Dollar Weakness Could Be the Catalyst Commodities Are Looking For

Date Posted: January 10, 2020

Read time: 61 min

Commodities as a whole had a mostly positive 2019, returning 16.53 percent as measured by the S&P GSCI. This far surpasses the five-year average of about negative 11.52 percent, between 2014 and 2018.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

It’s that time of year again! Near the start of every year, I share with you our ever-popular Periodic Table of Commodity Returns, now updated to reflect the final results of 2019. To view the interactive table and download a copy of your own, click here.

Commodities as a whole had a mostly positive 2019, returning 16.53 percent as measured by the S&P GSCI. This far surpasses the five-year average of about negative 11.52 percent, between 2014 and 2018.

Precious metals were responsible for much of the growth. For the third straight year, and for the fourth time in six years, palladium was the top-performing commodity. The metal, used widely in the production of catalytic converters, increased an incredible 54.21 percent to end 2019 at $1,912 an ounce, a slightly higher price than gold’s all-time high set in September 2011.

As was the case in past years, palladium benefited from mounting global demand to curb emissions from gasoline-burning engines. It’s also among the world’s scarcest precious metals, mined primarily in Russia and South Africa, which means supply will potentially remain in deficit for years to come.

Having broken above $2,000 an ounce earlier in the week, palladium in now forecast by Citi analysts to hit $2,500 by the middle of this year.

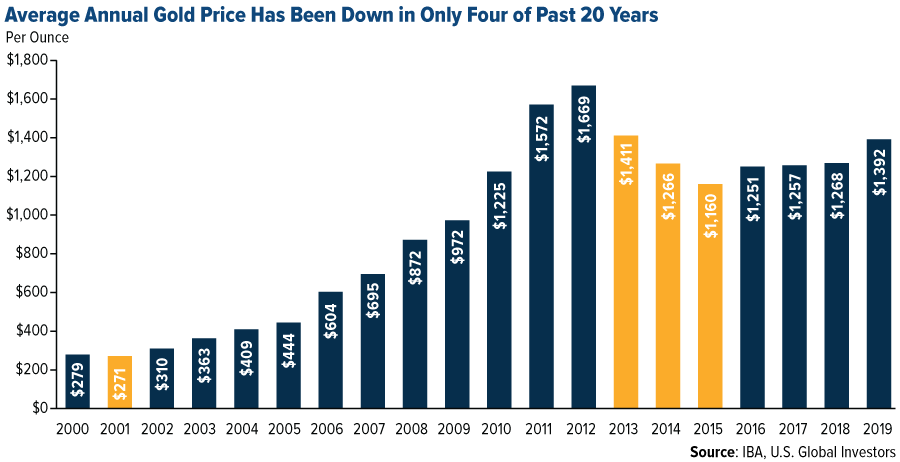

Gold Price Up in Four out of Every Five Years

Gold, meanwhile, had its best year since 2010, climbing as much as 18.31 percent. The yellow metal’s role as an exceptional store of value shined brightly in the second half of the year when the pool of negative-yielding debt around the world began to skyrocket, eventually topping out at around $17 trillion in August. On the news this week that Iran launched a counterstrike against U.S.-occupied military bases in Iraq, the safe haven briefly broke above $1,600 an ounce for the first time since April 2013.

In the past two decades, gold has helped investors limit market volatility and portfolio losses. Between 2000 and 2019, the precious metal’s average annual price was down in only four years. Put another way, gold was up on average in four out of every five years—a remarkable track record.

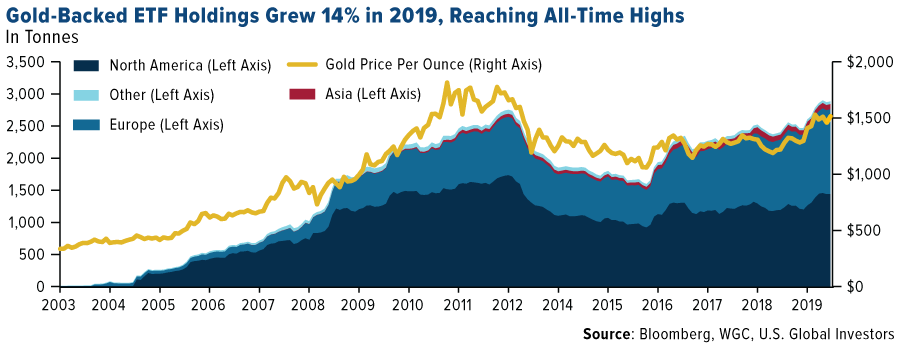

Safe haven-seeking investors around the world piled into gold-backed ETFs in 2019, making it the best year on record for gold holdings. Assets under management (AUM) in gold bullion ETFs expanded 37 percent from the previous year, adding $19.2 billion, or 400 tonnes, according to the World Gold Council (WGC). During the fourth quarter, total holdings hit a jaw-dropping 2,900 tonnes, the equivalent of 102 million ounces, which is the most on record.

As of the end of this week, gold looks slightly overbought on a relative strength basis, meaning a correction wouldn’t be such a bad thing and in fact expected.

Has the Greenback Peaked?

Short of escalating tensions in the Middle East or a pullback in stocks, the catalyst for higher gold prices—and, indeed, commodity prices in general—may very well be a substantial weakening of the U.S. dollar. On Tuesday, the U.S. Dollar Index experienced a “death cross,” a bearish signal that takes places when an asset’s 50-day moving average crosses below its 200-day moving average. We haven’t seen this from the greenback since May 2017.

Other firms and analysts have recently made the case that the dollar is ready to decline in 2020, which would give gold and other hard assets the room to gain momentum. Below are just three such forecasts from the past couple of weeks:

“Our view is that the dollar is ready to decline in 2020 and will be encouraged to do so as negative interest rates abroad turn less negative while the Fed holds pat (or cuts)… In the event of an unlikely recession in 2020, U.S. fiscal and monetary policy will turn sharply expansionary, the dollar will decline further, and gold will do well.”

~Murenbeeld & Co., January 3

“We expect that U.S. dollar weakness will likely characterize global financial markets throughout 2020… A weaker dollar is always good news for commodity prices. We are particularly bullish gold at this point. Gold is a direct play on a weaker dollar and could also benefit from any major flare-up in geopolitical tensions.”

~Alpine Macro, January 6

“Starting 2020, the key setup from a macro perspective is the confirmed top in the U.S. Dollar Index as well as the U.S. Trade-Weighted Broad Dollar Index… The U.S. Dollar Index (DXY) has broken below the 97 support to trigger the bearish implication of the June-December topping pattern (head-and-shoulders top) and the U.S. Trade-Weighted Broad Dollar Index has broken below the early-November 2019 low as well as the 200-day moving average to confirm a similar topping pattern to the DXY.”

~CLSA, January 7

Bitcoin as a Safe Haven Asset

Gold isn’t the only asset that responded positively to geopolitical uncertainty involving Iran. The price of bitcoin, the world’s largest cryptocurrency by market cap, surged on the news that President Donald Trump had ordered a strike on Iranian general Qasem Soleimani, before commenting that the U.S. was targeting as many as 52 sites in Iran.

