3 Things Driving Oil Prices This Week

Date Posted: April 26, 2019

Read time: 57 min

I'm incredibly honored to play a role in this emerging and very promising industry, and it's a responsibility I take very seriously, despite not drawing a salary. The search for a new HIVE CEO is underway, but in the meantime, I'm committed to the company's success, and I see no greater duty than fulfilling my fiduciary obligation to all shareholders equally.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

We’ll get to talking about oil and energy in just a moment, but first I have something important to share with you all.

As many of you know, aside from being the chief executive of U.S. Global Investors, I also serve as the interim chairman and interim CEO of HIVE Blockchain Technologies, the first publicly listed company engaged in the mining of cryptocurrencies.

I’m incredibly honored to play a role in this emerging and very promising digital industry, and it’s a responsibility I take very seriously. The search for a new HIVE CEO is underway, but in the meantime, I’m committed to the company’s success, and I see no greater duty than fulfilling my fiduciary obligation to all shareholders equally. On top of all this, I haven’t taken a salary as interim CEO.

If you’ve studied corporate law, you might be familiar with duty of care and duty of loyalty, the twin pillars of fiduciary duty. Whereas the former charges officers and directors to act prudently, the latter says that they should refrain from benefiting themselves at the expense of the company they serve.

To me, that means insisting on good corporate governance and transparency. I expect that from not only HIVE’s own leaders but also those at Genesis, HIVE’s strategic partner and largest shareholder.

Sadly, Genesis seems not to be of the same mind.

I won’t rehash all of the grievances here. Those curious can read the press release.

Suffice to say, though, that ideologies clashed this past weekend, of all weekends, when many families were celebrating Easter or Passover. After months of what I believed were good faith efforts to get Genesis to disclose all costs for mining operations—leading to a breach of contract we value at around $50 million, as per the master service agreement (MSA)—Genesis tried to “resolve” the dispute by removing all HIVE directors who were independent of Genesis’ self-interests, including myself, and replacing them with their own officers and employees.

Ultimately, this boardroom dispute failed.

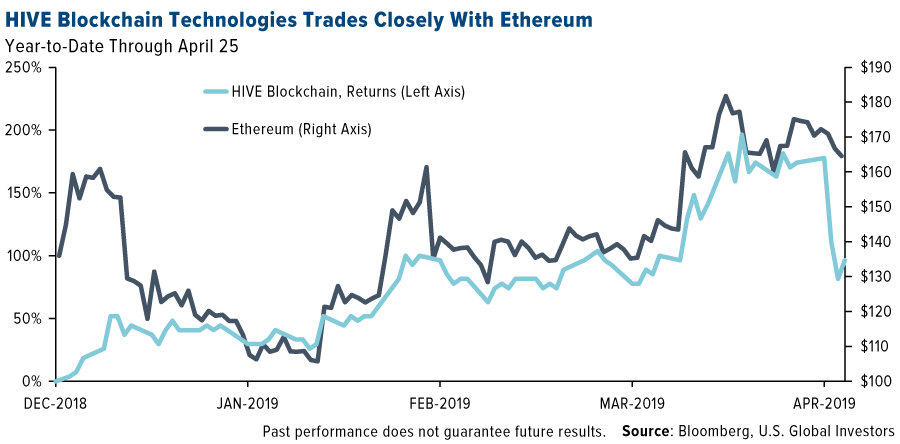

So why am I sharing this with you? One, I wanted to give you some insight into why HIVE stock fell some 40 percent over two days this week. Before the selloff, HIVE had been tracking Ethereum and was up nearly 200 percent for 2019. As Warren Buffett might say, Mr. Market was none too pleased with Genesis’ actions.

And two, I take my role as interim CEO seriously. I believe that my fiduciary duties extend to all shareholders of HIVE, not just to Genesis. I seek and fight for good governance. I manage conflicts of interest. And I demand transparency. These are qualities I admire in companies as chief investment officer of U.S. Global Investors.

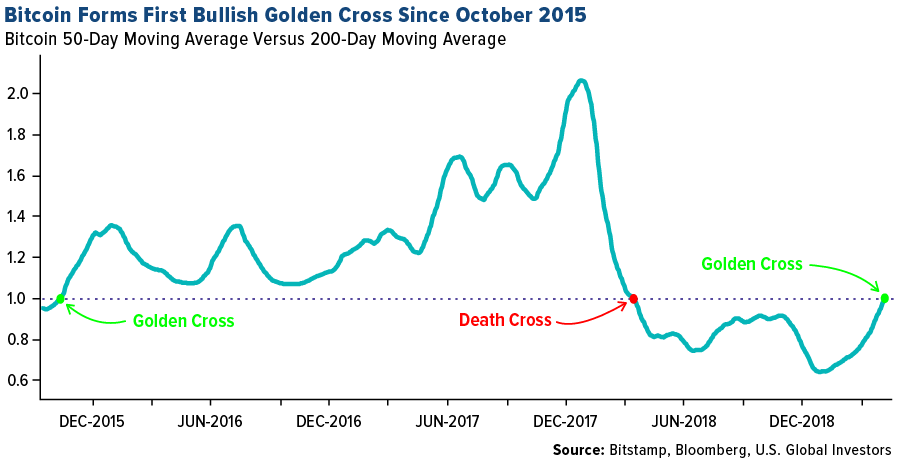

Despite all this, I’m hopeful that a satisfactory resolution can be reached between the two parties, especially now as prices of digital currencies are stirring to life. In an exciting bit of news, bitcoin not only traded above $5,500 this week but also signaled a bullish “golden cross” for the first time since 2015. To read more, jump to the Blockchain and Cryptocurrency section by clicking here.

Now let’s talk about energy! Below are three things from this past week that you should know about.

1. Goodbye, Iran Oil Import Waivers. Hello, Higher Energy Prices?

Besides Occidental Petroleum’s bidding war with Chevron for fellow producer Anadarko Petroleum, the big energy news this week is that President Donald Trump, as expected, moved to end all sanction waivers for nations that import Iranian oil. Starting in May, countries that still buy oil from Iran could face U.S. penalties. In response, Brent crude hit $75 per barrel for the first time in six months.

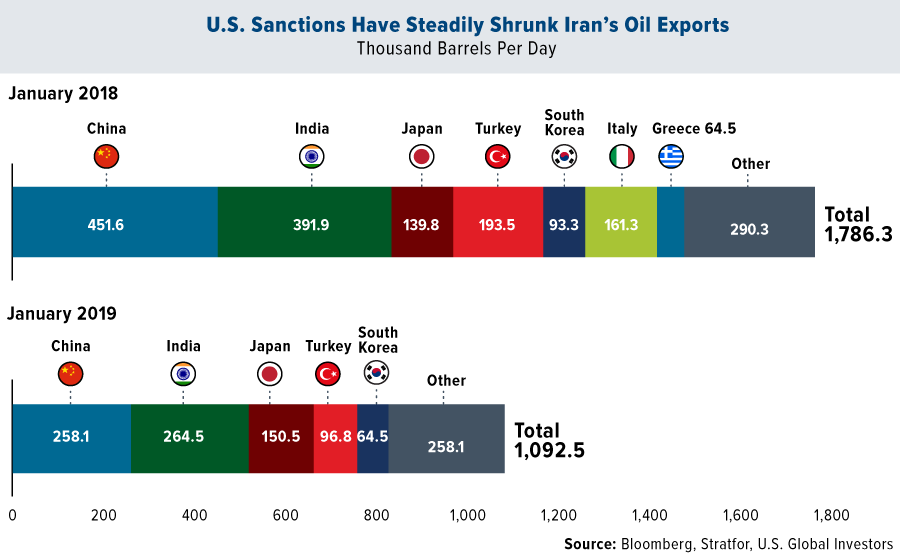

Oil and natural gas are the Middle Eastern country’s most important export, so the policy is intended to hit Tehran where it hurts. The plan, announced last summer, appears to be working so far. Between January 2018 and January 2019, Iranian oil exports fell by nearly 700,000 barrels per day (b/d). (The data could be inaccurate, though, since Iranian oil tankers are believed to be turning off their transponders in an effort to conceal themselves from satellite tracking systems.)

