Are All Your Ducks in a Row? Positioning Your Portfolio for the Market’s Next Move

Date Posted: August 23, 2019

Read time: 51 min

If you've paid any kind of attention to recent market headlines, you've surely seen the term "recession" among the most prominent topics in your newsfeed.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

If you’ve paid any kind of attention to recent market headlines, you’ve surely seen the term “recession” among the most prominent topics in your newsfeed. This shouldn’t come as a shock, either—the global growth picture isn’t as rosy as it could be.

Take a look at Germany. There are wide indications that the world’s fourth largest economy is heading into a recession, with its GDP shrinking in the second quarter and its 10-year bond hitting a record-low negative yield. Some analysts warn that U.S. investors should be alert due to a potential spillover effect.

Then there’s the purchasing managers’ index (PMI), a forward-looking indicator I write about often. Right now, PMIs are falling around the world. In July, the U.S. Manufacturing PMI was 50.4, its lowest reading since September 2009. Thursday’s August “flash,” or preliminary, reading for the IHS Markit U.S. Manufacturing PMI dropped even lower, coming in at 49.9, indicating contraction. According to Morningstar, this is the first time in nearly a decade that the reading declined below the neutral reading mark of 50.0.

White House Bifurcates on Recession Risks

President Donald Trump and his economic advisors have been sharing their thoughts on whether or not a recession could be making landfall in the near future. Trump says the U.S. economy is “doing really well,” and on Sunday, economic adviser Larry Kudlow downplayed signs that a recession is in the works.

White House economic adviser Larry Kudlow does not see a recession.

Photo by: Gage Skidmore | Attribution-ShareAlike 3.0 Unported (CC BY-SA 3.0)

Kudlow’s comments are notable here due to his questionable record of forecasting economic pullbacks. Before the 2007-2008 financial crisis, for example, he wrote: “There’s no recession coming. The pessimists were wrong. It’s not going to happen…”

We’ll have to wait and see if he’s gotten any better at making these types of calls. But if you remember, Kudlow was wrong about gold during most of its incredible run-up in the 2000s.

Although the White House insists there isn’t problem, certain actions are telling a different story.

Trump has made it clear to Federal Reserve Chair Jerome Powell that he believes interest rate cuts should be made more aggressively; Trump has delayed imposing additional tariffs on goods imported from China until after the Christmas shopping season; and the White House is even weighing whether to cut payroll taxes.

Awaiting Thoughts from Jackson Hole

The Fed and the European Central Bank (ECB) released minutes from their recent policy meetings this week, but all eyes have been fixed on Powell’s speech at the annual and much-anticipated Jackson Hole symposium, happening this Friday and into the weekend.

At the symposium, central bankers will meet and discuss what can be done, monetarily, to keep the world economy on track.

On Friday, Powell said that the U.S. economy is close to both goals of price stability and full employment, and that he will act appropriately to sustain the expansion. He did, however, comment that the global economic outlook is deteriorating, talking specifically at length regarding tariffs and trade wars.

Certainly after today’s announcement from China regarding new tariffs on $75 billion worth of U.S. goods, many including a variety of agriculture and commodity-focused products, we’re curious to learn what comes out of the full weekend of discussions. In conversing over the news with analysts in Canada today, for example, some ponder whether this direct hit to the farm belt was done to sway opinions against the U.S. President. Stay tuned…

What I Learned at Camp Kotok – John Mauldin Recaps Diverse Economic Gathering

|

On the topic of Jackson Hole, I am reminded of an interesting piece written recently by my good friend of 30 years, John Mauldin. In his newsletter, Thoughts from the Frontline, he discussed “What I Learned at Camp Kotok,” an annual fishing trip in Maine and quite a contrasting event from what is taking place in Wyoming this weekend.

While the bankers meet at Jackson Hole, Mauldin says Camp Kotok was a “meeting of wickedly smart people focused on economics and markets.”

This year’s conversations focused on three key long-term themes which were discussed one by one: 1) A future where global interest rates remain permanently near zero; 2) Modern Monetary Theory and U.S. fiscal policy; and 3) A fundamental change in the U.S./China relationship.

