. secrets and about Beijing transferring Israeli technological know-how to its ally, Iran, an arch foe of Israel.”

- Central banking policies and currency effects around the region—and from the United States Fed and dollar—could continue to play outsized roles in the near future in or around a trade deal (or lack thereof).

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended February 15 was TokenCard, up 203.48 percent.

- For the very first time this week, two U.S. pension funds became investors in a cryptocurrency-focused venture capital fund. Fairfax County Retirement Systems, which manages three separate defined benefit plans in Virginia, announced that two of their funds made allocations to Morgan Creek Capital’s new $40 million Digital Asset Index Fund, according to Bloomberg. Although these are the first-ever pension funds to gain exposure to crypto assets, other institutional investors have come before them, including Yale University.

- In a press release, computer technology giant Oracle said that it has vastly expanded its blockchain platform business to help users “speed up the development, integration and deployment of new blockchain applications.” With this latest release, Oracle has added “developer-oriented productivity enhancements,” “consortium-oriented identity management features” and other applications for companies and organizations that conduct transactions via a blockchain network.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended February 15 was The Currency Analytics, down 90.34 percent.

- The rollout for Bakkt, the highly anticipated digital asset network supported by New York Stock Exchange operator Intercontinental Exchange (ICE), has been delayed yet again. During an earnings call, ICE CEO Jeff Sprecher said that the Bakkt launch is now set for late 2019, after initially being expected in early 2019. In addition, ICE CFO Scoot Hill raised eyebrows by calling Bakkt a “moonshot bet.”

- A report by Ernst & Young shows that, in early February, disgraced Canadian cryptocurrency exchange QuadrigaCX inadvertently transferred 103 bitcoins valued at almost $500,000 to cold wallets to which the company no longer has access. A “cold wallet” is any storage device not connected to the internet, protecting it from unauthorized access and cyberattacks. The incident could deteriorate investors’ confidence in digital assets.

Opportunities

- Bitcoin payments could soon be coming to Square’s Cash App. Square and Twitter CEO Jack Dorsey told podcaster Stephan Livera this week that plans are in development to integrate bitcoin scaling technology with the popular mobile payments service. During the podcast, Dorsey, a prominent cryptocurrency investor and advocate, said he wants to help bitcoin expand past just “buying and selling” and to “make happen the currency aspect.” In other news, JPMorgan Chase plans to launch the very first U.S. bank-backed cryptocurrency, dubbed the JPM Coin, for clients of its wholesale-payments business. The bank, which has successfully tested the movement of transactions made with the coin, believes it can help reduce clients’ counterparty and settlement risk, decrease capital requirements and enable instant value transfer, Bloomberg reports. What’s more, Nasdaq announced on Monday that it will begin sending real-time bitcoin and Ethereum index level information on its global index data service.

- One financial expert believes a bitcoin ETF is inevitable. During an interview on CNBC’s “ETF Edge” at the Inside ETFs Conference in Hollywood, Florida, Edelman Financial Engines founder Ric Edelman said that such an ETF is “virtually certain.” “The only question is when,” he added. Edelman remarked that he’s confident the industry will overcome “several legitimate thoughtful concerns,” and that once a bitcoin ETF appears on the market, he’ll be “much more comfortable recommending that ordinary investors participate.”