From January 2, the day before the strike, to January 8, when Trump announced that Iran appeared to be “standing down,” bitcoin traded up as much as 21 percent to its highest level in six weeks. In addition, there were reports that local bitcoin sellers in Iran were charging three times the market rate in response to the threat of war with the U.S.

Google searches for “bitcoin” were also up. Cointelegraph reports that the search term “bitcoin Iran” exploded more than 4,450 percent in the seven days through January 8.

All of this tells me that bitcoin continues to mature as an asset, and that investors and savers increasingly trust it as a store of value in times of uncertainty.

Looking for the inside scoop on mining companies? Click here to read U.S. Global Investors portfolio manager Ralph Aldis’ interview with MoneyShow and get his favorite mining picks for 2020!

Gold Market

This week spot gold closed at $1,562.34, up $10.14 per ounce, or 0.65 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 2.63 percent. The S&P/TSX Venture Index came in off just 0.87 percent. The U.S. Trade-Weighted Dollar rose 0.53 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Jan-7 | Eurozone CPI Core YoY | 1.3% | 1.3% | 1.3% |

| Jan-7 | Durable Goods Orders | -2.0% | -2.1% | -2.0% |

| Jan-8 | ADP Employment Change | 160k | 202k | 124k |

| Jan-9 | Initial Jobless Claims | 220k | 214k | 223k |

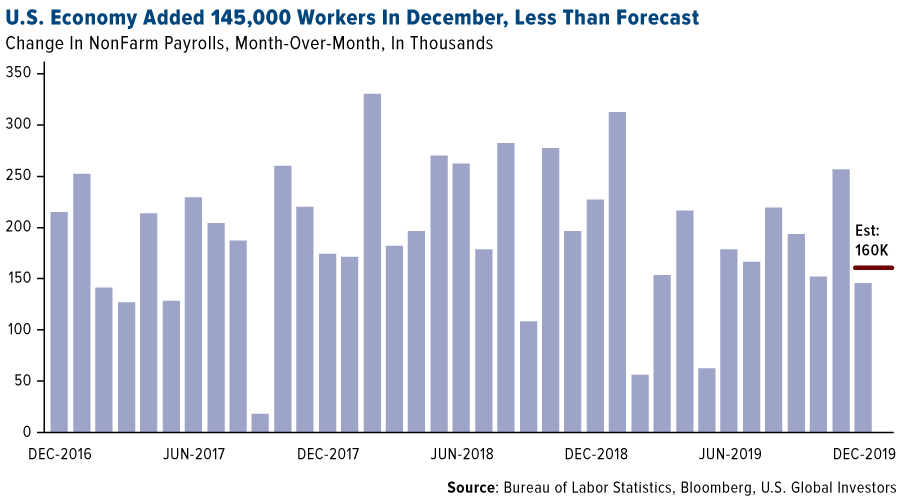

| Jan-10 | Change in Nonfarm Payrolls | 160k | 145k | 256k |

| Jan-14 | CPI YoY | 2.4% | — | 2.1% |

| Jan-15 | PPI Final Demand YoY | 1.3% | — | 1.1% |

| Jan-16 | Germany CPI YoY | 1.5% | — | 1.5% |

| Jan-16 | Initial Jobless Claims | 220k | — | 214k |

| Jan-16 | China Retail Sales YoY | 7.9% | — | 8.0% |

| Jan-17 | CPI Core YoY | 1.3% | — | 1.3% |

| Jan-17 | Housing Starts | 1380k | — | 1365k |

Strengths

- The best performing metal this week was palladium, up 6.48 percent, notching its best weekly advance since June. While global car sales are weak, loadings for their catalytic converters are going up with regulatory requirements.Gold traders and analysts were spilt on their outlook for the yellow metal next week after this week saw big price swings due to U.S.-Iran tensions escalating then subsiding. Gold futures swung between gains and losses on Friday as traders assessed slower-than-expected hiring and wage growth against low unemployment. Bloomberg reports that nonfarm payrolls rose 145,000, below expectations of 256,000, and average hourly earnings climbed 2.9 percent – the first below 3 percent reading since July 2018.

- The Perth Mint reported that gold coin and minted bar sales in December totaled 78,912 ounces – a big jump from November’s 54,261 ounces. BullionVault said the number of first-time precious metals investors using the service grew 25 percent to a two-year high in 2019. The growth was led by clients in the Eurozone. The Royal Mint announced that its bullion division saw a 572 percent boost in sales revenue and a fivefold increase in the average order value over the past weekend compared with the prior weekend, reports Bloomberg. Turkey’s gold reserves rose $2.4 billion from the previous week to bring the central bank’s holdings to $27.5 billion as of January 3.

- Newmont Goldcorp announced on Monday that it is streamlining its name after last year’s megamerger with Goldcorp. The company will now go by simply Newmont, and has promised shareholders a 79 percent increase in its quarterly dividend. Centamin reported that its fourth quarter gold output at the Sukari mine was up 51 percent from the same period last year for a total of 158,387 ounces. The company said its 2019 total gold production was up 2 percent from the previous year. Bloomberg reports that Sibanye Gold Ltd has exercised its option to buy an additional 168 million shares in DRDGold to take controlling shareholding interest in the surface-tailings producer.

Weaknesses

- The worst performing metal this week was platinum, down just 0.28 percent on somewhat of a choppy trading week for the metal. Spot gold surged as much as 2.4 percent on Tuesday to cross the $1,600 an ounce mark for the first time since 2013 after news of the U.S. killing a top Iranian general spurred a retaliatory strike on U.S. interests. Geopolitical tensions are historically positive for the yellow metal as it is seen as a perceived safe haven asset. Relations between the U.S. and Iran cooled later in the week and gold subsequently fell back toward $1,540 an ounce. David Govett, head of precious metals trading at Marex Spectron Group, says the “focus will now return to economic drivers as opposed to conflict worries.”

- The All India Gems and Jewellery Domestic Council said this week that the total business volume of gems and jewellery industry has posted a 30 percent decline in terms of demand over the last six months. Chairman Anantha Padmanabhan claims that due to the increase in customs duty, goods and services tax there was an increase in gold smuggling and customers are opting to purchase gold instead from neighboring countries.

- Evolution Mining forecasts that its gold production for the full year will be at the low end of 725,000 to 775,000 ounces. The miner reported second quarter all in sustaining costs rose 9.9 percent year-over-year to A$1,069.

Opportunities

- Goldman Sachs Group Inc. said in a note this week that gold is a better hedge than oil in the Iranian crisis. “History shows that under most outcomes gold will likely rally to well beyond current levels. This is consistent with our previous research which shows that being long gold is a better hedge to such geopolitical risks.” The bank added that “additional escalation in U.S.-Iranian tensions could further boost gold prices.” According to Citigroup, spot gold prices might breach $1,625 an ounce this quarter due to elevated geopolitical risks sending investors to seek tail risk hedges.

- Brazil plans to allow mining in Amazonian indigenous reserves. Bento Albuquerque, a Navy admiral, told Bloomberg News in an interview that “a majority of the 600 indigenous communities want this” and “nothing is more damaging to the environment than illegal activity.” Although a negative step toward protecting Amazonian lands, the new bill aims to reduce illegal mining, which is more harmful than legal mining operations. The Amazon Geo-Referenced Socio-Environmental Information Network estimates that there are 453 wildcat mines in the Amazon already.

