If Inflation Is the Trick, Gold Is the Treat

Date Posted: October 30, 2020

Read time: 48 min

Want to hear something really scary? Inflation, the scourge of the modern economy, may be running much faster than we're led to believe.

Want to hear something really scary? Inflation, the scourge of the modern economy, may be running much faster than we’re led to believe.

I’ll use consumer spending on Halloween as an example of what I mean.

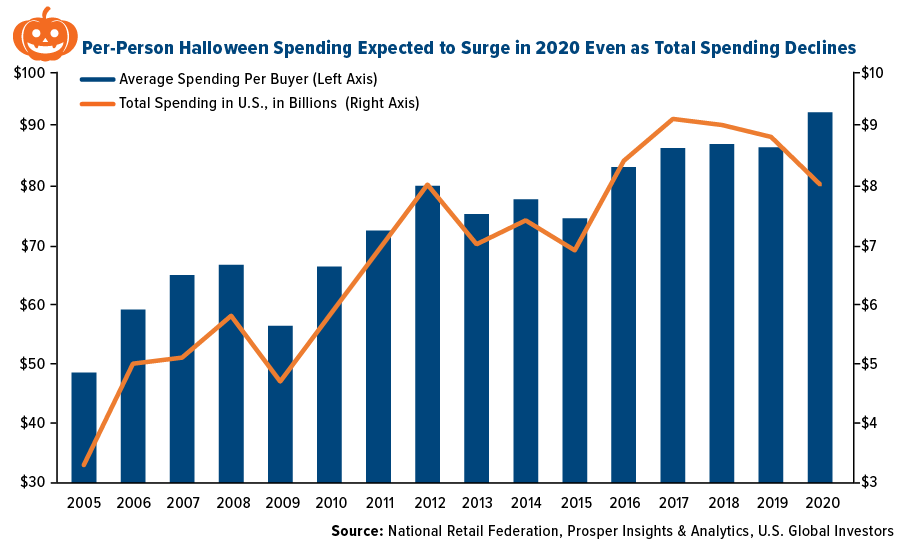

Total Halloween spending has fallen for the past three years and is projected to fall yet again this season, to $8 billion from $8.8 billion last year, according to recent data from the National Retail Federation (NRF).

No surprise there. With many people still avoiding large gatherings due to the pandemic, and health officials calling trick-or-treating a “high-risk activity,” less is going to be spent on candy, costumes, party decorations and other Halloween-related items.

Indeed, spending on costumes is forecast to plunge a not insignificant $600 million compared to last year, from $3.2 billion to $2.6 billion.

Given this, you might suppose that on a per-person basis, Halloween spending would also be down. And yet that’s not the case, according to the NRF’s survey. Average spending per consumer is expected to increase almost 7 percent, from $86.28 to $92.12.

So what’s going on here?

There may be a number of possible explanations for this phenomenon, but I believe the most convincing is also the simplest: Inflation.

And as I’ve said before, the real inflation may be much higher than the official consumer price index (CPI) issued monthly by the Bureau of Labor Statistics (BLS).

Earlier this month, the BLS reported that consumer prices were up only 1.4 percent in September compared to the same time last year. If we remove volatile food and energy prices, they were up slightly more, at 1.7 percent.

How can this be, when consumers are spending 7 percent more on candy and costumes this year, despite total Halloween spending declining?

The truth is that the CPI has undergone several changes in methodology over the years. At one time, it was a genuine cost of goods index (COGI). Today, however, it’s more of a cost of living index (COLI). So when you see that inflation is up 1.4 percent year-over-year, you can be sure it’s actually higher—potentially much higher.

How much higher? Economist John Williams, who runs the popular website ShadowStats.com, uses the 1980 methodology for measuring inflation. According to this gauge, consumer prices are up closer to 9 percent than 1 percent.

The implication, of course, is that inflation could be eating your lunch faster than you realize. And that’s truly scary, whether you’re still in your wealth building years or retirement.

Positioning Your Portfolio for Treasury Secretary Elizabeth Warren

There’s reason to believe that the rate of inflation could get a boost next year, particularly if we see additional multi-trillion-dollar stimulus packages. I’ll discuss the election more in-depth below, but I’ll say upfront that it’s being reported that Massachusetts senator Elizabeth Warren is seeking an appointment as Treasury secretary should Joe Biden win on Tuesday.

|

|

This is the same Elizabeth Warren who, while still a presidential candidate, said her Medicare-for-all health care plan would cost a staggering $52 trillion.

I’ve written before about modern monetary theory (MMT), the controversial economic thought that says governments with complete control over their own currencies can spend as freely as it wants. To a proponent of MMT, a $52 trillion price tag means nothing. Just print more money.

Currently the system is just that—a theory—but with the possibility of a Treasury Secretary Warren, MMT may become a reality sooner than we expected.

That said, get ready for unrestricted money printing—and, as a result, hyperinflation.

Last week, I shared with you Goldman Sachs’ forecast of higher inflation next year. The investment bank recommends commodities, raw materials and other hard assets, which would benefit in a high-inflation environment.

Many big-name money managers are urging investors get exposure to gold. Speaking at the Robin Hood Investors Conference this week, billionaire family office manager Stanley Druckenmiller said he believed a “blue wave” would hurt equities long-term and that bond yields and gold prices would rise.

Also this week, I had the pleasure of co-hosting a webcast with my friend Kevin O’Leary, “Mr. Wonderful.” Kevin said he was maintaining a 5 percent weighting in gold, split between physical bullion and shares of SPDR Gold Shares (GLD). Gold, he said, is “all about hedging against inflation.”

