Frank Talk

Are the Bitcoin ETFs Eating Gold’s Lunch?

Date Posted: March 4, 2024

Read time: 7 min

Bitcoin and gold were both top of mind at last week’s 2024 Investment U Conference in Ojai, California, which I had the privilege of presenting at. There was a rumor circulating that the Bitcoin price rally was sparked by a large financial institution recommending a 2% to 3% weighting to some of its high-net-worth clients. I can’t confirm this, but it’s being reported that Bank of America and Wells Fargo are now offering the Bitcoin ETFs to certain wealth management clients, joining Charles Schwab, Robinhood and others.

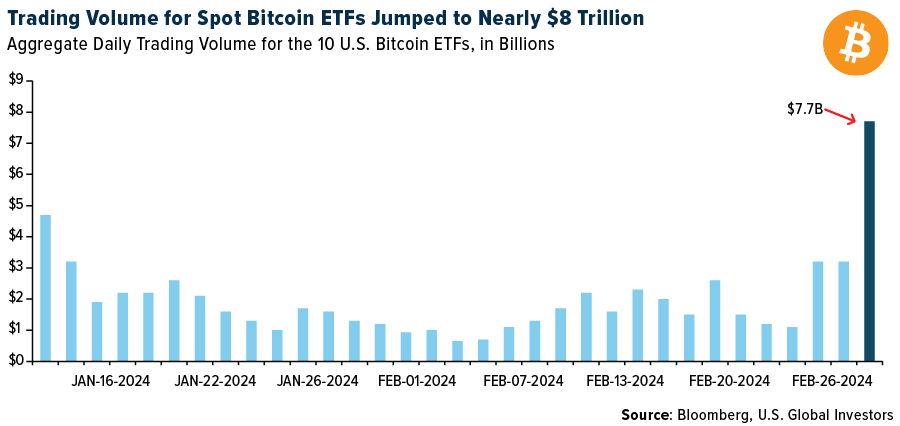

The price of Bitcoin pumped more than 45% in February, with around half of those gains recorded in the final week, as demand for the long-awaited spot Bitcoin ETFs hit a fever pitch. Combined daily trading volume for the 10 ETFs was a jaw-dropping $7.7 billion on Wednesday alone, fueled by institutional speculation and leveraged bets that pushed the price of the underlying asset to a near-record high.

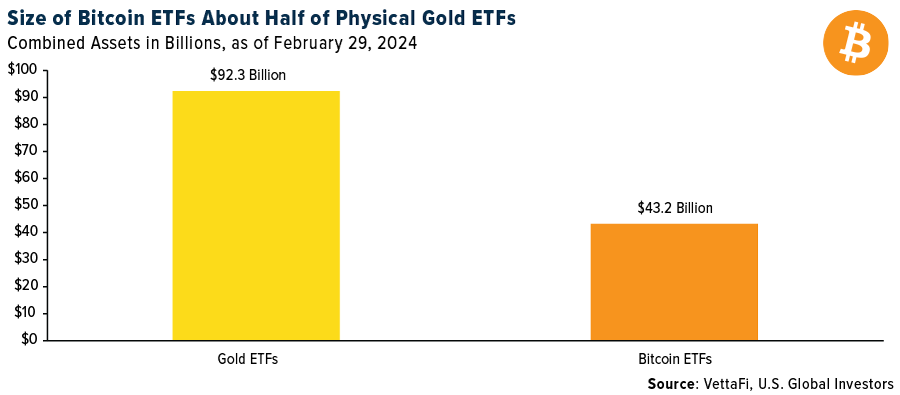

Remarkably, as of February 29, the combined value of the holdings in U.S.-based Bitcoin ETFs was roughly half the value of all known gold ETFs. The Bitcoin ETFs, which began trading in January, held $43.2 billion, while gold ETFs held $92.3 billion.

The cryptocurrency’s breathless catch-up to gold is reflected in the dramatic difference in sentiment between the two assets right now. CoinStats’ Crypto Fear and Greed Index is currently flashing Extreme Greed, while JM Bullion’s Gold Fear and Greed Index sits in Neutral territory.

A Tale of Two Assets: Risk and Reward

As you know, I often recommend a 10% weighting in gold, with half in physical gold (coins, bars, jewelry) and the other half in high-quality gold mining stocks, mutual funds and ETFs. I believe this weighting is suitable for most investors seeking a non-correlated asset, but especially conservative investors who might not have a long-term investment horizon.

For investors with a longer horizon, or those with a bigger risk appetite, there’s Bitcoin, whose volatility is about eight times greater than that of gold, its analog cousin. Whereas the precious metal has a 10-day standard deviation of ±3%, Bitcoin’s is ±25%.

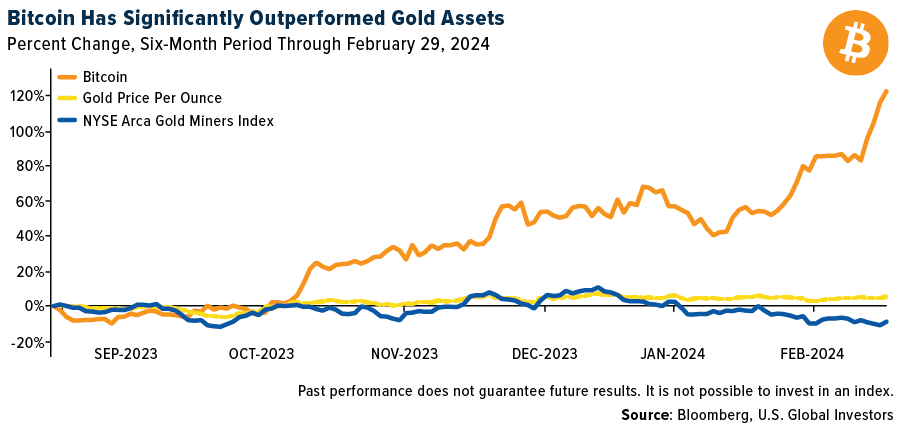

Though not guaranteed, with greater risk can come greater reward. For the six-month period through the end of February, Bitcoin more than doubled in price, surging close to 130%. Over the same period, gold increased a little over 5% while gold majors, as measured by the NYSE Arca Gold Miners Index, lost 9%.

