Commodities Were the Top Performers in 1H 2021: Halftime Report

Date Posted: July 16, 2021

Read time: 46 min

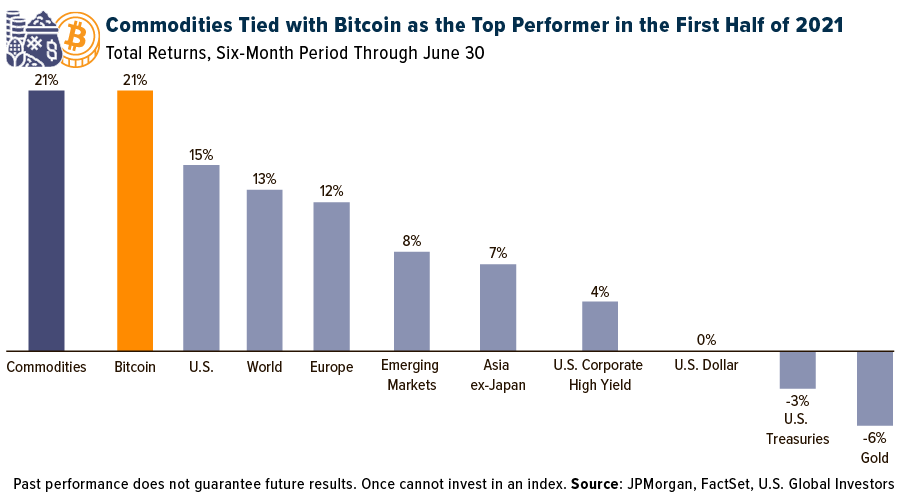

Commodities rallied 21% in the first half of 2021, making them the top performing asset group ahead of U.S., European, emerging market and non-Japan Asian stocks. The broad-based index of energy, agriculture, industrial metals and precious metals rose the same amount as high-flying Bitcoin, which pulled back after hitting its all-time high of more than $63,000 on April 13.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

Commodities rallied 21% in the first half of 2021, making them the top performing asset group ahead of U.S., European, emerging market and non-Japan Asian stocks. The broad-based index of energy, agriculture, industrial metals and precious metals rose the same amount as high-flying Bitcoin, which pulled back after hitting its all-time high of more than $63,000 on April 13.

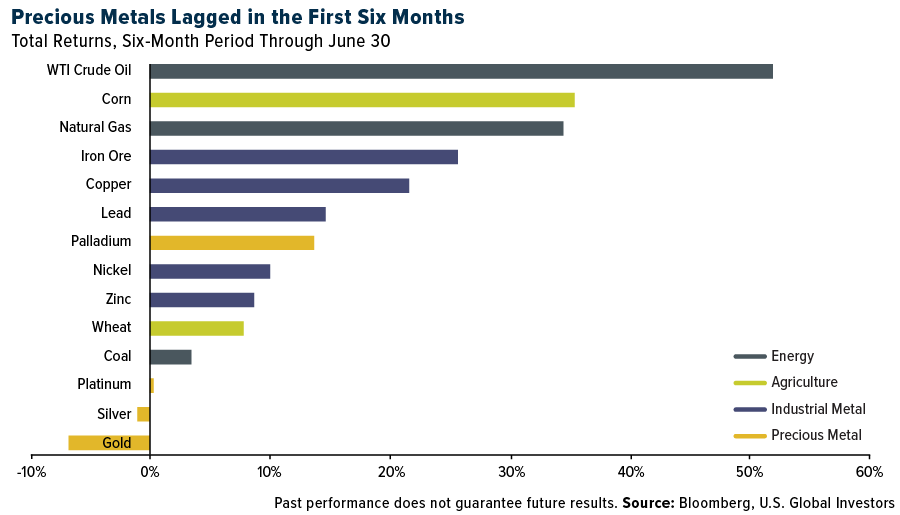

Among the commodities we track, West Texas Intermediate (WTI) crude oil was the number one performer, up nearly 52% on higher-than-expected demand and tight supply, while precious metals lagged, with silver down 1% and gold down more than 6%.

This represents a nearly complete reversal from the price action we saw in 2020. According to our Periodic Table of Commodity Returns, precious metals were last year’s winners—silver surged close to 48%, gold 25%—and oil was the big loser, slipping as much as 20%.

But appetite for risk has changed now that huge segments of the economy are reopening. Demand for fuel has increased as Americans act on pent-up wanderlust: Earlier this month, a greater number of people flew on commercial jets in the U.S. than on the same day in 2019, before the pandemic. And in the days leading up to the busy Fourth of July holiday weekend, gas stations across the country were reportedly running out of gas.

After a Remarkable Turnaround, Oil Demand Sets a New Record

The last six months were a profitable time to invest in the oilfield. The S&P Oil & Gas Exploration & Production Select Industry Index gained approximately 65%.

We participated with a number of companies, including ConocoPhillips, Valero Energy, Phillips 66 and Halliburton, among others. Earnings for the second quarter aren’t expected until next month, but we believe investors will be pleased. In April, Moody’s forecast that oil companies’ earnings may rise by a median rate of 50% compared to last year—though it’s worth noting that this is off a very low base.

Production companies should be well positioned going forward as long as they can maintain capital discipline and operating efficiency. Bloomberg reports that U.S. oil consumption hit a new record seasonally-adjusted high during the week ended July 2. “While gasoline and diesel demand have returned to pre-pandemic levels, a surge in petroleum use for products such as plastic, asphalt, lubricants and other industrial needs is propelling the recovery,” the article reads.