It’s unlikely that all countries will immediately zero-out imports from Iran. I would be surprised to see China, the number one consumer, trim its imports much further. Iran is such a key strategic player connecting Asia and the Middle East as part of China’s Belt and Road Initiative (BRI).

So who will pick up the global slack if Trump’s plan succeeds and Iranian exports go offline? Trump suggests Saudi Arabia and the United Arab Emirates (UAE) will. Secretary of State Mike Pompeo also believes the U.S. can, but this would “be a stretch,” according to Bloomberg.

“Oil condensate from the Eagle Ford shale basin in Texas is similar, though a bit heavier than Iran’s light South Pars condensate. But the Eagle Ford produces only about 150,000 b/d of its product, compared with Iran’s daily output of 600,000 barrels in 2017,” the article reads.

2. U.S. Crude Inventories Climb More Than Expected

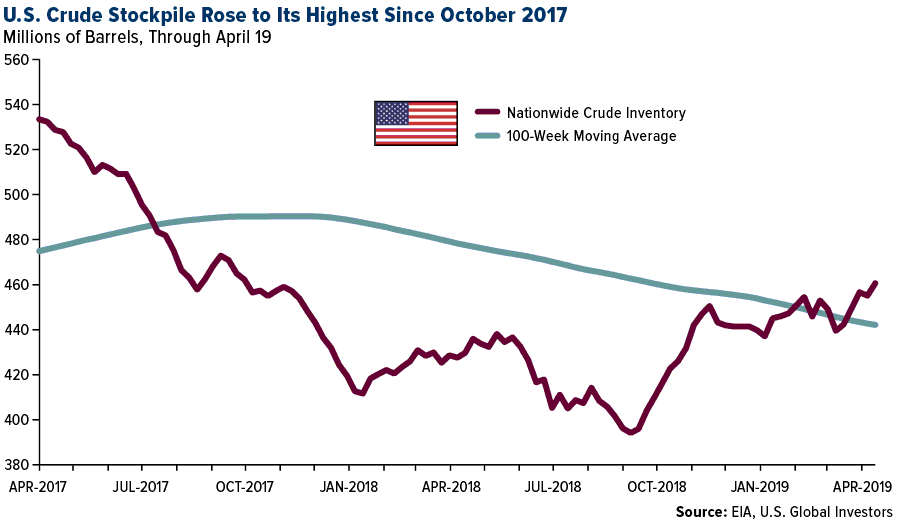

But maybe there’s something to what Pompeo says after all. Thanks to its fracking industry, the U.S. is producing oil at a breakneck pace. This is turning up in domestic inventories, which have been building steadily over the past seven months or so. For the week ended April 19, oil stocks rose by 5.5 million barrels, much more than what analysts had anticipated. At 460 million barrels, total crude stocks now sit at their highest level since October 2017.

The U.S. is already the biggest oil producer in the world, having overtaken Saudi Arabia and Russia last year. Looking ahead, U.S. output could equal that of both countries by 2025, according to International Energy Agency (IEA) estimates. And in January, the Department of Energy said that the U.S. will become a net exporter of energy in 2020—something it hasn’t achieved in almost 70 years.

3. Oil Prices Were Headed for Overbought Territory… Until Trump Stepped In

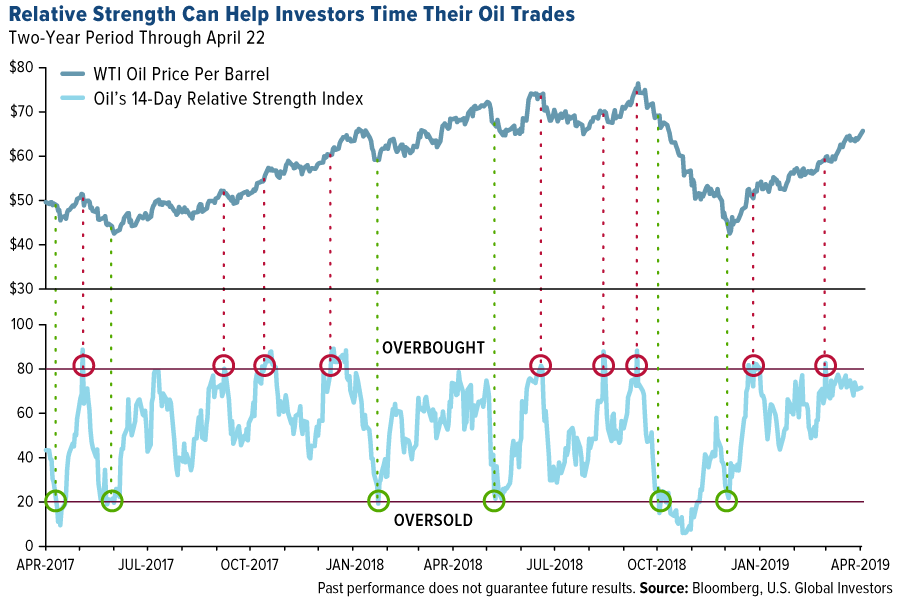

Oil prices neared overbought territory, as you can see in the chart below, which shows oil’s 14-day relative strength index (RSI). When an asset’s RSI rises above 80, it typically means that it’s overbought, suggesting it might be time to take some profits. When it falls below 20, meanwhile, it often means that the asset is oversold, signaling a possible entry point.

Again, oil prices looked to be on the overbought side, especially after the administration announced the end to sanction waivers. But the trend could reverse very rapidly.

Case in point: On Friday, the president, who favors lower energy costs, claimed that he “called up” OPEC and told the global oil exporting cartel: “You’ve got to bring [gasoline prices] down, you’ve got to bring them down.” Which, of course, is not in Saudi Arabia’s best interest.

In any case, the price of West Texas Intermediate (WTI) plunged close to 4 percent on Friday, its biggest one-day drop since mid-December. As a result, oil’s RSI sharply turned down to around 50, from nearly 72 on Monday.

Depending on what happens in the next few days, oil traders might be looking at another buying opportunity.

Get even more award-winning market commentary by subscribing to my CEO blog Frank Talk!

Gold Market

This week spot gold closed at $1,286.25, up $10.42 per ounce, or 0.82 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 0.36 percent. The S&P/TSX Venture Index came in up 0.24 percent. The U.S. Trade-Weighted Dollar gained 0.57 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Apr-19 | Housing Starts | 1225k | 1139k | 1142k |

| Apr-23 | New Homes Sales | 649k | 692k | 662k |

| Apr-25 | Durable Goods Orders | 0.8% | 2.7% | -1.1% |

| Apr-25 | Initial Jobless Claims | 200k | 230k | 193k |

| Apr-26 | GDP Annualized QoQ | 2.3% | 3.2% | 2.2% |

| Apr-29 | Hong Kong Exports YoY | -2.6% | — | -6.9% |

| Apr-30 | Germany CPI YoY | 1.5% | — | 1.3% |

| Apr-30 | Conf. Board Consumer Confidence | 126.1 | — | 124.1 |

| May-1 | ADP Employment Change | 180k | — | 129k |

| May-1 | ISM Manufacturing | 55.0 | — | 55.3 |

| May-1 | FOMC Rate Decision (Upper Bound) | 2.50% | — | 2.50% |

| May-1 | Caixin China PMI Mfg | 51.0 | — | 50.8 |

| May-2 | Initial Jobless Claims | 218k | — | 230k |

| May-2 | Durable Goods Orders | — | — | 2.7% |

| May-3 | Eurozone CPI Core YoY | 1.0% | — | 0.8% |

| May-3 | Change in Nonfarm Payrolls | 185k | — | 196k |

Strengths

- The best performing precious metal for the week was palladium, up 2.79 percent as hedge funds boosted their net bullish positions. Despite U.S. dollar strength, gold traders and analysts returned to their majority bullish position on the yellow metal this week, according to the weekly Bloomberg survey. The U.S. currency kept pressure on gold up until Canada’s central bank decided to remove a bias to higher interest rates. This pushed long-term debt yields lower than short-term, explains Bloomberg, which is seen by some economists as a sign of a looming recession, potentially good for gold.