Mauldin shared his observations on the diverse group of opinions at Camp Kotok, noting that, in general, the group agreed the tariffs were having a global impact, slowing growth elsewhere. However, nearly everyone was glad Trump is pushing back on China, (but agreed perhaps he should do it in another way).

I highly encourage you to read the full article here. Whether you agree with thoughts from Jackson Hole or thoughts shared during this fishing trip, it’s worth your time to consider every opinion.

Expect the Best, Prepare for the Worst

The powers that be are all working on ways to prevent, or at least lessen, the effects of a recession, whether that is fiscally (President Trump and Congress) or monetarily (the Federal Reserve). Government policy is a precursor to change, after all, so it’s important to follow these decisions closely.

I encourage you to consider what you will be doing in the event of a pullback. How will you prepare your portfolio?

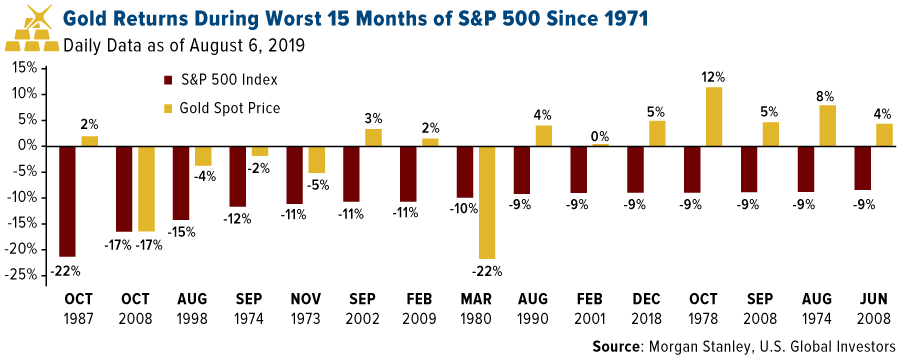

As I’ve written about many times, gold has traditionally been a good hedge in times of economic instability. The chart below is a perfect illustration of how gold can benefit your portfolio during a market downturn.

I continue to advocate for the 10 Percent Golden Rule of having 5 percent in physical gold or beautiful gold jewelry, and 5 percent in well managed gold mutual funds or ETFs, rebalancing quarterly.

What’s Next for Gold?

Last week I said to buy gold in the dips, after witnessing the yellow metal soar above $1,500 an ounce for the first time since September 2013. With gold up two-and-a-half standard deviations, the theory of mean reversion says it will be due for a correction. Indeed, it’s receded somewhat from its 52-week high of close to $1,550, though it’s still above $1,500.

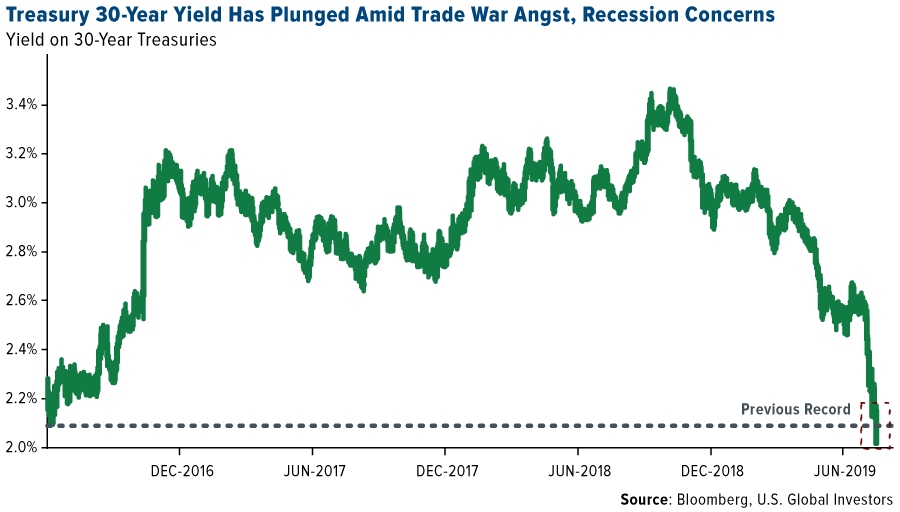

As you can see in the chart below, gold looked overbought and began to correct at the start of the week. On Wednesday, however, the yellow metal rose 1 percent on news that an additional inversion in the U.S. Treasury yield curve occurred. Unfavorable economic data out of the eurozone also continued to push for its haven appeal.