Gold Fundamentals Remain Solid

It’s no secret gold had a rough six months, but a retrace of the bull market could be in the works due to strong fundamentals.

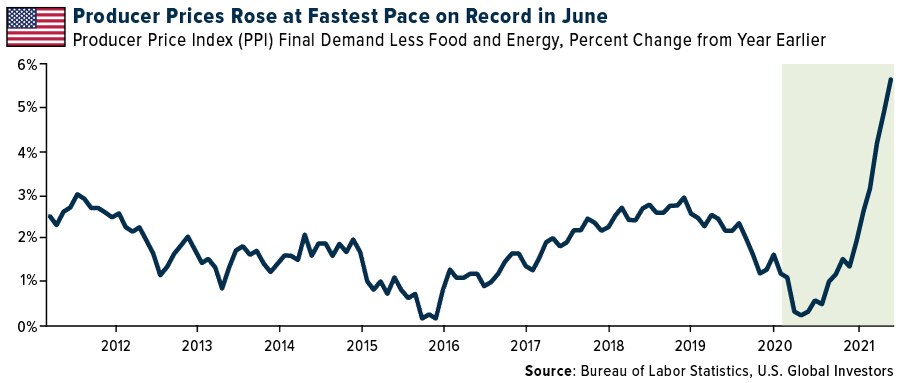

To me, inflation is looking like a greater risk than Powell & Co. are admitting to publicly. Anyone who’s shopped for a new car in the past few months knows that prices are heading sharply up. The cost to eat out jumped 0.7% in June from the previous month, the biggest such increase since January 1982. The producer price index (PPI) for final demand, excluding volatile food and energy, skyrocketed 5.6% compared to the same month last year, representing the fastest pace since records began in 2011.

Investors seeking a haven may need to look elsewhere than government bonds. The 30-year Treasury yield currently trades below 2%, even less when you factor in inflation, meaning investors are effectively paying the U.S. government to hold its debt. As I said last month, gold is the ultimate contrarian investment right now. The metal remains extremely undervalued compared to the S&P 500. The current climate definitely feels risk-on, but I believe it’s only wise to hold around 10% in gold and gold mining stocks to help soften the impact of a worsening pandemic, debt crisis or some other potential shock. I also recommend no more than a 1% to 2% allocation to Bitcoin and Ether, as well as crypto mining stocks.

Mark Your Calendars!

Speaking of cryptos: As most of you know, HIVE Blockchain Technologies listed on Nasdaq on July 1, and on Monday of this week, representatives of HIVE and I had the pleasure of ringing the closing bell. You can see part of the video by clicking here.

On Wednesday, August 18, I will be participating in a webcast on gold and Bitcoin, and I will be joined by none other than Bitcoin evangelist Michael Saylor, founder and CEO of MicroStrategy. This is one webcast you do not want to miss! To get the link to book your spot for this exclusive conservation, email me at info@usfunds.com with subject line “Michael Saylor webcast.” Hope you can join us!

Index Summary

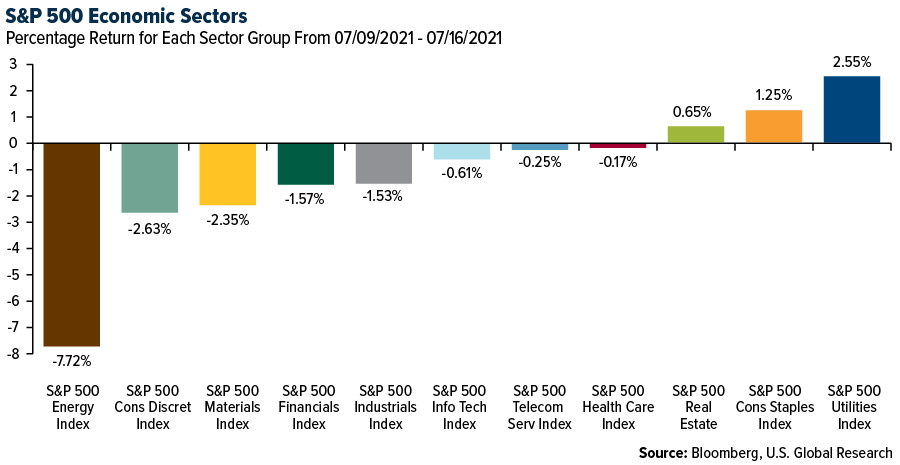

- The major market indices finished down this week. The Dow Jones Industrial Average lost 0.52%. The S&P 500 Stock Index fell 0.97%, while the Nasdaq Composite fell 1.87%. The Russell 2000 small capitalization index lost 5.12% this week.

- The Hang Seng Composite gained 2.50% this week; while Taiwan was up 1.32% and the KOSPI rose 1.83%.

- The 10-year Treasury bond yield fell 6 basis points to 1.29%.

