Yes, Gold Is Being Manipulated. But to What Extent?

Date Posted: May 17, 2019

Read time: 53 min

This week the European Commission announced that it's fining five big banks for rigging the international foreign exchange (forex) market.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

Another day, another banking scandal.

This week the European Commission announced that it’s fining five big banks for rigging the international foreign exchange (forex) market. As many as 11 world currencies—including the euro, British pound, Japanese yen and U.S. dollar—were allegedly manipulated by traders working at Barclays, the Royal Bank of Scotland (RBS), Citigroup, JPMorgan and Japan’s MUFG Bank.

Altogether, the fines come out to a whopping 1.07 billion euros ($1.2 billion).

According to the press release dated May 16, the infringements took place between December 2007 and January 2013. Traders working on behalf of the offending banks secretly shared sensitive trading information. This enabled the traders—who were direct competitors—to “make informed market decisions on whether to sell or buy the currencies they had in their portfolios and when.”

Financial services is already the least trusted sector among seven others worldwide, according to the 2019 Edelman Trust Barometer. News of the coordinated forex rigging—which follows other high-profile scandals such as the Libor scandal, Wells Fargo fake account scandal, gold fixing scandal (which I’ll get to later), among many more—is unlikely to improve public sentiment.

As I’ve said before, I believe that strong distrust in traditional financial services, especially among millennials, greatly contributed to early bitcoin adoption. With bitcoin, there’s no third-party risk. Transactions are peer-to-peer. Users of the digital coin find this sort of freedom very attractive, and because it’s built on top of blockchain technology, price manipulation is much more difficult to pull off.

That’s not to say that bitcoin hasn’t been, or isn’t still being, manipulated. There are those who argue that the cryptocurrency’s meteoric rise to nearly $20,000 in late 2017 was at least in part due to coordinated price manipulation. And early today its price dramatically lost as much as $1,702, its worst intraday drop since January 2018, after breaching $8,300 on Thursday.

Bitcoin Seen as a Threat to Global Fiat Currencies

None of this should come as a surprise to anyone who’s been paying attention, of course. I’ve seen and heard the aggressive stance bankers have taken against bitcoin and other cryptocurrencies, as I’m sure you have.

Quite simply, banks don’t want the competition. If you recall, JPMorgan CEO Jamie Dimon called people who buy bitcoin “stupid” and said he’d fire any trader caught trading it. (And then in an amazing about-face, his bank announced in February the rollout of its own digital coin, the “JPM Coin.”)

Quite simply, banks don’t want the competition. If you recall, JPMorgan CEO Jamie Dimon called people who buy bitcoin “stupid” and said he’d fire any trader caught trading it. (And then in an amazing about-face, his bank announced in February the rollout of its own digital coin, the “JPM Coin.”)

Also consider the comments made by Agustín Carstens, general manager of the Bank of International Settlements (BIS). The BIS, in case you’re unfamiliar, is often called the “central bank of central banks.” That’s because it provides banking services to as many as 60 financial institutions from all over the world, including heavyweights such as the Federal Reserve, Bank of England (BoE), European Central Bank (ECB) and Bank of Japan (BoJ). Its influence on global monetary and financial policy, in other words, is monolithic.

Ever since bitcoin hit $4,000 or so, General Manager Carstens has been on a global PR campaign to stop its momentum—because, again, it’s seen as a threat to sovereign currencies. As recently as November of last year, he laid out 10 reasons why central banks should discourage the use of digital coins.

Among them: “Cryptocurrencies are highly conducive to illegal activities.”

Anyone else see the irony? Fiat currencies are still very much used to conduct illegal activities, despite the enactment of anti-money laundering (AML) and know your customer (KYC) laws. In November 2017, Jennifer Fowler, deputy assistant secretary for the Office of Terrorist Financing and Financial Crimes (TFFC), testified before the Senate Judiciary Committee that the U.S. dollar “continues to be a popular and persistent method of illicit commerce and money laundering,” and that, although virtual currencies are also used, “the volume is small compared to the volume of illicit activity through traditional financial services.”

The BIS doesn’t stop at bitcoin, though. It’s also put gold in its crosshairs.

Gold Suppression: It’s Not a Question of IF but to WHAT EXTENT

First of all, let me say that gold price suppression (“fixing,” “rigging,” “manipulating” or however else you want to think about it) is not just a conspiracy theory. It’s a well-documented phenomenon, with real actors and real ramifications. In 2014, Barclays was fined nearly $44 million for failing to prevent traders from manipulating the London gold “fix.” Late last year, a former JPMorgan trader pleaded guilty to manipulating the U.S. metals markets. Remember the gold futures “flash crash” of 2014?

The best people to speak to about this subject are the folks at the Gold Anti-Trust Action Committee, or GATA. For 20 years now, Chris Powell and others at GATA have made it their mission to expose collusion by international financial institutions to control the price and supply of gold.

The best people to speak to about this subject are the folks at the Gold Anti-Trust Action Committee, or GATA. For 20 years now, Chris Powell and others at GATA have made it their mission to expose collusion by international financial institutions to control the price and supply of gold.

This week I had the chance to sit down with Chris, GATA’s secretary/treasurer. I asked him how institutions manage to manipulate the price of gold on such a global scale.

“It’s done largely in the futures markets,” Chris told me. “It’s also done in the London over-the-counter (OTC) market. The mechanisms are gold swaps and leases between central banks and bullion banks, and through the sale of futures contracts.”