Despite gold’s dip from last week’s six-year high, billionaire hedge fund manager Mark Mobius reaffirmed his bullish outlook for the yellow metal on Tuesday in a Bloomberg interview.

“Gold’s long-term prospect is up, up and up, and the reason why I say that is money supply is up, up and up,” Mobius explained. “I think you have to be buying at any level, frankly.”

Mobius isn’t the only one with gold on the brain. Interestingly enough, we’ve seen a spike in traffic to our gold-themed pages since the start of 2019. In particular, visits to our gold-focused ETF page from January have jumped over 200 percent from this same time frame in 2018, (also, a spike in airline-related and travel content).

The yellow metal is top of mind for many investors and I believe this will continue to be the case.

Want to learn more about gold and how it could benefit your portfolio? Subscribe to my award-winning blog by clicking here!

Gold Market

This week spot gold closed at $1,536.40, up $12.80 per ounce, or 0.84 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 2.96 percent. The S&P/TSX Venture Index came in up 1.88 percent. The U.S. Trade-Weighted Dollar fell 0.44 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Aug-19 | EC CPI Core YoY | 0.90% | 0.90% | 0.90% |

| Aug-22 | US Initial Jobless Claims | 216k | 209k | 220k |

| Aug-23 | US New Home Sales | 647k | 635k | 646k |

| Aug-26 | US Durable Goods Orders | 1.10% | — | 1.90% |

| Aug-26 | HK Exports YoY | -9.40% | — | -9.00% |

| Aug-27 | US Conf. Board Consumer Confidence | 130 | — | 135.7 |

| Aug-29 | GE CPI YoY | 1.50% | — | 1.70% |

| Aug-29 | US Initial Jobless Claims | 215k | — | 209k |

| Aug-29 | US GDP Annualized QoQ | 2.00% | — | 2.10% |

| Aug-30 | EC CPI Core YoY | 1.00% | — | 0.90% |

Strengths

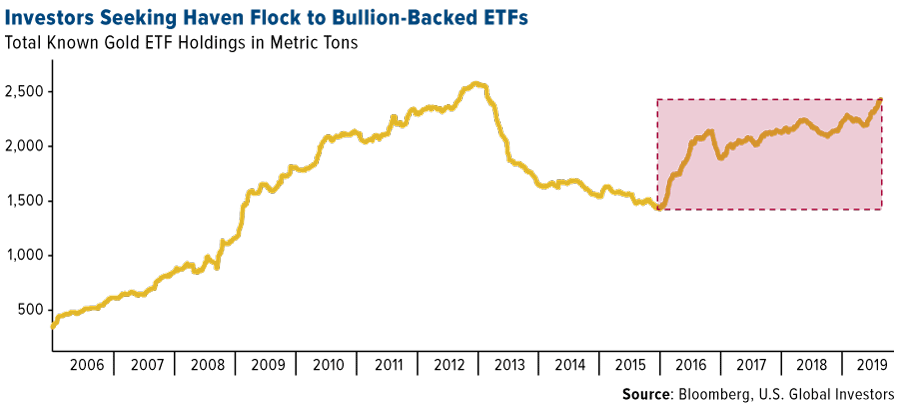

- The best performing metal this week was silver, up 2.03 percent. Gold came in second place, up 1 percent. Inflows into ETFs backed by gold have hit 1,000 metric tons since holdings bottomed in early 2016. Bloomberg data shows that total known ETF holdings rose to 2,424.9 tons on Wednesday, which is the highest since 2013. Goldman Sachs predicts that the price of the yellow metal will climb to $1,600 an ounce over the next six months.