- Scottie Resources Corp. announced positive drill results this week at its Bow Property in British Columbia. Highlights include a drill hole with 73.32 grams per ton of gold and 71.01 grams per ton of silver over a 4.38 meter length. Just days after the results were released, Scottie announced a $2 million private placement financing with Eric Sprott.

Threats

- 2019 was a great year for jobs, but it was also the worst since 2011. Friday data was released showing that employers added 145,000 jobs in December, down from 266,000 in November. Bloomberg’s Reade Pickert writes “the broader picture of a slowdown is in line with what many economists expected in the 11th year of the record-long U.S. expansion, with fading stimulus from tax cuts and headwinds from tariff uncertainty also weighing on hiring.” Pickert adds that a slowdown in jobs growth could weigh on President Trump’s re-election chances.

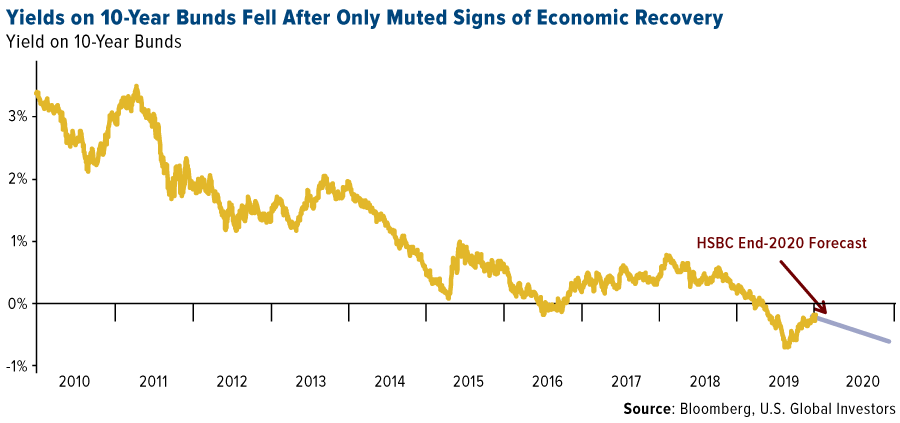

- According to HSBC Holdings, there will be more joy for bond bulls in 2020 as sovereign bonds have smashed expectations in the last ten years. Steven Major, global head of fixed income research, says “low-for-longer interest rates are a reality, no longer a forecast.” In a Bloomberg Opinion piece, Brian Chappatta writes that the bond market looks incredibly expensive as the 30-year Treasury yield is just a few months removed from its all-time low of 1.9 percent. Chappatta cites the “Sherman Ratio”, which shows the amount of yield investors receive for each unit of duration, and it is close to the lowest level ever. This means it would take a smaller move higher in interest rates to wipe out the income return on a fund tracking the Bloomberg Barclays U.S. Aggregate Bond Index. Chappatta says the corporate bond market is “truly frightening” as the Bloomberg Barclays U.S. Corporate Bond Index hit a record-low yield-to-duration ratio that week after a relentless decline in 2019.

- Tax shield investors are piling into funds that plan to take advantage of “opportunity zone” tax incentives that were introduced in the late-2017 tax overhaul signed by President Trump. Investors added $2.26 billion into funds, a 51 percent jump from December, reports Bloomberg. Noah Buhayar writes that opportunity zones were once heralded as a novel way to help distressed parts of the U.S., but they are now being slammed as a “government boondoggle.” The perks of such investing are being used to “juice potential investment returns in luxury developments” and “reports have shown that politically connected investors influenced the selection of zones to benefit themselves.” Meanwhile, an increasing number of hospital bankruptcies have left sick and injured with nowhere to go for treatment. According to data compiled by Bloomberg, at least 30 hospitals entered bankruptcy in 2019 as Americans are leaving rural areas in favor of urban centers. The American Hospital Association calculated that payments from Medicare and Medicaid lagged costs by $76.6 billion in 2018, leaving hospitals struggling to make up for the difference in government reimbursements.

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average gained 0.66 percent. The S&P 500 Stock Index rose 0.96 percent, while the Nasdaq Composite climbed 1.75 percent. The Russell 2000 small capitalization index lost 0.22 percent this week.

- The Hang Seng Composite gained 0.88 percent this week; while Taiwan was down 0.71 percent and the KOSPI rose 1.38 percent.

- The 10-year Treasury bond yield rose 3 basis points to 1.82 percent.

Domestic Equity Market

Strengths

- Information technology was the best performing sector of the week, increasing by 2.17 percent versus an overall increase of 0.92 percent for the S&P 500.

- Apache Corp. was the best performing S&P 500 stock for the week, increasing 26.04 percent.

- Some of the most expensive software stocks are starting 2020 with a bang. Coupa Software, valued at 30.6 times sales, has gained 17 percent over the first seven days of the year, as analysts raised their price targets. Meanwhile, Atlassian, with a multiple of 24.8, has rallied 13 percent. Investors are rushing back to the shares after concerns about frothy valuations triggered a wave of selling in September and October.

Weaknesses

- Energy was the worst performing sector for the week, decreasing by 1.07 percent versus an overall increase of 0.92 percent for the S&P 500.

- Under Armour was the worst performing S&P 500 stock for the week, falling 9.57 percent.

- Walgreens Boots Alliance stock fell more than 8 percent this week after the company reported a fiscal first-quarter profit miss and a 2.2 percent U.S. retail sales decline. The stock has fallen more than 25 percent over the last year while the S&P 500 index has gained 26 percent over that period.

Opportunities

- The electronic sports industry is likely to grow significantly in coming years and stocks in the sector are poised to benefit, according to DBS Group Holdings. Live streaming will help lead to “exponential growth,” with companies such as Activision Blizzard, Nintendo and Tencent Holdings set to benefit, according to the bank’s quarterly CIO outlook report.

- Chip stocks are expected to gain a further 50 percent or more over the next four to five quarters, according to investment bank Liberum, anticipating that upside in 2020 will be mainly driven by earnings upgrades.

- Synnex shares jumped to their highest level on record after reporting better-than-expected fourth-quarter earnings, better earnings per share (EPS) guidance and announcing plans to separate into two publicly traded companies. Citigroup analysts reiterated their buy rating while raising the price target to $175 from $140.

Threats

- Urban Outfitters sank by the most in seven weeks after it reported a disappointing holiday season. The “weaker than anticipated margins came as a surprise with the consensus view being that the company was the ‘best house on a bad block’ this holiday,” Citigroup’s analysts wrote in a note.

- Fourteen months after Canada Goose Holdings CEO said the company was rising like a “rocket ship,” a growing number of investors have found the stock showing unimpressive performance. Shares have fallen after each of the past four earnings reports, and the stock lost 17 percent last year.

- Superdry shares plunged as much as 24 percent, the most in more than a year, after the U.K. clothing seller cut its pretax profit forecast. Superdry’s move to full-price sales after Black Friday was healthier for the brand long term, but led to sales falling 16 percent in the last 10 weeks as rivals offered discounts to lure customers, according to Jefferies.