- Ahead of the U.S. GDP data release, gold headed for its first weekly gain in five, reports Bloomberg, also being supported by haven demand as some countries show signs of economic weakness. On Friday, some of the underlying numbers in the U.S. GDP report came in weaker-than-expected. This, along with a drop in the dollar, pushed gold toward its biggest advance in more than a month. It extended its one-week high too, as investors assessed corporate earnings.

- The Romanian Parliament has approved the return of gold reserves from the U.K., reports Bloomberg. Lawmakers in the country voted 165 to 90 to approve a law forcing the central bank to bring back Romania’s gold reserves from the Bank of England (BOE), according to Deputy Speaker Florin Iordache.

Weaknesses

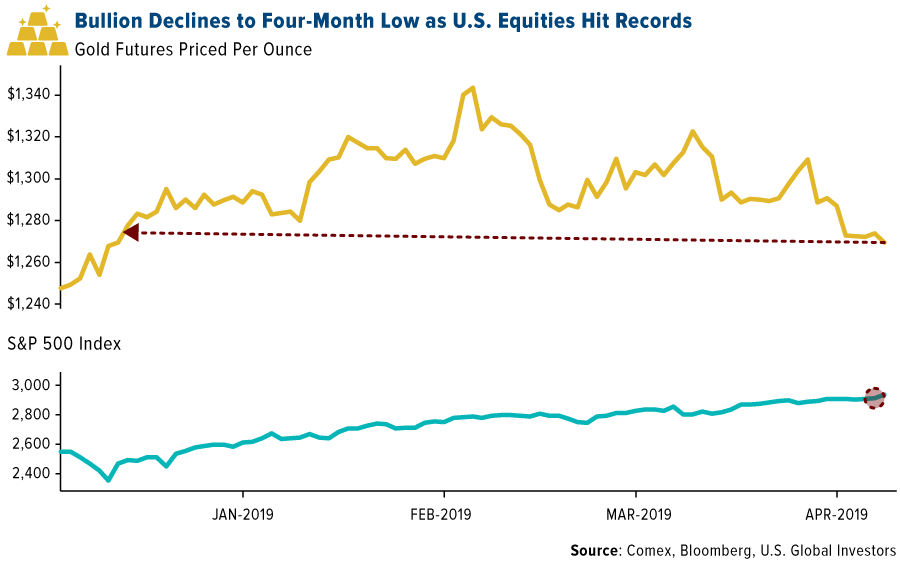

- The worst performing precious metal for the week was platinum, down 0.45 percent as hedge funds cut their new bullish position from the prior week. Demand for bullion as a haven asset has been wavering, reports Bloomberg, as better-than-expected earnings bolster equities and the dollar strengthens. On Tuesday, the yellow metal fell to a 2019 low as U.S. equities climbed to record highs. Other factors hurting haven demand for gold include prospects for a U.S.-China trade deal, Bloomberg continues, along with outflows from exchange-traded funds (ETFs).

- Turkey’s central bank saw its gold reserves fall $473 million from the previous week, according to official weekly figures from the central bank in Ankara. The bank’s gold holdings as of April 19 were $20.4 billion, dropping 20 percent year-over-year.

- When deposits of precious metal form in the earth, geologists often speak of the changes taking place over hundreds of millions of years. Investors in Guyana Goldfields experienced geologic time at a significantly faster pace this spring, writes the National Post. The company previously sat on nearly 4 million ounces of contained gold at its Aurora mine, but by the end of the day that number had fallen by around 1.5 million ounces. “The gold was never there – the new resource model has shown us that,” Scott Caldwell, chief executive and director, told the Financial Post this week.

Opportunities

- Investors who are striving to optimize their portfolios should consider taking cues from the world’s central banks, writes the Financial Express. “Informed money,” such as these banks, is the cash invested by those who have a better understanding of the market, or with access to information channels that a regular investor does not. Furthermore, Bloomberg writes that official sector gold purchases could reach 700 tons this year, “assuming the China trend continues apace and Russia at least matches its 2018 volumes.” India’s central bank is likely to join its counterparts, as the Reserve Bank of Index (RBI) may purchase 1.5 million ounces in 2019, according to Howie Lee, an economist at Oversea-Chinese Banking Corp.

- According to the World Bank, gold prices are expected to remain higher in 2019, on account of strong demand and an extended pause in interest rate hikes by the Federal Reserve. As Goldman Sachs outlines in a note this week, investors should take long positions on gold and short silver in order to benefit from the current “not too hot and not too cold macro environment.” And despite the group lowering its forecast on the yellow metal, it still remains bullish.

- Demand for safe haven assets ensures a “constant flow” of debt buyers, writes Bloomberg, with Treasuries offering positive yield amid a sea of sub-zero rates. Is gold the next safe haven in line as U.S. debt continues to pile up as it is no one else’s liability? Then there’s U.S. housing inflation, which Bloomberg says will make a substantial contribution to a projected acceleration in consumer prices by year-end. At a time when Fed policy makers are losing confidence that inflation will pick up soon, this will help jump-start it.

Threats

- During his speech to some 40 world leaders at the Belt and Road forum in Beijing this week, Chinese President Xi Jinping seemed to aim his thoughts at the U.S.—particularly Donald Trump. A large portion of his speech focused on domestic reforms, pledging to address state subsidies, and so on, writes Bloomberg—all items that the U.S. is addressing in trade talks with Beijing. “He appeared to be offering his personal approval of the concessions that China is likely to make as part of an imminent U.S.-China trade deal,” said Tom Rafferty, the Economist Intelligence Unit’s regional manager of China.

- Bloomberg Businessweek recently outlined the Venezuelan gold trading scheme with Turkey where at least $900 million in gold has been shipped before the U.S. banned anyone from doing business with its gold sales. Gold sales have been vital to Nicolas Maduro ability’s to maintain the government in Venezuela and have been a major headwind to gold breaking out of its current sideways trading pattern. Although the U.S. has intensified its focus on stopping the selling of the gold, Turkey and Venezuela show no signs of ending the trade.

- A Reuters analysis found that billions of dollars’ worth of gold is being smuggled out of Africa every year, going through the United Arab Emirates (UAE) in the Middle East. In fact, according to customs data, the UAE imported $15.1 billion in gold from Africa in 2016. This is more than any other country and up from $1.3 billion in 2006, the Reuters report continues. A majority of the gold wasn’t recorded in the exports of African states, and according to trade economists interviewed by Reuters, this “indicates large amounts of gold are leaving Africa with no taxes being paid to the states that produce them.”