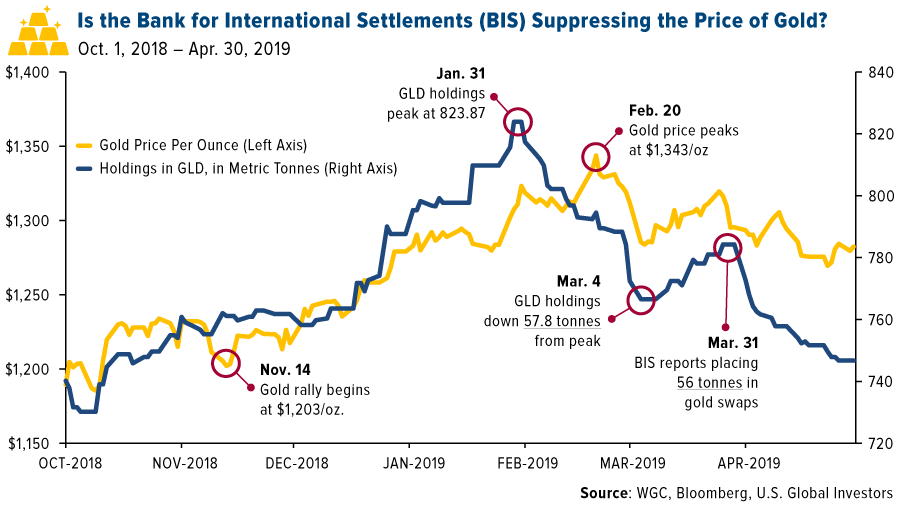

GATA’s Robert Lambourne reported on this in March of this year. As you can see in the chart below, gold rallied between November 2018 and February, when it peaked at around $1,343 an ounce.

Ordinarily, you could expect inventory in the bullion-backed SPDR Gold Shares ETF (GLD) to continue to climb at least until then. But that’s not at all what happened. Three weeks before the price of gold peaked, the holdings in the GLD curiously began to fall, and by March 4, the ETF had lost approximately 57.8 metric tonnes. And because the GLD is the largest gold ETF in the world—its value stands at $30.2 billion, as of this week—such selling will naturally impact the price of gold. Sure enough, the yellow metal soon fell below $1,300. What gives?

The answer to that question may lie in the BIS’ monthly statement of account for February. According to Robert’s reporting, the BIS was still actively trading gold swaps, which it uses to gain access to the metal held by commercial banks. Specifically, the bank placed as much as 56 metric tonnes of gold swaps into the market in February.

If you ask me, that amount is remarkably close to the 57.8 tonnes that fled the GLD in the first quarter of this year.

Hard to believe? This is only scratching the surface. I’ll let Chris Powell be the one to elaborate, but it will have to wait until a Frank Talk next week. Trust me when I say this is an interview you don’t want to miss! Make sure you’re subscribed to Frank Talk so you can be one of the first to read it.

Gold Market

This week spot gold closed at $1,277.65, down $8.40 per ounce, or 0.65 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 1.80 percent. The S&P/TSX Venture Index came in up 1.61 percent. The U.S. Trade-Weighted Dollar rose 0.71 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| May-14 | Germany CPI YoY | 2.0% | 2.0% | 2.0% |

| May-14 | ZEW Survey Current Situation | 6.3 | 8.2 | 5.5 |

| May-14 | ZEW Survey Expectations | 5.0 | -2.1 | 3.1 |

| May-14 | China Retail Sales YoY | 8.6% | 7.2% | 8.7% |

| May-16 | Housing Starts | 1209k | 1235k | 1168k |

| May-16 | Initial Jobless Claims | 220k | 212k | 228k |

| May-17 | Eurozone CPI Core YoY | 1.2% | 1.3% | 1.2% |

| May-23 | Initial Jobless Claims | 215k | — | 212k |

| May-23 | New Homes Sales | 675k | — | 692k |

| May-24 | Durable Goods Orders | -2.0% | — | 2.6% |

Strengths

- The best performing precious metal this week was gold, down 0.65 percent. Gold bulls regained the upper hand this week in the Bloomberg survey of traders and analysts, as investors weigh U.S.-China trade tensions and the outlook for global growth. Bloomberg reports that open interest, a tally of outstanding futures contracts in bullion, surged the most since mid-2016 on Monday to the highest in seven weeks.

- Turkey’s gold reserves rose $246 million from the prior week to now be worth $20.7 billion, according to figures from the nation’s central bank in Ankara. Intercontinental Exchange Inc.’s plan to slow down lightning-fast traders in the futures market has the approval from the U.S. Commodity Futures Trading Commission, reports Bloomberg’s Ben Bain. The exchange’s plans to impose a 3-millisecond trading delay on gold and silver contracts, and would be the first-ever “speed bump” for futures trading.

- Bloomberg reports that China’s holdings of U.S. Treasury securities dropped in March for the first time in four months amid the trade dispute. China’s holdings of notes, bills and bonds declined by $10.4 billion from the prior month to total $1.12 trillion, according to Treasury Department data.

Weaknesses

- The worst performing precious metal this week was platinum, down 5.30 percent as hedge funds cut their bullish position to a six-week low. Better-than-expected U.S. economic data boosted the dollar, taking gold down for the week despite the ongoing trade concerns. Bloomberg reports that after reaching a one-month high on Tuesday, gold has failed to hold those gains on a strong dollar. U.S. home starts rose while jobless claims fell.

- Commodity ETFs saw seven straight weeks of outflows, led by precious metals funds, which had $429 million of losses. Silver is at its cheapest relative to gold in more than 25 years, however that doesn’t necessarily mean it’s ready for a rebound. According to Ole Hansen, head of commodity strategy at Saxo Bank A/S, gold’s premium over silver – “the forgotten metal” – will keep increasing as long as traders focus on safe-haven and growth worries. Silver has industrial and jewelry uses, making it more exposed to economic and trade jitters.