The Economy and Bond Market

Strengths

- A rebound in sales and production lifted a gauge of U.S. service activity to a four-month high in December, indicating the broader economy remains stable in the face of further deterioration in manufacturing. The ISM non-manufacturing index climbed to 55, exceeding the median projection of 53.9 from a month earlier, according to data issued Tuesday.

- The latest figures on U.S. unemployment show the rate held steady at 3.5 percent in December – a 50-year low.

- The number of Americans who applied for unemployment benefits fell in early 2020 for the fourth week in a row, putting new jobless claims back near the lowest level in about 50 years. Initial jobless claims declined by 9,000 to 214,000 in the seven days ended January 4.

Weaknesses

- The U.S. jobs market ended 2019 on a sour note with December’s payroll growth missing expectations. Nonfarm payrolls increased by just 145,000 while economists surveyed by Dow Jones had been looking for 160,000.

- U.S. wage growth missed expectations in December, with average hourly earnings rising by just 2.9 percent, below the 3.1 percent projection. December marked the first time that wage gains were below 3 percent on a year-over-year basis since July 2018.

- New orders for real durable goods for November were at the lowest level of orders since January 2018. Orders in November 2019 were down 7.6 percent from one year ago, marking the fastest rate of month-over-month contraction since July 2016. This was also the fourth month in a row of contraction and the ninth month of contraction out of the last 10. Three of the last four months have contracted faster than 6.0 percent.

Opportunities

- The first major U.S. release next week is on Tuesday with the consumer price index (CPI) for December. The headline rate of CPI is expected to have edged up from 2.1 percent to 2.3 percent year-over-year in December, which could reflect some economic strengthening, while the core rate is forecast to have held steady at 2.3 percent.

- The highlight on Wednesday will be U.S. retail sales figures for December. Retail sales are expected to have increased by 0.4 percent over the month, accelerating slightly from the prior 0.2 percent rate. If confirmed, it would signal consumers finished the year on a confident note.

- Rounding out the week on Friday is the preliminary reading of the University of Michigan’s consumer sentiment index for January. Consumer sentiment has remained upbeat amidst geopolitical tensions and has been a driver of strength for the economy.

Threats

- It will be somewhat of a muted week in the Eurozone next week with the only data capable of stirring the markets being the initial full year GDP estimate for Germany. Despite some signs of stabilization in growth across the euro area, the threat of a German recession has not completely faded, and Europe’s largest economy may still take a turn for the worse if President Trump decides to impose tariffs on European imports in the coming months.

- U.S. manufacturing updates next week will come from the New York Fed’s Empire State manufacturing index on Wednesday and the Philadelphia Fed will publish its manufacturing gauge on Thursday. Investors will be bracing for these data releases given the continued weakness in the U.S. manufacturing sector.

- One of the Federal Reserve Board’s top economists said a U.S. recession could drive both short- and longer-term Treasury yields close to zero, limiting the tools the central bank has to aid the economy. Michael Kiley, a deputy director in the Fed Board’s financial stability unit, said even a moderate recession in the U.S. “may result in near-zero interest rates at long maturities, bringing U.S. experience closer to that seen in Europe and Japan.” Kiley pointed out that U.S. rates are already low and “decline notably” for several years after a recession.

Energy and Natural Resources Market

Strengths

- The best performing major commodity for the week was sugar, which gained 5.71 on concerns that a global deficit will get worse as almost every major producing region is suffering a down season. Orders for LME aluminum rose 21 percent on Thursday, hitting a 10-month high, and halting the metal’s weekly decline. Prices reversed early weekly losses on the London Metal Exchange after orders jumped to 610,750 tons, which reduced the amount of available inventory to the lowest in two months. The metal did eventually end the week down just 0.98 percent. After tensions eased between the U.S. and Iran mid-week, nickel led all base metals higher.

- Nucor, the largest U.S. steelmaker, raised prices for a fifth time since October, adding to signs of a rebound in the industry, reports Bloomberg News. Nucor said in a letter to clients that the cost for new orders of hot-rolled, cold-rolled and galvanized sheet will increase by $40 a short ton effective immediately. The world’s largest steel producer, ArcelorMittal, also raised prices.

- Over the past few weeks, Norway has seen three times more snow and rain than normal, which is a huge positive for the region’s power reservoirs. Bloomberg’s Lars Paulsson reports that Norway has Europe’s biggest battery, in the form of huge dams, that provide electricity free from carbon emissions and is as dependable as a traditional fossil fuel plant. Nordic power prices are at the lowest since 2017.

Weaknesses

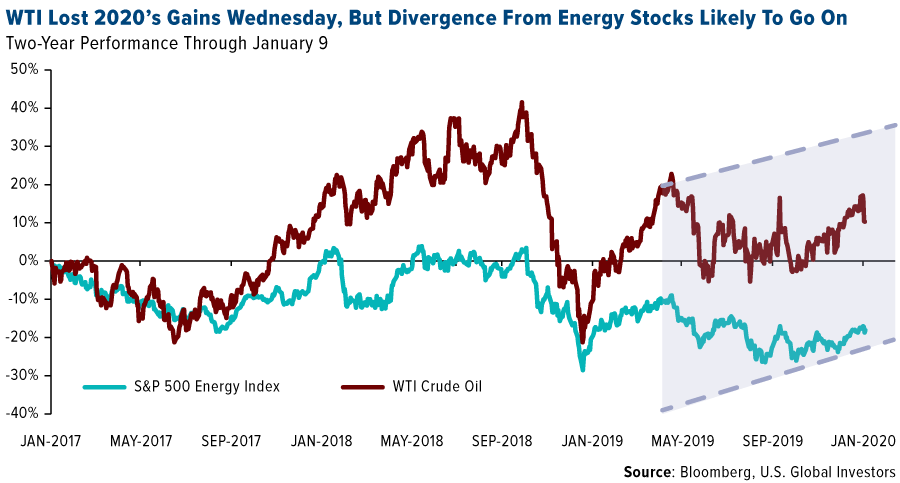

- The worst performing major commodity for the week was oil, which fell 6.23 percent. Oil had a wild ride this week, soaring to an eight-month high above $65 a barrel then falling back below $60. The fuel spiked as U.S.-Iran tensions escalated early in the week then fell after the prospect of immediate confrontation between the two powers abated. The collapsing oil price knocked down drilling stocks so fast that U.S. regulations aiming at tampering volatility kicked in, reports Bloomberg. The 2010 SEC measure begins when a stock plunges 10 percent and only allows short selling at a price above the best bid. Bloomberg Intelligence’s Mike McGlone says “while the U.S. shifting to a net exporter will limit WTI advances, something more powerfully negative is at hand in energy equity prices.” Energy stocks have diverged from the oil price and the trend could continue due to geopolitical risks.

- Lithium giant Livent Corp. fell as much as 14 percent on Wednesday after it cut revenue and profit estimates, reports Bloomberg. The company said it is reviewing expansion plans as lower prices of lithium, a key battery metal, persist. Livent lost more than a third of its value in 2019. CEO Paul Graves said “current market conditions remain challenging, with lower prices seen across all regions and most end markets.”

- Iron heavy hitter Fortescue was cut to underperform at Bank of America this week amid an expected drop in metal prices. Bank analysts wrote that the company offers sector-leading free cash flow and dividend yields and that it is “as good as it gets”. The bank predicts shares will likely fall as iron ore prices decline in 2020. Bloomberg reports that Vale, Rio Tinto and BHP are all expected to boost iron supply this year, while China steel demand growth is seen moderating.

Opportunities

- Anglo American Plc is in advanced talks with Sirius Minerals Plc to buy a U.K. potash mine that was running out of money. Bloomberg reports that the deal is likely to secure 1,200 jobs and save the development of a mine in one of the U.K.’s most economically deprived areas. Sirius shares traded 32 percent higher in London on Wednesday.

- Royal Dutch Shell Plc, which already owns 200 gasoline stations in 12 states in Mexico, is looking to grow its share of the retail fuel market in the country to as much as 15 percent from 1 percent now, reports Bloomberg. Even as regulatory changes have made it harder for foreign companies to operate in the country, Shell continues to push forward. Murray Fonesca, Shell’s downstream director for Mexico, said in an interview that “we’re planning to invest more heavily in 2020 than we did in 2019” and that if “conditions stay the same, Mexico will become a heartland for Shell.”

- According to a report from Rhodium Group, across the U.S. economy, emissions that cause climate change fell an estimated 2 percent and coal consumption fell 18 percent last year. JetBlue Airways Corp. announced that it will be the first large U.S. airline to become carbon neutral as it will begin using sustainable aviation fuel on select flights. Saudi Arabia has renewed its push for renewable energy, as the energy ministry is seeking bidders for solar projects. Bloomberg reports that shares of Korean battery makers rose for a second day on Thursday after President Moon Jae-in said that the nation’s battery industry will grow bigger than its memory chip industry in 2025. Jae-in added that Korea has a plan to increase the number of electric vehicles to 33 percent of all new cars by 2030.

Threats

- Copper producers in Zambia cite electricity supply as the biggest risk in 2020. Bloomberg reports that a longstanding agreement between state-owned Zesco Ltd. to sell power to Copperbelt Energy Corp., which then distributes it to miners, will come to an end on March 31 and the Zambian government does not plan on renewing it. The mining industry accounts for more than half of the country’s electricity consumption and is concerned about uncertainty on how they will continue to receive power.

- Borden Dairy Co. filed for bankruptcy this week, just two months after America’s biggest milk producer Dean Foods filed for Chapter 11 protection. The price of raw milk is up 27 percent in the last 12 months, however, retail prices and margins have been dropping. Dairy producers have been hurt by a reduced consumption of milk and increase in milk alternatives such as soy, rice and nut milk, reports Bloomberg News.

- Australia’s wildfires continue to burn and the smoke is spreading halfway across the world. According to the National Oceanic and Atmospheric Administration, the bushfire smoke has drifted across to South America and spread out over Buenos Aires. Bloomberg reports that more than 25 million acres have burned, which is about the size of the State of Indiana. Record heat has contributed to the deadly fires and authorities warn that there is no end in near sight.

Emerging Europe

Strengths

- Turkey was the best performing country this week, gaining 4.4 percent. Easing geopolitical tension in the Middle East pushed stocks trading on the Istanbul exchange higher. Erdogan offered to help defuse the conflict between the U.S. and Iran. Moreover, the presidents of Turkey and Russia called for ceasefire in Libya.

- The Turkish lira and Russian ruble were the best performing currencies this week, gaining 1.6 percent. Russian and Turkish leaders inaugurated TurkStream pipeline in Istanbul on Wednesday, deepening energy ties. TurkStream enabled Russia to bypass Ukraine to sell gas to Europe, while bolstering Turkey as a major energy transport hub.

- Industrials was the best performing sector among eastern European markets this week.

Weaknesses

- Hungary was the worst performing country this week, losing 1.7 percent. MOL Hungarian Oil and Gas Company and OTP Bank were the biggest negative contributors to Budapest underperformance. MOL’s ratings were cut to reduce at HSBC. OTP Bank corrected over the past five days after gaining 20 percent in the last quarter of 2019.

- The Hungarian forint was the worst performing currency in the region this year, losing 1.6 percent. The Central Bank of Hungary kept a dovish stance for years, and most likely, there will be no change to its monetary policy in the short term. The bank’s rate remains at a record low of 90 basis points since mid-2016.

- Health care was the worst performing sector among eastern European markets this week.

Opportunities

- The International Monetary Fund (IMF), which helped fund Greece’s bailout during its crisis, announced it would be shutting down its office in Athens, as Greece came out of strict supervision. The country exited the last three bailouts in August 2018, but the euro zone and the IMF, which together lent Athens 250 billion euros ($278.60 billion) during the decade-long debt crisis, are still monitoring its fiscal progress.

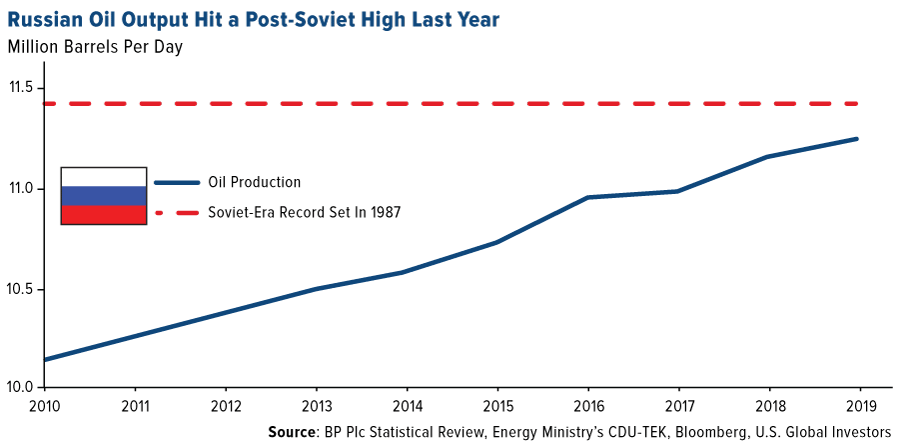

- Bloomberg reported that in 2019 Russia’s crude oil and condensate output hit a post-Soviet high even as the country curbed production under an agreement with OPEC. Russia has agreed to deepen its reduction by 70,000 barrels a day to about 300,000 a day in the first quarter. However, its baseline and monthly production calculations will exclude a type of light oil called condensate, potentially making it easier to hit its cut targets. If Russia decides to end the deal with OPEC, it has capacity to produce about 500,000 barrels a day more, which could pave the way for a new output record in 2020.

- The President of the Bank of England (BOE) Mark Carney, in his speech on Thursday, made dovish comments, suggesting interest rate cuts within the next few months. Money markets are now pricing in an almost 60 percent probability of a quarter-point cut in May compared with less than 30 percent on Wednesday. The BOE was one of the few major central banks that did not join the global monetary policy easing in 2019. The next policymaker’s decision will be announced January 30.