Airline Sector

Strengths

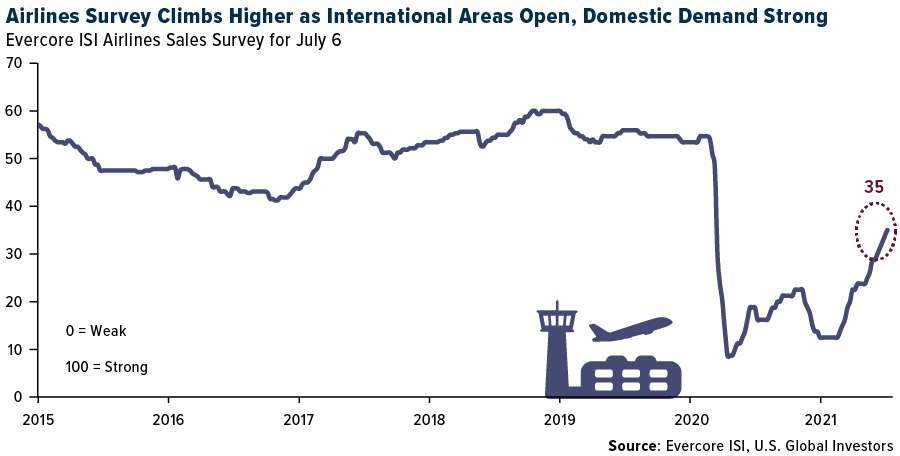

- The best performing airline stock for the week was Bombardier, up 5.8%. ISI’s Airline Survey of overall forward revenue continues to climb higher, increasing from 33.8 to 35.0, while the international portion of the index rose from 7.5 to 10.0. Domestic leisure travel demand remains the area of greatest recovery, with international demand lagging. However, recent data is encouraging in terms of areas that are starting to reopen. Mexico and the Caribbean are solid, for example, while trans-Atlantic is looking a little better as more countries loosen restrictions.

- Airline traffic continues to improve. According to UBS, the most recent datapoint for July shows booked traffic at -13% versus 2019 levels (which was -27% last week). August was at -20% (versus -26%) and September came in at -2% (the first datapoint for August was -28%).

- Earnings are being reported better than guidance. American Airlines pre-announced its second quarter results better than consensus due to costs being 2-5% below the previous guidance. Revenues were slightly higher than consensus due to higher traffic volumes. Delta Air Lines also reported better-than-expected earnings due to strong revenues. The third quarter is expected to be profitable, and the company indicated that leisure demand is back to pre-pandemic levels while corporate demand is at 40% of pre-pandemic levels. Alaska Airlines published an investor update guiding to higher-than-expected operating cash flow, an improved cost outlook, and revenue at the better end of its prior guidance range (down 33% versus down 33% to 35% prior). Notably, the company produced a pretax profit during the month of June, the first profitable month since February 2020.

Weaknesses

- The worst performing airline stock for the week was Great Lakes, down 57.1%. Fuel prices continue to increase, which could be worrisome for the industry. In fact, jet fuel is up 15% in the second quarter and is up 42% year-to-date. This is due to higher oil prices being passed on by refineries.

- Airline growth is improving, but not at the rate that the consensus is expecting. U.S. to European planned capacity growth for the second quarter is down 74% versus the second quarter of 2019 (and down 77% in the first quarter of 2021). Early looks at the third quarter indicate a 52% year-to-year decline, down 380 basis points.

- The Financial Times reports that the European Commission will announce the planned introduction of a tax on jet fuel for the first time on Wednesday, to help the European Union (EU) meet its ambition of reducing average carbon emissions by 55% by 2030. Jet fuel is not currently taxed in the EU per Article 14 of the 2003 Energy Taxation Directive. The move would reportedly require unanimous backing from the 27-member states.

Opportunities

- According to Morgan Stanley, the second quarter will likely be the last quarter for U.S. airlines experiencing red ink across the board as the economic and travel recovery gather momentum. The second quarter was soft to start as vaccinations in the U.S. slowly picked up steam but once restrictions started to come down, there was a surge of travelers into quarter end.

- Canada is working toward its vaccination targets (38% fully vaccinated versus 20% target; 69% of population has one dose versus 75% target) and is inching closer to a potential reopening in August. Based on U.S. trends, a pickup in vaccination rates and a loosening of restrictions could spur pent up demand in the second half of 2021 and early 2022 as Canadians are allowed to travel again and the transborder opens. • Porter Airlines’ decision to purchase up to 80 new E195-E2’s to expand service to new routes across North America represents a fairly meaningful acceleration of its growth strategy in Canada. However, the new aircraft will not go into service until the second half of 2022.

- Porter intends to operate the E2s from popular destinations such as Ottawa, Montreal, Halifax, and Toronto Pearson. While the news has Porter establishing service at Pearson Airport for the first time, the company will still operate flights from its existing hub at downtown Toronto’s Billy Bishop Airport.

Threats

- Starting in September 2021, American Airlines is facing a lot of Southwest Airlines and Spirit Airlines capacity growth into its routes, with Southwest increasing capacity +34%/+41%/+32% and Spirit increasing capacity +26%/+47%/+44% for September/October/November, respectively.

- Bank of America expects it will be challenging for airlines to pass on higher costs this year given the early stages of the travel recovery and excess capacity, which has resulted in the bank’s lowering of forecasts. European airlines have reduced hedging levels to 50-90% of their 12-month jet-fuel consumption. Soaring carbon prices and more-stringent EU regulation for aviation carbon emissions are likely to result in significantly higher carbon costs for European airlines. The bank estimates that the EU carbon costs will more than double from 2019 to 2022 for European airlines on average, representing 2.5% of revenues in 2022.