- Gold prices were up sharply on Friday morning after China announced retaliatory tariffs on $75 billion in American goods. The escalating trade war creates geopolitical uncertainty, which often translates to greater demand for safe haven assets like gold and bonds. On Thursday, gold saw a small bounce when U.S. PMI data for August declined to 49.9, below the level that separates growth from contraction.

- Veteran investor and founder of Mobius Capital Partners LLP, Mark Mobius, gave gold a big endorsement on Bloomberg TV this week. Mobius said “I think you have to be buying at any level” and that “gold’s long-term prospect is up, up and up” due to rising money supply. Another believer of the yellow metal? A Sandler Capital Management hedge fund that is known as one of the top performers this year, reports Kitco News. The fund has $2.1 billion in assets and just made gold its top holding by increasing its investment in the SPDR Gold Trust by 180 percent.

Weaknesses

- The worst performing metal this week was palladium, which was still up 0.88 percent. Higher gold prices and a bad monsoon season are weighing on the gold demand outlook in India, the world’s second largest consumer, ahead of festival season when buying usually peaks. Bloomberg reports that demand for jewelry grew 9 percent in the January to June period, but high taxes, record prices and slowing economic growth are likely to counteract.

- Kitco News reports that Wells Fargo is cautioning investors from buying too much gold. According to a note by John LaForge, head of real asset strategy, gold is one of the best assets to own in times of economic uncertainty, but that most investors don’t understand it and could buy too much as prices hover around $1,500. Wells Fargo sees gold ending the year around $1,400 to $1,500 as the economy stabilizes.

- BN Americas reports that production from the 10 biggest gold miners in Mexico fell in the second quarter due to declining reserves, technical challenges and lower grades. The top 10 miners produced 675,450 ounces of gold in the second quarter, compared to 709,385 ounces in the same period last year.

Opportunities

- Russian President Vladimir Putin signed a law removing the 20 percent value-added tax (VAT) on investments in gold and other precious metals, reports Kitco News. Russian newspaper Izvestia predicts that demand for precious metals in the next five years could surge 50 tonnes a year – an increase of 15 times current levels. The Russian central bank continues to be a big buyer of bullion, purchasing 300,000 ounces in July.

- A Texas woman visiting Arkansas’s Crater of Diamond State Park found a 3.72 carat yellow diamond this week. The park reports that this is the largest registered diamond found since March 2017 and the largest yellow diamond found since 2013. The 37-acre park is one of the only places in the world that visitors can search for real diamonds.

- Dan Oliver, founder of Myrmikan Capital, told The Street in an interview this week that “there’s a lot of pressure into gold, and we’ve just barely begun this cycle.” Oliver noted that once gold broke above $1,350 an ounce, institutional investors began to pay more attention, including Ray Dalio. Oliver added that breaching that level was the first step for gold to climb to $3,000.

Threats

- Growing trade tensions and global economic uncertainty continue to rile markets. In a speech at Jackson Hole Friday morning, Federal Reserve Chairman Jerome Powell said “the global growth outlook has been deteriorating since the middle of last year. Trade policy uncertainty seems to be playing a role in the global slowdown and in weak manufacturing and capital spending in the United States.”

- A special feature in CNN this week highlighted how “bloody” gold continues to support the troubled Venezuelan government and economy. General Manuel Crisopher Figuera, the former head of Venezuela’s intelligence service, told CNN that “just like the blood diamonds [in Africa], the gold that is being extracted from Venezuela, outside of any protocol, is bloody gold.” The nation has the world’s largest oil reserves and some gold reserves of its own. The feature describes how workers face treacherous conditions to mine gold for the government without regulations or safety concerns. President Maduro has been able to sell some of its gold reserves in recent months that had pushed global prices down.

- Georgette Boele, senior FX and precious metals strategist at ABN AMRO, expects silver prices to decline in the near term and further deterioration in global growth and trade, reports FX Street. “If the global economy and global trade slow further (we don’t expect a recession), this will weigh on silver demand and the outlook for silver prices. In addition, we expect profit taking in gold prices and this should also drag silver prices lower.”

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 0.99 percent. The S&P 500 Stock Index fell 1.44 percent, while the Nasdaq Composite fell 1.83 percent. The Russell 2000 small capitalization index lost 2.28 percent this week.