- Zimbabwe’s largest gold producer, Metallon Corp., is suing the country’s central bank for $132 million because it has been paying for gold in local currency, rather than U.S. dollars. Zimbabwe abandoned its local dollar in 2009 after hyperinflation, and then adopted the U.S. dollar. However, it’s since introduced a quasi-currency that can only be used within the nation and the business sector is not happy.

Opportunities

- A rate cut is already being priced in as a near certainty. Bloomberg’s Emily Barrett writes that traders of Fed funds are currently positioning for a rate cut of just over 25 basis points this year and that the inflation market suggests the Fed should slash rates, rather than just trimming them. Something that stayed out of headlines this week: yields on 3-month Treasuries are again higher than those on 10-year notes. The inversion picked up a week ago when President Trump announced an increase in tariffs on Chinese goods. Gold regained some of its appeal this week on safe haven demand after three straight monthly declines.

- Tavi Costa, a global macro analyst at Crescat Capital LLC – one of last year’s best performing hedge funds – expects China’s debt woes to spur a rally in gold, reports Bloomberg. 2019 is shaping up to be the biggest so far for defaults in its $13 trillion bond market. In a telephone interview, Costa says that “the one pattern we found is that gold in local currency terms tends to rise significantly as a credit bust develops.” Costa calls its bullish bet on gold the “trade of the century.”

- This was a busy week for M&A activity and speculation. Australian gold producer St Barbara Ltd. agreed to acquire Vancouver-based Atlantic Gold Corp for C$722 million. Alexandria Minerals will be acquired by Osisko Mining Inc. in combination with Chantrell Ventures Corp and will be renamed O3 Mining. Bloomberg reports that Canadian miner Iamgold Corp. is exploring a possible sale of all or part of the company. BMO analyst Brian Quast writes that New Gold, Pretium Resources, TMAC Resources and Wesdome are potential targets for Australian miners looking to expand into Canada through acquisitions.

Threats

- According to a monthly poll of consumers, expected inflation three years ahead dropped to 2.7 percent in April, which is the lowest reading since August 2017. A similar University of Michigan survey measure of expected inflation in five to 10 years also fell in April to a half-century low. These polls, however, were conducted before President Trump raised tariffs to 25 percent from 10 percent on $200 billion worth of Chinese imports. This is a noticeable difference in sentiment, as Goldman Sachs says the trade war escalation will actually noticeably drive inflation above 2 percent next year, saying the cost of tariffs has fallen entirely on U.S. businesses and consumers.

- According to Greg Longstreet, CEO of Del Monte Foods Inc., the U.S. is in an inflationary environment right now, with tariffs driving up prices on his company’s canned fruits and vegetables as much as 25 percent, according to Bloomberg. Walmart Inc. announced this week that shoppers will absorb some of the costs from the tariffs and will likely set the tone for other retailers as they decided whether or not to pass along additional costs to consumers or absorb them.

- The U.S.-China trade war continues to worsen. On Friday morning, China’s state media signaled a lack of interest in resuming the trade talks under the current threat of higher tariffs, writes Bloomberg. Also adding fuel to the fire is the Trump administration placed restrictions on Huawei, China’s top technology company.

Index Summary

- The major market indices finished mostly down this week. The Dow Jones Industrial Average lost 0.69 percent. The S&P 500 Stock Index fell 0.76 percent, while the Nasdaq Composite fell 1.27 percent. The Russell 2000 small capitalization index lost 2.37 percent this week.

- The Hang Seng Composite lost 2.11 percent this week; while Taiwan was down 3.07 percent and the KOSPI fell 2.48 percent.

- The 10-year Treasury bond yield fell 7 basis points to 2.392 percent.

Domestic Equity Market

Strengths

- Real estate was the best performing sector of the week, increasing by 1.35 percent versus an overall decrease of 0.77 percent for the S&P 500.

- Coty was the best performing stock for the week, increasing 14.09 percent.

- Nvidia’s shares gained more than 5 percent in after-hours trading on Thursday after the chipmaker reported both top- and bottom-line beats and gave guidance that outpaced expectations.

Weaknesses

- Financials was the worst performing sector for the week, decreasing by 2.10 percent versus an overall decrease of 0.77 percent for the S&P 500.

- Qorvo was the worst performing stock for the week, falling 14.84 percent.

- Pinterest posted its first quarterly results as a public company, reports Business Insider, and unfortunately announced a larger-than-expected loss. The company also gave a disappointing full-year revenue forecast, sending shares down by as much as 19 percent on Thursday.

Opportunities

- For the very first time, Warren Buffett’s Berkshire Hathaway has revealed its large stake in Amazon for the first quarter, reports CNBC. The company bought 483,300 Amazon shares, making its stake worth $904 million, according to a filing out Wednesday.

- Walmart announced this week its next-day delivery offer, keeping pace with e-commerce competitor Amazon. The next-day service will be rolled out first in Phoenix and Las Vegas early next week and applies to orders costing at least $35.

- Microsoft and Sony made a joint announcement on Thursday that they would "explore joint development of future cloud solutions in Microsoft Azure to support their respective game and content-streaming services." Since the two companies have been fierce rivals since the first Microsoft Xbox challenged the Sony PlayStation 2 in 2001, the partnership came as a bit of a surprise, reports Business Insider.