Threats

- Geopolitical tensions increased after the U.S. killed Iranian Major General Qasem Soleimani among others in Baghdad. In retaliation, Iran attacked U.S. military bases in Iraq. There were no causalities reported, and President Trump decided not to strike back. However, the question remains if the Boeing 737 plane caring 167 passengers crashed in Iran shortly after take-off from Tehran (killing all on board just a few hours after Iran fired missiles toward U.S. bases in Iraq), was due to the plane’s technical problems or not?

- Wood and Company, in its EME Macro Strategy report titled “2020 – follow the money,” warned that the conditions are not in place for a V-shaped recovery in Turkey. The Central Bank of Turkey will most likely continue to cut the policy rate aggressively, but domestic consumption most likely will not rebound strongly, which historically has been the main driver of economic growth. The lira could depreciate further against the dollar.

- European legal experts traveled to Poland to review the judicial reform. Law & Justice proposed a new law that would give politicians the power to fire or fine judges, a law that the European Union has urged Polish authorities to suspend. The bill still needs approval from the Senate, where the opposition has a slim majority. However, more clashes between Poland and Brussels are expected.

China Region

Strengths

- In a relatively quiet, mixed week for the region across the first full week of trading in 2020, Korea’s KOSPI was the lone finisher up over 1 percent on the week, rising 1.38 percent in that time. In other news, on Saturday, Taiwan goes to the polls for elections, with Taiwanese President Tsai Ing-wen expected to claim an easy victory.

- Information technology was the top performing Hang Seng Composite Index sector in Hong Kong over this first full week of trading of 2020.

- Both exports and imports came in higher than expected in Taiwan. Imports for the December period versus a year ago were up 13.9 percent, much higher than expectations for only a 5.0 percent growth rate, while exports clocked in at 4.0 percent, ahead of analysts’ consensus for a 3.1 percent reading.

Weaknesses

- Somewhat similarly to Korea on the upside, Malaysia’s FTSE Bursa Malaysia Kuala Lumpur Composite was the lone finisher down more than 1 percent in the red, dropping 1.24 percent on the week.

- Materials was the poorest performing HSCI sector for this first full week of 2020, dropping by 2.40 percent.

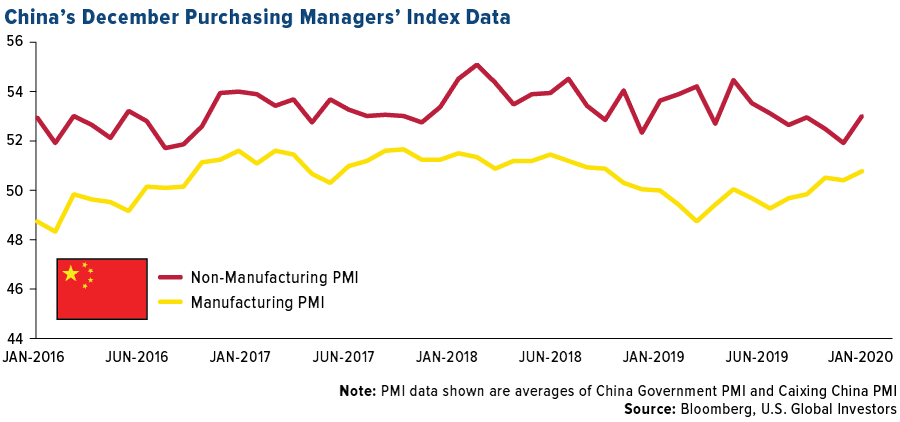

- While all of China’s official and Caixin readings on PMIs did clock in at above-50 expansionary levels, only the official Manufacturing PMI came in better than expectations, and that only slightly so, with a 50.2 reading versus consensus for a 50.1 print. Official Non-manufacturing PMI came in at 53.5, shy of expectations for a 54.2 print; the Caixin China Manufacturing PMI was a 51.5, just shy of consensus for a 51.6 reading, and the Caixin Services PMI came in at a 52.5 level, also short of expectations, this time for a 53.2 print.

Oppurtunites

- Bloomberg News reported this week that investors rung in the New Year by pouring money into emerging market stocks and bonds exchange traded funds, marking the thirteenth straight week of inflows.

- The macro world of late seems much more focused on the geopolitical sphere and Iran than much else, but perhaps therein lies quiet opportunity: in the background, next week should usher in the signing of the U.S.-China Phase One agreement, and in addition to the lack any immediate threat of U.S.-China trade war escalation, the Chinese authorities remain stimulative and supportive heading into the Lunar New Year celebrations that will mark the end of the month across the region in general and China in particular. Moreover, Hong Kong is now ready to spend "boldly," Bloomberg News reports HK’s Financial Secretary Paul Chan as saying, to shore up an economy ravaged by months of violent protests. “Spending on infrastructure and public services will be maintained even as additional stimulus is added,” the article noted.

- While Indonesia’s PMI lagged behind most of its regional peers in contractionary territory at 49.5 on the Markit Indonesia Manufacturing PMI, the country’s tourism arrivals through the month of November is up by 3.6 percent year-over-year.

Threats

- The European Union released a report blasting China over thefts of intellectual property and technology, noting that the country’s technology transfer practices are still deeply problematic, as the United States has argued vehemently throughout the recent trade war. Bloomberg highlights that the EU report describes China as responsible for “the lion’s share of counterfeit and pirated goods arriving in the EU.”

- Thailand’s surplus with the United States has now passed some $20 billion in the latest readings (trailing twelve months through November of 2019), which may raise the odds, Bloomberg News observes, of the country being added to the U.S. Treasury’s watch list of currency manipulators. Treasury seeks to limit bilateral trade deficits to no more than $20 billion. The Thai baht gained almost 6 percent against the USD over the last year, and the United States remains Thailand’s third-largest trading partner. In an interview this week, Thailand’s central bank Governor Veerathhai Santiprabhob stated that the bank will make moves to ease restrictions on capital outflows over the coming months; the currency did fall following his comments (“[W]e think the baht has appreciated too much,” Santiprabhob said on Bloomberg TV).

- While there are some bright spots—Tesla delivered its first cars made in China this week, for example—overall car sales in China fell an annual 3.6 percent last month to 2.17 million, capping a second straight annual decline, Bloomberg reported. According to the China Passenger Car Association, the overall drop for all of 2019 was 7.5 percent.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended January 10 was Tap, up 336.68 percent.

- Bitcoin’s price hit a new record for 2020 at the start of the week, reports CoinDesk. The cryptocurrency moved as high as $8,438 before pulling back slightly. According to the article, the upward rise comes following Iranian missiles striking the U.S. and coalition bases in Iraq, causing traders to reallocate capital into safe-haven assets like gold and oil away from riskier assets.

- The mining power of bitcoin has reached fresh, all-time highs, reports CoinDesk. When looking at a seven-day average, the article explains, the hash rate has risen from around 93 exa-hashes per second (EH/s) on December 30 to over 106 EH/s on January 5. The record high reached this week comes amid rising prices and anticipation of the miner reward halving later this year.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended January 10 was Omnitude, down 80.74 percent.

- Cryptocurrency exchanges experienced more hacks in 2019 than in 2018, reports CoinTelegraph, when only nine exchanges fell victim to security breaches. Last year, 12 major crypto exchange hacks occurred and of these, 11 resulted in the theft of cryptocurrency while only one involved stolen customer data.