- With the delta variant of the coronavirus sweeping through many regions of the world, parts of Asia, Australia and Europe have reintroduced travel restrictions. With varying restrictions across the world and different paces of vaccination rollout, the international recovery remains a slow process. While international tickets sold took another slight step up to -35.7% versus 2019 (versus -38.4% last week and -40.1% the week prior), the pace of improvement has slowed down when compared to leisure/corporate travel.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was the Czech Republic gaining 3.80%. The best performing country in Asia for the week was South Korea, gaining 0.8%.

- The Turkish lira was the best performing currency in emerging Europe, gaining 1.6%. The South Korean won was the best performing currency in Asia for the week, gaining 0.55%.

- China’s customs export growth accelerated to 32.2% year-over-year in June from 27.9% a month prior, defying expectation of a moderation to 23.1%. Imports were also better than expected at 36.7% versus consensus 30.0%, following 51.1% in May. Trade balance improved.

Weaknesses

- The worst performing country in emerging Europe for the week was Russia, losing 2.2%. The worst performing country in Asia for the week was Vietnam, losing 3.6%.

- The Hungarian forint was the worst performing currency in emerging Europe this week, losing 1.7%. The Philippine peso was the worst performing currency in Asia, losing 0.75%.

- China’s corporate bond defaults hit a record high. Local governments are less willing to bail out troubled state-owned firms. Bond defaults have totaled CNY62.59 billion ($9.67 billion) in the first six months of this year. Fitch said 25 firms had defaulted in the first half of 2021 versus 19 in the first half of 2020.

Opportunities

- European Central Bank (ECB) President Lagarde said the upcoming July 22 ECB meeting will have “some interesting variations and changes.” She added that “it’s going to be an important meeting. Given the persistence that we need to demonstrate to deliver on our commitment, forward guidance will certainly be revisited.” Lagarde also said that she expects the current EUR1.85 trillion pandemic emergency purchase program to run at least until March 2022, followed by a transition into a new format. Fresh measures may be introduced to support the euro-area economy after the current bond buying program ends next year.

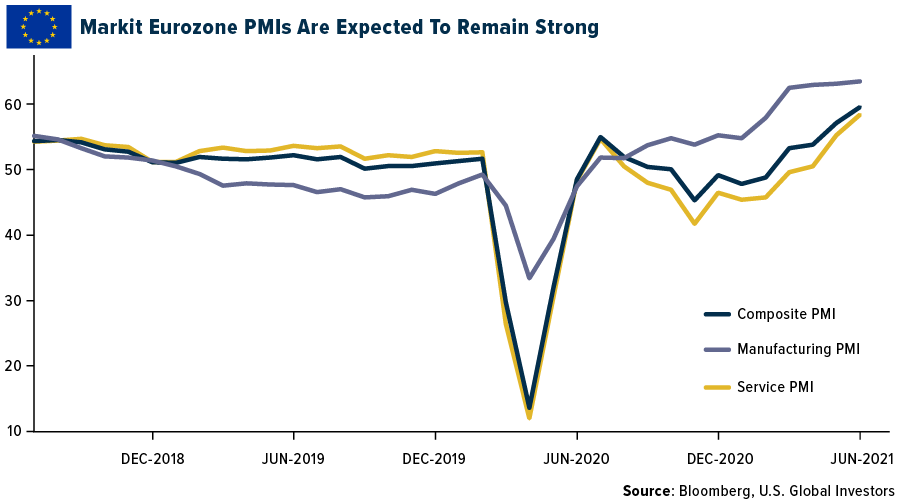

- Next week the purchasing managers’ index (PMI) data will come in for the Eurozone. Service and Manufacturing PMIs should remain strong due to better pandemic situations in many parts of Europe. Many markets allowed tourists to travel again over the summer months, which bodes well for Service PMI.

- Amundi SA, a Paris-based firm, is planning to more than double assets under management in China, Hong Kong, and Taiwan by 2025. The firm currently holds $120 billion in these markets and wants to increase its exposure to $250 billion.

Threats

- Poland has postponed a Constitutional Court verdict, on whether EU or Polish law has primacy in the country. The EU Commission has urged Poland to scrap the procedure. Polish human rights activist Ombudsman Adam Bodnar said the process "sooner or later will lead to Poland’s removal from the EU."

- Last week, the People’s Bank of China (PBOC) surprisingly cut its lenders’ reserve required ratio. The move may be a sign that China is worried about slowing economic growth momentum while uncertainties remain high. Specifically, the latest coronavirus outbreak in the Guangdong province affected port activity and slowed export turnover.

- The Cyberspace Administration of China on Saturday proposed draft rules calling for all data-rich tech companies with over 1 million users to undergo security reviews before listing overseas in the wake of the regulatory probe of Didi Chuxing last week. The security review will put a focus on risks of data being affected, controlled, or manipulated by foreign governments overseas.

Energy and Natural Resources Market

Strengths

- The best performing commodity for the week was wheat, up 12.60%. U.S. wheat futures edged higher on Friday and set for the biggest weekly gain in four years as adverse weather stoked concerns about global supplies.

- Goldman Sachs and Credit Suisse upgraded their price forecasts for the iron ore amidst expectations of a tighter market, while iron ore futures rose 6.15% during the week. Analysts noted that there’s a lack of material supply in response to higher prices and that there’s no additional investment to accelerate production from major miners. During the first half of the year, prices for iron ore have whipsawed as China took steps to cool the commodity boom.