Missed the webcast? Email me at info@usfunds.com to get a copy of the replay!

Gold Investment at Record Highs

The yellow metal’s traditional haven status has definitely strengthened this year. The World Gold Council’s (WGC) summary of the third quarter shows that total holdings in gold-backed ETFs hit a record high of 3,880 tonnes, having added 272.5 tonnes in the three months ended September 30.

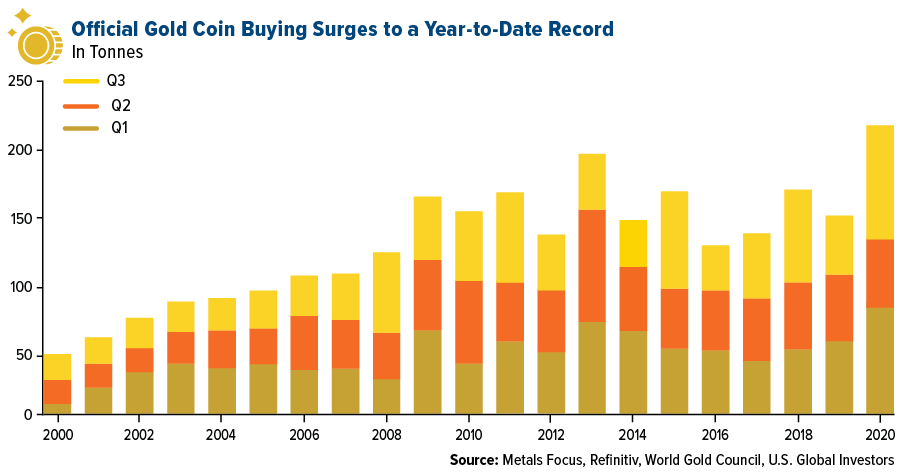

Physical gold investment also hit a new all-time high. Gold bar and coin purchases increased an incredible 49 percent year-over-year through the end of the third quarter, reaching 222.1 tonnes. Largest volume increases were seen in Western markets, China and Turkey, the WGC says.

Final Comments Before the Election

Speaking of breaking records… As I write this, it’s being reported that a record 80 million Americans have participated in early voting. Here in my home state of Texas, more than 9 million people have voted early—which exceeds the total number of Texans who went to the polls in 2016.

What this suggests is that voters this cycle are galvanized like never before.

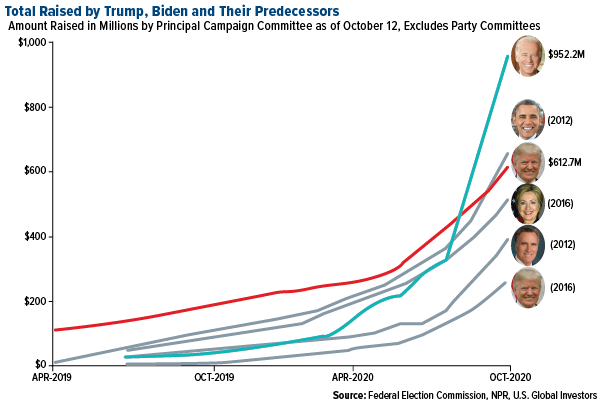

But we already knew that. For what it’s worth, Biden has raised more money than any other presidential candidate in U.S. history. As of October 12, his war chest stood at a head-spinning $952.2 million, which is one and a half times as much as President Donald Trump has raised over the same period.

The market also appears to be pointing toward a Biden victory. In August, I shared with you that when the market was up from July 31 to October 31, it historically favored the incumbent party. And when the market was down, it favored the challenger.

As I write this, the S&P 500 is down about 0.40 percent from July 31. What’s more, this week has been the worst for stocks since mid-March.

What’s working in Trump’s favor right now? Certainly stellar economic growth in the third quarter. GDP expanded at a record pace of 7.4 percent quarter-over-quarter and 33.1 percent annualized.

Also, manufacturing activity has been incredibly positive. The U.S. ISM Manufacturing PMI has been in expansionary mode for the past three months. And this week, the manufacturing index for the Federal Reserve Bank of Richmond shows factories growing at a record pace. The index hit 29.0 in October, the highest reading going back to 1992.

Nothing is set in stone, obviously, and there’s always the possibility that election results will be contested. However things turn out, be prepared for heightened volatility.

Have a happy, safe Halloween, and I’ll see you on the other side of the election!

Gold Market

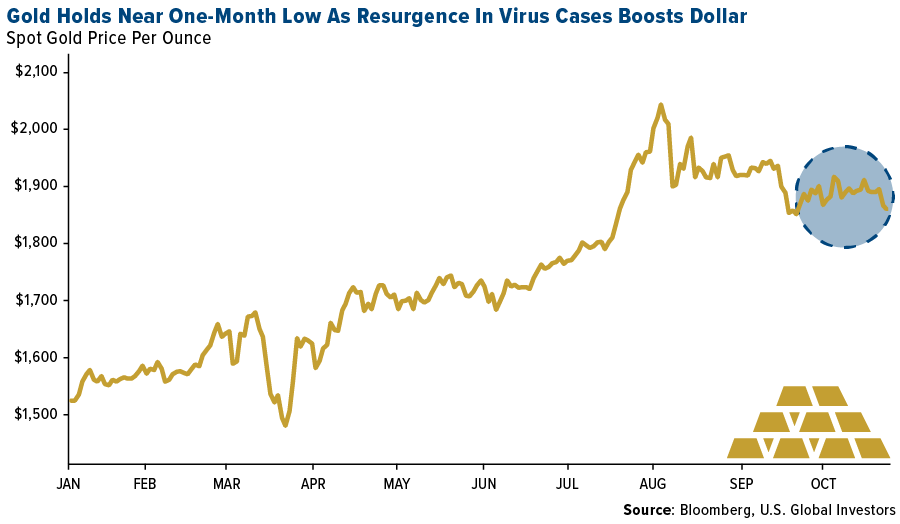

This week spot gold closed at $1878.81, up/down $23.24 per ounce, or 1.22 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 3.26 percent. The S&P/TSX Venture Index came in off 4.78 percent. The U.S. Trade-Weighted Dollar rose 1.21 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Oct-26 | New Homes Sales | 1025k | 959k | 994k |

| Cct-27 | Hong Kong Exports YoY | 0.2% | 9.1% | -2.3% |

| Oct-27 | Durable Goods Orders | 0.5% | 1.9% | 0.4% |

| Oct-27 | Conf. Board Consumer Confidence | 102.0 | 100.9 | 101.3 |

| Oct-29 | Initial Jobless Claims | 770k | 751k | 791k |

| Oct-29 | GDP Annualized QoQ | 32.0% | 33.1% | -31.4% |

| Oct-29 | ECB Main Refinancing Rate | 0.000% | 0.000% | 0.000% |

| Oct-29 | Germany CPI YoY | -0.3% | -0.2% | -0.2% |

| Oct-30 | Eurozone CPI Core YoY | 0.2% | 0.2% | 0.2% |

| Nov-1 | Caixin China PMI Mfg | 52.8 | — | 53.0 |

| Nov-2 | ISM Manufacturing | 55.6 | — | 55.4 |

| Nov-3 | Durable Goods Orders | — | — | 1.9% |

| Nov-4 | ADP Employment Change | 688k | — | 749k |

| Nov-5 | Initial Jobless Claims | 746k | — | 751k |

| Nov-5 | FOMC Rate Decision (Upper Bound) | 0.25% | — | 0.25% |

| Nov-6 | Change in Nonfarm Payrolls | 600k | — | 661k |

Strengths

- The best performing precious metal for the week was spot gold, but still off 1.22 percent. UBS raised its price forecast for palladium to $2,500 an ounce by the end of December, up from $2,400 an ounce. Analysts at the bank say palladium imports from China have hit a record high on strong domestic car sales and tighter emission standards. Spot prices are up nearly 22 percent year-to-date. Impala Platinum says demand for platinum-group metals has remained strong as its output rose in the third quarter, reports Bloomberg. Platinum output from the top producer totaled 408,000 ounces compared with 281,000 ounces the same quarter last year.

- Newmont reported all-time high revenue of $3.17 billion in the third quarter, thanks to record high gold prices. CEO Tom Palmer said, “I am confident that our world-class portfolio is best positioned to generate industry-leading value and returns for our shareholders.”

- Brixton Metals and High Power Exploration agreed to a joint venture of $44.5 million for exploration at the Hog Heaven silver-gold-copper-lead-zinc deposit in Montana. High Power is a privately-owned mineral exploration company led by Ivanhoe Mines founder Robert Friedland.

Weaknesses

- The worst performing precious metal for the week was palladium, down 7.59 percent on no specific news, although palladium has been the biggest gainer in prior weeks. Gold fell this week on worsening coronavirus outbreaks and a stronger U.S. dollar. The yellow metal is set for a third consecutive monthly drop – its longest run of declines since early 2019 – as investors continue to favor the U.S. dollar as a haven ahead of the presidential election.

- Gold-backed ETFs had two consecutive weekly outflows for the first time this year, reports Bloomberg, with 145,533 ounces in withdrawals. Analysts say investors could be taking profits before next week’s presidential election.

- Central banks were net sellers of gold for the first time since 2010 in the third quarter. Net sales totaled 12.1 tons, compared with purchases of 141.9 tons a year earlier, according to World Gold Council (WGC) data. Countries are taking advantage of record high gold prices to soften the blow from the economic impact of the coronavirus.

Opportunities

- Demand for gold in China, the world’s top consumer, could continue to rebound as the country recovers economically from the coronavirus. WGC data shows China’s jewelry demand fell 25 percent year-over-year in the third quarter but was up 31 percent from the prior quarter. Gold bar and coin demand rose 35 percent year-over-year in the quarter to 57.8 tons.

- Suki Cooper, precious metals analyst at Standard Chartered Bank, said in a report dated October 23 that the macro backdrop is favorable for gold, and there could be more upside if a “blue wave” occurs. “Even though polls continue to indicate a Biden victory and a Democratic Senate, gold price action has stalled, despite this election scenario potentially posing the greatest upside risk for the metal,” she said. Copper added that negative real rates, expectations for a weaker dollar and stimulus package are all bullish for the yellow metal.

- Jake Klein, executive chairman of Evolution Mining, says now is the best environment for gold in the past 15 years. In a Bloomberg TV interview, Klein said due to massive money printing “fiat currencies generally are on the decline against a hard asset like gold.” Klein notes gold has been trading range-bound and could see a pop after the U.S. presidential election.

Threats

- Gold jewelry demand in India usually picks up in the last three months of the year during festival and wedding seasons. This year due to coronavirus and weak economic growth, sales are likely to fall below last year’s 194 tons to the lowest quarterly numbers since 2008, according to Metals Focus. WGC data shows purchases of gold jewelry, coin and bars fell by half from a year earlier in the first nine months through September.

- The fate of oil drilling in the Arctic and the Pebble gold mine in Alaska hang in the balance of the presidential election, writes Bloomberg Green. Trump is pushing for development of the region while Biden has pledged to protect the natural resources. For the Pebble gold mine project in particular, the Trump administration has scrapped Obama administration pollution restrictions blocking the mine and Biden has promised to block the project if he wins, calling the area “no place for a mine.”

- Although the S&P 500 Index is trading near historic highs, all might not be well with the market. Bloomberg reports that through the third quarter, 25 companies in the index reported liabilities exceeding assets, the most in 25 years. This is more than double the high of 12 companies with negative equities during the Great Recession.

Index Summary

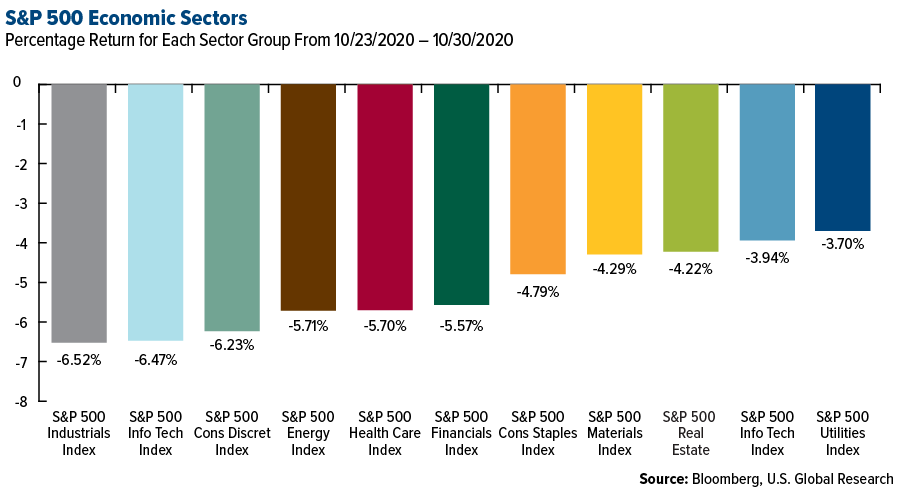

- The major market indices finished down this week. The Dow Jones Industrial Average lost 6.47 percent. The S&P 500 Stock Index fell 6.16 percent, while the Nasdaq Composite fell 5.51 percent. The Russell 2000 small capitalization index lost 6.67 percent this week.

- The Hang Seng Composite lost 1.83 percent this week; while Taiwan was down 2.73 percent and the KOSPI fell 3.97 percent.

- The 10-year Treasury bond yield rose 3 basis points to 0.873 percent.

Domestic Economy and Equities

Strengths

- Coming off the worst quarter in history, the U.S. economy grew at its fastest pace ever in the third quarter as a nation battered by an unprecedented pandemic started to put itself back together, the Commerce Department reported Thursday. Third-quarter gross domestic product, a measure of the total goods and services produced in the July-to-September period, expanded at a 33.1 percent annualized pace, according to the department’s initial estimate for the period. The gain came after a 31.4 percent plunge in the second quarter and was better than the 32 percent estimate from economists surveyed by Dow Jones. The previous post-World War II record was the 16.7 percent burst in the first quarter of 1950.

- U.S. households boosted spending for a fifth straight month, helping the economy climb further out of the deep hole created by the pandemic. The Commerce Department said personal-consumption expenditures rose 1.4 percent last month. Consumers have increased spending since the summer, although the pace of gains slowed into early fall. Personal income was up last 0.9 percent month, after a sharp decline in August, rising on higher pay and remaining pandemic-related aid.

- Coldwell Banker Richard Ellis (CBRE) Group was the best performing S&P 500 stock for the week, increasing 8.02 percent. Shares of CBRE jumped on Thursday after the company reported strong third-quarter earnings results. CBRE also said it was moving its headquarters from Los Angeles to Dallas, confirming recent rumors.

Weaknesses

- Consumer confidence waned in October, reflecting somewhat less optimism about the jobs market and the U.S. economy in the next six months amid another outbreak of coronavirus cases. The index of consumer confidence dipped to 100.3 this month from a pandemic high of 101.3 in September, the Conference Board said Tuesday. The decline was slightly bigger than Wall Street expected. The latest survey was largely compiled before the sharp upturn in coronavirus cases this month, suggesting confidence could suffer an even bigger swoon in November. Confidence is still far below pre-pandemic levels. The index stood at 132.6 before the viral outbreak in February.

- Sales of new U.S. single-family homes unexpectedly fell in September after four straight monthly increases. New home sales fell 3.5 percent to a seasonally adjusted annual rate of 959,000 units last month. August’s sales pace was revised down to 994,000 units from the previously reported 1.011 million units. Economists polled by Reuters had forecast new home sales, which account for about 12.8 percent of housing market sales, rising 2.8 percent to a rate of 1.025 million units.

- Dexcom was the worst performing S&P 500 stock for the week, falling 22.24 percent. The diabetes management company sank after quarterly results that were described as overall directionally positive, but with some caveats by analysts. Namely, there is concern about intensifying competition and pricing headwinds.

Opportunities

- Opinion polls still have Biden comfortably ahead of Trump, but the president has narrowed the gap, and investors are reducing their risk exposure ahead of the event in fear of another upset or a contested election. According to betting markets, the most likely outcome is still a landslide Democratic victory, with the probability that the Democrats take full control of government sitting at around 56 percent. This scenario is expected to deliver massive stimulus packages to heal the economy, so it could boost the wounded stock market but sink the U.S. dollar on concerns of large deficits.

- On the data front next week, the main event will be the jobs numbers for October. Nonfarm payrolls are expected to have risen by 850,000, pushing the unemployment rate down to 7.7 percent from 7.9 percent previously.

- The biggest credit-market selloff in five weeks going into the most volatile U.S. election in modern history is a buying opportunity for heavyweight investors BlackRock and DoubleLine Capital. “Risk assets will do well as earnings broadly exceed expectations, the U.S. election is resolved, and the second Covid-19 wave is less severe than feared,” said Jim Keenan, chief investment officer and global co-head of credit at BlackRock. The pandemic flare up, fund outflows, an oil slump and volatile equities pummeled credit markets in recent days, particularly the riskiest types of debt. In such environments, investors generally take a more cautious stance, rotating into higher-rated debt and defensive sectors. Instead, DoubleLine is buying junk bonds in parts of the economy, like airlines and gaming, which were forced into distress by lockdowns aimed at containing the virus spread. “We’re in a recovering environment, it’s a good time to own credit,” said Robert Cohen, director of DoubleLine’s global developed-credit team.

Threats

- PMI data for both manufacturing and services will be published next week. Flash surveys showed the U.S. economy gaining some momentum, linked to the further loosening of COVID-19 containment measures during the month. However, with virus numbers reaching new daily highs, the surveys also showed weakness in consumer markets and a cooling job market recovery.

- The S&P 500 Index is on track for its second consecutive monthly loss ahead of Tuesday’s presidential election. If that wasn’t bad enough, the equity benchmark could face a plunge of as much as 20 percent under a contested crisis scenario to the November 3 vote – where both sides refuse to accept the results – according to a team of economists and strategists at Bank of America, without citing a specific timeframe. “Prior macro shocks since 1998 have historically translated to a 13 percent peak-to-trough decline on average, but we could potentially see an even bigger decline, as political uncertainty combined with uncertainty around additional stimulus could put much more pressure on stocks,” they wrote.

- Fourteen states spanning the Rocky Mountain West to Pennsylvania recorded all-time highs in cases this week, the most of the pandemic. Illinois, Indiana and Iowa are among the states that hit single-day highs Thursday, according to Covid Tracking Project data. Pennsylvania, Colorado and others reported highs earlier in the week, the data show. The superlatives show how the wave that started in the upper Midwest is now hitting most of the nation, having moved to more populous states in the region and even pushing into the Northeast and West. Overall, cases hit a single-day record of 88,452 on Thursday, while the number of people hospitalized with the virus in the U.S. rose to 46,095, the most since Aug. 13, the project’s data show.

Energy and Natural Resources Market

Strengths

- The best performing commodity for the week was lumber, up 6.05 percent, on mill capacity restraints coupled with strong housing demand. U.S natural gas futures continue to rise as flows to LNG export terminals jump to the highest level on record. Bloomberg reports front-month futures are set for a sixth weekly gain for the longest streak since July 2016. Iron ore had its first weekly gain in three due to recent strength in China’s steel market. Fortescue Metals Group CEO Elizabeth Gaines says robust demand from the steel market is supporting sentiment and demand will remain strong next year, despite rising supplies.

- Total SE posted third-quarter profit that exceeded the highest analyst estimate and says it is doing ok with $40 a barrel oil. Bloomberg notes the French energy giant has fared better than its rivals and posted net income of $848 million, well above the average estimate of $478 million.

- Solar energy supplied 100 percent of South Australia’s electricity demand earlier this month, writes Bloomberg, making the state one of the first gigawatt-scale grids in the world to serve its entire demand with solar. The state aims for net 100 percent renewable electricity by 2030 and is working to reduce gas power plants’ securing of the grid.

Weaknesses

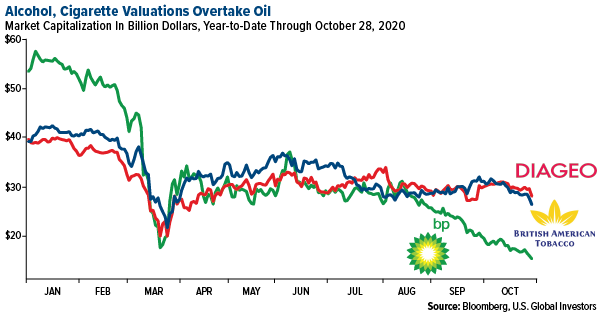

- The worst performing commodity for the week was crude oil. Oil is saw its largest monthly drop since March as concerns grow over the resurgent pandemic. Crude fell 10.59 percent for the week and 11.84 percent for the month of October. Oil giants continue to lose market cap, with BP falling below that of Diageo and British American Tobacco, top alcohol and cigarette companies. BP’s market cap fell below $50 billion for the first time since 1997 – a drop of 60 percent since the beginning of the year.

- Exxon Mobil warned it may take up to $30 billion in write-downs on natural gas fields. The oil major lost $680 million in the third quarter and its shares are down 50 percent for the year. The company announced firing and layoffs that will affect 14,000 workers globally, reports Bloomberg. Chevron announced it will lay off about 25 percent of Noble employees after completing the purchase of the company earlier in the month.

- Glencore, the world’s biggest shipper of coal, reduced its production target for the third time this year after facing an extended strike at a key Colombian mine, reports Bloomberg. The company expects to produce 109 million tons, compared with an earlier goal of 144 tons of the fossil fuel.