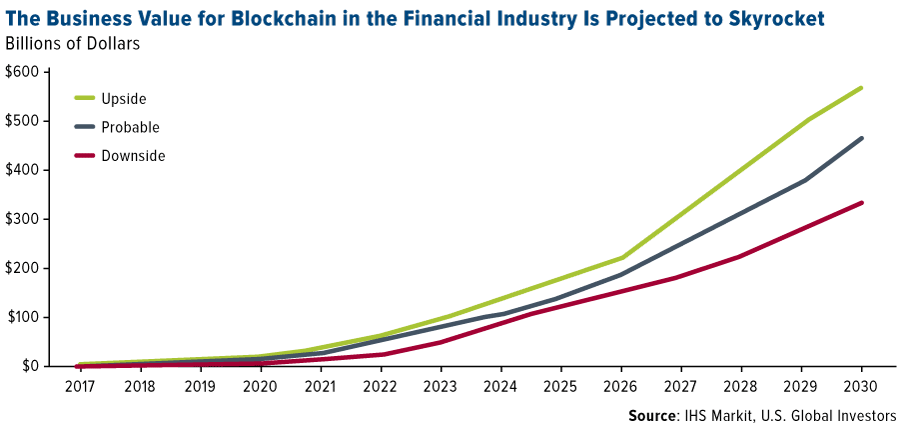

- Blockchain’s value to banks and financial institutions is projected to climb from $1.9 billion in 2017 to as much as $462 billion by 2030, according to global information provider IHS Markit. Don Tait, principal analyst at IHS Markit, stated in a press release that financial regulatory bodies around the world “are reacting positively towards blockchain technology within the financial sector… The backing by these regulatory bodies bolsters the credibility of blockchain technology, helping it become more mainstream.”

Threats

- A new wrinkle has emerged in the case involving Gerald Cotten, the former CEO of QuadrigaCX, Canada’s largest cryptocurrency exchange. As readers might already know, Cotten passed away in December at the age of 30, reportedly of Crohn’s disease, taking with him the only known password to access some $190 million in clients’ crypto holdings. ABC News now reports that Cotten had allegedly wanted out of the business for some time, which raises questions about the nature and timing of his death. What’s more, it now appears as if Cotten had been running his entire business operations from a single personal laptop. In the words of Michael Gokturk, CEO of Vancouver-based Einstein Exchange, “Makes no sense for a pioneer [in the industry] to make such a rookie mistake. It’s like walking out on the street with $1 million in 100s on him at all times.”

- Recently discovered hardware vulnerabilities, which could affect chips manufactured by Intel, ARM and AMD, raise the chances of investors having their passwords and crypto assets stolen from personal electronic devices. “An attacker who has knowledge of a sufficiently powerful vulnerability can theoretically force your CPU to reveal secret data such as private keys used to control your bitcoin,” says Bitcoin Core developer Bryan Bishop.

- “There’s no good reason to trust blockchain technology.” That’s according to noted American cryptographer Bruce Schneier, writing for WIRED. Schneier contends that blockchain technology has been hailed as a tool to eliminate the need for trust, but “when you analyze both blockchain and trust, you quickly realize that there is much more hype than value. Blockchain solutions,” he writes, “are often much worse than what they replace.” Part of Schneier’s bearishness stems from his belief that blockchain simply “shifts some of the trust in people and institutions to trust in technology,” and when that trust fails, “there is no recourse.”

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| Oil Futures | 55.74 | +3.02 | +5.73% |

| S&P Energy | 485.89 | +22.05 | +4.75% |

| Russell 2000 | 1,569.25 | +62.85 | +4.17% |

| S&P Basic Materials | 341.41 | +11.11 | +3.36% |

| DJIA | 25,883.25 | +776.92 | +3.09% |

| S&P 500 | 2,775.60 | +67.72 | +2.50% |

| Nasdaq | 7,472.41 | +174.21 | +2.39% |

| Natural Gas Futures | 2.63 | +0.05 | +1.82% |

| 10-Yr Treasury Bond | 2.66 | +0.03 | +1.06% |

| Korean KOSPI Index | 2,196.09 | +19.04 | +0.87% |

| S&P/TSX VENTURE COMP IDX | 615.92 | +3.98 | +0.65% |

| Gold Futures | 1,324.70 | +6.20 | +0.47% |

| Hang Seng Composite Index | 3,740.84 | +0.67 | +0.02% |

| S&P/TSX Global Gold Index | 190.09 | -2.37 | -1.23% |

| XAU | 75.64 | -0.11 | -0.15% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| S&P/TSX Global Gold Index | 190.09 | +15.93 | +9.15% |