- Copper and tin rose on the back of stronger economic data from China and the continued recovery in the U.S. economy. China reported that its gross domestic product (GDP) grew 7.9% year-over-year in the second quarter, showing more balance as consumer spending also picked up. Meanwhile, applications for U.S. state unemployment insurance fell to a pandemic low last week. This continuous recovery in the two biggest copper-consuming nations point to increasing global demand. Copper was essentially flat at -0.52% this week, while tin was up 5.23%, drawing closer to an all-time high.

Weaknesses

- The worst performing commodity for the week was lumber, falling 28.94%. Lumber futures tanked more than 40% in June alone, suffering their worst month on record dating back to 1978. After the June price rate increase, lumber prices have come back down this week as supply increased, speculative trading action cooled, and homebuilding demand eased.

- Oil fell to a four-week low this week on the back of the Organization of Petroleum Exporting Countries and its allies (OPEC+) signaling that it could raise output soon and a strengthening U.S. dollar. Delegates of the OPEC+ alliance said that the United Arab Emirates and Saudi Arabia made significant progress towards resolving their standoff, and an inventory report in the U.S. showed that expanding fuel supplies and crude production also weighed on the prices. West Texas Intermediate (WTI) declined 3.69%.

- A study conducted by the University of Texas at Austin on the deep freeze that gripped Texas in February concluded that parts of the natural gas delivery system failed, leading to mass power outages, while the state grid operator underestimated power demand from the freeze by 14%. It also added that some power generators were inadequately prepared for such extreme weather and that natural gas storage was also limited. The power outages led to the death of at least 150 people and had left millions without power for days.

Opportunities

- Demand for lithium is expected to grow by 20% for 2022 and by 35% for 2030 when compared to the second half of 2020, according to a report by BloombergNEF. This year, higher demand and a tightness in the supply side has pushed lithium hydroxide and lithium carbonate prices up 25% and 38% respectively. With a push to increase electric vehicle adoption across the globe, demand for energy-dense batteries that require lithium hydroxide would mean a higher upside than carbonate, which historically has traded at a 19% discount to hydroxide.

- The Western Green Energy Hub, proposed to be the largest renewables project in the world to be built in Western Australia, could have a capacity of 50 gigawatts of wind and solar energy covering more than 5,800 square miles, around half the size of Belgium. The project is expected to cost $75 billion and can produce as much as 3.5 million tons of green hydrogen or 20 million tons of green ammonia per year for export and domestic use. InterContinental Energy and CWP Global, two members of the consortium behind the proposal, are also involved in the Asian Renewable Energy Hub.

- Royal Dutch Shell is stepping up its operations of capturing carbon emissions and burying them underground and believes that it could be a money-maker for the oil and gas companies developing the technology. Shell’s Head of Integrated Gas, Renewables and New Energy Solutions said that the industry is going to create the use of carbon capture and storage (CCS) as a service to industries of all sorts. Currently, Shell is linked to several CCS projects, including the Northern Lights project backed by Equinor ASA and TotalEnergies SE, which will liquefy industrial carbon dioxide to transport and bury offshore. Shell also proposed building a large-scale facility with a 300-million-ton storage capacity at its Scotford complex in Alberta, Canada.

Threats

- Rise in commodity prices was put in focus as Siemens Gamesa Renewable Energy SA warned of a profit decline as the company, which specialized in wind farm construction and related services, cut its 2021 revenue forecast to the lower end of its earlier estimates, and reduced its margin forecast. This news led to the slide in Europe’s biggest wind-turbine markers as Vestas Wind Systems A/S and Nordex SE fell along with Siemens Gamesa. Director at E3 Analytics, a renewables consultancy firm, said that the knock-on effects of rising commodity prices could lead to project delays and even project cancellations.

- To reduce carbon emissions, many cities around the U.S. are considering phasing out natural gas hookups to homes and businesses, the Wall Street Journal reports. Restaurants and chefs are pushing back against local laws and ordinances banning gas, arguing that electric stoves do not achieve the same quality of cooking, but so far, such challenges have been dismissed. “Americans love cooking with gas, so it is understandable that misguided policy makers would try to soften the blow of policies that eliminate affordable, reliable and clean natural gas by exempting natural gas for cooking,” commented Karen Harbert, president of the American Gas Association, which has lobbied to defend stovetop cooking.

- The historic heatwave and drought in the Pacific Northwest are decimating this year’s crop of wheat and fruit and may contribute to already increasing food inflation. Last week the U.S. Agriculture Department rated nearly 70% of Washington State’s spring wheat and 36% of its winter wheat in poor or very poor condition, Reuters reports. The soft white wheat grown in the region is prized by Asian buyers, who use it to make noodles. Some Washington counties, including Benton and Yakima, have seen “complete crop failures,” according to the Seattle Times.

Domestic Economy and Equities

Strengths

- Jobless claims hit a fresh pandemic low. Weekly initial jobless claims were released at 360,000, in line with consensus and better than the prior week’s upwardly revised numbers. The latest reading was the lowest since March of last year.

- Confidence among small businesses in the United States improved slightly in June after declining in May, despite owners worrying about a labor shortage and inflation. The National Federation of Independent Business Optimism Index rose 2.9 points to a reading of 102.5 in June.

- Ever Source Energy was the best performing S&P 500 stock for the week, increasing 5.7%. The company will publish its latest earnings at the end of July.

Weaknesses

- Industrial production increased 0.4% in June after moving up 0.7% in May, below expected increases of 0.6%. The chip shortage continues to weigh on the automotive sector.

