Billionaire Investor: “Gold Has Everything Going For It”

Date Posted: June 14, 2019

Read time: 54 min

NULL

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

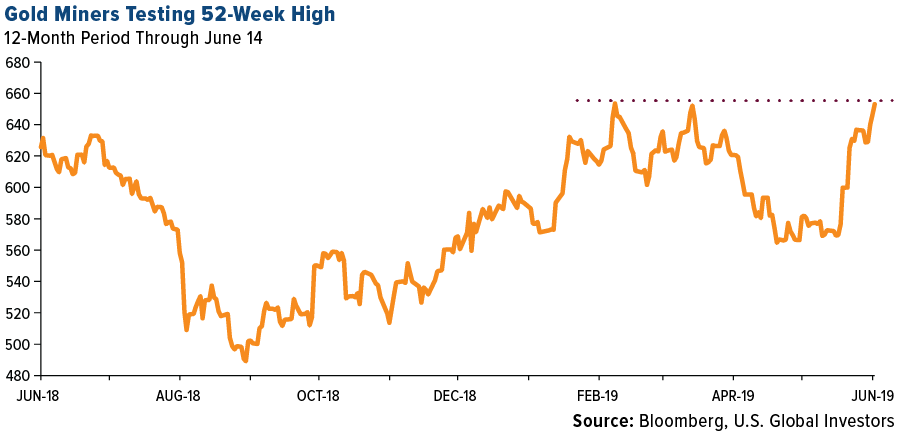

It was another strong week for gold, which managed to eke out its fourth straight week of positive gains. The price of the yellow metal broke above $1,350 an ounce on Friday, while gold miners, as measured by the NYSE Arca Gold Miners Index, tested their 52-week high.

Investors sought safe haven investments on a number of geopolitical risks, including protests in Hong Kong over an extradition bill and an attack on two oil tankers near Iran and the Strait of Hormuz, the world’s busiest sea lane through which a fifth of global oil consumption passes. After placing the blame on Tehran, President Donald Trump now faces a tough decision on how to respond, if at all.

Billionaire investor Paul Tudor Jones, founder of and hedge fund manager at Tudor Investment Corp., said in a Bloomberg interview this week that geopolitical disruptions have made gold his favorite trade in the next 12 to 24 months.

The yellow metal “has everything going for it,” he said, adding that if it can reach $1,400 an ounce, it will push to $1,700 “rather quickly.”

The biggest catalyst for such a move, Jones believes, is the ongoing U.S.-China trade war and the broader implication of shrinking global trade. After 75 years of globalization and free trade, we’re seeing a return to the use of tariffs and other protectionist policies.

Remember, it was the 1930 Smoot-Hawley tariff “that helped send the U.S. and world economy into a decade-long depression,” according to a 2015 article by now-National Economic Council Director Larry Kudlow and former Federal Reserve Board of Governors nominee Stephen Moore. Just last month, global manufacturers contracted for the first time since 2012 due in large part to trade tensions. World trade volume has also sunk the most since the financial crisis.

Meanwhile, Trump is threatening to impose tariffs on $325 billion in imports from China, in addition to the approximately $200 billion that are already being taxed. Trump and China’s president Xi Jinping are expected to meet later this month at the G20 summit in Japan, where hopefully the two leaders can hash out a resolution to the trade war.

Says Jones, this reversal in globalization “would make one think that it’s possible we go into a recession. It would make one think that rates in the United States go back down to the zero-bound level. Gold in that situation is going to scream. It will be the antidote for people with equity portfolios.”

Gundlach and Dalio Also Bullish on Gold

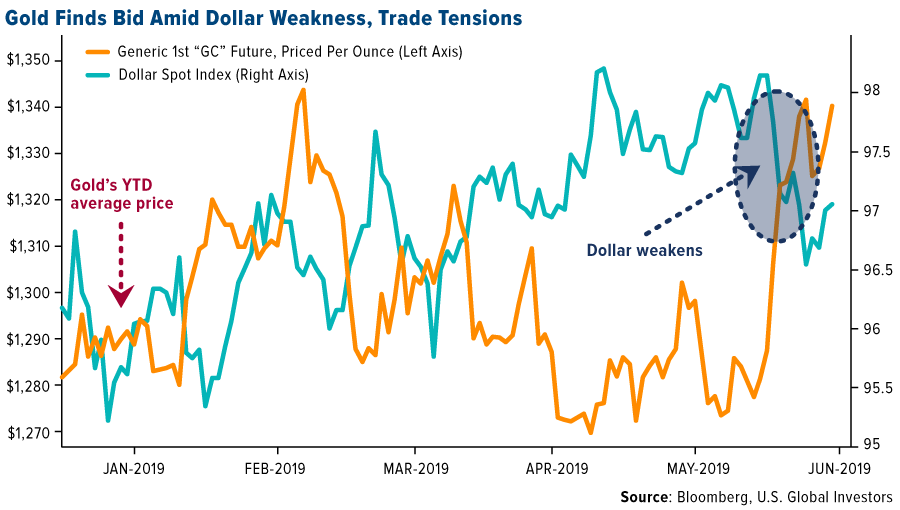

Jones isn’t the only billionaire hedge fund manager who thinks gold looks attractive right now. In a recent investor webcast, DoubleLine CEO Jeffrey Gundlach said that he’s “long gold.” His call is based on the belief that the U.S. dollar will be substantially lower by the end of the year. (Want a sure way to push the dollar down? Wipe out all $1.5 trillion in student loan debt in the U.S. Senator and presidential hopeful Elizabeth Warren will reportedly introduce a bill intended to do just that. What’s next—mortgages?)

And then, of course, there’s Ray Dalio, the world’s most profitable hedge fund manager. Dalio is a true believer in the 10 Percent Golden Rule, and according to Bridgewater’s SEC filings, he maintains significant positions in gold across all tiers in the industry.

Yield Curve Flashes a Warning Sign—Another Catalyst for Gold?