- Lawyers that represent the messenger giant Telegram are saying that proving data-privacy compliance could take months, reads one CoinTelegraph headline. To ensure Telegram’s compliance with all foreign data privacy laws, the U.S. Securities and Exchange Commission has requested these records in order to analyze approximately 4,600 transactions, involving around 770 entities and individuals. Telegram says this could take five to seven weeks to prepare.

Opportunities

- The world’s largest bitcoin mine, located in the industry’s new “hotspot” Rockdale, Texas, has landed customers including SBI Holdings and Japanese internet-service provider GMO Internet Inc., writes BNN Bloomberg. The companies have in principle agreed with Northern Bitcoin AG subsidiary Whinstone Inc. to process the cryptocurrency transactions at the German company’s facility within the coming months.

- Not only has the Iran crisis sent the bitcoin price higher this week, a new internet search trend has emerged. According to data from Google Trends, and reported by CoinTelegraph, the search term “Bitcoin Iran” surged 4,450 percent in the seven days to January 8. Topping the list for both terms’ most frequent country of origin was Nigeria, followed by Canada, Singapore and the United States.

- As reported by a domestic news outlet in China, the country’s central bank has completed the top-layer design and joint testing of its soon-to-be released central bank digital currency (CBDC). The latest developments were set forth in a dedicated article by the People’s Bank of China (PBoC), which also highlighted plans to improve cybersecurity of the financial industry network and formulates rules for the accreditation of critical information infrastructure.

Threats

- Law enforcement data requests rose by nearly 50 percent, according to crypto exchange Kraken. Apparently, the cost of responding to requests for user data is rising year on year and in a Tweet on Tuesday Kraken indicated receiving 710 requests in total last year – that’s a 49 percent rise from 2018.

- A strict new regulatory regime is dawning upon European firms handling cryptocurrency, reads one CoinDesk article this week. The European Union’s 28-member nation-states have until today to adopt the Fifth Anti-Money Laundering Directive or AMLD5. According to the article, the new rules require crypto exchanges and custodial service providers to register with their local regulator, and demonstrate compliance with thoroughgoing know-your-customer and anti-money-laundering AML procedures. Not only that, these rules give “greater power and reach to financial intelligence units and law enforcement.”

- Following threats from angry investors, a popular South Korean cryptocurrency YouTube personality was assaulted in his home on Friday, reports CoinDesk Korea. Around 1:00 local time, Kyu-hoon “Spunky” Hwang was beaten in an elevator in his apartment. “It is judged to be a planned crime aimed at [Hwang’s] life,” said a community notice from CoinRunners.

Airline Sector

Strengths

- The U.S. Transportation Department released a proposal that would require airlines to offer lavatories accessible to disabled passengers on more aircraft. The plan would require airlines to ensure new, single-aisle jets with at least 125 seats to have accessible toilet seats and other features, reports Bloomberg. Current rules do not require single-aircraft to have accessible lavatories, even as those planes are increasingly used for long-haul flights.

- Australia’s Qantas Airways decided to use the Airbus A350-1000 over Boeing’s 777X for proposed ultra-long haul flights connecting Sydney with New York and London. Qantas plans to begin commercial services between 2022 and 2023, and had used the Boeing 787 Dreamliner for test flights of the 20 hour routes. Bloomberg reports that Airbus will fit an additional fuel tank on the A350 to give the aircraft the range to fly the routes with a full passenger load.

- Airlines for America (A4A) projected that 47.5 million passengers would fly globally on U.S. airlines over the 18-day winter holiday travel period from December 19 through January 5. The industry trade organization reports that an average of 2.6 million passengers would fly each day during the period, an increase of 3 percent from the same period a year ago.

Weaknesses

- Boeing announced that it would halt production of its 737 MAX plane in January as the troubled plane is yet to be approved to return to service. The manufacturer had been producing around 40 of the planes per month at its assembly plant in Washington, employing 12,000 workers. Boeing said that it will redirect workers to other projects. Since Boeing is a major contributor to the U.S. economy, chief economist at Wilmington Trust Luke Tilley predicts that stopping production for one quarter would cut 0.3 of a percentage point from quarterly annualized GDP growth. The Wall Street Journal reported that Boeing has a backlog of 4,545 MAX orders as of the end of November.

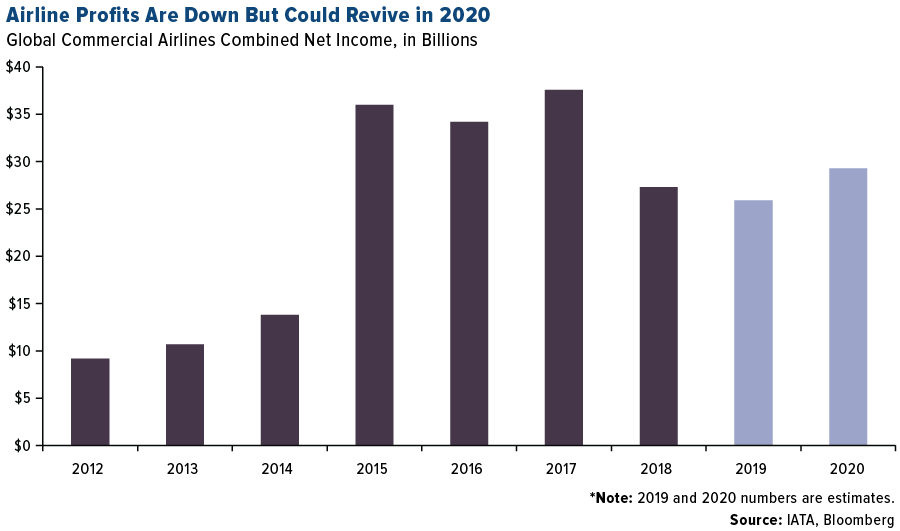

- The International Air Transport Association (IATA) lowered its annual 2019 profit estimate for the airline industry to $25.9 billion, which is $2.1 billion less than its prediction in June and almost $10 billion down from estimates a year ago. The organization stated that a main concern for 2020 is that the new 737 Max aircraft with return to service and expand capacity too fast. The IATA does, however, expect 2020 to fare better than 2019, with an estimate of $29.3 million in profits.

- An American Airlines mechanic pleaded guilty to attempted destruction of an aircraft for tampering with a flight-monitoring device on a jet in Miami, reports Bloomberg News. The mechanic said he was upset over stalled contract talks and court records show that his brother might have been involved with the Islamic State group, reports the Associated Press. Pilots got an error message in the cockpit and aborted takeoff after noticing the error in the device.

Oppurtunites

- FTSE Russell said that EasyJet PLC will be returning to the FTSE 100 Index just six months after being removed. The budget airline suffered in early 2019 on concerns that Brexit would hurt demand for air travel between the U.K. and Europe. Bloomberg reports that EasyJet then recovered in October when the carrier reported earnings would hit the top end of guidance.

- After 20 years, Delta Air Lines is selling its struggling private jet charter business to Wheels Up Partners. Delta CEO Ed Bastain said in an interview that the luxury charter business had been marginally profitable and didn’t grow as hoped. However, Delta is confident that Wheels Up will be able to provide greater marketing power and focus. Wheels Up is an on-demand aviation company with 6,000 members, according to Bloomberg.