- June headline CPI increased to 0.9% month-over-month, well above May’s 0.6% monthly pace and consensus for 0.5%. It was the fourth consecutive monthly beat for headline CPI and fastest monthly rise since 2008. Inflation spiked to 5.4% year-over-year, higher than consensus of 4.9% and May’s 5.0% rate. The debate remains over what proportion of these price hikes is transitory.

- Norwegian Cruise Line was the worst performing S&P 500 stock for the week, losing 15.8%. Shares declined following the escalation of the company’s battle against Florida’s Surgeon General prohibiting “vaccine passports.”

Opportunities

- Preliminary July PMIs will be released next week. Manufacturing, Service, and Composite PMIs should all remain strong supported by markets re-opening and huge fiscal and monetary stimulus.

- According to FactSet’s latest Earnings Insight report, S&P 500 earnings are expected to increase 64% year-over-year in the second quarter, up over 12% from the start of the quarter. This would mark the best performance since the fourth quarter of 2009 when earnings grew nearly 110%. Strong company earnings should positively impact the stock market’s performance.

- Michigan consumer confidence, which is regarded as a leading indicator of consumer sentiment in the United States, will likely move higher next week. Michigan’s current condition will be released the same day; this should point to further economic recovery from the pandemic.

Threats

- Senate Majority Leader Schumer and Budget Committee Democrats led by Senator Sanders reached a deal late Tuesday on a proposal that sets a limit of $3.5 trillion for an infrastructure package. Sanders backed the proposal, despite a price tag lower than the $6 trillion he pushed for. Schumer has said he wants to hold votes on the two packages before the August recess. Some moderate Democrats have said they might not support anything over $2 trillion.

- Reuters polled over 100 economists finding that a strong majority expects the Federal Reserve will shutter its asset purchase program by the end of 2022, with a few more predicting a rate hike as early as next year. They see new COVID-19 variants as the biggest economic risk. Only two respondents to the survey expect quantitative easing to end later, in early 2023.

- U.S.-China tensions continue to escalate. China refused to grant President Biden’s deputy secretary of state a meeting with her counterpart. On Friday, the Biden administration issued a blanket warning to U.S. firms about the risks of doing business in Hong Kong. The U.S. is also expected to sanction Chinese officials over Beijing’s crackdown on Hong Kong democracy.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Axie Infinity, rising 49.67%.

- The European Central Bank (ECB) reported that it will start the investigation phase of a Eurozone central bank digital currency (CBDC), which can last up to 24 months. ECB’s President, Christine Lagarde, said in March that a CBDC could be launched within four years; the ECB started discussing the potential of a CBDC for the 19 Eurozone countries in January of this year.

- The People’s Bank of China (PBOC) reported that the total value of transactions using the country’s central bank digital currency (CBDC) reached $5 billion by the end of June, adding that to the total number of transactions at 70.75 million, across 21 million personal wallets and 3.5 million enterprise wallets. The digital yuan, China’s CBDC, will be compatible with smart contracts and has been under trial for over a year. PBOC did not give a timetable for the CBDC’s launch, but its progress will surely push other nations to experiment with their own CBDC’s.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performer for the week was Telcoin, down 33.46%.

- The U.S. Securities and Exchange Commission (SEC) postponed its decision on WisdomTree’s Bitcoin ETF application. The SEC is seeking feedback from the public and industry experts on the application to determine whether the Bitcoin ETF would be a safe investment product. Currently, the SEC is reviewing over a dozen active Bitcoin ETF applications, and even delayed its decision on VacEck’s application. The U.S. regulator has raised concerns around crypto market manipulation and investor protection.

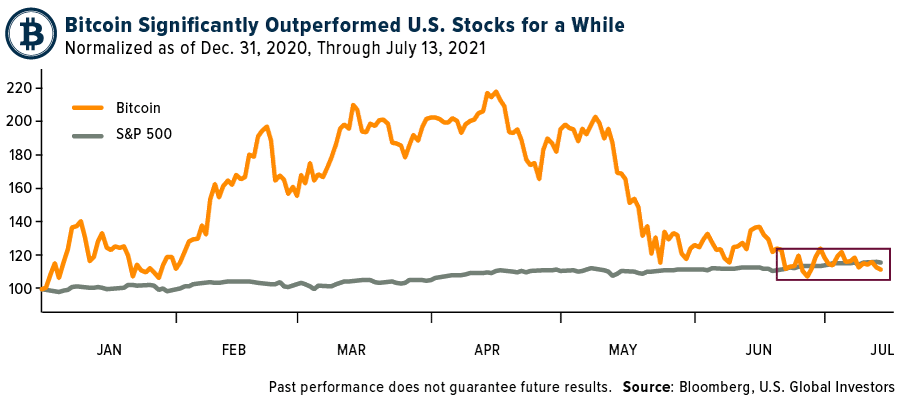

- Binance, the largest cryptocurrency exchange in the world, is set to stop support and service for tokens linked to stocks. The service, which began three months ago, has received scrutiny from regulatory bodies around the world. With the stock tokens, Binance allowed its customers to buy fractions of shares in companies like Tesla, Coinbase, Microstrategy, Microsoft and Apple. Support for these tokens will end on October 14, 2021. Binance has been issued warnings against operating in the U.K., Japan, and Hong Kong. Furthermore, Bitcoin’s gains for the year are now comparable to that of the S&P 500 and the chart below shows the largest cryptocurrency’s performance this year, which peaked in April and has slid ever since.