This week the yield curve inversion between the five-year and three-month Treasury yields passed a key threshold that, in the past, has telescoped a recession. In a tweet dated June 13, Bloomberg’s Lisa Abramowicz shared a chart of the yield inversion and commented: “Cam Harvey, the economist who first linked an inverted yield curve to economic declines, pinpoints the 3-month/5-yr curve as a key recession indicator once it inverts for a full quarter. It officially finished a full quarter of being inverted yesterday,” meaning Wednesday.

As for when we can expect a recession, Gundlach says he now believes there’s a 40 percent to 45 percent chance of one occurring within six months, a 65 percent change in the next year.

Oil Prices Jump on Tanker Explosions, but Don’t Overlook Norway

The big news involving oil this week was, as I mentioned earlier, the attacks on the two tankers near the Strait of Hormuz, among the world’s most important strategic chokepoints. Every day, as many as 17.2 million barrels of oil pass through the strait, if you can believe it. Because it’s the only way into and out of the Persian Gulf, both Saudi Arabia and the United Arab Emirates (UAE) have proposed building pipelines in order to bypass the historically dangerous shipping route.

Following the attack on Thursday, oil prices jumped as much as 4 percent.

But unless this incident escalates into something else—a U.S. military response, for instance—I see it as merely a short-term boost to oil.

A much more meaningful, long-term impact on oil and oil stocks is Norway’s divestiture from fossil fuels. The Scandinavian country’s sovereign wealth fund, known as the Norwegian Government Pension Fund, is the largest such fund in the world, valued at more than $1 trillion. Established in 1990 to invest in the profitable North Sea oilfields, the fund also invests heavily in international stocks, bonds and property in nearly 80 countries.

In the first quarter of this year, the fund delivered returns of $85 billion, its best quarter ever.

But following a recommendation from the country’s parliament, the fund will sell off some $13 billion of stocks in companies involved in the exploration and production of fossil fuels, including oil, gas and coal. The move is a huge step toward shifting assets into renewable energy.

The divestiture won’t have much of an impact on large-cap companies such as Royal Dutch Shell and Exxon Mobil, but it could have consequences for some mid-tier firms such as Anadarko Petroleum, Occidental Petroleum and EOG Resources.

Combined with OPEC’s recent forecast for weaker global oil demand, Norway’s decision—perhaps needless to say—is expected to be a headwind for the fossil fuel energy industry as whole.

All Eyes on Hong Kong

On a final note, I wish to express my support for the 7.4 million people in Hong Kong, especially the hundreds of thousands who have taken to the streets this past week to protest the recent amendment that would allow suspected criminals in Hong Kong to be extradited to mainland China.

The former British colony, now autonomous territory, is one of the world’s great success stories. For more than 20 years, it has ruled itself with its own government, currency and police force, and thanks to economic liberalization, it’s risen to become one of the top three financial hubs following New York and London. It consistently ranks among the most competitive places on earth, as well as one of the best to conduct business in.

Every nation wishes to have the freedom to make its own decisions with respect to its laws, economy, security and more, without interference from another sovereign state. That wish is at the heart of Brexit and, frankly, the election of Donald J. Trump. At the same time, it’s important to remember that government policy is a precursor to change.

Hong Kong official are now calling for the extradition amendment to be delayed. Let’s see if the protestors can manage to get it turned over permanently.

Looking for someone to make sense of the markets? Subscribe to Frank Holmes’ award-winning Frank Talk CEO blog! Click here to sign up!

Gold Market

This week spot gold closed at $1,341.85, up $1.04 per ounce, or 0.08 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 2.19 percent. The S&P/TSX Venture Index came in off 1.46 percent. The U.S. Trade-Weighted Dollar rose 1.04 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Jun-11 | PPI Final Demand YoY | 2.0% | 1.8% | 2.2% |

| Jun-12 | CPI YoY | 1.9% | 1.8% | 2.0% |

| Jun-13 | Germany CPI YoY | 1.4% | 1.4% | 1.4% |

| Jun-13 | Initial Jobless Claims | 215k | 222k | 219k |

| Jun-14 | China Retail Sales YoY | 8.1% | 8.6% | 7.2% |

| Jun-18 | Eurozone CPI Core YoY | 0.8% | — | 0.8% |

| Jun-18 | Germany ZEW Survey Current Situation | 6.1 | — | 8.2 |

| Jun-18 | Germany ZEW Survey Expectations | -5.8 | — | -2.1 |

| Jun-18 | Housing Starts | 1240k | — | 1235k |

| Jun-19 | FOMC Rate Decision (Upper Bound) | 2.5% | — | 2.5% |

| Jun-20 | Initial Jobless Claims | 220k | — | 222k |

Strengths

- The best performing metal this week was palladium, up 7.97 percent on hedge funds boosting the net-long position to a 10-week high. Gold traders were bullish on their outlook for the yellow metal this week due to growing geopolitical tensions and the prospect of the Federal Reserve cutting rates, according to the weekly Bloomberg survey. Gold saw its fourth weekly gain.

- Bloomberg reports that an ETF fund trader bought around $82 million worth of the iShares Gold Trust ETF, which was the fund’s largest block trade in almost two months. Central banks are also stocking up on gold. China has now added to its reserves for a sixth straight month. The People’s Bank of China has expanded its gold holdings by more than 70 tons since December. Turkey’s gold reserves rose $968 million from the previous week, according to central bank data.

- In an array of different global currencies, gold has never been more expensive – from Australia to Brazil to Sweden. Bloomberg reports that hedge funds boosted their long position in gold bullion by the most in almost 12 years last week.

Weaknesses

- The worst performing metal this week was silver, down just 1 percent on little news. Although gold is moving up, it has mostly pared its gains due to a stronger U.S. dollar. “The fact that gold has managed to trade over $1,340 is a positive sign for next week,” said Chintan Karnani, chief market analyst at Insignia Consultants. Gold touched 52-week highs on Friday, only to fall back down.

- South Africa, once the world’s top producer, saw its gold output decline yet again in April and is now on a 19-month contraction streak. Bloomberg reports this is the longest streak of declines since the financial crisis a decade ago.