| Russell 2000 | 1,569.25 | +114.55 | +7.87% |

| DJIA | 25,883.25 | +1,676.09 | +6.92% |

| Oil Futures | 55.74 | +3.43 | +6.56% |

| Nasdaq | 7,472.41 | +437.72 | +6.22% |

| S&P 500 | 2,775.60 | +159.50 | +6.10% |

| S&P Energy | 485.89 | +27.79 | +6.07% |

| S&P Basic Materials | 341.41 | +17.27 | +5.33% |

| Hang Seng Composite Index | 3,740.84 | +168.17 | +4.71% |

| Korean KOSPI Index | 2,196.09 | +89.99 | +4.27% |

| Gold Futures | 1,324.70 | +24.40 | +1.88% |

| 10-Yr Treasury Bond | 2.66 | -0.06 | -2.17% |

| Natural Gas Futures | 2.63 | -0.75 | -22.28% |

| S&P/TSX VENTURE COMP IDX | 615.92 | +17.88 | +2.99% |

| XAU | 75.64 | +6.10 | +8.77% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| S&P/TSX Global Gold Index | 190.09 | +26.64 | +16.30% |

| Gold Futures | 1,324.70 | +97.50 | +7.94% |

| Hang Seng Composite Index | 3,740.84 | +219.38 | +6.23% |

| Korean KOSPI Index | 2,196.09 | +108.03 | +5.17% |

| Russell 2000 | 1,569.25 | +45.13 | +2.96% |

| Nasdaq | 7,472.41 | +213.38 | +2.94% |

| DJIA | 25,883.25 | +593.98 | +2.35% |

| S&P 500 | 2,775.60 | +45.40 | +1.66% |

| S&P Basic Materials | 341.41 | -0.49 | -0.14% |

| S&P Energy | 485.89 | -3.76 | -0.77% |

| Oil Futures | 55.74 | -0.72 | -1.28% |

| 10-Yr Treasury Bond | 2.66 | -0.45 | -14.37% |

| Natural Gas Futures | 2.63 | -1.41 | -34.87% |

| S&P/TSX VENTURE COMP IDX | 615.92 | -8.42 | -1.35% |

| XAU | 75.64 | +10.65 | +16.39% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (12/31/2018):

Freeport-McMoRan Inc.

Ivanhoe Mines Ltd.

Citigroup Inc.

Jastrzebska Spolka Weglowa (JSW)

Polskie Gornictow Naftowe (PGN)

Agnico Eagle Mines Ltd

Evolution Mining Ltd

Harmony Gold Mining Co Ltd

Newcrest Mining Ltd

Pure Gold Mining Inc

Barrick Gold Corp

New Gold Inc

Royal Dutch Shell Plc

Alamos Gold Inc

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks.

The Russell 2000 Index is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months.

The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange.

The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver.

The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar.

The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500.

The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500.

The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period.

The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500.

The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500.

The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500.

The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500.

The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500.

The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500.

The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns.

The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

Bloomberg Industrial Metals Subindex is a commodity group subindex of the Bloomberg CITR. It is composed of futures contracts on aluminum, copper, nickel and zinc. It reflects the return on fully collateralized futures positions and is quoted in USD. The Ho Chi Minh VSE is a major stock market index which tracks the performance of 303 equities listed on the Ho Chi Min and Hanoi Stock Exchange in Vietnam. The Straits Times Index comprises the top 30 SGX Mainboard listed companies on the Singapore Exchange selected by full market capitalization. The Michigan Consumer Sentiment Index (MCSI) is a monthly survey of U.S. consumer confidence levels conducted by the University of Michigan. It is based on telephone surveys that gather information on consumer expectations regarding the overall economy. The Empire State Manufacturing Index (ESMI) is a survey given out by the Federal Reserve Bank of New York to manufacturing companies within the state of New York. It measures how the people who run these companies feel towards the economy.