Threats

- The stock market’s “single-best leading indicator” is flashing a warning signal, according to one research firm. Copper has been leading the stock market for 18 months and is now signaling weakness ahead for stocks, according to Capital Economics.

- Unprofitable companies like Uber and Lyft are rushing to go public, and it could throw the market off track, writes Business Insider. "If underperformance of these blockbuster listings becomes the straw that breaks the unicorns’ backs, the bull market could feel the pain," said Michael Arone, the chief investment strategist for State Street Global Advisors’ U.S. SPDR business.

- The U.S. Supreme Court ruled against Apple in a case centered on the App Store. Justices voted to allow a class-action lawsuit from consumers who accused Apple of monopoly power to raise the prices of iPhone apps, reports the NY Times.

The Economy and Bond Market

Strengths

- The Leading Index rose for the third straight month in April, reaching 112.1, the Conference Board said Friday. Last month’s reading reflected a 0.2 percent gain over March, following a 0.3 percent increase that month, and 0.2 percent rise in February.

- Jobless claims last week fell to the lowest level in a month, dragging them back near a post-recession low and suggesting all is well in the U.S. labor market. Initial jobless claims, a rough way to measure layoffs, sank by 16,000 to a seasonally adjusted 212,000 in the seven days ended May 11, the government said Thursday.

- U.S. consumer sentiment jumped to a 15-year high in early May amid growing confidence over the economy’s outlook, but much of the surge was recorded before an escalation in the trade war with China. The University of Michigan said its consumer sentiment index increased 5.3 percent to 102.4, the highest reading since 2004. Economists polled by Reuters had forecast a much lower reading of 97.5.

Weaknesses

- U.S. retail sales declined slightly in April, according to a Commerce Department report. Advance estimates of U.S. retail and food services sales for last month totaled $513.4 billion— a decrease of 0.2 percent from the previous month.

- U.S. manufacturing fell again in April, which is fresh evidence that a slowing global economy and trade frictions are hurting part of the U.S. economy. Manufacturing output, the biggest component of industrial production, fell 0.5 percent in April from a month earlier, the Federal Reserve said Wednesday. That helped tug down broader output across factories, mines and utilities last month. Industrial production was down 0.5 percent in April, well below expectations among economists surveyed by The Wall Street Journal for a flat reading.

- The world’s second largest economy showed more signs of slowing. Retail sales in April out of China grew at their slowest annual pace since May 2003, while industrial output and fixed-asset investment also weakened.

Opportunities

- Next Wednesday’s Fed minutes are likely to add further color to the debate about future FOMC policies. The lack of inflationary pressure has raised expectations that we might see the Fed lean into talks of possible rate cuts. However, the latest minutes are expected to reinforce the view that the Fed is in no rush to move on policy in either direction.

- New home construction rose for a second month and topped estimates in April, which is a sign of positive momentum for the housing sector. Residential starts increased 5.7 percent to a 1.24 million annualized rate after a 1.7 percent gain in March that was previously reported as a drop, according to government figures released Thursday. Permits, a proxy for future construction, advanced 0.6 percent to a 1.30 million rate.

- President Donald Trump announced a Friday a delay in imposing tariffs on imported vehicles and parts from the European Union, Japan and other nations for 180 days to pursue negotiations. This avoids opening another front in his tariff battle with some of America’s key allies.

Threats

- German 10-year government bond yields were well over three percentage points more than Japanese ones at the start of the 2000s, when Europe was raising rates to contain mounting price pressures and Japan was mired in deflation. Today their yields are roughly equal, which is the consequence of the European debt crisis and a slide in trend growth and inflation rates similar to Japan’s experience. “Most commentators now accept the Japanification of mainland Europe has occurred, but they just cannot conceive that the same thing might happen with the U.S.,” said Albert Edwards at Societe Generale SA.

- The fed funds futures market is getting aggressive about a 2019 Federal Reserve interest rate cut, with one now priced in at a roughly 80 percent probability. But that’s nothing compared with the message from traders of inflation-linked Treasuries. Pricing in these markets suggests Fed policy makers might need to take drastic action with monetary policy if they’re serious about meeting their inflation mandate. The central bank’s inflation target is 2 percent, but the Treasury breakeven rate, or investors’ expected inflation rate as deduced from yields on various U.S. government bonds, implies this figure will languish around 1.4 percent over the next five years, according to Martin Hegarty, a former BlackRock Inc. managing director. “We’re priced for one cut by the end of the year, and my view is that if this inflation profile that’s priced by the market turns out to be correct, we need to price in more,” said Hegarty, a fixed-income portfolio manager specializing in inflation markets.

- The U.S.-China trade war continues to escalate, which economists agree bodes poorly for the U.S. and global economies.

Energy and Natural Resources Market

Strengths

- The best performing major commodity for the week was corn, which gained 11.90 percent as recent rains, and more forecast in the coming days, is delaying spring planting. Iron ore prices hit the highest level in almost five years this week on bets of a supply scramble, nearing the $100 per ton. Bloomberg reported that futures in Singapore gained as much as 3.2 percent on Friday, the most since mid-2014. The rally is driven by supply disruptions out of Brazil and Australia. Fortescue, the world’s fourth biggest iron ore exporter, gave shareholders a surprise A$1.85 billion in dividends due to the metal’s price surge this year.

- Amid the growing trade tensions, U.S. oil has found new buyers due to slowed Chinese buying. Bloomberg reports that America shipped 470.2 million barrels to 38 countries from October through March, versus just 31 nations in the previous six months, according to Census Bureau data. Overall shipment volumes increased even as shipments to China sank by nearly 80 percent.