- According to people familiar with the matter, the Hinduja Group is likely to bid for the grounded carrier Jet Airways India. Bloomberg reports the group plans to submit an expression of interest by January 15. Jet Airways, which was once India’s largest by market value, saw its stock fall almost 90 percent in 2019 as it fell victim to a price war initiated by budget carriers and defaulted to banks.

Threats

- The air travel industry continues to come under fire for being a big global polluter. The European Green Deal was unveiled by the European Commission, which aims to fight climate change in many ways, including a fuel tax. According to a July report from the commission, the new taxes could cost airlines 14.4 billion euros per year, more than double their currently yearly taxes in the bloc. Airlines have pushed back against a fuel tax, saying that investment in sustainable fuels and electric planes would be more effective in reducing carbon emissions, reports Bloomberg News.

- Hong Kong’s air travel industry has been hurt further by continued protests in the city that have deterred visitors. Cathay Pacific Airways reported a fourth straight monthly drop in passenger traffic and may have to cut as many as 1,000 jobs. Bloomberg reports that the Hong Kong Airport Authority said it seized seven planes from Hong Kong Airlines for failing to make certain payments.

- South Africa’s government is placing South African Airways (SAA) under a local form of bankruptcy protection to try and prevent the total collapse of the airline, reports Bloomberg. The state-owned carrier will receive around $274 million in funding for radical restructuring. SAA last turned a profit in 2011 and has received billions in bailouts since 1994.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| 10-Yr Treasury Bond | 1.82 | +0.03 | +1.68% |

| Oil Futures | 59.18 | -3.87 | -6.14% |

| Hang Seng Composite Index | 3,908.72 | +34.05 | +0.88% |

| S&P Basic Materials | 373.89 | -0.99 | -0.26% |

| Korean KOSPI Index | 2,206.39 | +29.93 | +1.38% |

| S&P Energy | 453.87 | -4.90 | -1.07% |

| Nasdaq | 9,178.86 | +158.09 | +1.75% |

| DJIA | 28,823.77 | +188.89 | +0.66% |

| Russell 2000 | 1,657.17 | -3.70 | -0.22% |

| S&P 500 | 3,265.79 | +30.94 | +0.96% |

| Gold Futures | 1,561.40 | +9.00 | +0.58% |

| XAU | 102.25 | -3.16 | -3.00% |

| S&P/TSX VENTURE COMP IDX | 582.63 | -4.81 | -0.82% |

| S&P/TSX Global Gold Index | 254.74 | -4.43 | -1.71% |

| Natural Gas Futures | 2.21 | +0.08 | +3.57% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Korean KOSPI Index | 2,206.39 | +100.77 | +4.79% |

| 10-Yr Treasury Bond | 1.82 | +0.03 | +1.45% |

| Gold Futures | 1,561.40 | +86.40 | +5.86% |

| S&P Basic Materials | 373.89 | -1.38 | -0.37% |

| S&P 500 | 3,265.79 | +124.16 | +3.95% |

| DJIA | 28,823.77 | +912.47 | +3.27% |

| Nasdaq | 9,178.86 | +524.81 | +6.06% |

| Oil Futures | 59.18 | +0.42 | +0.71% |

| Hang Seng Composite Index | 3,908.72 | +280.65 | +7.74% |

| S&P/TSX Global Gold Index | 254.74 | +3.86 | +1.54% |

| XAU | 102.25 | +2.69 | +2.70% |

| Russell 2000 | 1,657.17 | +25.25 | +1.55% |

| S&P Energy | 453.87 | +17.06 | +3.91% |

| S&P/TSX VENTURE COMP IDX | 582.63 | +46.31 | +8.63% |

| Natural Gas Futures | 2.21 | -0.04 | -1.65% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| XAU | 102.25 | +10.12 | +10.98% |

| S&P/TSX Global Gold Index | 254.74 | +6.53 | +2.63% |

| Gold Futures | 1,561.40 | +53.70 | +3.56% |

| DJIA | 28,823.77 | +2,327.10 | +8.78% |

| S&P 500 | 3,265.79 | +327.66 | +11.15% |

| Nasdaq | 9,178.86 | +1,228.08 | +15.45% |

| Korean KOSPI Index | 2,206.39 | +178.24 | +8.79% |

| Natural Gas Futures | 2.21 | -0.01 | -0.54% |

| S&P Basic Materials | 373.89 | +21.17 | +6.00% |

| Russell 2000 | 1,657.17 | +171.81 | +11.57% |

| Oil Futures | 59.18 | +5.63 | +10.51% |

| Hang Seng Composite Index | 3,908.72 | +420.99 | +12.07% |

| S&P/TSX VENTURE COMP IDX | 582.63 | +40.03 | +7.38% |

| S&P Energy | 453.87 | +31.76 | +7.52% |

| 10-Yr Treasury Bond | 1.82 | +0.15 | +8.92% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (09/30/2019):

Nucor Corp

Fortescue Metals Group Ltd

BHP Group Ltd

Anglo American Plc

Royal Dutch Shell Plc

JetBlue Airways Corp

MOL Hungarian Oil and Gas Company

OTP Bank Nyrt

Newmont Goldcorp Corp

Centamin PLC

Apache Corp.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The FTSE Bursa Malaysia Index Series is a broad range of real-time indices, which cover all eligible companies listed on the Bursa Malaysia Main and ACE Markets. The indices are designed to measure the performance of the major capital segments of the Malaysian market, dividing it into large, mid, small cap, fledgling and Shariah-compliant series, giving market participants a wide selection and the flexibility to measure, invest and create products in these distinct segments. The Bloomberg Barclays US Aggregate Bond Index, or the Agg, is a broad base, market capitalization-weighted bond market index representing intermediate term investment grade bonds traded in the United States. The Bloomberg Barclays US Corporate Bond Index measures the investment grade, fixed-rate, taxable corporate bond market. It includes USD-denominated securities publicly issued by US and non-US industrial, utility and financial issuers. The University of Michigan Confidence Index is a survey of consumer confidence conducted by the University of Michigan. The report, released on the tenth of each month, gives a snapshot of whether or not consumers are willing to spend money. The New York Empire State Manufacturing Survey is conducted by the Federal Reserve Bank of New York. It is based on survey responses on the first day of each month to an unchanged pool of about 200 top manufacturing executives. The index summarizes general business conditions in New York State. The Manufacturing Business Outlook Survey, conducted by the Federal Reserve Bank of Philadelphia, is a monthly survey of manufacturers in the Third Federal Reserve District. Participants indicate the direction of change in overall business activity and in the various measures of activity at their plants: employment, working hours, new and unfilled orders, shipments, inventories, delivery times, prices paid, and prices received. The U.S. Dollar Index is an index of the value of the United States dollar relative to a basket of foreign currencies, often referred to as a basket of U.S. trade partners’ currencies. The Index goes up when the U.S. dollar gains "strength" when compared to other currencies. The trade-weighted US dollar index, also known as the broad index, is a measure of the value of the United States dollar relative to other world currencies. It is a trade weighted index that improves on the older U.S. Dollar Index by using more currencies and the updating the weights yearly.