Opportunities

- Hashdex Ltd., a Brazilian digital asset management firm, is set to launch a Bitcoin exchange traded fund (ETF) which will use a portion of its management fee to buy carbon credits to offset the carbon produced by the Bitcoin held in the fund. The Hashdex Nasdaq Bitcoin Reference Price Index Fund (BITH11) will list on the Brazilian stock exchange B3 on August 4, 2021. Hashdex will partner with the Crypto Carbon Ratings Institute (CCRI) to generate annual reports with estimates of energy consumption and carbon emissions related to the mining process of all Bitcoins acquired by BITH11.

- Bank of America announced that it has approved trading of Bitcoin futures for certain clients. Due to increased demand, the second-largest bank in the U.S. will trade the Chicago Mercantile Exchange (CME) Bitcoin futures on behalf of clients. This news comes a few weeks after it emerged that Bank of America had created a team dedicated toward researching cryptocurrencies and related technologies. CME is the leading Bitcoin futures trading platform, with a total open interest at $11.3 billion, which is down from its April 13 peak of $27.3 billion.

- Square Inc.’s CEO Jack Dorsey said that the company is opening a new business to focus on creating an open developer platform to provide non-custodial, decentralized financial services, adding that the unnamed division’s primary focus will be Bitcoin. Square already has Square Crypto, a division working on the Lightning Development Kit to allow for quicker and easier payments.

Threats

- State governments in provinces of Anhui, Henan, and Gansu ordered a halt of cryptocurrency mining operations. This is the latest in a series of similar orders implemented in other provinces of China amidst a nationwide crackdown on the industry. The government has increased its efforts to curb crypto mining operations due to environmental and financial concerns.

- India’s ICICI Bank, one of the country’s largest private lenders, reported that its customers that intend to transfer money under the Reserve Bank of India’s (RBI) remittance scheme will need to sign a declaration stating that proceeds will not be used for trading cryptocurrencies and that the proceeds are not from redemption of cryptocurrency investments. The regulatory environment for cryptocurrencies in India remains uncertain as several private banks have decided against offering services to cryptocurrency-related businesses.

- ApeRocket, which is a decentralized finance (DeFi) protocol built on the Binance Smart Chain, suffered two flash loan attacks, costing users around $1.26 million. This is one of several flash loans attacks that have occurred in the DeFi space within this year, and Binance Smart Chain has been at the center of many of those hacks. Such DeFi yield farming protocols allow individuals to earn interest or rewards on their crypto deposits, but this nascent space has suffered hacks which deter increased participation.

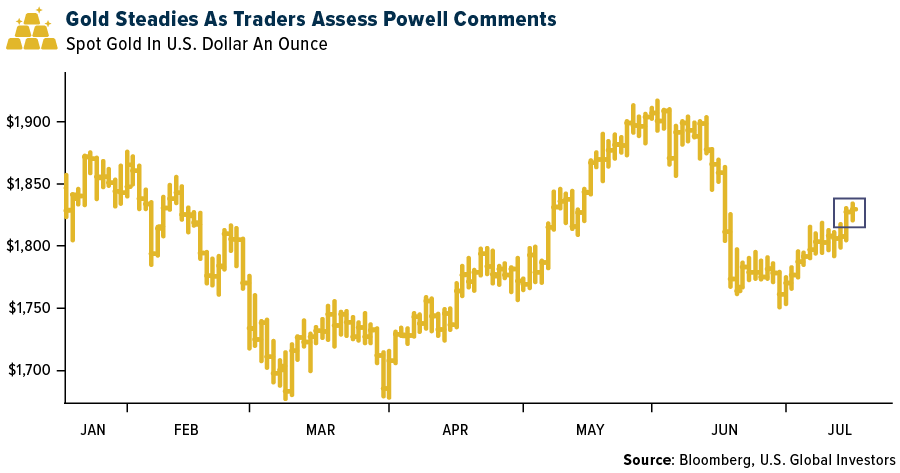

Gold Market

For the week ended July 16, spot gold closed at $1,812.05, up $3.73 per ounce, or 0.21%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 0.66%. The S&P/TSX Venture Index came in off 3.21%. The U.S. Trade-Weighted Dollar rose 0.60%.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Jul-13 | Germany CPI YoY | 2.3% | 2.3% | 2.3% |

| Jul-13 | CPI YoY | 4.9% | 5.4% | 5.0% |

| Jul-14 | PPI Final Demand YoY | 6.7% | 7.3% | 6.6% |

| Jul-14 | China Retail Sales YoY | 10.9% | 12.1% | 12.4% |

| Jul-15 | Initial Jobless Claims | 350k | 360k | 386k |

| Jul-16 | Eurozone CPI Core YoY | 0.9% | 0.9% | 0.9% |

| Jul-20 | Housing Starts | 1590k | — | 1572k |

| Jul-22 | ECB Main Refinancing Rate | 0.000% | — | 0.000% |

| Jul-22 | Initial Jobless Claims | 350k | — | 360k |

Strengths

- The best performing precious metal for the week was gold, up 0.21%. Gold remained stable during the week as bond yields retreated and investors weighed the outlook for global growth on concerns that coronavirus variants may threaten the economic recovery. The dip in Treasury yields last week helped boost the appeal of the non-interest-bearing metal. Gold then stabilized later in the week as the dollar and Treasury yields pared some of their gains made in the wake of U.S. inflation data that came in significantly higher than expected. Prices paid by U.S. consumers surged in June by the most since 2008, topping all forecasts and testing the Federal Reserve’s commitment to sticking with ultra-easy monetary support for the economy.