- On Friday the U.S. reached a deal with Canada and Mexico to immediately lift metals tariffs, removing a key roadblock to approval of the new North American trade deal. The agreement removes the 25 percent tariff on steel and 10 percent tariff on steel that had been in effect for months. The new agreement will also require all countries to monitor for and prevent a surge in steel imports from other countries – this should be positive for both metals.

Weaknesses

- The worst performing major commodity for the week was lumber, which fell 5.61 percent. West Fraser cut lumber production at two sawmills in British Columbia due to continued pricing challenges in the global lumber markets while log prices remain high. As the U.S.-China trade war escalated even further this week, several commodities have suffered. Bloomberg News reported that base metals followed equities lower on Friday morning after Chinese media reported that the Trump administration should show its negotiating sincerely. Copper is headed for its worst run since July and a fifth weekly decline as the trade tensions hurt the outlook for demand. Effective June 1, China will increase the tariff on U.S. LNG to 25 percent. The nation came out with a list of additional tariffs on Monday against the U.S. Fortunately crude oil was not on that list.

- The energy sector has had the second most bankruptcies so far this year, according to Bloomberg data. Once one of the top providers of oil-well drilling and completion, Weatherford International Plc announced last week that it was preparing to file for bankruptcy. Halcon Resources Corp. and Alta Mesa Resources Inc. have raised doubts about their ability to stay afloat amid investor demands for returns rather than pouring more money into capital expenditures. Many U.S. shale producers have had to scale back growth and make big changes to cut operating costs.

- On Wednesday the California Department of Forestry and Fire Protection released its findings on the 2018 Camp Fire and concluded that it was caused by electrical transmission lines owned and operated by PG&E, reports Bloomberg. Morgan Stanley analysts led by Stephen Byrd wrote in a note that PG&E Corp will likely come under pressure and has the potential for shareholder liability to total $5.2 billion.

Opportunities

- Equinor ASA, the Norwegian state-controlled oil company, will pay Shell $965 million in cash to raise its stake in the Caesar Tonga oil field in the U.S. Gulf of Mexico from 22.45 percent to 46 percent. This will give the company an opportunity to boost production, as the U.S. is one of its key areas of international growth. The company said in a statement on Monday that the acquisition will add almost 18,000 barrels of oil equivalent a day to Equinor’s current output of 110,000 barrels a day from the Gulf of Mexico.

- The European Commission will impose an aviation tax that could help cut the sector’s emissions by 11 percent. Although the proposed tax of 330 euros per 1,000 liters of jet fuel would raise European ticket prices by around 10 percent, it is a positive step toward decarbonizing aviation. BloombergNEF’s Bo Qin writes that the tax should not distort competitiveness or curb efficiency investments by cutting into airline profit.

- Whether or not there is a trade deal anytime soon, some are bullish on copper, even as it falls amid the trade tensions. The International Copper Study Group says the red metal will post a 189,000 ton deficit in 2019, driven by a 2 percent increase in usage and flat mine output. Goldman Sachs analysts including Hui Shan expect a continued selloff in risk assets, including copper, but that if tensions escalate with China, the nation will likely implement stimulus measures to buoy demand for copper.

Threats

- The U.S. battery boom could soon be another victim of the ongoing trade war. Bloomberg reports that lithium-ion batteries are on the list of $300 billion worth of Chinese goods that the Trump administration plans to put a tariff on of up to 25 percent. China accounts for around 40 percent of America’s battery imports. Datamyne said in a report last month that a tariff on batteries would hurt China’s exports “but would also exact a bigger toll on downstream users in the U.S.”

- Tensions rise in the Middle East after Saudi Arabia said two of its oil tankers were attacked by Iran while sailing toward the Persian Gulf. Saudi Arabia also halted its main cross-country oil pipeline after a drone attack damaged pumping stations in a strike claimed by Iran-backed rebels in Yemeni, reports Bloomberg. This could potentially curb supply out of Saudi Arabia.

- Congress had a hearing on Wednesday discussing 13 bills designed to control a large group of chemicals, which are used to make various items such as textiles, paper, cookware and more. The chemicals, called per- and polyfluoroalkyl, have persisted in the environment and their toxicity has spurred multimillion dollar litigation across the country involving many companies. Although positive for citizens, new regulations could increases costs on producers to clean up the chemicals.

Emerging Europe

Strengths

- Russia was the best relative performing country this week, gaining 2.5 percent. Shares of Gazprom, the company operating a domestic and international gas pipeline system, gained more than 20 percent in the past five days. The company announced a higher dividend payout ratio, with the new dividend yield at almost 10 percent.

- The Russian ruble was the best performing currency this week, gaining 70 basis points against the U.S. dollar. The Russian government continues to sell local currency bonds and there is a high demand for them.

- Energy was the best performing sector among eastern European markets this week.

Weaknesses

- Hungary was the worst performing country this week, losing 2.9 percent. Shares of pharmaceutical company Richter declined 7.5 percent and OTP Bank lost 3.6 percent in the past five days. Richter reported disappointing first quarter results and OTP announced plans to purchase Mobiasbanca, the fourth largest bank in Moldova.

- The Hungarian forint was the worst performing currency this week, losing 1.7 basis points against the U.S. dollar. A day after the Prime Minister of Hungary met President Trump in the White House, news emerged that the U.S. prepared anti-Orban sanctions over his erosion of democracy and deepening ties with Russia and China.

- Health care was the worst performing sector among eastern European markets this week.

Opportunities

- Growth among central emerging European countries came in higher than forecasted on an annual basis. Preliminary first quarter growth data in Hungary showed expansion of 5.3 percent, Romania 5 percent, Poland 4.6 percent and the Czech Republic 2.5 percent. Domestic demand remains the key diver to economic growth in the region. Polish and Romanian central banks kept their rates unchanged despite inflation moving higher.

- European Trade Commissioner Cecilia Malmstroem expects U.S. President Donald Trump to delay a May 18 deadline for U.S. tariffs on cars imported from the European Union. The decision on European cars, which could impact 47 billion euros ($53 billion) worth of cars and auto parts, could be delayed as Washington focuses on its ongoing trade negotiations with China.

- Jonathan Lamb and Ondrej Slama from Wood & Company believe that IMO regulations that will be implemented at the beginning of next year present opportunities for some central emerging Europe’s refineries. The new regulations will reduce demand for high sulphur fuel oil and increase consumption for diesel. They believe that Turkish Tupras, Polish Lotus (LTS) and Polskki Koncern Naftowy (PKN) will be the biggest beneficiaries on the upcoming IMO change.

Threats

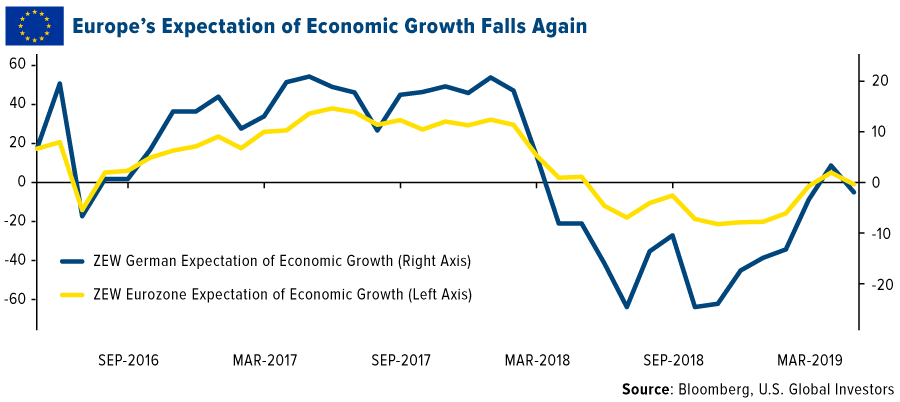

- Germany’s ZEW economic sentiment turned back to negative territory while the eurozone’s expectation for economic growth dropped below zero as well. The dispute between the U.S. and China has escalated, increasing uncertainty over German exports, Europe’s largest economy.

- A day after U.S. Secretary of State Michael Pompeo met with Russian President Vladimir Putin (and said the two countries would like to restore better relations following the conclusion of Mueller’s investigation), House Democrats restarted debates over additional sanctions on the country for meddling in the 2016 elections. The new sanctions could target Russian sovereign debt, the energy sector and financial institutions.

- According to Bloomberg, fund managers continue to cut U.K. exposure. In case of early elections in the country, Brexit supporters will gain more votes according to the latest opinion poll. The Opinium survey places the Brexit party on 34 percent of the vote, a higher level than the two main parties put together, with the Labour party slipping to 21 percent and the Conservative collapsing to just 11 percent.

China Region

Strengths

- Vietnam and India stuck it out this week and finished in the green for the last five trading days, with the Ho Chi Minh Index up 2.65 percent and the NIFTY and SENSEX Indices up 1.14 and 1.25 percent, respectively. The rest of the region was deeply.

- In a red week for all sectors in Hong Kong’s Hang Seng Composite, properties and construction finished out as the best relative performer, down only 53 basis points in that time, just barely nudging out risk-off utilities, which declined by 59 basis points.

- In a mild echo of some of China’s better-than-expected numbers earlier in the year, Hong Kong announced late this week that its final first quarter year-over-year GDP reading was 0.6 percent, better than an anticipated 0.5 percent pace, while quarter-over-quarter growth was 1.3 percent, beating estimates for only 1.2 percent.

Weaknesses

- Indonesia had a rough go this week, as the Jakarta Composite fell by 6.13 percent. Taiwan was down more than 3 percent, while Hong Kong, South Korea, the Philippines and Thailand all finished down more than 2 percent.

- Information technology was the laggard sector of the week in Hong Kong’s Hang Seng Composite Index, declining by 3.83 percent.

- Industrial production missed in China, coming in at 5.4 percent year-over-year growth versus expectations for a 6.5 percent pace for the April measurement period. Retail sales also missed, clocking in at only 7.2 percent growth, below estimates for an 8.6 percent pace, and fixed asset investment (FAI) came in at only 6.1 percent, behind expectations for a 6.4 percent growth rate.

Opportunities

- Up-and-comer Chinese Starbucks competitor Luckin Coffee began trading on Friday, rising 19.88 percent on the day and finishing with a market cap of roughly $4.8 billion. The company plans to almost double its outlets by the end of the year.

- As has been the custom lately—and because any new reader should also be aware—we will reiterate that the possibility of some kind of trade deal with China has still not been ruled out. While there certainly has been a distinct escalation in tariffs and rhetoric between the two nations, the late-June Osaka G-20 meeting between the U.S. and Chinese presidents may yet keep some options open. Secretary Steve Mnuchin said he expects to go to Beijing soon for further talks.

- Vietnam’s Chinese foreign direct investment (FDI) projections have risen throughout the trade war thus far, even as President Donald Trump recently singled out the Southeast Asian economy as a rising one set to take advantage of growth and trade throughout the region.