- Who is now the top gold producer in Africa? Ghana. The small West African nation has dethroned South Africa to become the top producer on the continent as it benefits from lower cost mines, friendlier policies and new development projects. Cardinal Resources could be a big beneficiary from the increased investments in projects in the country as their Namdini Project has 5.1 million ounces of proven and probable reserves, which is of sufficient scale for a major gold miner to have interest in its acquiring.

Opportunities

- One policy both sides of the aisle are discussing? Managing the U.S. dollar. Senator Elizabeth Warren, who is running for president, says that managing the value of the dollar could help boost exports. President Donald Trump continues to slam the Federal Reserve for high interest rates, saying the euro and other currencies are devalued against the dollar. Historically, a weaker dollar has been positive for the price of gold.

- A few notes from gold bulls this week. According to Rhona O’Connell, head of market analysis at INTL FCStone, gold may hit $1,400 an ounce this year as investors are looking to hedge risk. O’Connell says that “all the dominant asset classes have a question mark over them at the moment, which is generally when gold comes into play.” Billionaire hedge fund manager Paul Tudor Jones expressed his support for gold this week in a Bloomberg interview. Jones said if gold can reach $1,400, then it will follow to $1,700 shortly after. Edel Tully from UBS says that gold represents “insurance” against geopolitical risks surrounding the trade war.

- Nikos Kavalis, director of research at Metals Focus, says that silver may hit $18 per ounce this year due to gold rising on the back of a weakening dollar and a Fed rate cut. “We maintain a cautiously optimistic outlook for silver and this is very much reliant on our expectation for gold." Agnico Eagle announced this week that it has offered to acquire Alexandria Minerals, which rose over 44 percent for the week.

Threats

- The Trump administration’s urgency to end Fannie Mae and Freddie Mac’s conservatorships absent a clear guarantee of their securities, is worrying traders on Wall Street, reports Bloomberg. Credit rating companies, financial firms and real estate agents say such a move would be a disaster, as it might prompt big asset managers to curtail their bond buying. This in turn could dry up some of the financing that keeps the mortgage market humming, the article continues.

- Financial concerns are affecting the mental and physical health of relatively wealthy Americans, according to a study by Bank of America Corp. Out of 1,000 respondents, 59 percent say financial concerns impact them mentally, while 56 percent say their physical health has been hurt.

- The biggest union in South Africa’s platinum industry, the Association of Mineworkers and Construction Union, is demanding wage increases as much as 48 percent from producers in the world’s top supplier of the metal, reports Bloomberg. This sets up the state for a tough fight in upcoming pay talks. Now the producers are gearing up for the hefty demands, says Jana Marais, a spokeswoman for Anglo Platinum. “We expect another tough round of negotiations,” she explains. “Our employees’ disposable income has been under increasing pressure in a difficult economy, while the platinum industry also continues to face significant challenges.” In related news, Toyota has innovated to cut platinum use in its fuel-cell vehicles – breaking expectations that these vehicles can help offset the expected losses in PGM demand caused by adoption.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 0.41 percent. The S&P 500 Stock Index rose 0.48 percent, while the Nasdaq Composite climbed 0.70 percent. The Russell 2000 small capitalization index gained 0.53 percent this week.

- The Hang Seng Composite gained 0.73 percent this week; while Taiwan was up 1.11 percent and the KOSPI rose 1.11 percent.

- The 10-year Treasury bond yield remained flat, closing at 2.085 percent.

Domestic Equity Market

Strengths

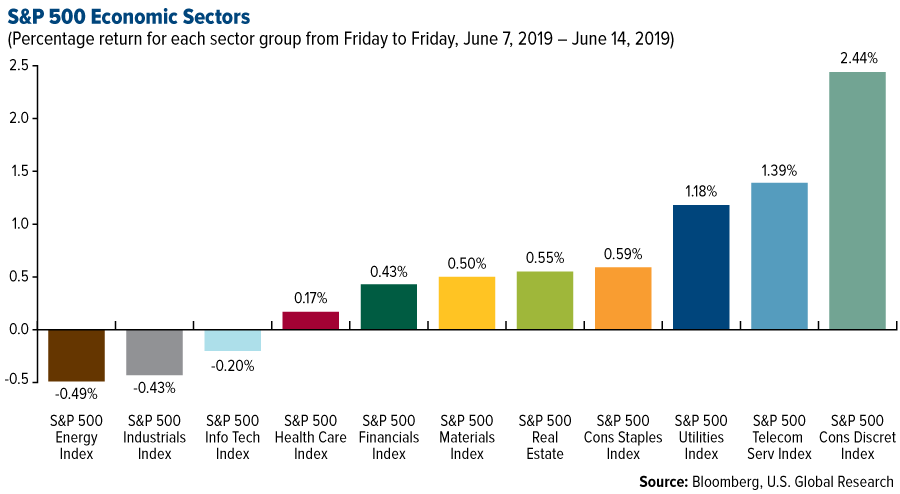

- Consumer discretionary was the best performing sector of the week, increasing by 2.44 percent versus an overall increase of 0.62 percent for the S&P 500.

- CF Industries was the best performing stock for the week, increasing 9.45 percent.

- PetSmart Inc.-controlled Chewy Inc. surged in its first day of trading after raising $1.02 billion in an initial public offering. Investors are betting that pet owners will do more of their pet shopping online. Chewy’s shares rose as much as 88 percent in the first hour of trading Friday from the $22 offer price. After opening at $36, they were up 58 percent to $34.82 at 1:48 p.m., giving the company a market value of about $13.88 billion.

Weaknesses

- Energy was the worst performing sector for the week, decreasing by 0.49 percent versus an overall increase of 0.62 percent for the S&P 500.

- Allergan was the worst performing stock for the week, falling 8.82 percent.

- Broadcom Inc. tumbled on Friday after the chipmaker cut its full-year sales outlook, citing the impact of the trade war between China and the U.S. While the weaker guidance didn’t come as a shock, the scale of the reduction caught some analysts off guard, and it was seen as further diminishing the idea that semiconductor demand would rebound in the second half of the year.

Opportunities

- Corners of the stock market are pricing in a “Trump recession” and investors should get ready for a bounce, according to JPMorgan Chase & Co. strategist Marko Kolanovic. Concerns that President Donald Trump’s trade war against China will sink the economy have chased investors out of economically sensitive stocks and into defensive shares, Kolanovic said.

- Uber, MasterCard, Visa and other big companies have reportedly signed on to Facebook’s blockchain efforts. The Silicon Valley tech giant is expected to formally announce what it has been building next week.

- Raytheon and United Technologies announced a deal to form a $120 billion aerospace and defense giant.

Threats

- With arguably two of the year’s biggest events looming for markets, Bank of America has analyzed what’s at stake for investors. The S&P 500 may rise above 3,000 should the Federal Reserve continue a dovish pivot at its policy meeting next week and a trade deal be reached between the U.S. and China at the Group of 20 summit the week after, according to strategists led by Michael Hartnett. Should the Fed prove hawkish and no trade agreement emerge, the index risks falling below 2,650, their analysis showed. In the event the Fed stays dovish but no trade deal is struck at the G-20 meeting, the S&P 500 may decline to 2,750.

- The stock market’s biggest source of buying power may soon disappear. Buybacks, which have accounted for $3.7 billion worth of stock market purchases over the past five years and have been the biggest source of demand over that time, are slowing down, and that could make the next crash even more painful, according to INTL FCStone.

- U.S. equity forecasters can’t get their story straight. In the last month, 10 of 24 strategists tracked by Bloomberg cut 2019 profit estimates for the S&P 500. But exactly none has lowered the end of year price prediction for the index. “We acknowledge that we underestimated the potential trade war damage,” said Brian Belski, chief investment strategist at BMO Capital Markets who this week cut his S&P 500 profit prediction to $165 a share from $174. “Despite this revision, we see no reason to alter our year-end S&P 500 price target of 3,000 since our models and analysis still suggests that this level remains highly achievable.”

The Economy and Bond Market

Strengths

- U.S. retail sales increased in May and sales for the prior month were revised higher, writes Reuters, suggesting a pick-up in consumer spending. The Commerce Department said on Friday retail sales rose 0.5 percent last month. Data for April was revised up to show retail sales gaining 0.3 percent, instead of dropping 0.2 percent as previously reported.

- U.S. industrial production rose in May, a welcome sign of strength in the sector after a spate of weak readings this year, reports the Wall St. Journal. Industrial production rose a seasonally adjusted 0.4 percent in May from the prior month, the Federal Reserve said Friday.

- President Trump has suspended tariffs on Mexican goods, saying "I am pleased to inform you that The United States of America has reached a signed agreement with Mexico," in a Tweet last week. "The Tariffs scheduled to be implemented by the U.S. on Monday, against Mexico, are hereby indefinitely suspended."

Weaknesses

- U.S. consumer sentiment weakened in June and long-term inflation expectations dropped to the lowest on record. The University of Michigan’s preliminary sentiment index fell to 97.9 from 100 in May.

- A U.S. business conditions gauge, with indicators from services to manufacturing and hiring, dropped this month by the most on record, reports Bloomberg. The headline index, compiled by Morgan Stanley, is another sign that the world’s largest economy is slowing, the article continues.

- U.S. initial jobless claims unexpectedly rose last week, writes CNBC, which could add to concerns that the labor market was losing steam after job growth slowed sharply in May. While layoffs remain relatively low, the third straight weekly increase in claims suggests some softening in labor market conditions.

Opportunities

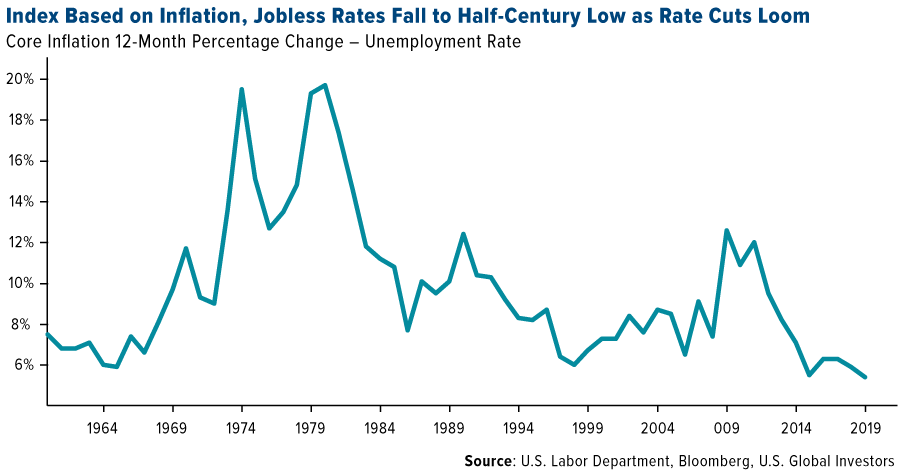

- U.S. consumers are in their best position in more than half a century even before the Federal Reserve considers interest-rate cuts, according to Yoav Sharon, a money manager at Driehaus Capital Management LLC. Sharon cited a version of the misery index, the sum of inflation and unemployment rates. He looked at the core consumer price index, excluding food and energy, which was 2 percent higher in May than a year earlier. Adding last month’s jobless rate brought the misery index to 5.6 percent, the lowest since 1966.

- During its June 18-19 meeting in Washington, the Federal Open Markets Committee (FOMC) will lay the groundwork for a possible cut in the Fed funds rate next month, according to various strategists and economists.

- With most states seeing tax collections rise at a faster-than-expected pace, governments have been setting aside more money to help them avert deep spending cuts the next time the economy contracts, write Bloomberg News. According to a report from the National Association of State Budget Officers, those rainy-day funds have swelled to about $68.2 billion, with the median state having enough to cover about 7.5 percent of its annual budget, the most on record. Next year, those reserves are expected to grow to $74.7 billion.

Threats

- Stanley Druckenmiller warns the U.S. is headed for losses in its trade war with China. "I will go to my grave — you’re not going to tell me that protectionism is as good as free trade," Druckenmiller said at a recent event hosted by the Economic Club of New York. "I just don’t believe it."

- President Donald Trump said Iran was responsible for attacks on oil tankers in the Persian Gulf this week. “Iran did do it and you know they did it,” Trump said Friday during a phone interview with Fox News. “You saw the boat at night,” he said. The president’s comments follow American officials’ release of images they said show that Iran was involved in an attack on an oil tanker near the entrance to the Persian Gulf on Thursday, one of two incidents that have raised tensions between the U.S. and the Islamic Republic. Iranian officials have rejected the accusation.

- Bank of America has raised its U.S. junk bond spread target and predicts a higher pace of defaults. The credit market is "misreading the Fed’s intentions to cut rates at a time when risk assets are nearly fully priced. Something has to give here, and either risk needs to be marked down or rates need to go higher," said analysts from the bank.

Energy and Natural Resources Market

Strengths

- The best performing major commodity for the week was lumber, which marked its biggest weekly gain in 24 years; rising 22.32 percent on news Canadian producers were significantly curtailing production capacity. Iron ore rose back above $100 per ton this week as the physical market for demand remains tight. South African stocks saw the benefits from higher prices as its main stock index rose for a seventh day on the news. Iron ore futures in China closed at the highest since 2014 on Wednesday due to hopes for China to increase infrastructure spending. Base metals rebounded from a five month low on the news as well.

- Rio Tinto Group, the world’s number-two miner, released thousands of pages of contracts it signed with governments regarding exploration and mining projects, reports Bloomberg. This is a big positive signal in the industry’s efforts to become more transparent. Another top miner, Glencore, released its first human rights report to address allegations of abuses and detail how the company is working to make sure workers are safe.

- Venture Global LNG Inc. has made a deal to send Poland’s PGNiG 2.5 million tons of LNG from the not yet built terminal in Louisiana. This is up 1 million from a previous agreement. The deal is part of the effort of the Trump administration to see more gas sent overseas, reports Bloomberg. Exxon Mobile Corp. agreed to pay $10 million for the rights to some of FuelCell Energy Inc.’s technology patents just hours after the company said it might go under, writes Bloomberg’s David Baker.

Weaknesses

- The worst performing major commodity for the week was coffee, which fell 4.90 percent on news that dry weather in Brazil, the world’s top grower and exporter, would lead to an accelerated harvest. Oil is set for another weekly loss. Even as tankers were attacked in the Middle East, the deepening trade war and growing U.S. stockpiles overshadowed the news. WTI crude fell on Wednesday after a report showed U.S. stockpiles rose 2.21 million barrels last week to the highest level since July 2017, reports Bloomberg. According to Morgan Stanley, estimates for March and April are pointing to year-on-year oil demand declines due to slowing global growth and trade tensions.

- The bearish signs for copper continue to flash. The red metal’s 50-day moving average fell below its 200-day moving average – known as a death cross. Copper has been hurt by the ongoing trade war as it rattles concerns for demand. Workers began a planned strike Friday morning at Codelco’s third largest copper mine as three unions rejected the company’s offer for a contract.

- The cost for storing radioactive waste from nuclear power plants – which is paid by the U.S. government and not private companies – is set to soar to $35.5 billion. The Energy Department estimates that nuclear waste storage liabilities will continue to increase every year. In BP’s annual review of world energy, global carbon emissions rose the most in seven years in 2018.

Opportunities

- Romania is reopening three mines for the production of rare earth metals in an attempt to attract investments in electric battery plants. Economy Minister Niculae Badalau said this week that Romania is hoping to become a member of the European Battery Alliance and ensure that at least one factory to produce electric batteries will be located in the nation.

- Although the trade war is still raging on between the U.S. and China, a deal could be hugely positive for American natural gas. According to Morgan Stanley, a deal between the nations could result in large Chinese purchases of LNG, which would help shrink the trade deficit. U.S. share of China’s gas imports could reach 21 percent by 2025 versus 5 percent without a deal.

- According to the Environment Ministry, Japan has approved a long-term strategy to achieve carbon neutrality by 2050 and cut greenhouse gas emissions by 80 percent by that time as well. Bloomberg reports that Japan is submitting its plan to the United Nations before the G-20 summit.

Threats

- Geopolitical tensions in the Middle East rose high this week after two oil tankers were attacked near the entrance to the Persian Gulf on Thursday. The U.S. has blamed Iran.

- President Trump told reporters this week during a meeting with Polish President Andrzej Duda that he is considering using U.S. sanctions to stop construction of the Nord Stream 2 pipeline between Russia and Germany, reports Bloomberg. The U.S. is opposed to the pipeline out of concern for Russia pressuring Europe to be dependent on its supply. Currently about one third of Europe’s natural gas comes from Russia.

- “A lot of the risk capital that had gone into the lithium sector is now running into cannabis,” according to Tobias Tretter, managing director of Commodity Capital AG. As seen in the chart below, investments in the cannabis company Canopy Growth is rising while Nemaska Lithium is falling. Bloomberg’s Laura Millan Lombrana writes that many of the sessions at the Lithium Supply and Markets Conference in Chile this week had half-empty rooms and there was a lack of investors and fund managers in attendance.

Emerging Europe

Strengths

- Greece was the best performing country this week, gaining 3.9 percent. Greek equites continue to perform well, with banks leading the gains. Shares of Piraeus Bank rose 21 percent over the past five days.

- The Russian ruble was the best performing currency this week, gaining 62 basis points against the U.S. dollar. There is high interest in Russia on the back of no new sanctions. According to Renaissance Capital, Russia is the largest overweight for actively managed, global EM funds.

- Materials was the best performing sector among eastern European markets this week.

Weaknesses

- Turkey was the worst performing country this week, losing 3.2 percent. Tension between Turkey and the Unites States is increasing as the deadline for the delivery of S-400 missiles from Russia is approaching. The U.S. threatened to impose sanctions on the country for buying military equipment from Vladimir Putin.

- The Hungarian forint was the worst performing currency this week, losing 1.9 percent against the U.S. dollar. The liquidity surplus in the interbank market is falling. The net sum of overnight deposits and loans held at the central bank fell to 86 billion forint as of June 12, the lowest since November.

- Industrials was the worst performing sector among eastern European markets this week.

Opportunities

- Russian exports of fuel oil are shrinking while exports of gasoline are at seasonal highs thanks to modernization efforts across the nation’s refineries. Russia accounts for roughly 40 percent of global fuel-oil production, but in the face of shrinking demand and new rules from the International Maritime Organization that will limit the sulfur content in marine fuel, Russian refineries have been investing in upgrades to reduce their fuel-oil output.

- Turkish equites are trading in a well-over-sold territory at about 50 percent discount to the MSCI Emerging Market Index in terms of 12 months forward P/E. Once the Istanbul elections are over, paving the way to a potential four-year period without elections, and once Turkey can make progress on the issue of taking the delivery of the S-400 missiles from Russia, we could see a significant rally in Turkish assets.

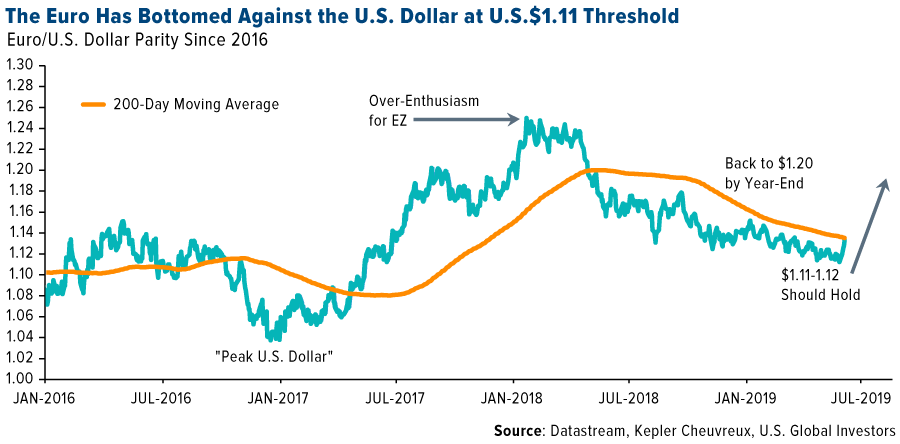

- Kepler Cheuvreux, in Strategic Frame’s research published June 10, stated that the euro has bottomed against the dollar at the US 1.11 threshold. A stronger euro would simply emphasize that Europe is no longer in the front line of stress in the world.

Threats

- After last week’s Draghi announcement that the European Central Bank (ECB) will provide more stimulus if Europe’s economic data weakens, some investors worry the bank has no room to provide more stimulus. Rates in Europe are already negative and the bank’s bond purchases are constrained by rules stating it cannot own more than 33 percent of any country’s outstanding debt.

- The Norwegian parliament approved the country’s decision to divest the $1 trillion sovereign wealth fund from oil and gas exploration firms and invest more in renewable energy companies that are listed on stock markets. The Government Pension Fund Global will now gradually sell off an $8 billion stake in 134 oil and gas firms, affecting those solely involved in fossil fuel exploration. The fund may replace them with companies investing in wind, solar and other green energy projects.

- The MSCI Emerging Europe Index has gained 10 percent since mid-May, and now investors may see some correction. In the past month Russia outperformed, gaining 16 percent, followed by Greece up 16 percent and Romania up 12.6 percent.

China Region

Strengths

- The best performing index in the region for the week was China’s Shanghai Composite, which rose 2.11 since trading before holiday last Friday.

- The best-performing sector in Hong Kong’s Hang Seng Composite Index since reopening after the Friday holiday last week was consumer services, up 2.19 percent.

- China’s retail sales data for the May measurement period offered a ray of light on otherwise disappointing data today, as the retail sales print came in up 8.6 percent year over year, ahead of expectations for only 8.1 percent.

Weaknesses

- The worst-performing index in the region for the week was Malaysia’s FTSE Bursa Malaysia Kuala Lumpur Composite, which declined by 59 basis points.

- The poorest-performing sector in Hong Kong’s Hang Seng Composite Index this week was telecommunications, which declined by 2.06 percent.

- Fixed assets investment (FAI) in China declined to only 5.6 percent year-over-year growth, below expectations for a 6.1 percent print, while industrial production for the May period came in at 5.0 percent year-over-year growth, missing estimates for a 5.4 percent print. Both data were down from their prior readings as well.

Opportunities

- Vice Premier Liu He—a by-now familiar face to readers, as China’s chief trade negotiator amid the recent rounds of trade war shuttle talks—stressed that a long-term upside to external pressures in China will seek to strengthen its domestic capital markets and consumption all while cutting financial risk and innovating and diversifying with respect to supply chain issues, all items undoubtedly on China’s long-term agenda anyway. Thus the upside of the turmoil may be a quickening of the changes already afoot.

- While it may be a sign of the U.S. losing some cache with respect to the IPO scene for Chinese markets—or who knows, perhaps just a sign of these troubled times for trade between the two nations—Hong Kong can nonetheless celebrate in landing the announcement from NYSE-listed Chinese tech juggernaut Alibaba Group Holding Company for a $20 billion secondary stock offering in Hong Kong.

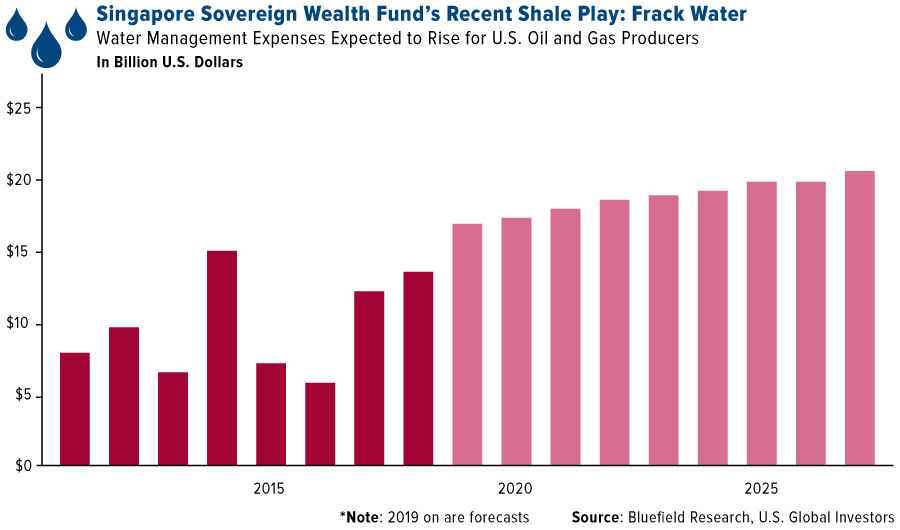

- Here’s an interesting twist for you: we’re highlighting as an FYI the relatively recent Singaporean sovereign wealth fund’s investment into a privately-held Texas wastewater company that specializes in handling oil-drilling water from booming U.S. shale operations. The Wall Street Journal reported recently that WaterBridge Resources—which was seeded by Texas investment firm Five Point Energy with some $200 million in only 2016, and which only acquired its first Permian Basin wastewater-handling assets in 2017—has now achieved a valuation of $2.8 billion following the Singaporean investment. While WaterBridge now also has the largest system of wastewater pipelines and disposal-well capacity for handling wastewater generated by fracking operations, the WSJ also reports that company has supposedly scrapped its IPO plans.

Threats

- The threat of U.S.-China trade war escalation continues, with obvious potential regional and global implications. While consensus seems to expect no major resolution in trade issues in the meantime, there remains an optimistic contingent that perhaps a G20 sit-down between Donald Trump and Xi Jinping might lead to a continuation of talks—a resetting of the trade “truce”—if the U.S. president feels the deal is acceptable and progress can be made once again. On the other hand, President Trump has also threatened to raise tariffs even further than expected, and in any case, has said he’ll wait until after the G20 meeting to decide. As Huawei issues and Hong Kong protests exacerbate pressure on China’s Xi Jinping—who also faces the prospect of slowing growth at home—the G20 meeting may indeed present an intriguing decision point for President Xi. The initial trade truce, struck back in December 2018 at the G20 meeting, has showed a truce can be reached for an interim period. The threat may be if it can’t.

- As mentioned above, the hotly-contested (or maybe hotly “protested” is a fairer statement) Hong Kong extradition bill—and the surrounding protests over it—continue to raise alarm internationally (and most fervently among Hong Kongers) over potential mainland Chinese interference in Hong Kong affairs and over the security and stability of Hong Kong’s longstanding “one country, two systems” status as a free speech, common law, capitalist SAR vis-à-vis the Communist mainland that has served as the bedrock of Hong Kong’s ties to the broader developed and financial world. The world is watching.

- A New York Times article this week highlighted the decline in U.S. tourism from China year-over-year from 2017 to 2018, with the expected and obvious conclusions that those numbers will probably decline again in the present year given the current situation. This is somewhat unfortunate, given that the average Chinese visitor to the United States spends an average of some $6,700 per stay, almost 50 percent more than other international visitors. From some 3.2 million visitors in 2017, 2018’s number of visiting Chinese fell to 2.9 million. Over the previous decade, the number of Chinese tourists had climbed by an average annual growth rate of 23 percent. (Perhaps there is a silver lining to be found in other countries’ tourism numbers, since the swelling ranks of Chinese middle class travelers must be going somewhere.)

Blockchain and Digital Currencies

Strengths

|

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended June 14 was Equal, up 600.17 percent.

- The cryptocurrency exchange Coinbase has expanded its Visa debit card service to six European countries, reports Coindesk, enabling its customers in that region to spend their digital assets. The exchange first rolled out a crypto Visa debit card in April, at the time exclusively for users based in the U.K.

- According to technical analysis from Fundstrat Global Advisors, the recent pullback in cryptocurrencies is over and investors should consider buying. Strategist Rob Sluymer wrote in a note that investors should remain patient following the big surge in May, reports Bloomberg, and that now there’s early evidence of renewed potential for gains. Sluymer predicts a rally for bitcoin in the $8,800 to $9,000 range.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended June 14 was Themis, down 67.17 percent.

- The price of bitcoin experienced a minor pullback from $7,900 to around $7,500 at the start of the week, CCN Markets.Over the last seven days the price has fallen over 10 percent, the article continues, leading technical analysts to ponder the possibility of an extended pullback. Crypto Thies points out that the relative strength index (RSI) of the digital asset touched the 92-95 range, which historically has led the price of an asset to drop by around 30 percent.

- Few women are contributing code to major cryptocurrency projects, according to data collected from a Github study over the top 100 blockchain projects. The study shows that a deep lack of gender diversification exists, with women committing only about 5 percent of the code, reports Coindesk.

Opportunities

- Traditional asset managers like Fidelity are joining crypto powerhouses to enter the emerging market in hopes of bridging the gap between the asset class and institutional investors, reports NewsBTC.com. In fact, just last month, sources familiar with the matter told Bloomberg News that investment giant E*Trade is close to launching a crypto trading desk.

- A highly anticipated next step for securing the bitcoin network, known as lightning network “watchtowers,” are coming soon, reports CoinDesk. It is these watchtowers that have long been considered a missing piece of the cryptocurrency’s lightning layer. The article explains they are crucial for preventing fraud on the experimental, off-chain network that could make bitcoin payments faster and more scalable. Now, version 0.7 of the LND software is set to release at an undisclosed date in June.

- Payments company square has hired former Google director Steve Lee as the first member of its new crypto team, reports Coindesk. Lee spent eight years with Google, leaving the company in 2015, and has since become a Bitcoin Optech contributor. According to the article, Lee is also an angel investor who lists Lyft, Pinterest and Yardbarker as key exits.

Threats

- During the G20 meeting in Fukoka, Japan, over the weekend, the group of nations reaffirmed it will align with standards for anti-money laundering (AML) and countering the funding of terrorism, set to be finalized by the Financial Action Task Force, reports CoinDesk. The new standards, which theoretically will protect the crypto industry, are in fact expected to set tough operating procedures for exchanges. Blockchain analysis firm Chainalysis recently argued that the expected changes would be unrealistic and harmful for the crypto industry.

- The chief of the Philippines central bank has warned over the risks of growing cryptocurrency use, reports CoinDesk. As a surge in use has continued, the central bank stresses that it does not intend to endorse any cryptocurrency. Nevertheless, the institution said it aims to regulate the technology when used for delivery of financial services, the article continues, particularly for payments and remittances.

- The Financial Industry Regulatory Authority (FINRA) has fined and suspended an investment adviser over undeclared cryptocurrency mining activities, writes CoinDesk. On June 10, FINRA published a letter of acceptance, waiver and consent, stating that Kyung Soo Kim had been working at Merrill Lynch and was registered with the watchdog as a general securities representative through the firm from March 2014. In December 2017, Kim formed a company called S Corporation to engage in crypto activities and also struck a deal with another firm to build and operate hardware and software for the mining effort. However, he failed to provide written notice of the mining venture to his employer, thus breaking two of FINRA’s rules, the article explains.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| S&P/TSX Global Gold Index | 205.10 | +5.69 | +2.85% |

| Gold Futures | 1,344.60 | -1.50 | -0.11% |

| Natural Gas Futures | 2.39 | +0.05 | +2.27% |

| S&P/TSX VENTURE COMP IDX | 586.97 | -9.57 | -1.60% |

| 10-Yr Treasury Bond | 2.09 | +0.00 | +0.10% |

| Nasdaq | 7,796.66 | +54.56 | +0.70% |

| Oil Futures | 52.53 | -1.46 | -2.70% |

| Hang Seng Composite Index | 3,620.02 | +26.25 | +0.73% |

| S&P 500 | 2,887.01 | +13.67 | +0.48% |

| DJIA | 26,089.61 | +105.67 | +0.41% |

| Korean KOSPI Index | 2,095.41 | +23.08 | +1.11% |

| Russell 2000 | 1,522.44 | +8.05 | +0.53% |

| S&P Energy | 447.48 | -2.21 | -0.49% |

| S&P Basic Materials | 360.98 | +1.78 | +0.50% |

| XAU | 75.81 | +1.48 | +1.99% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.39 | -0.21 | -8.11% |

| S&P/TSX Global Gold Index | 205.10 | +22.96 | +12.61% |

| 10-Yr Treasury Bond | 2.09 | -0.29 | -12.17% |

| Oil Futures | 52.53 | -9.49 | -15.30% |

| Gold Futures | 1,344.60 | +40.90 | +3.14% |

| S&P 500 | 2,887.01 | +36.05 | +1.26% |

| S&P Energy | 447.48 | -23.94 | -5.08% |

| Hang Seng Composite Index | 3,620.02 | -150.49 | -3.99% |

| DJIA | 26,089.61 | +441.59 | +1.72% |

| Korean KOSPI Index | 2,095.41 | +2.63 | +0.13% |

| Nasdaq | 7,796.66 | -25.49 | -0.33% |

| S&P Basic Materials | 360.98 | +21.80 | +6.43% |

| Russell 2000 | 1,522.44 | -25.83 | -1.67% |

| S&P/TSX VENTURE COMP IDX | 586.97 | -20.57 | -3.39% |

| XAU | 75.81 | +7.51 | +11.00% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.39 | -0.47 | -16.29% |

| 10-Yr Treasury Bond | 2.09 | -0.55 | -20.75% |

| DJIA | 26,089.61 | +379.67 | +1.48% |

| Oil Futures | 52.53 | -6.08 | -10.37% |

| S&P 500 | 2,887.01 | +78.53 | +2.80% |

| Gold Futures | 1,344.60 | +37.00 | +2.83% |

| S&P Energy | 447.48 | -37.76 | -7.78% |

| Nasdaq | 7,796.66 | +165.75 | +2.17% |

| Korean KOSPI Index | 2,095.41 | -60.27 | -2.80% |

| S&P Basic Materials | 360.98 | +14.33 | +4.13% |

| Russell 2000 | 1,522.44 | -27.19 | -1.75% |

| Hang Seng Composite Index | 3,620.02 | -238.07 | -6.17% |

| S&P/TSX Global Gold Index | 205.10 | +12.28 | +6.37% |

| S&P/TSX VENTURE COMP IDX | 586.97 | -36.10 | -5.79% |

| XAU | 75.81 | +0.48 | +0.64% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (03/31/2019):

Broadcom Inc.

Cardinal Resources Ltd

Anglo American Platinum Ltd

Agnico Eagle Mines Ltd.

Alexandria Minerals Corp

Royal Dutch Shell Plc

EOG Resources Inc.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry.

The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks.

The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months.

The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange.

The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver.

The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar.

The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500.

The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500.

The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period.

The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500.

The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500.

The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500.

The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500.

The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500.

The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500.

The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns.

The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance in the global emerging markets. The MSCI Emerging Markets Eastern European Index (Russia at 30 percent market-cap weighted) is a capitalization-weighted index that monitors the performance of emerging market stocks from all countries that make up the Eastern European Region. The University of Michigan Confidence Index is a survey of consumer confidence conducted by the University of Michigan. The report, released on the tenth of each month, gives a snapshot of whether or not consumers are willing to spend money. The Bloomberg Dollar Spot Index (BBDXY) tracks the performance of a basket of 10 leading global currencies versus the U.S. Dollar. The FTSE Bursa Malaysia KLCI, also known as the FBM KLCI, is a capitalization-weighted stock market index, composed of the 30 largest companies on the Bursa Malaysia by market capitalization that meet the eligibility requirements of the FTSE Bursa Malaysia Index Ground Rules.