- A UBS call with a leading diamond expert indicates diamond market fundamentals remain attractive with demand strong in the U.S. and China with mid-stream and producer inventories healthy. Midstream inventories have fallen to more sustainable levels due to structural changes and tighter credit, and profitability has returned. Supply fell 6% in 2020 to 119 million carats, the lowest level since the 1990s, due to curtailments/closures. Rough prices are back to pre-COVID levels, after falling 15% in the first half of 2020.

- Kirkland Lake Gold reported positive production and sales information. The company produced 379,000 ounces of gold in the second quarter, 9% above consensus. Second quarter sales were 365,000 ounces, 5% above consensus. The company expects to end 2021 in the top half of 1.3-1.4-million-ounce guidance. Dundee Precious Metals reported preliminary production results for the second quarter as well, with consolidated gold output of 85,100 ounces exceeding consensus of 73,700 ounces. Gold production at Chelopech was very strong with 52,600 ounces benefiting from higher grades and improved recoveries. Performance remained solid at Ada Tepe. Dundee has produced 155,400 ounces and puts the company in good shape to aim for the higher end of the guidance range.

Weaknesses

- The worst performing precious metal for the week was palladium, down 6.45% as UBS reported substitution with cheaper platinum is already taking place in auto-catalysts, becoming more pronounced in 2022. New Gold reported that weaker performance was achieved at Rainy River due to lower grades—stronger Rainy River second-half results are expected, but the mine is reportedly now on track to achieve the low end of guidance.

- Fiore Gold released production for the three months ended June 30 of 11,800 ounces, slightly below estimate of 12,400 ounces from Stifel, but up 8% from the second quarter. The miss against Stifel’s numbers was driven by lower tons stacked and lower grade. The company ended the quarter with a cash balance of $18.5 million, slightly below anticipated $20.4 million.

- Pure Gold announced second quarter production results. Second quarter (pre-commercial) gold production of 6,300 ounces was 40% below the 10,400-ounce forecast. Average daily mill throughput in the quarter of 509 tons per day was below the average 538 tons per day delivered in the first quarter.

Opportunities

- According to the CEO of Barrick Gold, Mark Bristow, due to an aggressive near-mine exploration program, Kibali was continuing to replace its reserves faster than it was mining them, and now has a resource base that is approaching the 2013 levels when the mine first went into production. The company also said that significant exploration successes could extend the Tongon gold mine’s life. Bristow said 10 years after it went into production Tongon could get a new lease on life thanks to promising results from near-mine exploration campaigns designed to replace the mine’s depleted reserves.

- AngloGold Ashanti is pleased to announce that a non-binding proposal has been submitted to the Board of Directors of Corvus Gold Inc. under which its direct wholly owned subsidiary, AngloGold Ashanti Holdings plc, would be willing to acquire for cash all the issued and outstanding common shares of Corvus. AngloGold Ashanti currently holds a 19.5% indirect interest in Corvus.

- Aya Gold & Silver reported second quarter production from Zgounder of 439,100 ounces handily beating aggressive estimates of 401,700 ounces due to higher throughput and head grade. This puts the mine on track for 1.66 million ounces in 2021, well above guidance of 1.2 million ounces.

Threats

- Jefferies is cautious on mining equities in the near-term as investors’ sentiment has turned more negative on the sector. The group said, “we attribute the weakness to the delta variant of coronavirus and associated lockdowns, China tightening, and fears of weaker demand as some believe global growth has peaked.”

- On July 15, Barrick reported that an incident occurred at its Hemlo mine on the evening of July 14, resulting in the death of a contractor. Hemlo operations are suspended and an investigation is underway.

- Sibanye Stillwater Ltd. may wind down its three South African gold mines in the next decade or so as it becomes harder to exploit aging assets in an industry that was once the world’s largest. Sibanye, which was spun off from Gold Fields’ oldest South African mines in 2013, employs about one-third of the roughly 93,000 workers in the nation’s gold industry. Sibanye is actively seeking gold acquisitions, likely in North America.

Leaders and Laggards

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (06/30/2021):

Alaska Airlines

American Airlines

Delta Air Lines

Southwest Airlines

Spirit Airlines

ConocoPhillips

Valero Energy Corp.

Phillips 66

Halliburton Co.

Kirkland Lake Gold

Dundee Precious Metals

Fiore Gold

Pure Gold Mining

Barrick Gold

Aya Gold and Silver

AngloGold Ashanti

Corvus Gold Inc.

Sibanye Stillwater Ltd.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

Cash Flow is a measure of the amount of cash generated by a company’s normal business operations.

The National Federation of Independent Business’s (NFIB) Index of business optimism is based on responses from 1221 member firms.

The S&P Oil & Gas Exploration & Production Select Industry Index represents the oil and gas exploration and production segment of the S&P Total Market Index. The oil and gas exploration and production segment of the S&P TMI comprises the following sub-industries: Integrated Oil & Gas, Oil & Gas Exploration & Production, and Oil & Gas Refining & Marketing.

The Producer Price Index (PPI) measures prices received by producers at the first commercial sale. The index measures goods at three stages of production: finished, intermediate and crude.