Threats

- The threat of trade war tariff escalation and fallout continues apace. To be sure, there also remains a possibility of some more amicable resolution. But as we’ve been saying, for the time being, stay tuned, and just remember, “It ain’t over ‘till it’s over…”

- The Chinese yuan weakened significantly, climbing (weakening) to 6.9179 on the week and reaching levels last seen back in November of 2018.

- The U.S. dollar closed the week back over 98 and remains strong relative to the rest of the world’s major currencies, which could exacerbate threats to sentiment in emerging markets

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended May 17 was Matic Network, up 268.60 percent.

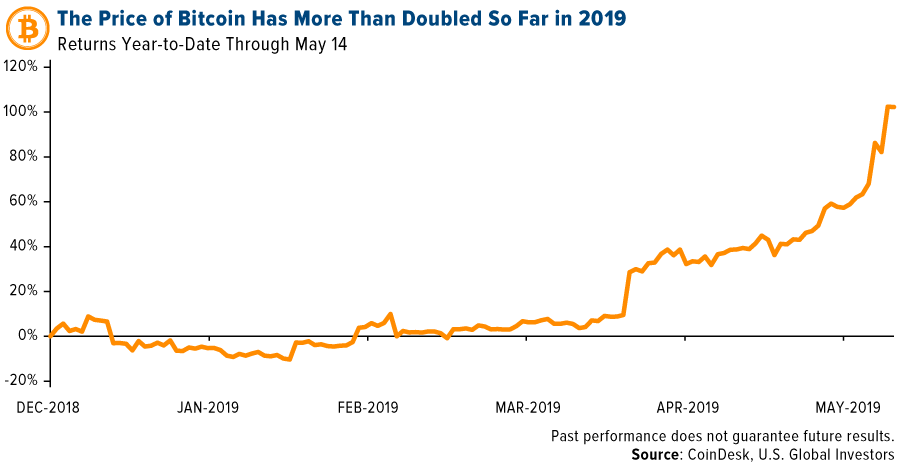

- While mainstream markets tumbled at the start of the week, bitcoin made its case as an uncorrelated, safe-haven asset, reports CNBC. On Monday, the world’s largest cryptocurrency was up as much as 15 percent, continuing its trek higher mid-week to the $8,000 mark. Meanwhile, U.S. equity markets were headed in the opposite direction, with the Dow Jones tumbling as much as 696 points on Monday, the article continues.

- Bitcoin isn’t the only digital currency gaining ground this week. The price of litecoin (LTC) hit an 11-month high on Thursday, jumping to $107.71, reports CoinDesk. This is the highest level since June 12, 2018, and the coin could shine even brighter over the next few weeks, the article explains, as the mining reward halving is now less than 90 days away.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended May 17 was Blockport, down 85.68 percent.

- As the price of bitcoin cracked the $8,000 mark on Tuesday trading, some aren’t so sure the move is sustainable, writes MarketWatch, noting the upward price spike is “nothing more than confirmation it’s not ready for widespread adoption.” Craig Erlam, senior market analyst at Oanda, not only wants to see cryptos maturing, but says until the price action changes, he struggles to see institutional investors getting too involved.

- According to data from Google, “bitcoin” as a current search term greatly trails its popularity in late 2017, reports MarketWatch. At the start of May, the search term on Google scored a 9 on a scale from 0-100, compared to a 100 recorded in December 2017, the article continues. However, this might not mean people are disinterested, explains Jeff Dorman, chief investment officer at Arca. “For the most part, bitcoin is a household name now, people don’t need to search it to know what it is or how to invest in it,” Dorman said. “Much like Apple, everyone knows bitcoin by now.”

Opportunities

- HIVE Blockchain Technologies announced a strategic partnership and share swap agreement this week with Argo Blockchain, according to a press release from the company on Monday. This partnership could create the world’s largest business-to-business mining service provider aimed at large-scale enterprise and institutional customers.

- According to Steven Quirk, TD Ameritrade executive vice president, tens of thousands of the company’s clients are interested in futures tied to cryptocurrency, despite the fluctuation in the price of bitcoin. During a panel at CoinDesk’s Consensus 2019 in New York, Quirk said “we get calls, emails, 60,000 clients have traded something in this complex.” He continued by stating the intense interest is not just from millennials either, but from older retail investors too.

- The World Bank and the Commonwealth Bank of Australia have teamed up to enable recording of secondary market bond trading using blockchain technology, writes CoinDesk. Their successful recording of a secondary transaction on a distributed ledger for bond-i was announced on Wednesday. Bond-i is a blockchain-operated debt instrument, and according to the article, the transaction marks the first bond to have both issuance and trading recorded on a blockchain platform.

Threats

- Blockchain author Alex Tapscott and his investment firm NextBlock Global have been fined by the U.S. Securities and Exchange Commission (SEC) over securities violations. According to the SEC, the Canada-based firm has been offering securities not registered with the SEC “in any capacity” and false representations were made about the firm when soliciting investors, CoinDesk reports.

- According to experts at Coveware, ransomware activity is growing, with attacks up in the first quarter of 2019. Once hackers encrypt an infected computer, however, CoinDesk poses the question – then what? A study by ProPublica found that ransomeware solutions providers simply get rid of hackers by paying them off in cryptocurrency, charging a premium for their trouble.

- A third of all ether cryptocurrency is owned by just 376 “whales” as of May 1, reports CoinDesk. A whale, as defined by Chainalysis, are the top 500 holders of a cryptocurrency, excluding services, who store their holdings off exchanges. Chainalysis published a study on Wednesday discussing the control these individuals have, and while may not have any “meaningful impact” on the ETH price, they do increase intraday volatility in the crypto market when they make large sell-offs.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| S&P/TSX Global Gold Index | 181.22 | +3.97 | +2.24% |

| Gold Futures | 1,277.50 | -9.90 | -0.77% |

| Natural Gas Futures | 2.63 | +0.01 | +0.23% |

| S&P/TSX VENTURE COMP IDX | 609.15 | +9.67 | +1.61% |

| 10-Yr Treasury Bond | 2.39 | -0.08 | -3.08% |

| Nasdaq | 7,816.29 | -100.66 | -1.27% |

| Oil Futures | 62.70 | +1.04 | +1.69% |

| Hang Seng Composite Index | 3,713.51 | -100.23 | -2.63% |

| S&P 500 | 2,859.53 | -21.87 | -0.76% |

| DJIA | 25,764.00 | -178.37 | -0.69% |

| Korean KOSPI Index | 2,055.80 | -52.24 | -2.48% |

| Russell 2000 | 1,535.76 | -37.23 | -2.37% |

| S&P Energy | 468.23 | -3.43 | -0.73% |

| S&P Basic Materials | 342.01 | -2.73 | -0.79% |

| XAU | 67.49 | +0.20 | +0.30% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.63 | +0.11 | +4.29% |

| S&P/TSX Global Gold Index | 181.22 | -7.54 | -3.99% |

| 10-Yr Treasury Bond | 2.39 | -0.20 | -7.82% |

| Oil Futures | 62.70 | -1.06 | -1.66% |

| Gold Futures | 1,277.50 | +0.70 | +0.05% |

| S&P 500 | 2,859.53 | -40.92 | -1.41% |

| S&P Energy | 468.23 | -31.28 | -6.26% |

| Hang Seng Composite Index | 3,713.51 | -338.39 | -8.35% |

| DJIA | 25,764.00 | -685.54 | -2.59% |

| Korean KOSPI Index | 2,055.80 | -190.09 | -8.46% |

| Nasdaq | 7,816.29 | -179.80 | -2.25% |

| S&P Basic Materials | 342.01 | -19.58 | -5.41% |

| Russell 2000 | 1,535.76 | -31.83 | -2.03% |

| S&P/TSX VENTURE COMP IDX | 609.15 | -0.90 | -0.15% |

| XAU | 67.49 | -6.43 | -8.70% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.63 | +0.05 | +2.02% |

| 10-Yr Treasury Bond | 2.39 | -0.26 | -9.91% |

| DJIA | 25,764.00 | +324.61 | +1.28% |

| Oil Futures | 62.70 | +8.29 | +15.24% |

| S&P 500 | 2,859.53 | +113.80 | +4.14% |

| Gold Futures | 1,277.50 | -42.90 | -3.25% |

| S&P Energy | 468.23 | -10.07 | -2.11% |

| Nasdaq | 7,816.29 | +389.33 | +5.24% |

| Korean KOSPI Index | 2,055.80 | -170.05 | -7.64% |

| S&P Basic Materials | 342.01 | +5.18 | +1.54% |

| Russell 2000 | 1,535.76 | -9.34 | -0.60% |

| Hang Seng Composite Index | 3,713.51 | -103.09 | -2.70% |

| S&P/TSX Global Gold Index | 181.22 | -7.63 | -4.04% |

| S&P/TSX VENTURE COMP IDX | 609.15 | +0.75 | +0.12% |

| XAU | 67.49 | -7.01 | -9.41% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (03/31/2019):

Gazprom Neft PJSC

OTP Bank

Polski Koncern Naftowy ORLEN S

Equinor ASA

Royal Dutch Shell PLC

St Barbara Ltd

Alexandria Minerals Corp

Osisko Gold Royalties Ltd

IAMGOLD Corp

Pretium Resources Inc

TMAC Resources Inc

Wesdome Gold Mines Ltd

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry.

The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks.

The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months.

The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange.

The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver.

The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar.

The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500.

The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500.

The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period.

The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500.

The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500.

The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500.

The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500.

The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500.

The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500.

The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns.

The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

Frank Holmes was appointed non-executive chairman of the Board of Directors of HIVE Blockchain Technologies. Both Mr. Holmes and U.S. Global Investors own shares of HIVE, directly and indirectly.

ZEW Germany Expectation of Economic Growth is a survey on the question of economic growth in six months.

There is no guarantee that the issuers of any securities will declare dividends in the future or that, if declared, will remain at current levels or increase over time.

The Conference Board index of leading economic indicators is an index published monthly by the Conference Board used to predict the direction of the economy’s movements in the months to come. The index is made up of 10 economic components, whose changes tend to precede changes in the overall economy.

The University of Michigan Confidence Index is a survey of consumer confidence conducted by the University of Michigan. The report, released on the tenth of each month, gives a snapshot of whether or not consumers are willing to spend money.

The Vietnam Stock Index or VN-Index is a capitalization-weighted index of all the companies listed on the Ho Chi Minh City Stock Exchange. The index was created with a base index value of 100 as of July 28, 2000. The NIFTY 50 index is National Stock Exchange of India’s benchmark broad based stock market index for the Indian equity market. The BSE SENSEX is a free-float market-weighted stock market index of 30 well-established and financially sound companies listed on Bombay Stock Exchange. The 30 component companies which are some of the largest and most actively traded stocks, are representative of various industrial sectors of the Indian economy. A basis point is one hundredth of one percent, used chiefly in expressing differences of interest rates. The Jakarta Stock Price Index is a modified capitalization-weighted index of all stocks listed on the regular board of the Indonesia Stock Exchange. The index was developed with a base index value of 100 as of August 10, 1982.