April 24, 2019Invest in Optimism: A Conversation With Keith Fitz-Gerald |

April 22, 2019The Hunger for Muni Bonds (And Gold!) Is Real |

April 15, 2019The Second Best Performing Asset Since 1999 |

|||

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average lost 0.06 percent. The S&P 500 Stock Index rose 1.20 percent, while the Nasdaq Composite climbed 1.85 percent. The Russell 2000 small capitalization index gained 1.66 percent this week.

- The Hang Seng Composite lost 1.68 percent this week; while Taiwan was down 0.15 percent and the KOSPI fell 1.66 percent.

- The 10-year Treasury bond yield fell 0.06 basis points to 2.50 percent.

Domestic Equity Market

Strengths

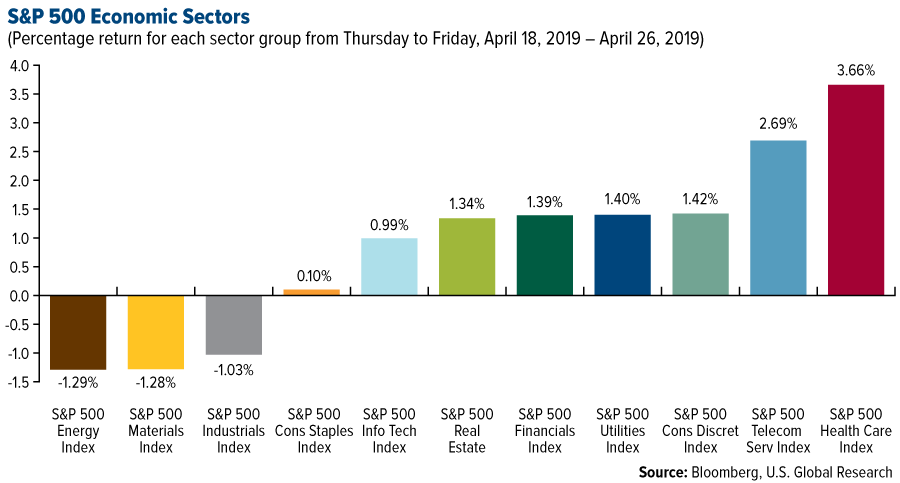

- Health care was the best performing sector of the week, increasing 3.66 percent versus an overall increase of 1.03 percent for the S&P 500 Index.

- Hasbro was the best performing stock for the week, increasing 15.56 percent.

- Microsoft briefly became a $1 trillion company, reports Business Insider, after the company posted third quarter earnings that blew away Wall Street estimates. Microsoft reported revenue of $30.6 billion, which is up 14 percent from the same period last year, and earnings of $1.14 per share.

Weaknesses

- Energy was the worst performing sector for the week, decreasing 1.29 percent.

- 3M was the worst performing stock for the week, falling 12.43 percent.

- Tesla had a dim first quarter, as sales of the Model S and Model X declined dramatically. The electric-car maker lost an adjusted $2.90 a share on revenue of $4.54 billion, missing the $1.30 loss and $4.84 billion that were expected. The stock fell 4.26 percent to $247.63 a share on Thursday, reports Business Insider.

Opportunities

- The stock market just hit its first record high since October, and if history is a guide, then it looks as if stocks could be headed even higher. Historically, following periods when new highs were not recorded for at least six months, S&P 500 returns over the next 12 months averaged 12.9 percent, with 17 of the 18 periods recording a positive return, according to LPL Financial’s Ryan Detrick.

- Uber is reportedly setting a price range of $44 to $50 for its upcoming IPO. The ride-hailing company could raise between $8 billion to $10 billion in public financial market at a valuation of up to $90 billion, according to a report from Bloomberg.

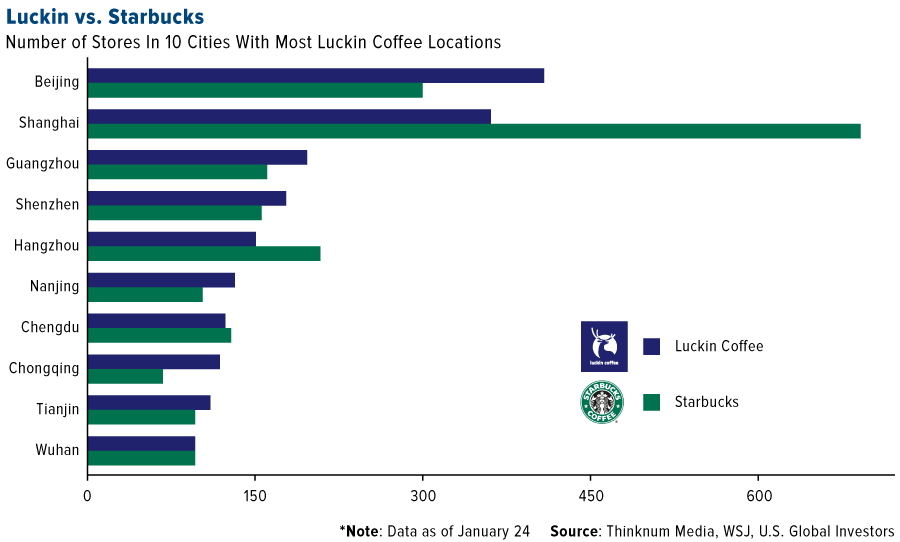

- Luckin Coffee, the Chinese rival to Starbucks, has filed for a U.S. initial public offering (IPO) and is aiming for a valuation of between $4 billion and $5 billion, Reuters says.

Threats

- Facebook said it’s expecting to pay a fine of between $3 billion to $5 billion to the Federal Trade Commission (FTC), reports the New York Times. News of the fine came out in the company’s earnings report, filed on Wednesday. Additionally, New York’s attorney general is investigating Facebook for harvesting 1.5 million users’ email data without their consent. Furthermore, the company is also looking at a potential $2.2 billion fine for storing millions of passwords insecurely. Europe’s default privacy regulator for Facebook will investigate whether the company broke the law after the social media company admitted to storing millions of passwords in plain text.

- Wall Street still can’t get behind Snap, writes Business Insider. Shares of the company have skyrocketed 110 percent this year, but Wall Street analysts are still overwhelmingly cautious to bearish on the name, the article continues. Additionally, in its latest report the company’s user growth stalled.

- Twitter’s first-quarter earnings beats Wall Street on revenue and profit, but the company is still losing monthly users at a rapid pace.

The Economy and Bond Market

Strengths

- U.S. gross domestic product (GDP) rose at a 3.2 percent annual rate in the first three months of the year, the Commerce Department said Friday. That is significantly better than most economists expected, and far better than the lackluster forecasts of early this year, when many forecast a near stall in growth.

- The University of Michigan’s Index of Consumer Sentiment has moved sideways, recording only small monthly variations for more than two years. The Sentiment Index has averaged 97.2 during the past 28 months—identical to the April 2019 reading—and has remained between 95.0 and 99.0 for 21 of those months. Confidence has been maintained at high levels due to low rates of unemployment and inflation as well as renewed income growth, said economist Richard Curtin, director of the U-M Surveys of Consumers. Although consumers now anticipate a slower pace of economic growth, they expect those favorable conditions to persist during the year ahead, he said.

- The U.S. Commerce Department reported Thursday that orders for large manufactured goods jumped 2.7 percent in March. Manufacturers’ shipments, inventories and orders rose $6.8 billion to $258.5 billion. The business investment segment within the durable goods orders grew at its strongest pace in eight months. The category rose 1.3 percent in March, which is its best showing since a 1.5 percent increase last July.

Weaknesses

- Sales of previously owned homes eased more than forecast in March, suggesting the housing market is still finding its footing after a weak 2018. Contract closings decreased to a 5.21 million annual rate, falling 4.9 percent from February’s downwardly revised pace, the National Association of Realtors said Monday.

- South Korea, a bellwether for global trade and technology, cast doubt over hopes for a quick rebound in the world economy by reporting its biggest contraction of GDP in a decade. Asia’s fourth-largest economy shrank 0.3 percent in the first quarter from the previous three months, versus estimates for a 0.3 percent gain. That’s a big worry for other manufacturing and technology-driven exporters, including Japan, Germany and Taiwan.

- Key gauges of confidence in the euro area’s two largest economies unexpectedly deteriorated, signaling that a long-expected rebound may still be some way off. Ifo said its closely watched index of German business sentiment dropped to 99.2 in April, missing forecasts for a slight improvement. Measures for current conditions and expectations among executives declined. In France, confidence in manufacturing slumped to the lowest level in almost four years as business leaders’ assessment of their own production plunged.

Opportunities

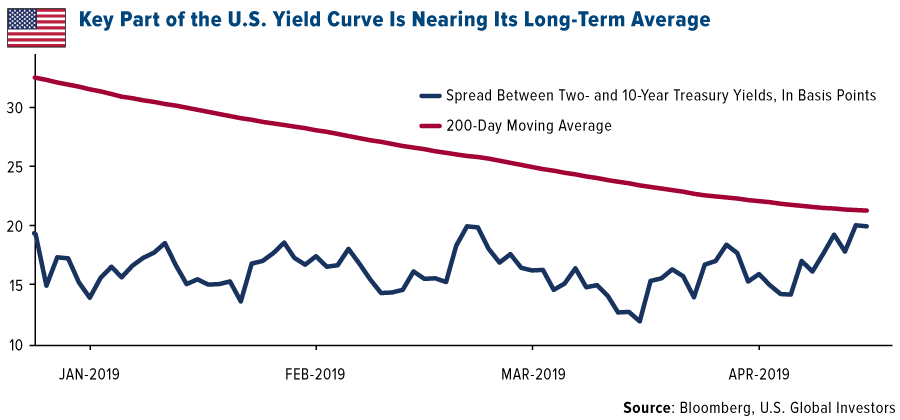

- U.S. recession fears flourished a month ago, but today the optimists look vindicated. Key segments of the Treasury yield curve have steepened, with the gap between two- and 10-year securities back near its 200-day moving average. LPL Financial Chief Investment Strategist John Lynch notes that the curve has steepened for four consecutive weeks, the longest stretch since November 2016. Further improvements in economic data and a patient Federal Reserve could boost the spread “25 basis points or more through the end of the year,” he wrote in a report Tuesday.

- The SIFMA Municipal Swap Index, a weekly index of tax-exempt debt with variable interest rates, rose 26 basis points to 2.3 percent on Wednesday. The jump left the index at the highest level since the 2008 credit crisis and follows an increase last week. The index now yields more than AAA rated municipals maturing in 2035.

- Wall Street is near record highs and recession worries are receding as investors wonder if the Fed will start raising rates again. Such a pivot is unlikely after the Fed killed off rate-rise expectations at its March meeting. And the latest Reuters poll all but puts to bed any risk of rates will go up this economic cycle, given inflation remains below the Fed’s alarm threshold and unemployment is the lowest in generations.

Threats

- The benchmark 10-year yield touched 2.61 percent last week, the highest since the Fed surprised traders in March by shifting to a more dovish stance. That was up from 2.34 percent on March 28, the lowest since December 2017. Traders are now pricing in a bit more than half of a quarter-point rate reduction this year, whereas a few weeks ago they were ready for more than a full cut. Technical indicators also suggest odds are greater for yields to rise, said Marty Mitchell, an independent strategist. The 10-year yield’s dive to 2.34 percent was an “extreme,” as confirmed by the 10-day moving average moving above the 30-day, he said.

- Some Fed policy makers seem resigned to running a heightened risk of asset bubbles and other financial excesses as they seek to keep the economic expansion going, writes Bloomberg News’ Rich Miller. That’s one of the messages tucked inside the minutes of the Federal Open Market Committee’s March 19-20 policy making meeting.

- Municipal analysts see the funding of public pensions to be the most important issue facing the market even after the retirement systems benefited from a surging stock market, according to a survey published by Smith’s Research & Gradings. After pensions, the level of fiscal preparedness for the next recession and demographic shifts in the U.S. are the second and third biggest issues cited by analysts who responded to the survey.

Energy and Natural Resources Market

Strengths

- The best performing major commodity for the week was lumber, which gained 3.63 percent. As Weyerhaeuser noted, sales would grow if the trade war is resolved. Heavy equipment maker Caterpillar reported first quarter profits and sales that beat estimates, largely driven by its mining business. Bloomberg’s Joe Deaux writes that “the results from Caterpillar, an economic bellwether, add to signs that industrial earnings are holding up in the face of the U.S.-China trade war and worries that some end users may be reaching the peaks in their growth cycles.”

- A bidding war for Anadarko Petroleum has begun after Occidental Petroleum made a $38 billion counteroffer. Occidental said this Wednesday that it is offering about a 20 percent premium over Chevron’s agreement to buy the company announced earlier this month. Anadarko has operations in the Permian Basin and Chevron hoped its acquisition would launch it into the upper leagues of oil companies.

- Several base metals—including copper and aluminum—saw a boost on Wednesday as declining stockpiles partially offset concerns over China’s economic stimulus. Nickel inventories reached their lowest levels since trading started in 2015. The London Metal Exchange (LME) announced that it will allow only responsibly-sourced metals to be traded on the exchange from 2022 onward due to rising demand for sustainable products.

Weaknesses

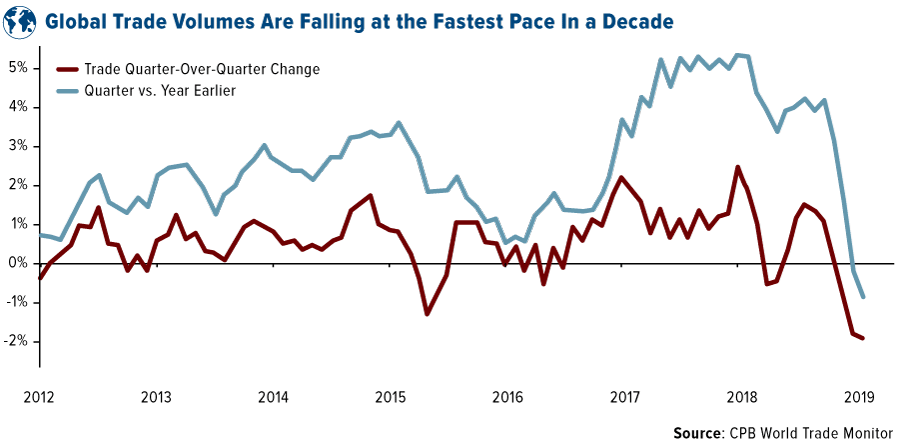

- The worst performing major commodity for the week was palm oil, which fell 4.51 percent on rising stockpiles and weakness in soybean oil. Copper traders and analysts were split on their price outlooks for the red metal this week in the Bloomberg survey, as markets await China PMI data that will be released next week. World trade volumes are plummeting at their fastest pace in a decade as calculated by Bloomberg using Dutch statistics on trade flows. Oil prices fell this week, breaking seven consecutive weeks of gains. BHP Group CEO Andrew Mackenzie said that the company will not make further investments in its thermal coal unit, but that there are no plans to exit the business. Bloomberg reports that Mackenzie said coal is expected to remain a part of the energy mix for several decades, even as demand is unlikely to rise at the same rate as gas and renewables.