Opportunities

- UBS raised its price forecast for palladium to $2,500 an ounce by the end of December, up from $2,400 an ounce. Analysts at the bank say palladium imports from China have hit a record high on strong domestic car sales and tighter emission standards. Spot prices are up nearly 22 percent year-to-date. Impala Platinum says demand for platinum-group metals has remained strong as its output rose in the third quarter, reports Bloomberg. Platinum output from the top producer totaled 408,000 ounces compared with 281,000 ounces the same quarter last year.

- Sinopec, China’s biggest oil refiner, says it is investing all along the hydrogen supply chain to become a major player in the future of energy. The company is already China’s biggest hydrogen producer, making about 3 million tons of the gas a year, mostly to use as feedstock to improve the quality of its fuels, reports Bloomberg.

- Agnico Eagle and Newmont were named top performers on a broad range of environmental, social and governance (ESG) metrics within the senior gold miners, according to Credit Suisse and as reported by Bloomberg. Angico is a leader because of its strong community relations, above-average employee engagement and stricter regulations in its operation jurisdictions. Newmont has the “most transparent and detailed ESG reporting.” Alamos and Yamana were top performers in the intermediate category.

Threats

- The fate of oil drilling in the Arctic and the Pebble gold mine in Alaska hang in the balance of the presidential election, writes Bloomberg Green. Trump is pushing for development of the region while Biden has pledged to protect the natural resources. For the Pebble gold mine project in particular, the Trump administration has scrapped Obama administration pollution restrictions blocking the mine and Biden has promised to block the project if he wins, calling the area “no place for a mine.”

- Shell CEO Ben van Beurden said the company’s oil output reached a peak in 2019 and that large U.S. shale M&A isn’t affordable for their financial framework now. The CEO added that Shell is in the “dog house” due to capital indiscipline across the industry.

- According to data compiled by Bloomberg, energy’s weight in the S&P 500 fell to a closing low of 1.96 percent on Wednesday – the lowest since at least 1989. David Wilson writes that “energy has become about as irrelevant for the S&P 500 Index’s value as any industry has been in decades.”

Airline Sector

Strengths

- The best performing airline for the week was Chinese domestic air transportation company Spring Airlines, up 1.19 percent. Spirit Airlines was up as much as 8 percent on Thursday after the budget carrier beat revenue estimates. Allegiant was up as much as 10 percent after it gave a sunny outlook and the CEO said they are “flirting with cash-flow break-even.” Low-cost, domestic-focused carriers have fared better than big network carriers, notes CNBC.

- Volaris, Mexico’s largest airline, lowered fares by 30 percent to coax people back onto leisure routes and it worked, with passenger totals boosted to more than 70 percent of last year’s levels. Bloomberg notes Volaris is reviewing options to raise as much as $170 million and has not received any government aid. Volaris has also announced deals with airport operator Grupo Aeroportuario del Sureste SAB to offer discounts on flights connecting Mexico City with destinations such as Cancun, Cozumel and Huatulco, as it looks to entice more customers.

- SpiceJet is starting a new seaplane service between the city of Ahmedabad and Kevadia, the site of the world’s tallest statue, which is a 182-meter tribute to the country’s first home minister, reports Bloomberg. The 30-minute trip on a 15-seater Twin Otter 300 aircraft will cost $20 one-way. “Infrastructural challenges have been a key deterrent for providing air connectivity to smaller towns and cities,” SpiceJet Chairman Ajay Singh said in a statement. “With the ability to land on a small water body, seaplanes are the perfect flying machines that can effectively connect the remotest parts of India into the mainstream aviation network without the high cost of building airports and runways.”

Weaknesses

- The worst performing airline for the week was Air Canada, down 13.77 percent. Carriers appear to be planning for a bleak winter travel season. Several carriers lowered fourth-quarter capacity from prior estimates. As seen in the chart below, both Qantas and Lufthansa slashed capacity significantly for the last three months of the year.

- Turkish Airlines is putting foreign national pilots on unpaid leave for at least six months starting on November 1 to mitigate the impact of decimated air travel demand. The carrier reported a $280 million loss in the second quarter and passenger numbers are down by nearly two thirds. Turkish Airlines is one of the few carriers to refrain from job cuts, instead cutting pilot wages by half through 2021 and reducing salaries across the board, reports Bloomberg.

- Commercial aircraft orders in the third quarter hit the lowest on record of just 13 orders placed globally. There were four orders in July, nine in August and zero in September, according to aerospace and defense lobby group ADS.

Opportunities

- Nippon Airways, Japan’s largest carrier, signed an agreement to start buying sustainable aviation fuel from a Singapore refinery run by Neste Oyj. Bloomberg Green writes this is a small step toward more environmentally friendly travel. Japan has called for the country to become carbon neutral by 2050 – an ambitious target. Sustainable jet fuel has a limited number of producers and is more expensive than traditional fuel.

- A U.S. Defense Department study found that particles the size of the coronavirus are quickly removed from commercial aircraft cabins. The study found that filtration systems and rapid air-exchange rates mean only 0.003 percent of infected particles entered a masked passenger’s breathing zone. “Rapid dilution, mixing and purging of aerosol from the index source was observed due to both airframes’ high air-exchange rates, downward ventilation design, and HEPA-filtered recirculation,” according to the study, which was conducted in August. This study could help passengers feel more comfortable that their chances of contracting the virus on a flight is low.

- United Airlines announced it plans to offer pre-flight COVID-19 testing in November for some travelers going from Newark to London. United will pay for the rapid tests and run the trial from November 16 to December 11, reports CNBC. The effort aims to get around travel restrictions and concerns about the virus amid travel bans and quarantine requirements.

Threats

- Airports Council International (ACI) Europe predicts that 193 out of 740 airports, or about one in four, will face insolvency as quarantine requirements remain in place and travel fails to recover. The airfields in doubt are mainly smaller, regional hubs but still account for about 277,000 jobs, ACI said. “The figures published today paint a dramatically bleak picture,” Director General Olivier Jankovec said in a statement. “Eight months into the crisis all of Europe’s airports are burning through cash to remain open, with revenues far from covering the costs of operations.”

- ANA Holdings announced it plans to launch a new low-cost carrier focusing on medium-distance flights to Southeast Asian and Oceania. However, investors are skeptical given the current air travel environment. “There are significant risks over whether this can be a success,” Goldman Sachs Group Inc. analysts including Ben Hartwright said in a report Wednesday. Bloomberg notes that there have been few successful regional carriers. ANA Holdings is already expecting its biggest loss ever of $4.8 billion for the 2020 fiscal year.

- South Africa agreed to a $641 million bailout for South African Airways, the national airline, after a long search for private investors failed. Finance Minister Tito Mboweni had long opposed providing more funds to the company that has not made a profit for nearly a decade, reports Bloomberg. The airlines’ funds will come from South African government departments, including police, tertiary education, basic school and health. The threat is that the airline will still face unprofitability and take a toll on the country’s economy.

Emerging Markets

Strengths

- The best relative performing country in emerging Europe for the week was Czech Republic, losing 2.3 percent. The best performing country in Asia this week was Indonesia, gaining 30 basis points.

- The Romanian ron was the best relative performing currency in emerging Europe this week, losing 1.6 percent. The Pakistani rupee was the best performing currency in the Asia region this week, gaining 70 basis points.

- Later today, China is expected to release strong October purchasing manager’s index (PMI) data. Bloomberg economists predict manufacturing PMI at 51.6 and non-manufacturing PMI at 56.0. Fintech company Ang Group will start trading next week on the Hong Kong and Shanghai Stock Exchanges. It is going to be the largest IPO ever, even bigger than Saudi Aramco, showing the strength of Chinese fintech companies and the economy.

Weaknesses

- The worst performing country in emerging Europe for the week was Poland, losing 7.8 percent. The worst performing country in Asia was South Korea, down 4 percent.

- The Turkish lira was the worst performing currency in emerging Europe this week, losing 5 percent. The Indian rupee was the worst performing currency in Asia this week, losing 1 percent.

- Europe is reporting a spike in COVID-19 cases. A number of countries have announced more restrictions in order to prevent the spread of the infections. France and Germany imposed nationwide lockdowns. Economic recovery from the first nationwide shutdowns might not be as fast as previously planned.

Opportunities

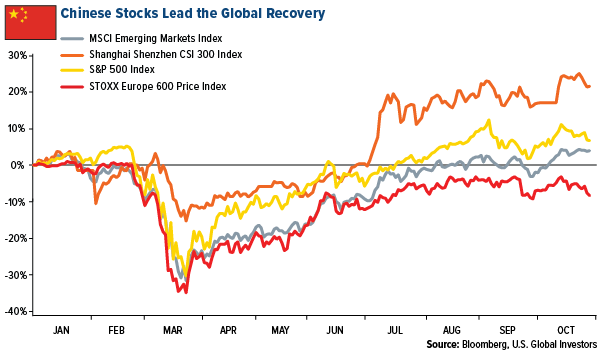

- Year-to-date, Chinese stocks have outperformed its global peers and this trend may continue. China not only managed to avoid a recession this year but actually sees its gross domestic product (GDP) growing 1.6 percent in 2020 while the world economy is expected to decline by 4.4 percent. Beijing is currently discussing its five-year development plan and a longer-term plan until 2035. Most analyst expect China to focus on domestic resources and consumption to guarantee growth.

- The pandemic has led to a decline in individual wealth, yet household wealth largely held up and even increased in China and India, Bloomberg reported. Household wealth in China grew 4.4 percent in the first half of the year and 1.6 percent in India. China benefited from reopening its economy quickly and ongoing government support to stimulate economic recovery.

- The European Central Bank (ECB) left its main rates unchanged and decided to hold off any changes to its bond buying program for now. However, the European bank declared it stood ready to provide more stimulus as needed. The pandemic bond-buying program will remain at 1.35 trillion euros.

Threats

- China increased buying U.S. farm products last month but remains well behind the schedule to get to a planned $140 billion of U.S. goods this year. As of September 30, China has purchased only $58.8 billion in goods covered by the agreement. Purchases should have reached $108 billion by that time to be on track toward the full-year target.

- With more lockdowns being implemented across Europe due to fast-spreading COVID-19 cases, the Eurozone Manufacturing PMI may fall further into contraction territory next week. The Final Service PMI most likely will be weaker than the preliminary reading of 46.2, further dragging the Composite PMI into lower levels. On a positive side, the Manufacturing PMI for the eurozone most likely will remain in the expansionary territory, above the 50 level. Most Bloomberg Economist predict 54.4 as a final reading for the manufacturing sector.

- The U.S. presidential election will take place next week with Joe Biden leading in the polls. His victory may increase political tensions with Russia and Turkey, with Democrats pushing for more sanctions against both countries. China, on the other hand, could see a positive reaction in case of Biden’s victory.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended October 30 was Money Plant Token, up 185 percent.

- A year-and-a-half after it was first announced, JPM Coin – JPMorgan Chase’s in-house stablecoin – is now live, writes CoinTelegraph. JPM Coin is in use by a major transnational tech firm for round-the-clock cross-border payments.

- Survey results released Tuesday from Grayscale’s “Bitcoin Investor Study” show more than half of U.S. investors are interested in buying bitcoin in 2020. As reported by CoinDesk, compared to the previous year, the results mark a “significant increase,” with a rise of 19 percent.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended October 30 was AML Bitcoin, down 96 percent.

- According to CoinGecko, an arbitrage trade exploiting weak points in DeFi protocol Harvest Finance led to some $24 million in stablecoins being siphoned away from the project’s pools on Monday, writes CoinDesk. The attacker used a “flash loan” to manipulate the process, and it sent the platform’s native token, FARM, down by 65 percent in less than an hour.

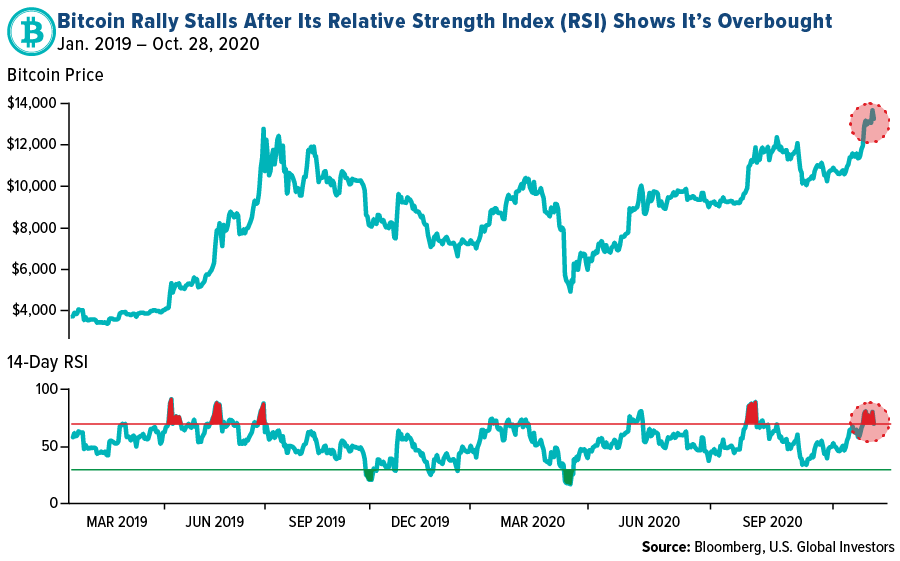

- Bitcoin has rallied higher over the past week, approaching the $14,000 mark. As shown in the chart below, however, despite the impressive gains, a correction could be imminent. The Relative Strength Index is showing the digital asset is overbought.

Opportunities

- 2020 is home to yet another crypto industry acquisition, reports CoinTelegraph. An official announcement highlights that INX has signed a term sheet for the acquisition of OpenFinance, which operates as a registered broker-dealer. “With the new deal, INX is set to acquire OpenFinance’s broker-dealer and alternative trading system business including its systems, digital asset listings, client base and licenses,” writes CoinTelegraph.

- The cryptocurrency industry is welcoming another high-profile executive from traditional finance, writes CoinTelegraph. Filomena Ruffa, former VP of innovation and strategic partnerships at Visa’s Latin America division, has joined Crypto.com to expand the company’s Latin American market, the article continues.

- Big data and analytics company CyberVein announced this week another major technological breakthrough during its Third Anniversary and a Re-branding Conference in Shanghai today, reports CoinTelegraph. CyberVein unveiled that it has piloted the first-of-a-kind decentralized non-fungible token (NFT) issuance platform, entitled CROSS.

Threats

- U.S. President Donald Trump’s campaign website was briefly compromised on Tuesday, writes CoinDesk, as hackers looked to fleece cryptocurrency from unsuspecting supporters in the final days before the 2020 election. The New York Times reports that the hackers were soliciting donations in the monero cryptocurrency due to privacy enhancing properties that make it hard to trace.

- Customers of hardware cryptocurrency wallet Ledger are being targeted by a phishing attack posing as an email from Ledger support, writes CoinDesk. The fake emails state, “Our forensics team has found several of the Ledger Live administrative servers to be infected with malware.” This claim is false and a phishing attempt, despite it looking professional.

- Investors who claim to have lost hundreds of thousands of pounds in an alleged cryptocurrency fraud, have had no luck persuading the police that there was in fact a crime committed, writes CoinDesk. West Midlands Police dropped the case, saying none of the provided evidence took it “further forward,” adding that “no offenses had been committed.” As the article continues, 14 investors are still pushing authorities to investigate the scheme.

Leaders and Laggards

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (09/30/2020):

SPDR Gold Shares

Impala Platinum Holdings Ltd

Newmont Corp

Brixton Metals Corp

Ivanhoe Mines Ltd

Evolution Mining Ltd

TOTAL SE

Grupo Aeroportuario del Sureste SAB

Allegiant Gold Ltd

Qantas Airways

United Airlines Holdings Inc

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The CSI 300 Index is a free-float weighted index that consists of 300 A-share stocks listed on the Shanghai or Shenzhen Stock Exchanges. The STOXX Europe 600 Index is derived from the STOXX Europe Total Market Index (TMI) and is a subset of the STOXX Global 1800 Index. With a fixed number of 600 components, the STOXX Europe 600 Index represents large, mid and small capitalization companies across 17 countries of the European region.