- The Hang Seng Composite gained 1.73 percent this week; while Taiwan was up 1.12 percent and the KOSPI rose 1.10 percent.

- The 10-year Treasury bond yield fell 3 basis points to 1.527 percent.

Domestic Equity Market

Strengths

- Utilities was the best performing sector of the week, increasing by 0.22 percent versus an overall decrease of 1.29 percent for the S&P 500.

- Target was the best performing stock for the week, increasing 23.00 percent.

- Shares in Peppa Pig’s owner jumped 30 percent after Hasbro’s $4 billion offer. The transatlantic deal gives Hasbro, which has seen growth with Marvel’s "Avengers" toys, access to Entertainment One’s lucrative infant and preschool market.

Weaknesses

- Materials was the worst performing sector for the week, decreasing by 3.03 percent versus an overall decrease of 1.29 percent for the S&P 500.

- L Brands was the worst performing stock for the week, falling 13.90 percent.

- Macy’s was downgraded to neutral from buy at Guggenheim, which wrote that its analysts “no longer see the secular headwinds facing the company abating.” The stock fell under $15 at its low of the session, and is trading at its lowest level since September 2009. Macy’s has dropped 60 percent from a November peak.

Opportunities

- Salesforce.com Inc. shares rallied on Friday after the company reported second quarter results that beat expectations. The maker of cloud-based applications also gave a revenue forecast that was ahead of estimates, reassuring investors that it would continue to see rapid growth.

- Target beat Wall Street estimates for quarterly same-store sales on Wednesday. The retailer benefited from higher online sales and an increase in shoppers at its stores, sending shares up 5 percent in pre-market trading.

- Cargojet Inc., a Canadian cargo carrier, soared to a record high after Amazon.com Inc. signed a deal that would allow the online retailer to buy a stake in the carrier.

Threats

- Representatives from as many as a dozen states met with Department of Justice officials to discuss a multi-state effort to investigate big tech companies like Facebook and Google. The states may announce their own, but coordinated, investigations as early as next month, the Wall Street Journal reports. Additionally, two U.S. lawmakers have called on a top financial regulatory panel to consider direct oversight of the cloud services big tech companies provide to banks. Katie Porter and Nydia Velázquez said Amazon Web Services, Microsoft Azure and Google Cloud should be considered systemically important like payment and settlement services.

- Three Federal Reserve policy makers voiced their resistance to the notion that the U.S. economy needs lower interest rates, and a fourth said he wanted to avoid taking further action “unless we have to,” foreshadowing a sharp debate with officials who want to cut rates again. Investors have fully priced a quarter percentage-point reduction at the Fed’s September 17-18 policy meeting, but dissenting Fed voices may limit the prospects for the larger move that some have advocated, including President Trump.

- Semiconductor and auto companies, such as Apple, fell sharply on Friday as the trade war between the U.S. and China continued to escalate. China’s Ministry of Finance said the country plans to levy retaliatory tariffs on another $75 billion of American goods.

The Economy and Bond Market

Strengths

- The Conference Board Leading Economic Index for the U.S. increased 0.5 percent in July to 112.2, following a 0.1 percent decline in June. "The U.S. LEI increased in July, following back-to-back modest declines. Housing permits, unemployment insurance claims, stock prices and the Leading Credit Index were the major drivers of the improvement," said Ataman Ozyildirim, Senior Director of Economic Research at The Conference Board.

- Sales of previously owned U.S. homes increased in July to a five-month high, writes Bloomberg, underscoring stability in the residential real estate market that may be starting to get a boost from falling borrowing costs. Contract closings rose 2.5 percent to a 5.42 million annual rate, the National Association of Realtors said Wednesday.

- The number of Americans filing applications for unemployment benefits fell sharply last week, reports CNBC, suggesting the labor market was holding firm despite a manufacturing slowdown. Initial claims for state unemployment benefits dropped 12,000 to a seasonally adjusted 209,000 for the week ended August 17, the Labor Department said on Thursday.

Weaknesses

- U.S. factory activity contracted in August for the first time since September 2009 as new orders shrank, according to Fortune. The IHS Markit manufacturing purchasing managers’ index (PMI) slipped to 49.9 from a final July reading of 50.4, according to a preliminary August report. Factory employment stagnated on the heels of weaker orders and subdued output.

- U.S. consumer expectations fell to a five-month low in August as fears of an economic downturn and stock market volatility weighed on sentiment, reports Bloomberg. The Bloomberg Consumer Comfort Index’s monthly expectations gauge fell to 48.5 from 55 as a larger share of respondents said the economy is getting worse, according to the Aug. 6-18 survey released Thursday.

- Sales of new U.S. single-family homes sank more than expected in July, writes Reuters, a sign that the housing market continued in low gear despite lower mortgage rates and a strong labor market. The Commerce Department reported new home sales dropped 12.8 percent to a seasonally adjusted annual rate of 635,000 units last month. It was the biggest monthly decline since July 2013.

Opportunities

- The second estimate of U.S. GDP for the second quarter will hit the markets on Thursday.

- U.S. personal income and spending data, as well as the core PCE Price Index for July will all be released next Friday.

- The U.S. and Japan are holding trade talks, and a deal could settle shaky markets. Americans want to export more beef and pork to Japan, while the Japanese want to avoid upcoming automobile tariffs.

Threats

- The U.S. budget deficit is growing faster than expected and President Trump’s trade war is weighing on the economy, according to a new Congressional Budget Office forecast that highlights key challenges ahead of the 2020 elections. The shortfall is set to widen to $1 trillion by fiscal year 2020, Bloomberg writes, two years earlier than previously estimated, according to the non-partisan group’s annual budget outlook released Wednesday.

- China’s currency just dropped to its lowest level in a decade. U.S. exporters are expected to feel the brunt as goods become more expensive to sell to China.

- A ‘hard Brexit’ could have massive consequences for global air travel. Though there had been concerns that flights would be grounded as soon as the UK left the bloc, interim agreements would prevent that in the short term, though most are yet to be agreed.

Energy and Natural Resources Market

Strengths

- The best performing major commodity for the week was palm oil, which gained 3.13 percent. Palm oil is the benefit of Chinese sanctions on American soybeans. Palm oil can be used as a substitute for soybean oil, which is derived from soybeans. China’s soybean imports fell 11 percent in the first seven months of this year, due to the tariff on American imports of the beans. China’s palm oil consumption rose more than 20 percent in the same period because of its price advantage, reports Bloomberg.

- Two LNG terminals are running again, boosting demand and giving a place for all the natural gas to go. BloombergNEF reports that two terminals in Texas have ramped up and are almost back to levels seen before maintenance began early this month. Demand for LNG exports hit an all-time high of 6.4 billion cubic feet on Wednesday. The demand jump is a “catch-up” to the rout of overproduction in early August.

- According to Goldman Sachs Group Inc., profits from turning crude into diesel in the second half of 2019 are forecast to be 31 percent higher than the first six months of the year. Margins have expanded around 40 percent since late April as the International Maritime Organization prohibits ships from using dirty fuel starting January 1. This should boost diesel demand.

Weaknesses

- The worst performing major commodity for the week was cotton, which fell 3.51 percent. China hit back with retaliatory tariffs against the U.S. on Thursday sending markets and commodities down. The additional tariffs on $75 billion of American goods will take effect in two stages in September and December and goods hit include soybeans, automobiles and oil. A five percent tariff will be applied to imported U.S. oil, which sent WTI futures in New York falling 3.1 percent and turned a weekly gain into a 1.82 percent loss.

- Adding to the poor oil outlook, Russia set its budget with the lowest breakeven oil price in over a decade. The highly oil-dependent economy’s budget balanced oil at $49 per barrel this year, demonstrating that it isn’t taking any chances due to additional sanction fears and general global uncertainty that could drive prices lower.

- Reuters reports that Chile-based SQM, the world’s number two producer of lithium, saw its quarterly earnings fall by nearly half due to a slump in prices for the battery metal even as volumes grew by 14 percent. Largely in line with analyst expectations, profits sank by 47.5 percent.