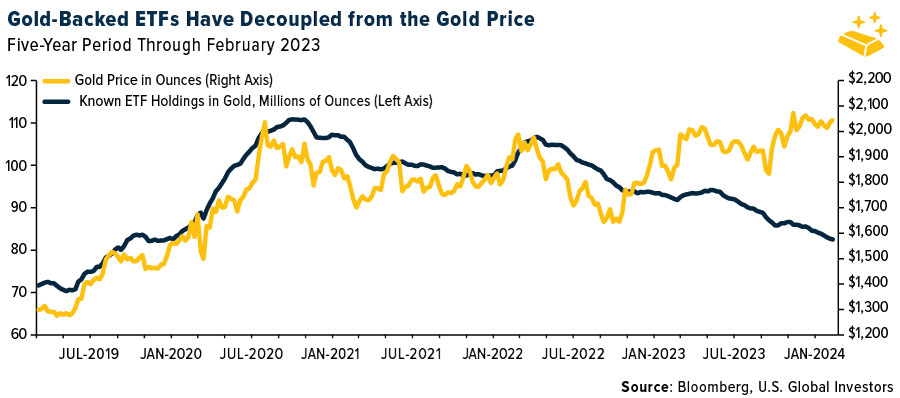

Whether the excitement surrounding Bitcoin is siphoning flows away from gold is unclear, but there does appear to be some disconnect between gold’s price action and investment levels. Historically, the gold price and holdings in gold-backed ETFs have traded in tandem, but starting in 2023, the two began to decouple, as you can see below. This could be caused by a number of factors, including changes in investor sentiment, monetary policy, portfolio balancing, currency fluctuations and more.

Gold Was Up, but Most Miners Couldn’t Expand Free Cash Flow

Analysts here at U.S. Global Investors looked at a basket of 85 gold mining stocks and found that, generally speaking, financial conditions worsened for the industry in 2023, despite the fact that gold had a relatively good year, jumping more than 13%.

Our analysis shows that, of those 85 names, only 47—or 55% of the basket—reported a positive free cash flow (FCF) yield as of December 31, 2023. That’s little changed from a year earlier, when 48 gold producers had positive FCF.

The same concerning results surfaced when we compared sales growth to changes in the price of gold. In December 2022, 23 out of 85 gold miners had positive FCF as well as sales growth that outpaced the yellow metal over the trailing 12 months (TTM); a year later, that figure fell to 10, representing only around 12% of the basket.

This means that fewer than one in 10 gold miners recorded an improvement in financial conditions… during a year when the price of gold was up.

For this reason and more, younger people just haven’t shown interest in gold stocks, which is a shame for the companies. We’re on the verge of history’s greatest transfer of wealth, with $84 trillion expected to be left to heirs over the next two decades. Perhaps more producers should take a page out of Bitcoin miners’ playbook and maintain gold on their balance sheets.

Will Central Banks Start Buying Bitcoin?

As I shared with you, some market watchers, including our shop, have noted that the driver of the gold price appears to have shifted in recent months. For decades, the yellow metal had an inverse relationship with real rates—rising when yields fell, and vice versa—but since the start of the pandemic in 2020, this pattern has broken down. During the 20 years before the pandemic, gold and real rates shared a highly negative correlation coefficient. Since that time, though, the correlation has turned positive, and the two assets now move in the same direction more often than not.

BMO Capital Markets commented on this in January, making the case that buying activity by central banks is the new driver of gold. It’s hard to argue against this position. Financial institutions, chiefly those in emerging economies, have been net buyers of the metal since 2010 in an effort to support their currencies and diversify away from the U.S. dollar.

For what it’s worth, Edward Snowden shared his 2024 prediction last week that a national government will be found to have been secretly buying Bitcoin, “the modern replacement for monetary gold,” the former NSA whistleblower said in a tweet.

This would be something, though I should point out that the government of El Salvador currently holds 2,381 bitcoins in its treasury. Its president, Nayib Bukele, says these holdings are up 40% after the recent price rally, and yet he has no intention of selling. El Salvador and the Central African Republic (CAR) are the only two countries so far that have made Bitcoin legal tender.

Past performance does not guarantee future results. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor. By clicking the link(s) above, you will be directed to a third-party website(s). U.S. Global Investors does not endorse all information supplied by this/these website(s) and is not responsible for its/their content.

Standard deviation is a quantity calculated to indicate the extent of deviation for a group as whole. The Gold Fear and Greed Index is based on a variety of data points, including physical gold premiums data, gold spot price volatility, social media sentiment around gold, proprietary retail activity for gold, and Google Trends data on Gold search terms. The Crypto Fear and Greed Index is based on volatility, social media sentiments, surveys, market momentum and more. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver.