Coinbase Goes Public, Opening the Crypto Floodgates

Date Posted: April 16, 2021

Read time: 47 min

Digital currencies stormed Wall Street in a big way this week. Crypto exchange Coinbase went public in a direct listing, opening the floodgates for a number of other crypto-related companies.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

Digital currencies stormed Wall Street in a big way this week. Crypto exchange Coinbase went public in a direct listing, opening the floodgates for a number of other crypto-related companies.

This move brings us one step closer to mass acceptance of cryptocurrencies.

Before now, investors seeking to participate had a few options other than to hold the underlying assets.

The most obvious among these is to own shares of the crypto miners, including HIVE Blockchain Technologies, the only publicly traded firm to mine both Bitcoin and Ether using green energy. There are also futures contracts through CME Group, and a number of issuers have filed for a Bitcoin ETF.

With Coinbase, ticker COIN, investors get exposure to the entire $2.2 trillion crypto ecosystem, including not just Bitcoin and Ether but also smaller yet fast-growing coins like Dogecoin. All cryptos mentioned hit fresh new highs this week following Coinbase’s debut.

The stock traded a staggering $29 billion in volume on its first day, which could be an all-time high, according to Bloomberg’s Eric Balchunas.

Several commentators pointed out that Coinbase ended lower than it opened at. As I told Cointelegraph this week, I’ve seen this story play out many times over my 30 years in managing money. Often when a company is up 300% in a year and goes public, it can easily sell off 30%. I don’t believe investors should be too worried about Coinbase’s volatility. I’m incredibly bullish.

That’s not to say the industry isn’t volatile. It remains extremely volatile. Dogecoin is up more than 400% from last Friday. A tweet by Documenting Ether today shows just how much your investment would be today had you used the April 2020 stimulus check to buy Bitcoin, Ether or Dogecoin. It’s hard to look at these figures and not kick yourself.

The first $1200 Stimulus check is now worth if invested in :$BTC: $10,203.94 (850.33%)$ETH: $16,533.46 (1,377.79%)$DOGE: $158,723.63 (13,226.97%)

— Documenting Ethereum ?? (@DocumentEther) April 16, 2021

Positive Economic News Points to Higher Inflation

A raft of positive economic news was released this week, pointing to a robust ongoing recovery from the pandemic-triggered downturn and adding to the thesis that inflation is set to accelerate.

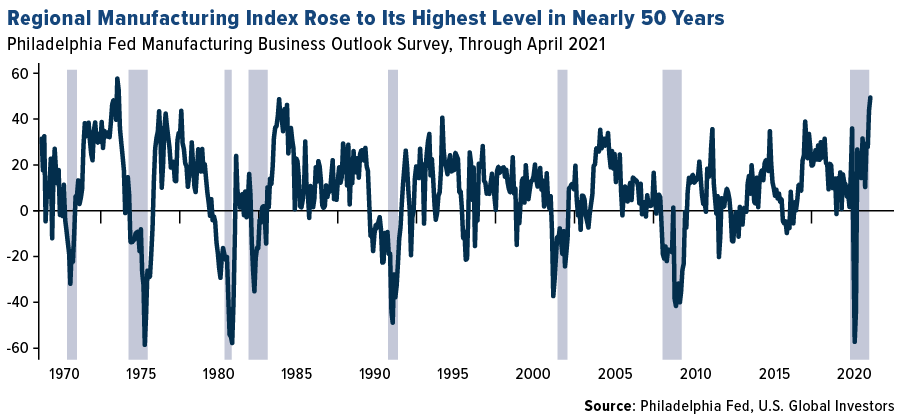

Leading manufacturing data from the Federal Reserve Banks of Philadelphia and New York were extremely constructive for business activity going forward. The Philadelphia Fed Index registered a 50.2 this month, which is the highest level in nearly 50 years if you can believe it. Nearly three in four firms reported higher input prices for raw materials as well as higher prices for their own manufactured goods.

Manufacturers in New York reported the same, with input prices rising at the fastest pace since 2008 and selling prices surging at a record-setting pace.

Indeed, the producer price index (PPI), issued monthly by the Bureau of Labor Statistics (BLS), shows prices rising at multiyear highs. The index for processed goods, for instance, moved up 4.0% in March, the biggest increase since August 1974. For the 12-month period, unprocessed goods exploded 41.6%, the strongest such growth since July 2008.

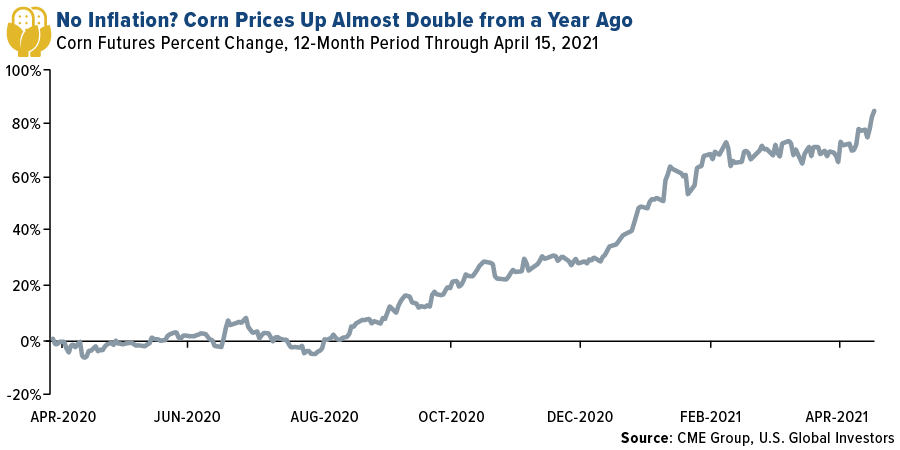

A number of commodities have been on a tear lately. Lumber futures are up for the fourteenth straight day. And just take a look at corn prices. Futures for the crop spiked above $6 a bushel for the first time since June 2013 on tight supply and strong demand from China and South Korea. Corn prices are now up 85% compared to the same time last year and could double before we see a retreat.

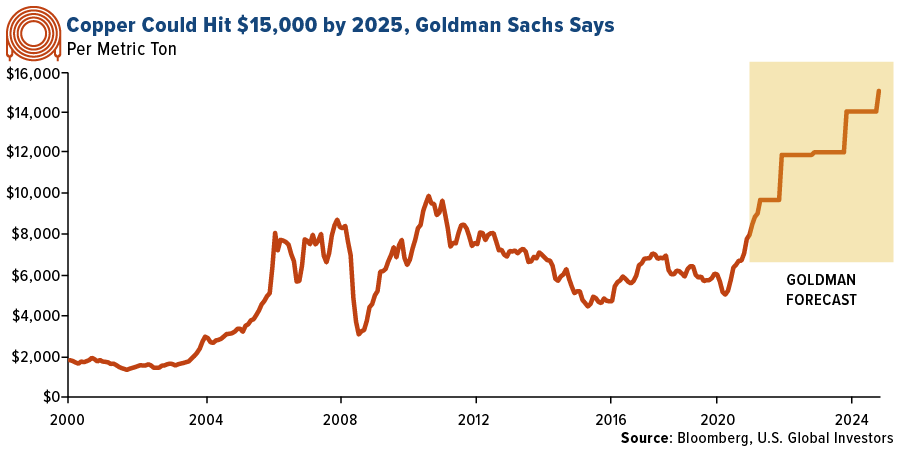

Copper continued its rally this week on a bullish report from Goldman Sachs, which sees the red metal climbing to an all-time high of $15,000 per metric ton by 2025 on an unprecedented supply-demand imbalance brought on by renewable energy. According to the analyst group, current copper prices of around $9,000 “are too low to prevent a near-term risk of inventory depletion.” Only a price point of around $15,000 is enough to incentivize the development of new copper projects.

Our favorite copper play continues to be Ivanhoe Mines, led by billionaire Robert Friedland, who sees the lack of new mines as a national security issue. Speaking at the virtual CRU World Copper Conference this week, Robert told listeners that markets still haven’t quite recognized how disruptive the transition to renewable energy and electrification-of-everything will be, nor just how much copper will be required.

“It’s all copper, copper, copper, copper, copper, copper,” Robert said.

Last week, Ivanhoe Mines announced it had produced a record 400,000 metric tons of ore grading 5.36% copper at its Kakula and Kansoko mines in March.

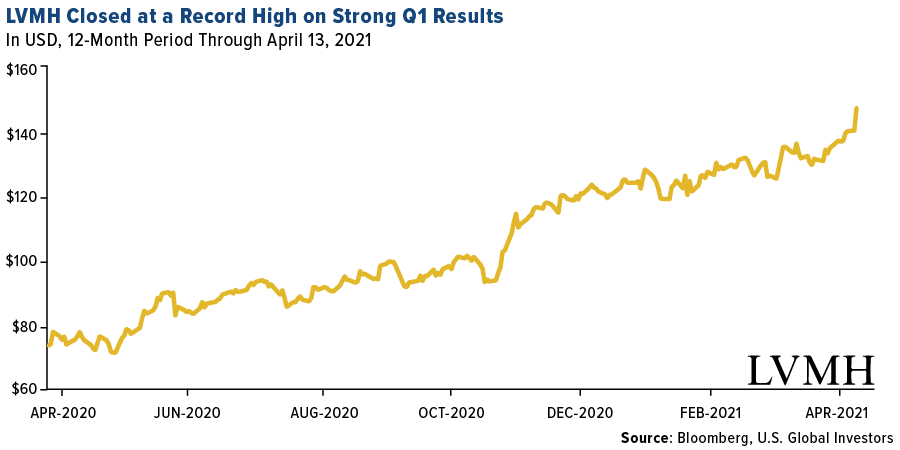

Luxury Giant LVMH Returns to Growth

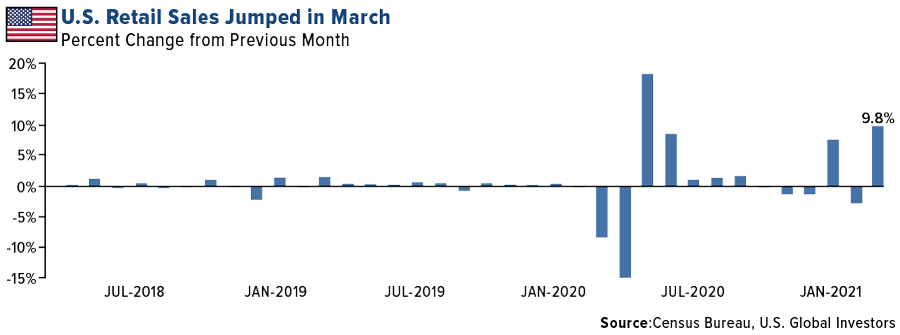

In March, retail sales jumped a whopping 9.8% from the previous month, the second largest surge on record, as consumers made good use of their stimmy checks. As I shared with you last week, sales of cars and light trucks were up an unbelievable 58% in March compared to last year, with many luxury carmakers setting new monthly and quarterly sales records.

The French luxury giant LVMH Moet Hennessy Louis Vuitton announced this week that it had returned to growth following the pandemic, reporting first-quarter revenue of 14 billion euros, or $16.75 billion.

Fashion and leather goods had an excellent start to the year, generating record revenue that was 52% higher than the same period in 2020 and an increase of 37% from 2019. The conglomerate was helped by its recent acquisition of U.S. jeweler Tiffany, bringing the number of companies it owns to over 75.

I’m very pleased with how LVMH has performed over the course of the pandemic, during which the fortunes of wealthy consumers has expanded. With a market cap of nearly 320 billion euro ($383 billion), LVHM is Europe’s most valuable company.

First-quarter sales were driven by Asia, particularly China, and the U.S., which have done a much better job of combating COVID-19 than Europe.

The increasing traffic at U.S. seaports is a clear sign that demand is strong right now. Following its record-setting February, the Port of Los Angeles processed 957,599 twenty-foot equivalent units (TEUs) in March, representing the busiest March in the port’s 114-year history. All combined, it was also the busiest first quarter ever for the seaport.

To see the top 10 countries with the largest shipping fleets, click here.

Gold Market

This week spot gold closed the week at $1,776.51, up $32.63 per ounce, or 1.87%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher 3.50%. The S&P/TSX Venture Index came in off 1.55%. The U.S. Trade-Weighted Dollar fell 0.68%.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Apr-13 | ZEW Survey Expectations | 79.0 | 70.7 | 76.6 |

| Apr-13 | ZEW Survey Current Situation | -54.1 | -48.8 | -61.0 |

| Apr-13 | CPI YoY | 2.5% | 2.6% | 1.7% |

| Apr-15 | Germany CPI YoY | 1.7% | 1.7% | 1.7% |

| Apr-15 | Initial Jobless Claims | 700k | 576k | 769k |

| Apr-15 | China Retail Sales YoY | 28% | 34.2% | — |

| Apr-16 | Eurozone CPI Core YoY | 0.9% | 0.9% | 0.9% |

| Apr-16 | Housing Starts | 1613k | 1739k | 1457k |

| Apr-22 | ECB Main Refinancing Rate | 0.000% | — | 0.000% |

| Apr-22 | Initial Jobless Claims | 650k | — | 576k |

| Apr-23 | New Home Sales | 885k | — | 775k |

Strengths

- The best performing precious metal for the week was palladium, up 5.13%, despite Nornickel stating that it expects to resume production ahead of schedule. Both Citigroup and UBS Group AG highlighted their expectations for further price gains in palladium. Gold rose on Wednesday after Fed Chair Jerome Powell reiterated his dovish view on monetary policy, sending the yellow metal’s headwinds, bond yields and the dollar, downward. Bullion hit a seven-week high and climbed above its 50-day moving average.

- Silver Bullion Pte Ltd. Is building a six-story vault in Singapore that could store 15,000 tons of silver. The warehouse near Changi airport currently holds 400 tons of silver, but with demand for coins and bars booming, the company expects promising years to come. According to the London Bullion Market Association (LBMA), the amount of silver stored in vaults in London rose 11% in March to a record. Bloomberg reports that JM Bullion, a major precious metals retailer, will open a 25,000-square-foot-warehouse in Dallas in June that will be used for holding silver and other precious metals.

- China has allowed international and domestic banks to import larger amounts of bullion, reports Reuters, saying 150 tonnes will be shipped next month. Gold imports by India, the world’s second biggest consumer, rose in March to the highest monthly total in nearly two years. A pullback in gold prices stoked demand during the ongoing wedding season, where gold jewelry gift giving is considered auspicious. Bloomberg reports overseas purchases rose more than sevenfold to 98.6 tons, up from 13 tons in March last year.

Weaknesses

- The worst performing precious metal for the week was platinum, down 0.05%. Both palladium and platinum have led the precious metals group this year with better than 12% gains in prices. Silver is on the verge of turning positive and gold is still the lagger, with losses of greater than 6%.

- Holdings in SPDR Gold Shares could fall below 1,000 tons in the next few weeks as investors continue to pull money out of the largest bullion-backed ETF. Bloomberg reports holdings have shrunk by a fifth near 1,280 tons last September.

- Sabina Gold fell as much as 18% intraday on Tuesday after a newsletter writer told its research clients to sell the stock due to the unlikelihood of takeover, reports Bloomberg. On the other hand, Sprott Capital Partners said in a February note that Sabina’s reserves beat estimates and that no other developer globally has a lower EV/resource multiple. Wesdome Gold Mines reported gold production for the first quarter of 22,564 ounces, down from 25,122 ounces year-over-year or 10%.

Opportunities

- Scottie Resources Corp. and AUX Resources Corporation announced a merger to consolidate the Stewart Mining Camp in the area known as the Golden Triangle of British Columbia. Ascot Resources Ltd. announced a C$20,640,000 private placement by Yamana Gold with the net offerings used to fund construction of Ascot’s gold product in British Columbia.

- CIBC analyst Cosmos Chiu wrote that he expects silver to benefit from its use in solar panels, especially given the growing importance of ESG investing. “Of all the metals, silver has the highest electrical conductivity, making it difficult for potential substitutes (such as copper and aluminum) to compete.”

- Philippine President Rodrigo Duterte will lift a 2012 ban and allow the government to approve new mining contracts to help boost revenue. The Philippine Stock Exchange’s mining and oil sector index rose 5.4% on the news.

Threats

- Brazil is investigating reports of COVID-19 vaccines being exchanged for illegal gold in the Yanomami indigenous reserve. Federal prosecutors are already investigating the diversion of vaccine shots intended for indigenous people. Brazil remains one of the worst hit countries by the pandemic.

- Research firm CrossBorder Capital found that bitcoin is dragging down gold’s fair value, reports Kitco News. "We calculate that the existence of Bitcoin has probably reduced the ‘fair value’ of gold by $158 per ounce given that liquidity is now spread a tad more thinly over these two combined stores of value," the analysts said in a report Wednesday. The report added that investors worried about monetary inflation to hold one unit of Bitcoin for every nine units by value of gold as a better hedge than gold alone.

- The Grayscale Bitcoin Trust could soon surpass the SPDR Gold Trust as the growing popularity of cryptocurrencies pushes the bitcoin ETF over $50 billion, close to the $57 billion held in the world’s second-largest commodity ETF. "In a world going digital, we believe gold symbolizes the diminishing potential for sustained commodity-price advances, notably vs. bitcoin," said Bloomberg Intelligence in a note to clients. "The crypto is a prime example of how advancing innovation suppresses commodity prices."

Index Summary

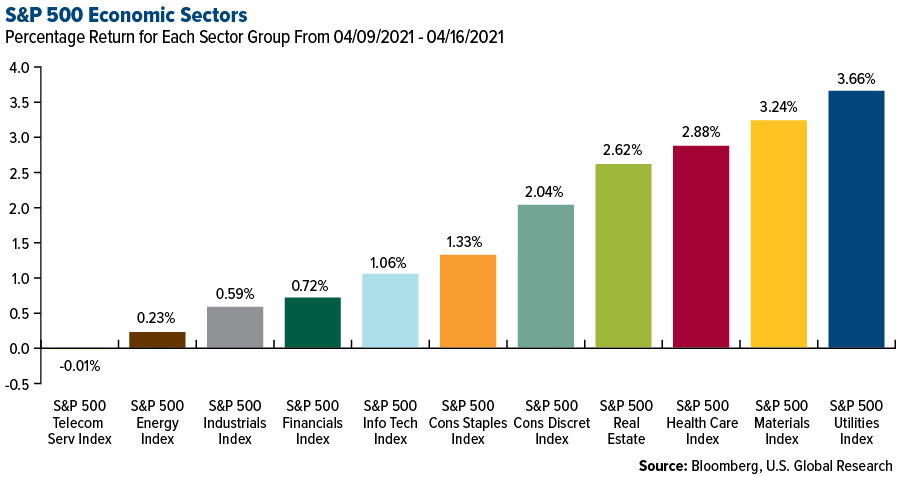

- The major market indices finished up this week. The Dow Jones Industrial Average gained 1.18%. The S&P 500 Stock Index rose 1.37%, while the Nasdaq Composite climbed 1.09%. The Russell 2000 small capitalization index gained 0.86% this week.

- The Hang Seng Composite gained 0.41% this week; while Taiwan was up 1.81% and the KOSPI rose 2.13%.

- The 10-year Treasury bond yield fell 6 basis points to 1.597%.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Dogecoin, rising 533.65%.

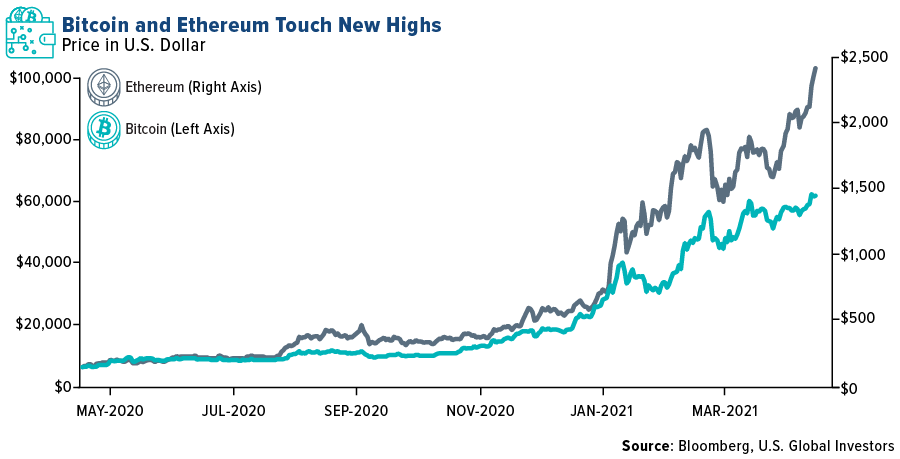

- Bitcoin and Ether, the two biggest cryptocurrencies by market cap, reached new all-time high prices this week, a few hours before the highly anticipated direct listing of crypto exchange Coinbase on Nasdaq. The rally in the biggest cryptocurrencies spilled into altcoins like Ripple, Dogecoin and Chainlink, with the latter two posting all-time highs as well. The chart below shows the rise in Bitcoin and Ether prices over the past year.

- New York-based Ark Investment Management, headed by crypto bull Cathie Wood, purchased an additional 341,186 shares of Coinbase, a day after buying 749,205 shares on the day of its listing on the Nasdaq exchange. The crypto exchange’s shares were purchased through three of its funds—the Ark Fintech Innovation ETF, Ark Innovation ETF and Ark Next Generation Internet ETF. The listing has been dubbed as a moment of validation for the cryptocurrency industry.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was Dent, down 28.28%.

- Whale Alert, that offers alert and tracking services in the crypto markets, announced this week that over $623 million worth of Bitcoin from Bitfinex, a crypto exchange, hacked in 2016 was moved to another wallet. This came the same day as Coinbase’s direct listing on Nasdaq. Trade The Chain, a real-time crypto data service, confirmed the number of Bitcoin moved, adding that it amounts to about 10% of the total amount that was stolen.

- Celsius, a crypto lending firm, reported that it discovered a data breach with one of its third-party service providers which led to exposed personal information of its customers. The hackers used the information to send fraudulent emails and text messages to Celsius’ customers in a bid to trick them into revealing the private keys to their funds. Celsius is still investigating how the hackers gained access to the customers’ phone numbers, considering the breach occurred with an email management system.

Opportunities

- WisdomTree Investments announced the listing of its Bitcoin exchange-traded product (ETP) on the Deutsche Boerse’s Xetra market based in Frankfurt. The Bitcoin ETP, trading under the ticker WBIT, tracks the spot price of Bitcoin and has a total expense ratio 0.95%. The listing comes while WisdomTree awaits the U.S. Securities and Exchange Commission’s (SEC) decision on whether to approve its Bitcoin ETF for U.S. investors.

- Earle Loxton, the co-founder of DCX Capital, has announced plans to launch South Africa’s first Bitcoin ETF. The company will be making an application through Easy Equities, an online trading platform that acquired a controlling stake in DCX Capital, to the Johannesburg Stock Exchange (JSE) for the ETF. DCX Capital is the manager of crypto index fund E10, which holds the world’s 10 largest cryptocurrencies as assets, which the company is planning on converting into an ETF.

- Galaxy Digital announced that it has filed with U.S. regulators for a Bitcoin ETF, becoming one of many investment management firms that have filed for such a product within the U.S. Currently, the SEC is reviewing two applications and has six additional applications in the pipeline. Galaxy Digital is the sub-advisor of the CI Galaxy Bitcoin ETF, which currently has $190 million in assets since launching last month.

Threats

- Mike Novogratz, a crypto bull and CEO of Galaxy Digital, warns that the crypto market could be in for a short-term washout due to the frenzy caused by Coinbase’s direct listing. These comments were directed toward altcoins gaining momentum this week from retail investors. He also added that the Coinbase listing has created a lot of euphoria for cryptocurrencies and brought the crypto market to a point of maximum financial risk, and that the market might see a temporary correction.

- The Central Bank of the Republic of Turkey has announced that it will prohibit crypto holders from using their digital assets for payments and will also prevent payments providers from providing fiat onramps for crypto exchanges. The ban will come into effect on April 30, 2021 and is set to render any crypto payment solutions and partnerships illegal. Banks are exempt from this regulation, meaning users can still deposit Turkish lira on crypto exchanges using wire transfers from their bank accounts.

- Director-general of Nigeria’s Securities and Exchange Commission, Lamido Yuguda, has said that the central bank’s ban on cryptocurrencies has caused significant disruptions in the market. Almost two months after the ban was put in place, the commission has been forced to pause its planned cryptocurrency regulatory framework, that was announced in September 2020, until exchanges can operate bank accounts in the country. Since the central bank’s ban, cryptocurrency buying and selling is only possible through peer-to-peer channels which has led to massive premiums on digital currency prices. The central bank governor emphasized that the bank was not against crypto trading in the country but that such transactions cannot occur through commercial banks.

Domestic Economy and Equities

Strengths

- Advance retail sales rose 9.8% for the March, compared to the Dow Jones estimate of a 6.1% gain and a decline of 2.7% in February. Sporting goods, clothing and food and beverage led the gains in spending and contributed to the best month for retail since the May 2020 gain of 18.3%, which came after the first round of stimulus checks.

- Unemployment claims sank by 193,000 in early April to a fresh pandemic low, an unusually large decline that reflects an improving economy but also ongoing problems in processing applications for jobless benefits. Initial jobless claims filed traditionally through the states fell to a seasonally adjusted 576,000 from 769,000 in the prior week.

- Freeport-McMoran Inc was the best performing S&P 500 stock for the week, increasing 12.04%. Copper’s rally on an improving global macro backdrop and demand for the metal is likely to support better financial performance for Freeport-McMoRan.

Weaknesses

- The U.S. leads the world in COVID-19 cases and deaths, with 31.5 million cases, or about 23% of the global total, while the 565,289 deaths make up about 19% of the global toll. The U.S. added at least 74,312 new cases and 909 new deaths on Thursday, according to a New York Times tracker. The U.S. has averaged 70,514 cases a day in the past week, up 8% from the average two weeks ago. Overall, cases are rising in 33 states and Washington, D.C.

- Texas faced a brief power grid scare Tuesday night, less than 60 days after widespread blackouts left millions without light and heat for days during a deep winter freeze. The grid operator, the Electric Reliability Council of Texas, asked for conservation for nearly four hours with a quarter of generators down for repairs and a mild cold front failing to reduce electricity demand as much as had been anticipated, leaving supply tight. Wholesale electricity prices jumped as high as 10,000% in some parts of the state.

- Discovery Inc was the worst performing S&P 500 stock for the week, decreasing 11.10%. With the launch of Discovery+ this January, the majority of the company’s paid content was made available to consumers online, leading to an average 16.2% drop in first quarter prime-time ratings.

Opportunities

- Website hosting service Squarespace Inc. publicly confirmed its plans to go public through a direct listing. Squarespace spelled out its plans in a filing Friday in which it also disclosed details of its finances, including 28% growth in revenue last year. The company had net income of about $31 million on revenue of $621 million last year. The company plans for its shares to trade under the symbol SQSP.

- Walt Disney Co.’s Disneyland resort in California is sold out for weekends through May, an indication of pent-up demand for leisure activities as the pandemic eases in the nation’s most-populous state. Universal Studios in Los Angeles opened its gates Friday and was sold out for the first three days. Many parks are requiring reservations for the first time, something Disney resorts chief Josh D’Amaro said benefits both the company and guests. Theme-park attendance during the seasonally strong summer months should accelerate as the vaccine rollout continues and demand for outdoor leisure activities increases, Fitch Ratings said in report Friday.

- Cisco Systems Inc. is getting another look on Wall Street as a return to offices points to an environment where the networking company could see a long-awaited return to revenue growth. The stock was a laggard last year as the pandemic pushed employers to embrace remote work, but a return to offices is expected to contribute to an acceleration in enterprise IT spending, providing a tailwind for growth. This idea has spurred at least three analysts to upgrade the stock in recent weeks, including Wolfe Research.

Threats

- Amazon.com Inc. is experimenting with a premium service that lets customers opt to have furniture or appliances assembled as soon they arrive at their homes, according to people familiar with the plan. The move, if adopted widely, would help the world’s largest online retailer compete more effectively with Wayfair, Best Buy, Home Depot and Lowe’s which all offer similar options.

- Splunk analysts were cautious on the news that Chief Technology Officer Tim Tully will be resigning, with KeyBanc downgrading the stock. The departure “comes at a tough time” and compounds other risks facing the company, including higher competition, pricing changes, and a transition of the customer base to the Splunk Cloud Platform.

- A U.S. affiliate of Mexican consumer-finance giant Crédito Realis is marketing a rare subprime auto bond backed by unconventional collateral including loans to recently bankrupt consumers and undocumented borrowers. “This is not very common within ABS deals,” said Clayton Triick, a portfolio manager at Angel Oak Capital Advisors. “The deal is interesting but definitely requires an extra risk premium for multiple reasons.”

Energy and Natural Resources Market

Strengths

- The best performing commodity for the week was lumber, up 14.71%. Forest product stocks outperformed after U.S. housing rebounded sharply in March, and Western SPF lumber prices hit another record.

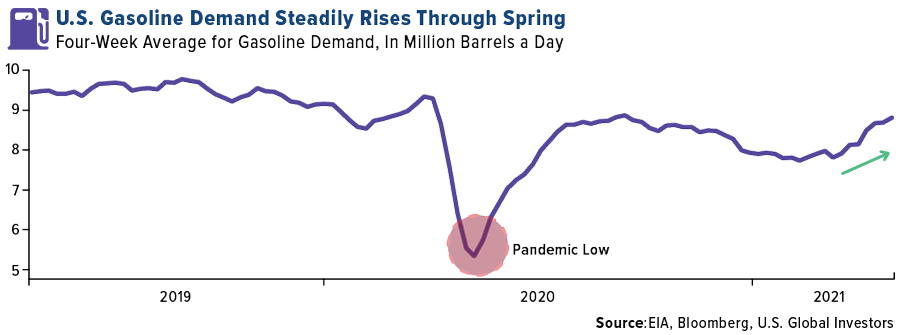

- The Energy Information Administration (EIA) for the U.S. reported that the four-week rolling average of U.S. gasoline demand rose to the highest level since August 2020, showing signs of recovery from the pandemic and reduced mobility caused by country-wide lockdowns. U.S. refiners are processing the most crude oil in over a year and are expecting a demand surge for the summer travel season. West Texas Intermediate (WTI) crude futures surged more than 6% this week, but more gains in diesel and jet fuel are needed to provide sure footing for the markets after the pandemic slump.

- The Energy Information Administration (EIA) for the U.S. reported that the four-week rolling average of U.S. gasoline demand rose to the highest level since August 2020, showing signs of recovery from the pandemic and reduced mobility caused by country-wide lockdowns. U.S. refiners are processing the most crude oil in over a year and are expecting a demand surge for the summer travel season. West Texas Intermediate (WTI) crude futures surged more than 6% this week, but more gains in diesel and jet fuel are needed to provide sure footing for the markets after the pandemic slump.

Weaknesses

- The worst performing commodity for the week was uranium, down 6.23%. Cameco Corp. announced that it will restart production at its Cigar Lake mine, and it could weigh on spot uranium prices in the near term as it is one of the world’s largest uranium mines and had been suspended since December 2020.

- Three of the biggest power companies in the U.S. – NextEra Energy Inc., Duke Energy Corp. and Southern Company, has told the Texas governor and lawmakers that proposed new laws would unload unfair costs onto wind and solar farms and reduce investment in the state. The proposed bill would make wind and solar farms pay for services to ensure the flow of power on the state’s grid remains smooth and steady. The bill was proposed on the back of February’s winter storm that left millions without power for days, as oil and gas supporter and conservative lawmakers blamed frozen wind turbines for the widespread failures, even though gas plants made up the bulk of power plants that failed. The three power companies have collectively invested about $15 billion in renewable energy operations in Texas alone. Jeff Clark, president of the Advanced Power Alliance, a renewable energy trade group, sees this bill as a direct attack on $60 billion worth of investment.

- The California Public Utilities Commission has voted unanimously to place PG&E Corp. under enhanced oversight after finding that the utilities company was not prioritizing tree trimming near power lines located in areas of high fire-risk. The commission has put PG&E into the first step of a six-step enforcement process that was set up as a condition of the company’s bankruptcy exit last year. This gives regulators the ability to ensure that PG&E is improving its safety performance after the company’s live wires sparked the deadliest wildfire in the state’s history. Additionally, the commission ordered PG&E to submit a corrective-action plan to regulators and issue periodic progress reports.

Opportunities

- Philippine’s President, Rodrigo Duterte, has signed an order that allows the country’s government to approve new mining contracts, effectively ending a 2012 ban in a bid to boost revenue. Following the news, the Philippine Stock Exchange’s mining and oil sector index rose by 5.4%, marking its biggest gain since October 2020. Philippine’s accounts for more than half of China’s nickel ore imports, but analysts do not expect nickel’s supply to increase significantly as growth potential for new and existing mines is limited. President Duterte is also pushing the Department of Environment and Natural Resources to review existing mining contracts for possible renegotiation and ensure compliance to safety and environmental policies.

- Trafigura Group, one of the largest commodities traders, announced that it is backing a plan by MAN Energy Solutions to produce ammonia-fueled ship engines. This marks the latest renewable-related investment by the firm as it seeks to diversify its operations amid the energy transition. MAN’s ammonia engine is expected to be commercially available for large-scale ships by 2024. Meanwhile, World Bank reported that green ammonia and hydrogen are the best candidates for shipping industry’s transition from fossil fuels to clean alternatives.

- Goldman Sachs Group Inc. is forecasting copper prices to reach $15,000 a ton by 2025, buoyed by the increase in demand for global green-energy transition. Analysts at the bank believe that higher prices will be needed to replenish supplies as usage in electric vehicles and renewable-energy projects surges.

Threats

- Automakers that are already struggling with pandemic-induced plant shutdowns and a global chip shortage could soon see another supply chain squeeze with rubber supplies dwindling. Rubber’s global supply is running short caused by China’s stockpiling of raw materials and a devastating leaf disease. This shortage threatens to further disrupt vehicle production just as demand rebounds and the Biden administration douses the U.S. economy with $1.9 trillion in stimulus spending.

- Texas faced another power-grid scare this week as the state’s grid operator, the Electric Reliability Council of Texas (Ercot), asked for conservation for almost four hours while a quarter of generators were down for repairs and a mild cold front failed to reduce electricity demand as much as had been expected, leaving supply tight. This caused wholesale electricity prices to jump as high as 10,000% in some parts of the state. Part of this week’s problem was self-inflicted, as Ercot failed to correctly forecast production from solar and wind farms.

- Surging demand for electric vehicles (EVs) is putting upward pressure on the price of raw materials, threatening to slow the push toward making cheaper batteries, the key to widespread EV adoption. Raw materials like lithium, cobalt and nickel have all rallied in the past year, with cobalt surging 57% last quarter and nickel jumping to a more-than six-year high earlier this year. China, the biggest player in EV batteries, has a stranglehold over a majority of the world’s capacity and the processing of crucial battery materials. In 2020, the average price of a lithium-ion battery pack dropped to $137/kWh, and EVs are expected to start reaching price parity with internal combustion cars when the price drops to $100/kWh.

Airline Sector

Strengths

- The best performing airline stock for the week was Sun Country Air, up 9.7%. Cash burn is improving drastically for North American airlines. United, American and Air Canada all reported improved cash burn trends. Cash burns were minimally negative in the month of March, and American was cash burn positive in March.

- Website traffic is increasing at U.S. airlines, and is now down only 20% from pre-pandemic levels, which is the best comparison since the pandemic started. JetBlue and Alaska Air had the best trends, being down only 8% and 5%, respectively.

- Air Canada is receiving increased government support. The Canadian government will receive an 8-10% stake in exchange for $5.9 billion Canadian. The carrier must also maintain jobs and facilitate refunds for non-refundable tickets. There are limitations on dividends, share repurchases and executive compensation. This increased liquidity should bridge the airline until the population is vaccinated and pent-up demand is unleashed.

Weaknesses

- The worst performing airline stock for the week was Avianca, down 21.9%. The company is seeking to do a $1.8 billion stock offering before it tries to exit bankruptcy. There are concerns about shareholders being diluted.

- First quarter earnings are in the process of being reported, and the data will be mixed. COVID news at the beginning of the quarter and storms in February have negatively impacted demand. March, however, showed strong improvement due to vaccine distribution. Delta reported first quarter earnings below expectations and guided second quarter revenues to be down 50-55%, which is below expectations. Leisure demand is 90% of normal levels and business demand is 20% of normal levels at Delta.

- Boeing asked 16 customers of the 737 MAX to ground 90 aircraft to inspect backup power units. Southwest, American, Alaska Air and United are the most negatively impacted carriers from this decision. Flights involving the 737 MAX have fallen significantly. United and American have reduced 737 MAX flights by 40-50%. Alaska Air has pulled all their 737 MAX flights. Eighty percent of the current flights for the 737 MAX are occurring in the U.S.

Opportunities

- Spirit appears to be positioned to have the strongest recovery. The airline has high exposure to Florida and markets in the Northeast that are reopening. The fleet is expected to be 100% utilized by year-end 2022.

- Analysts have been positive on the new IPO, Sun Country Airlines. The company has a low-cost structure and is positioned well for the growing leisure market. The company has the industry’s second highest margins and is also an operating partner for Amazon Air.

- An interview with the CEO of Allegiant Air offered some interesting insights into the airline industry. Balance sheets are much stronger than in prior downturns, and the potential for a spending surge is much higher than in previous downturns. The industry has also benefitted from an abundance of cheap aircraft and plenty of pilots.

Threats

- European daily flight activity is down 65% from 2019 levels, and the trend has been stable since the onset of the pandemic. Website visits are down 71% and bookings are down 85%. The region has not seen the improvement that has been seen in the U.S. and China.

- United pre-announced first quarter revenues of $3.2 billion, which is less than the $3.3 billion consensus. Also, the company will start a $9 billion debt sale to refinance loans, including loans from the CARES Act. However, rates will be higher than the CARES Act loans, so earnings may be negatively impacted.

- American Airlines entered the COVID pandemic with the most leveraged balance sheet and will exit it very leveraged. Since airlines have significant operating leverage, adding financial leverage to this will only make the carrier’s earnings more volatile.

Emerging Markets

Strengths

- The best performing country in Emerging Europe for the week was Russia, gaining 5.46%. The best performer in Asia was South Korea, up 2.7%.

- The Russian ruble was the best performing currency in Emerging Europe, gaining 2.17% while the Thai baht was the best performing in Asia, up 86 basis points.

- China’s first quarter GDP rose 18.3% year-over-year. However, March activity data was mixed. Industrial production rose 14.1% year-over-year vs. consensus estimates of 17.2% growth. Retail sales were up 34.2% and follows a 33.8% gain in the January and February period. Residential housing starts expanded 30.1%. Lastly, unemployment fell to 5.3% from 5.5% the month prior.

Weaknesses

- The worst performing country in emerging Europe for the week was Hungary, losing 2.1% while the worst performer in Asia was India, losing 1.22%.

- The Polish zloty was the worst relative performing currency in emerging Europe this week, up 38 basis points. The Philippines peso was the worst performer in Asia, still gaining 28 basis points.

- Eurozone industrial production fell 1.6% year-over-year. On a monthly basis, production dropped 1% month-over-month compared to the prior month’s reading of 0.8%. Among member states for which data are available, the largest decrease in industrial production was registered in France, which saw a 4.8% drop. On the other hand, the sharpest increases were observed in Hungary, Ireland and Croatia. ING said industrial production for the bloc is being held up by input shortages and this will lead to weaker growth in first quarter.

Opportunities

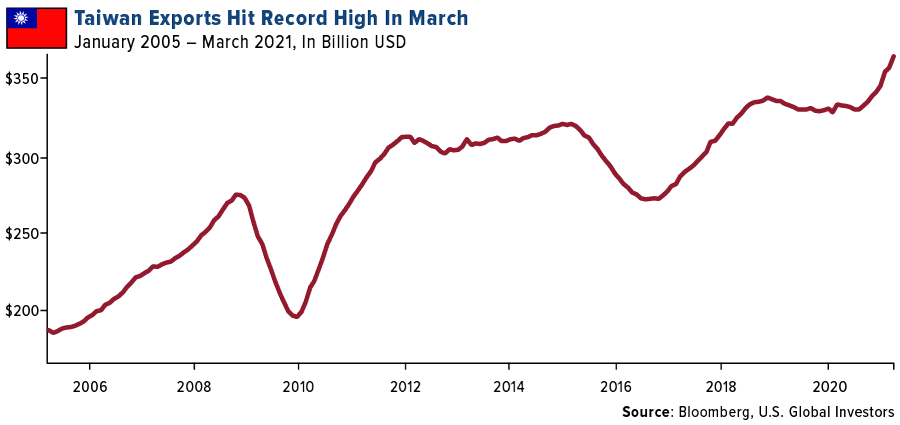

- Taiwan’s economic data is robust and driven by technology stocks. Cornerstone Macro sees the country as the safest Emerging Market in their Emerging Market Vulnerability Index. Taiwan’s exports hit an all-time high in March, rising 0.4% month-over-month and jumping 27.1% year-over-year.

- Bloomberg reports Eurozone governments will seek to an agreement on technical specifications for coronavirus passports. The "Digital Green Certificates" will offer proof that holders have had a Covid-19 vaccination or recently returned a negative test, while people who contract the disease should be recognized as immune from day 11 for about six months. Governments are encouraged to accept all vaccines that have secured WHO approval for emergency use and should recognize certificates issued by non-EU nations. A deal would pave the way for the resumption of incoming travel in the bloc.

- The European Central Bank (ECB) will most likely leave all rates unchanged next week but will continue to support measures providing liquidity to the market. At the last meeting in mid-March, policy makers increased their bond-buying program after yields rose. The ECB also is putting more pressure on regional governments to push forward with much needed fiscal stimulus.

Threats

- Following a peak in the daily number of Covid-19 infections, the Turkish government reintroduced strict measures to curb the spread including a curfew on inter-city travel, restrictions on using public transport and a risk "tier" system.

- The Biden administration imposed a set of new sanctions on Russia, including long-feared restrictions on buying new sovereign debt. America will prevent U.S. financial institutions from participating in the primary market for new debt issued by the Russian central bank starting on June 14.

- Chinese technology companies have been given a month to fix anti-competitive practices and publicly pledge to follow the rules or risk suffering the same fate as Alibaba, which was fined $2.8 billion over the weekend. China’s regulators issued the ultimatum at a meeting on Tuesday with the country’s 34 leading tech companies that included Tencent, ByteDance, Meituan and Alibaba. The regulator said it would conduct its own inspections at the end of the period and "severely punish" companies not in compliance.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| 10-Yr Treasury Bond | 1.60 | -0.06 | -3.80% |

| Oil Futures | 63.10 | +3.78 | +6.37% |

| Hang Seng Composite Index | 4,528.12 | +18.61 | +0.41% |

| S&P Basic Materials | 518.94 | +16.30 | +3.24% |

| Korean KOSPI Index | 3,198.62 | +66.74 | +2.13% |

| S&P Energy | 365.19 | +0.84 | +0.23% |

| Nasdaq | 14,052.34 | +152.15 | +1.09% |

| DJIA | 34,200.67 | +400.07 | +1.18% |

| Russell 2000 | 2,262.67 | +19.20 | +0.86% |

| S&P 500 | 4,185.47 | +56.67 | +1.37% |

| Gold Futures | 1,776.10 | +31.30 | +1.79% |

| XAU | 149.16 | +5.40 | +3.76% |

| S&P/TSX VENTURE COMP IDX | 944.46 | -14.89 | -1.55% |

| S&P/TSX Global Gold Index | 312.70 | +10.63 | +3.52% |

| Natural Gas Futures | 2.69 | +0.16 | +6.33% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Korean KOSPI Index | 3,198.62 | +151.12 | +4.96% |

| 10-Yr Treasury Bond | 1.60 | -0.05 | -2.92% |

| Gold Futures | 1,776.10 | +46.90 | +2.71% |

| S&P Basic Materials | 518.94 | +25.63 | +5.20% |

| S&P 500 | 4,185.47 | +211.35 | +5.32% |

| DJIA | 34,200.67 | +1,185.30 | +3.59% |

| Nasdaq | 14,052.34 | +527.14 | +3.90% |

| Oil Futures | 63.10 | -1.50 | -2.32% |

| Hang Seng Composite Index | 4,528.12 | -56.29 | -1.23% |

| S&P/TSX Global Gold Index | 312.70 | +15.81 | +5.33% |

| XAU | 149.16 | +4.96 | +3.44% |

| Russell 2000 | 2,262.67 | -73.72 | -3.16% |

| S&P Energy | 365.19 | -23.04 | -5.93% |

| S&P/TSX VENTURE COMP IDX | 944.46 | -53.08 | -5.32% |

| Natural Gas Futures | 2.69 | +0.16 | +6.25% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| XAU | 149.16 | +6.09 | +4.26% |

| S&P/TSX Global Gold Index | 312.70 | -0.65 | -0.21% |

| Gold Futures | 1,776.10 | -82.40 | -4.43% |

| DJIA | 34,200.67 | +3,209.15 | +10.35% |

| S&P 500 | 4,185.47 | +389.93 | +10.27% |

| Nasdaq | 14,052.34 | +939.70 | +7.17% |

| Korean KOSPI Index | 3,198.62 | +48.69 | +1.55% |

| Natural Gas Futures | 2.69 | +0.02 | +0.75% |

| S&P Basic Materials | 518.94 | +37.87 | +7.87% |

| Russell 2000 | 2,262.67 | +107.32 | +4.98% |

| Oil Futures | 63.10 | +9.53 | +17.79% |

| Hang Seng Composite Index | 4,528.12 | +17.99 | +0.40% |

| S&P/TSX VENTURE COMP IDX | 944.46 | +30.11 | +3.29% |

| S&P Energy | 365.19 | +29.05 | +8.64% |

| 10-Yr Treasury Bond | 1.60 | +0.47 | +41.33% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (03/31/2021):

Tencent Holdings Ltd

Meituan

Alibaba Group Holding Ltd

Wesdome Gold Mines Ltd

Ascot Resources Ltd

Ivanhoe Mines Ltd

LVMH Moet Hennessy Louis Vuitton SA

Amazon.com Inc

United Airlines Holdings Inc

American Airlines Group Inc

Air Canada

JetBlue Airways Corp

Alaska Air Group Inc

Delta Air Lines Inc

Southwest Airlines Co

Spirit Airlines Inc

Allegiant Travel Co

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The Philadelphia Federal Index (or Philly Fed Index) is a regional federal-reserve-bank index measuring changes in business growth covering the Pennsylvania, New Jersey, and Delaware region.