- Hitachi Construction Machinery, which is Asia’s second largest maker of mining and building equipment, announced this week that it forecasts profits to fall 30 percent on concerns about demand from China and Europe. The company said in a statement that demand for hydraulic excavators used in construction is set to fall, but that demand for super large dump trucks used in mining will likely increase. Freeport-McMoRan reported first quarter earnings per share that missed the average analyst estimate, as did Eni on its adjusted net, reports Bloomberg.

- JPMorgan downgraded Anglo American to neutral after holding an overweight view for almost three years. Shares of the company fell as much as 2.6 percent in London on the news out Wednesday. Goldman Sachs also said that they see a scope for underperformance in the mining sector. Glencore PLC is facing a new corruption investigation with the Commodity Futures Trading Commission (CFTC), this following the opening of an investigation last year by the Department of Justice.

Opportunities

- Brent crude oil went rising toward $75 per barrel in London on Monday after President Trump’s administration announced that waivers for Iran oil will not be renewed when they expire on May 2. The news increased fears of oil shortages and escalating military tensions in the Gulf. Oil has already climbed nearly 40 percent in 2019 as OPEC has reduced production. The oil cartel said that Saudi Arabia will coordinate with other producers to ensure that adequate supplies will be available in the market once the Iran waivers end.

- Tesla said it is targeting a battery pack for its driverless taxi service that would last for 1 million miles, reports Bloomberg. The ambitious target is 10 times the current mileage for a Tesla Model 3. Ford Motor will be investing $500 million in Rivian Automotive, an electric truck maker, which Amazon.com has backed with an investment announced in February.

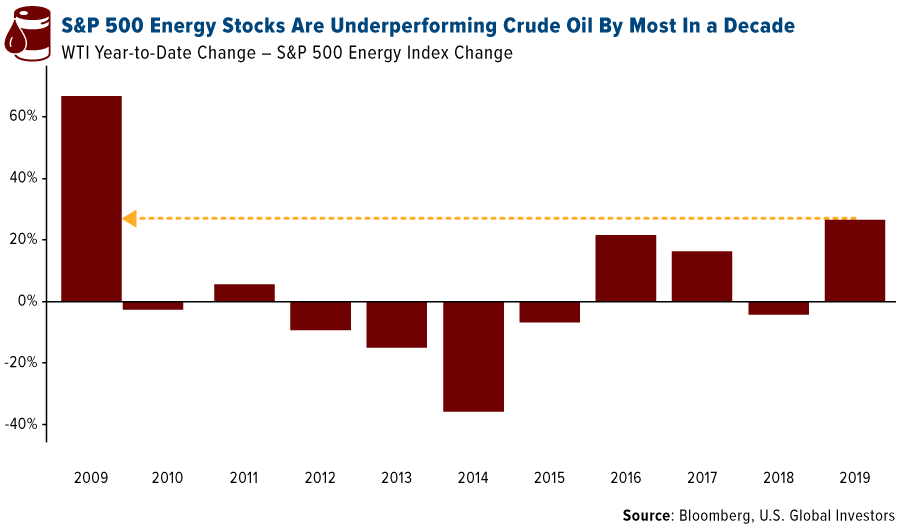

- Bloomberg data shows that the performance gap between U.S. crude oil and S&P 500 energy stocks is at its widest since 2009. This leaves a big opportunity for the oil companies to catch up to rallying oil. With the bidding war breaking out over Anadarko Petroleum after years of cost cutting, the world’s largest oil companies may once again be poised to invest in new resources. Haliburton Co. said U.S. oilfield-service prices have hit bottom and that it expects demand to improve. CEO Jeff Miller said it’s a first quarter earnings statement that they “believe the worst in the pricing deterioration is now behind us.”

Threats

- Although it could be an opportunity for oil to rally further, the U.S. ending Iran waivers might also be a threat by increasing geopolitical risks. Asian nations such as China, Japan, South Korea and India are some of the biggest buyers of Iranian oil and they will be tasked with either finding a new source for imports or defying the U.S. and continuing to buy from Iran anyway. Oil exports from Russia into Europe were halted by the end of week as their oil was found to be contaminated with organic chlorides which if refined would convert to hydrochloric acid and subsequently damage the refinery. Russian trade serendipity at its best when Iranian supplies are sanctioned from world markets?

- A lithium-ion battery exploded at an Arizona Public Service Co. substation last week. This news adds to growing concern over battery fires and explosions. According to BloombergNEF, at least 21 fires have already occurred at battery projects in South Korea.

- China’s largest maker of electric vehicle batteries, Contemporary Amperex Technology Co. Ltd., warned that competition will intensify to capture the growing market as the government reins in subsidies. Umicore SA fell the most ever on Monday after the company warned that profits will miss analyst expectations due to slowing demand for electric vehicles in China. Albermarle subsequently fell on the news as Umicore is one of its biggest customers.

Emerging Europe

Strengths

- Romania was the best performing country this week, gaining 80 basis points. The Bucharest stock exchange was closed on Friday as the country celebrates Easter, according to the Orthodox Church. OMV Petrom, Romanian oil and gas producer, gained almost 4 percent, contributing the most to the country’s outperformance. OMV Petrom shareholders approved its 2019 budget and the company announced a slightly higher dividend payout.

- The euro was the best relative performing currency this week, losing 80 basis points against the U.S. dollar. The dollar reached a new 52-week high, pushing the euro and other emerging European currencies lower. In fact, this week the euro traded at the lowest since 2017, and its downtrend could continue if the dollar continues moving higher, supported by upbeat economic data and outperformance of U.S. equites.

- Consumer staples was the best performing sector among eastern European markets this week.

Weaknesses

- Turkey was the worst performing country this week, losing 2.2 percent. Rising oil prices have a negative impact on Turkey’s economy, as the country is a net importer of oil. Turkey will continue to import oil from Iran despite President Trump removing waivers that allowed eight counties, including Turkey, to import oil from Iran.

- The Turkish lira was the worst performing currency this week, losing 2.2 percent against the U.S. dollar. As expected, the central bank left its main rate unchanged at 24 percent, but policymakers removed the hawkish rate pledge from its prior statement.

- Industrials was the worst performing sector among eastern European markets this week.

Opportunities

- Emerging market equities have recovered almost all of last year’s losses, but Franklin Templeton Emerging Markets Equity expects gains have farther to go. Chief Investment Officer for Franklin Templeton, Manraj Sekhon, believes emerging market companies will significantly increase their free cash flow over the next few years, which should allow an increase in dividend payouts and stocks buybacks.

- A few weeks ago, Turkey announced economic reforms in hopes of stimulating its troubled economy and weakening currency. This week the government injected 3.3 billion euros ($3.7 billion) into five state-owned banks to boost the banks’ capital and credit growth. A market stability fund within the government-controlled investor bought debt issued by the lenders under a recapitalization program announced Monday, reports Bloomberg. While some steps have been taken to bring the economy out of recession, even more may need to be taken.

- Next week’s final purchasing managers’ index (PMI) reading for the eurozone will be released, and most analysts predict the final number will confirm a small pick-up from March’s 47.5. Moreover, according to Bloomberg economists, euro-area inflation will improve in April as well. CPI is expected to rise to 1.5 percent with core inflation at 1 percent. Economic data and growth prospects in the eurozone may have hit a bottom and could be due for a rebound.

Threats

- Vladimir Putin signed a decree offering Russian passports to people living in breakaway regions of eastern Ukraine. This move may prompt western nations to impose additional sanctions against Moscow. Moreover, Putin’s announcement comes during a transition time in Ukraine. Volodymyr Zelenskiy secured 75 percent of votes in the second round of presidential elections last weekend, beating his opponent, former president of Ukraine Petro Poroshenko, by a wide margin. Zelenskiy is a popular actor, with little political experience.

- Europe’s oil refineries have stopped taking piped deliveries of Russian oil due to contamination. The piped oil has become tainted by organic chlorides that, when refined, become hydrochloric acid that can damage the plans. Pumping through a section of the Druzhba pipeline into central and eastern Europe came to a halt, cutting off the main source of oil supply to central and eastern Europe.

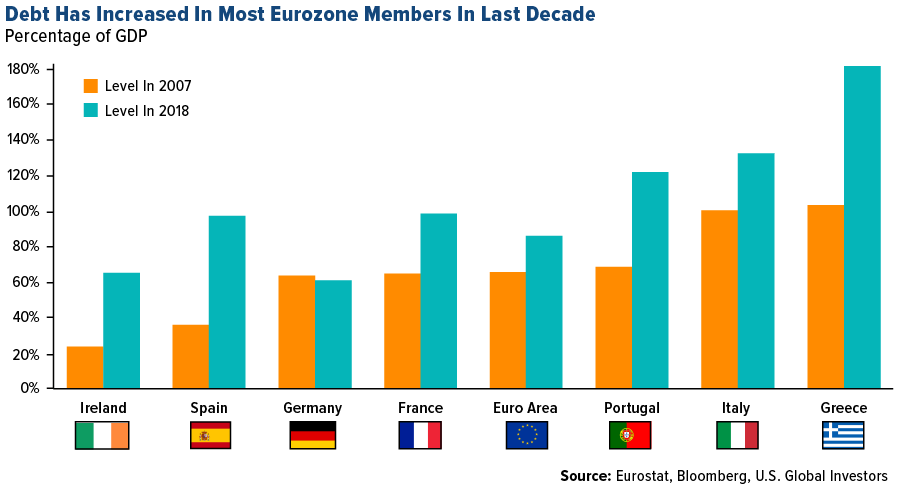

- Debt-ratio of euro-area governments may have fallen in 2018 from a year earlier, but they are still substantially higher than before the 2008 financial crisis. Eleven euro-zone countries had debt rations higher than 60 percent of GDP – the European Union ceiling. Greece, Italy and Portugal have the largest debt to GDP ratios.

China Region

Strengths

- The Philippines’ PCOMP rose 64 basis points in total return for the week, reopening this week after being closed the last two days of the prior week for holidays, while Malaysia’s FTSE Bursa Malaysia Kuala Lumpur Composite climbed 1.02 percent. Vietnam’s Ho Chi Minh Stock Index rose by 1.41 percent this week.

- Utilities was the best-performing sector in Hong Kong’s Hang Seng Composite Index for the week, and the only one to stay green in that time, rising by 12 basis points.

- Domestic vehicle sales in Vietnam jumped to a 44.9 percent year-over-year level, rebounding from the prior reading and reaching the fastest pace of growth in more than two years.

Weaknesses

- The Shanghai Composite fell 5.63 percent for the week, weakest in the region.

- Materials was the worst-performing sector in Hong Kong’s Hang Seng Composite Index for the week, falling 5.41 percent since last Thursday in a holiday-shortened trading week.

- Singapore’s industrial production declined 4.8 percent year-over-year for the March period, missing analysts’ estimates and dropping down from last month’s pace of 0.7 percent growth year over year. South Korea’s preliminary first quarter GDP readings also missed, coming in at only a 1.8 percent pace of growth year-over-year, well below the 2.4 percent analysts were expecting.

Opportunities

- U.S.-China trade talks remain ongoing, with more positive commentary and hints at a deal and confirmation of high-level talks on the schedule in the coming weeks in both Beijing and Washington. The Trump administration is floating the idea of U.S. concessions on the pharma side, while China’s Xi indicated—in a prominent late-week speech at China’s Belt and Road forum in Beijing—that reforms are set to continue, that the yuan will not be devalued competitively, and that more foreign ownership will be permitted—all part of U.S. demands in trade talks. The relatively positive tones, recent hints at a possible summit and the confirmed scheduling of the next round of back-and-forth trade talks are all likely positive indications that the U.S. and China may well be closing in on something that could pass muster for some sort of signing summit or ceremony.

- Luckin Coffee filed this week for a U.S. IPO as hinted at in past media reports. The fast-growing, up-and-coming chall enger to Starbucks is building stores at a furious pace, although Luckin notably lags far behind Starbucks in market share. Starbucks, which dominates China’s share, entered the massive Chinese market more than 20 years ago. Luckin, which partners with Tencent Holdings on deliveries and which also offers cashless, fast pick-up outlets, is looking to take advantage of the possibilities for further growth in Chinese coffee consumption. As the Wall Street Journal reported earlier in the year, “Annual coffee consumption per capita in China is roughly five to six cups per household, compared with the more than 300 cups per capita consumed by Americans annually.”

- China’s President Xi Jinping indicated at the Belt and Road forum this week that China will seek to focus increasingly upon financial sustainability of the vast infrastructure and trade network that is the Belt and Road Initiative (BRI).

Threats

- U.S.-China trade talks remain ongoing and tariffs remain delayed in implementation; a collapse of the former or the commencement of the latter remain a collective threat until resolution one way or the other amid the dispute. Once again, this is seeming less and less likely, given the positive signaling that appears to be coming from both the United States and China of late, but there remain a couple of pertinent threats to mind: first, the out-and-out collapse of the talks (again, seemingly less likely), and second, a perception by markets that the deal may be one in form but less so in substance.

- Higher oil prices may weigh on significant importers like Indonesia and India in particular, although President Donald Trump has reportedly been pressuring OPEC to lower prices. China, India, and South Korea have all enjoyed waivers on Iranian crude to date.

- The U.S. dollar remains strong and made new 52-week highs this year, which could conceivably pose a threat to emerging markets.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended April 26 was Neuro, up 170.84 percent.

- A notable bull cross, or a “golden crossover,” of key moving averages has formed for the first time in nearly four years, reports CoinDesk, with bitcoin moving to five-month highs on Tuesday. The crossover of the 50- and 200-day moving averages represents a long-term bearish-to-bullish trend change, although the rally could be preceded by consolidation or price pullback.

- Bitcoin spenders now have the ability to shop on e-commerce websites such as Amazon using the lightning network, reports CoinDesk. Crypto payment processing startup Moon announced this week that through its browser extension, any lightning-enabled wallet can now also be used. Moon CEO Ken Kruger told CoinDesk that by 2020, the lightning-enabled feature should work on almost any e-commerce site, regardless of whether that platform accepts bitcoin directly.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended April 26 was Bitcoin File, down 59.93 percent.

- Coinbase announced the closing of its Chicago office, known as Coinbase Markets, which was dedicated to creating sophisticated electronic markets technologies, reports CoinDesk. This high-speed trading division of the cryptocurrency exchange will be consolidated to match the similar engine work being done by the team in San Francisco. Thirty engineering jobs will be eliminated in the shutdown.

- The billionaire founder of SoftBank Group Corp., Masayoshi Son, reportedly lost $130 million on a bitcoin bet, reads a MarketWatch headline this week. Son made an enormous personal bet on the popular digital currency in late 2017. “Bitcoin peaked at nearly $20,000 in mid-December 2017, and Mr. Son sold in early 2018 after bitcoin had plummeted,” the article reads.

Opportunities

- Although it started with selling beer, age verification could unlock a whole industry to cryptocurrency, CoinDesk reports. Civic demonstrated its beer-selling machinery during this year’s South by Southwest (SXSW) in Austin, TX, and now the company has announced partnership with 12 major automated retail companies to bring similar technology to the masses, the article continues. Now Civic expects this blockchain technology to be used in 1,000 machines by the end of the year.

- Citing a person “familiar with Samsung’s internal situation,” an exclusive CoinDesk Korea report says that the electronics giant is developing its own Ethereum-based blockchain network. The report continues on to explain that when the development of the blockchain is completed, Samsung may also move to launch a “Samsung Coin” token.

- Thanks to France’s latest law on cryptocurrency, blockchain-related projects have the right to a bank account as long as they agree to appropriate regulation, reports CoinDesk. Under the new law, now the burden lies on banks to explain why they won’t serve startups, explains Domitille Dessertine, head of financial technology, innovation and competitiveness at AMF (the country’s financial markets overseer).

Threats

- The Santa Clara County’s District Attorney’s Office announced Monday that a 21-year old student from the U.S., Joel Ortiz, who stole over $7.5 million in cryptocurrency has been sentenced to 10 years in prison, reports CoinDesk. Ortiz stole the digital currency via SIM-swapping hacks, and at one point hacked the cellphones of at least 40 individuals. In fact, one crime in May 2018, say Ortiz steal more than $5.2 million “in minutes” from a crypto entrepreneur in Cupertino, California, the article continues.

- John, McAfee, the eccentric antivirus pioneer known for his brushes with the law, as Bloomberg describes him, says that he has spoken with the creator of bitcoin Satoshi Nakamoto and plans to reveal the person’s identity. McAfee originally told Bloomberg that he would expose Nakamoto “within a week,” but has since backed off of the plan, explaining on Twitter that this controversy could hurt his efforts to fight an extradition to the U.S.

- Despite bitcoin’s rally earlier this week to five-month highs and a golden crossover, short-term technical indicators are suggesting a drop in prices before the rally picks up pace again, writes CoinDesk. A bearish divergence on the relative strength index (RSI) in particular is pointing to the possible pullback. The RSI is widely considered an early sign of trend change and has yielded notable price reversals in the past.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| S&P/TSX Global Gold Index | 186.52 | -0.11 | -0.06% |

| Gold Futures | 1,288.10 | +12.10 | +0.95% |

| Natural Gas Futures | 2.57 | +0.08 | +3.05% |

| S&P/TSX VENTURE COMP IDX | 610.69 | +1.48 | +0.24% |

| 10-Yr Treasury Bond | 2.50 | -0.06 | -2.34% |

| Nasdaq | 8,146.40 | +148.34 | +1.85% |

| Oil Futures | 62.80 | -1.20 | -1.88% |

| Hang Seng Composite Index | 3,963.86 | -67.53 | -1.68% |

| S&P 500 | 2,939.88 | +34.85 | +1.20% |

| DJIA | 26,543.33 | -16.21 | -0.06% |

| Korean KOSPI Index | 2,179.31 | -36.84 | -1.66% |

| Russell 2000 | 1,591.82 | +26.07 | +1.66% |

| S&P Energy | 490.47 | -6.41 | -1.29% |

| S&P Basic Materials | 357.37 | -4.63 | -1.28% |

| XAU | 72.65 | -0.24 | -0.33% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.57 | -0.15 | -5.42% |

| S&P/TSX Global Gold Index | 186.52 | -15.49 | -7.67% |

| 10-Yr Treasury Bond | 2.50 | +0.13 | +5.62% |

| Oil Futures | 62.80 | +3.39 | +5.71% |

| Gold Futures | 1,288.10 | -28.80 | -2.19% |

| S&P 500 | 2,939.88 | +134.51 | +4.79% |

| S&P Energy | 490.47 | +2.08 | +0.43% |

| Hang Seng Composite Index | 3,963.86 | +111.51 | +2.89% |

| DJIA | 26,543.33 | +917.74 | +3.58% |

| Korean KOSPI Index | 2,179.31 | +33.69 | +1.57% |

| Nasdaq | 8,146.40 | +503.02 | +6.58% |

| S&P Basic Materials | 357.37 | +15.95 | +4.67% |

| Russell 2000 | 1,591.82 | +69.59 | +4.57% |

| S&P/TSX VENTURE COMP IDX | 610.69 | -15.61 | -2.49% |

| XAU | 72.65 | -5.86 | -7.46% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.57 | -0.53 | -17.20% |

| 10-Yr Treasury Bond | 2.50 | -0.22 | -7.95% |

| DJIA | 26,543.33 | +1,990.09 | +8.11% |

| Oil Futures | 62.80 | +9.67 | +18.20% |

| S&P 500 | 2,939.88 | +297.55 | +11.26% |

| Gold Futures | 1,288.10 | -4.20 | -0.33% |

| S&P Energy | 490.47 | +31.21 | +6.80% |

| Nasdaq | 8,146.40 | +1,072.94 | +15.17% |

| Korean KOSPI Index | 2,179.31 | +34.28 | +1.60% |

| S&P Basic Materials | 357.37 | +30.92 | +9.47% |

| Russell 2000 | 1,591.82 | +127.41 | +8.70% |

| Hang Seng Composite Index | 3,963.86 | +358.34 | +9.94% |

| S&P/TSX Global Gold Index | 186.52 | +9.61 | +5.43% |

| S&P/TSX VENTURE COMP IDX | 610.69 | +17.31 | +2.92% |

| XAU | 72.65 | +4.08 | +5.95% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (03/31/2019):

Eni SpA

BHP Group Ltd

Anglo American Plc

OMV Petrom SA

Starbucks Corp

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry.

The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks.

The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months.

The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange.

The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver.

The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar.

The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500.

The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500.

The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period.

The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500.

The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500.

The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500.

The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500.

The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500.

The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500.

The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns.

The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

There is no guarantee that the issuers of any securities will declare dividends in the future or that, if declared, will remain at current levels or increase over time.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500.

Free Cash Flow (FCF) represents the cash that a company is able to generate after laying out the money required to maintain or expand its asset base.

The relative strength index is a technical indicator used in the analysis of financial markets. It is intended to chart the current and historical strength or weakness of a stock or market based on the closing prices of a recent trading period.

The University of Michigan Consumer Sentiment Index is a consumer confidence index published monthly by the University of Michigan. The index is normalized to have a value of 100 in December 1966. Each month at least 500 telephone interviews are conducted of a contiguous United States sample.

The German Ifo Business Climate Index rates the current German business climateand measures expectations for the next six months. It is a composite index based on a survey of manufacturers, builders, wholesalers and retailers. The index is compiled by the Ifo Institute for Economic Research.

A basis point is one hundredth of one percent, used chiefly in expressing differences of interest rates.

The SIFMA Municipal Swap index is a 7-day high-grade market index comprised of tax-exempt VRDOs reset rates that are reported to the Municipal Securities Rule Making Board’s (MSRB’s) SHORT reporting system. The index is calculated on an actual/actual basis and is published every Wednesday by 4 p.m. Eastern Time.

A bond’s credit quality is determined by private independent rating agencies such as Standard & Poor’s, Moody’s and Fitch. Credit quality designations range from high (AAA to AA) to medium (A to BBB) to low (BB, B, CCC, CC to C).

The Philippine Stock Exchange Index is a capitalization-weighted index composed of stocks representative of the Industrial, Properties, Services, Holding Firms, Financial and Mining & Oil Sectors of the PSE.

The FTSE Bursa Malaysia Kuala Lumpur Composite comprises the largest 30 companies by full market capitalization that meet stated eligibility requirements.

The Vietnam Stock Index or VN-Index is a capitalization-weighted index of all the companies listed on the Ho Chi Minh City Stock Exchange.