Frank Talk

Is It Time to Consider Shipping Stocks?

Date Posted: January 10, 2024

Read time: 4 min

Growing tensions in the Red Sea, a crucial artery for international trade, have sparked a significant shift in the shipping industry. This shift, I believe, offers a compelling case for global shipping stocks.

As many readers are already aware, Iran-backed Houthis have recently attacked tankers and cargo vessels sailing through the Red Sea, a passage used by about 12% of global trade. These disruptions, which are related to the Israel-Hamas War, have prompted shippers to seek alternative, though costlier, routes, including around Africa’s Cape of Good Hope.

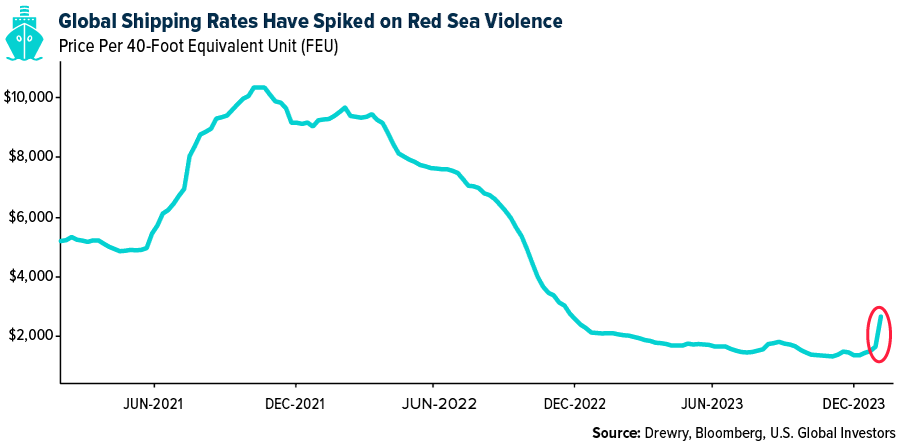

The detour has had an immediate impact: soaring container freight rates. Since tensions escalated last month, global rates have nearly doubled, a clear indicator of the increased costs incurred by carriers and passed on to exporters. According to Drewry data, a company that paid about $1,400 to ship a 40-foot container at the end of November 2023 can now expect to pay more than $2,600 to ship the very same container.

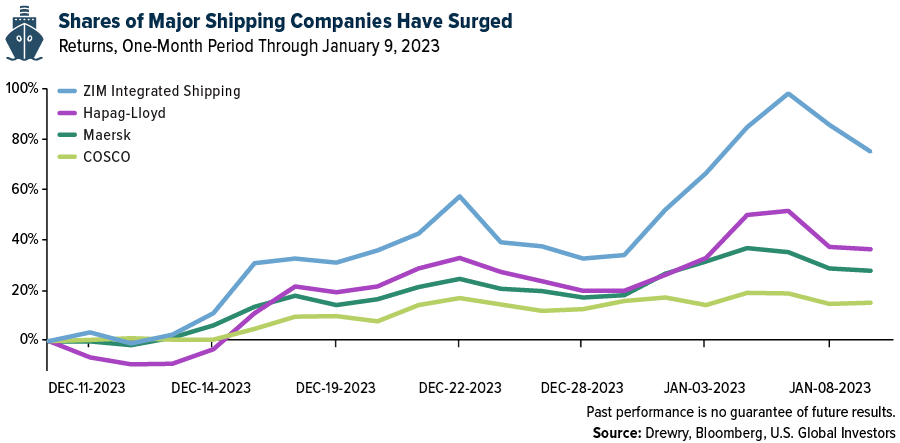

Shares of shipping companies have jumped as a result. For the one-month period through January 9, Israel’s ZIM Integrated Shipping surged over 73%, the highest of any company in the Solactive Global Shipping Index. Other top performers were Hapag-Lloyd, up 37% over the same period; AP Moller-Maersk, up 28%; and China’s Cosco Shipping, with a 14% return.

The Economic Ripple Effects of Shipping Detours

The financial implications of the detours are substantial. An extended round trip between Asia and northern Europe is believed to cost an additional $1 million in fuel per vessel, and given the strategic importance of the Suez Canal, the rerouting of ships adds significant delays to cargo shipments, further inflating costs.

Remember the March 2021 incident where the Ever Given container ship ran aground in the Suez Canal? The six-day episode cost the global economy an estimated $9.6 billion a day. The current standoff in the Red Sea could have a similarly profound economic impact, albeit spread out over a longer period.

The timing is also particularly sensitive, as China’s Lunar New Year approaches—a period traditionally marked by an increase in shipping demand. Even before the Houthi attacks, Maersk warned customers of “exorbitant” rates, “additional peak season surcharges” and a “shortage of empty containers” related to the Chinese holiday.

The cost implications are already visible. Rates for shipping goods from Asia to the Mediterranean and North America’s East Coast have risen sharply. We believe this trend is likely to continue.

Investment Opportunities in a Shifting Shipping Landscape

The strategic significance of the Red Sea and Suez Canal cannot be overstated. These routes not only link Europe with Asia’s major suppliers but also facilitate a substantial portion of the world’s crude oil and oil products transport. The diversion of tanker cargoes further escalates the demand for shipping, thereby increasing the ton-mile requirement, a key measure in the shipping industry.

In a recent note to investors, Bank of America outlined a “doomsday scenario” in which both the Suez Canal and Panama Canal, responsible for about 5% of global trade, become impassable. Such an event would “boost fleet demand between 1-2%,” among other ramifications, Bank of America analysts wrote.

Accurate or not, the current standoff presents a unique opportunity for investors to consider global shipping stocks, in my opinion. The hostilities are reshaping the logistics of international trade, leading to higher costs and extended transit times. The situation is likely to persist, offering a potentially lucrative method for investors seeking to capitalize on these developments.

To learn more about the global shipping industry, including how you can gain exposure, email us at info@usfunds.com with the subject line “Shipping Stocks.”

The Solactive Global Shipping Index consists of global shipping companies engaged in the maritime transportation of goods and raw materials, including consumer and industrial products, vehicles, dry bulk, crude oil and liquefied natural gas.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor. By clicking the link(s) above, you will be directed to a third-party website(s). U.S. Global Investors does not endorse all information supplied by this/these website(s) and is not responsible for its/their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of 12/31/2023: AP Moller – Maersk A/S, COSCO SHIPPING Holdings Co. Ltd.