Opportunities

- Bloomberg reports that Kazatomprom, the world’s largest uranium miner, will extend its production cuts through 2021 due to market oversupply and low prices. BMO analyst Alexander Pearce says that the extension is likely to support prices, helping uranium miners overall.

- It could be bargain time in the LNG market after prices have plunged to their lowest on record for this time of year, writes Bloomberg. Traders from Japan to India have started buying cargoes in anticipation of winter demand. Sanford C. Bernstein & Co. analysts wrote in a report that “we have likely reached bottom.”

- Bloomberg’s David Fickling writes that major miners agree that copper has a bright future, but the trouble is how to get to that point. Even when the red metal is trading near a three-year low of $2.61 per pound, mining is still profitable. Fickling adds that “there ought to be interesting opportunities for M&A in the current environment” with capped production, lower prices and growing demand for renewables.

Threats

- Private financing for coal-fired power plant projects in India dropped by 90 percent in 2018, while government-owned banks still issued loans, according to the Center for Financial Accountability. Bloomberg Law’s Lou Del Bello writes that this demonstrates how coal investments have become toxic for many as the world increasingly moves toward renewables. BHP Group CEO Andrew Mackenzie says that global efforts to cut carbon emissions mean that there is weaker long-term demand for thermal coal.

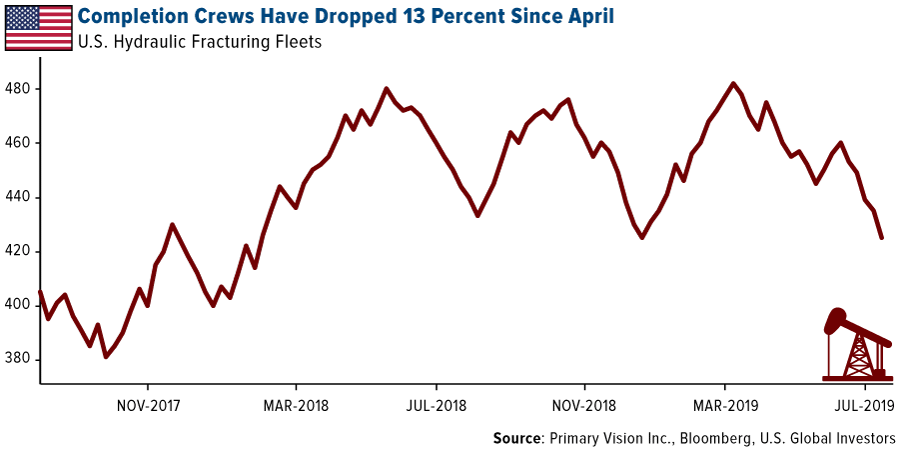

- According to data from Primary Vision Inc., the number of crews completing wells has dropped 13 percent from its peak in April. Between now and the end of the year, this figure could drop another 15 percent as spending cuts from oil and natural gas explorers flows through to oilfield-service providers, says Brad Handler, an analysts at Jefferies LLC. Bloomberg writes that frackers suffer from the advent of new electric-powered pumps.

- Bloomberg Law reports that at least 10 cities nationwide face elevated levels of lead in drinking water that have exceeded the EPA’s lead limit in each of the past two years. The levels are close to that of Newark, New Jersey, where the city was forced to take the extreme measure of providing residents with bottled water.

Emerging Europe

Strengths

- Greece was the best performing country this week, gaining 5 percent. Banks bounced back with Piraeus Bank gaining 18.3 percent in the past five days and National Bank of Greece gaining 16.2 percent. After years of economic crisis, Greece continues to apply reforms, restore credibility and attract foreign investments.

- The Russian ruble was the best performing currency this week, gaining 70 basis points against the U.S. dollar. At the beginning of the week, the ruble strengthened with the price of oil. However, on Friday China announced additional tariffs on $75 billion of U.S. goods, including an extra 5 percent tariff on American crude oil. The price of Brent crude dropped by 1.4 percent on Friday, but for the week oil still finished in the positive territory, gaining 82 basis points.

- Energy was the best performing sector among eastern European markets this week.

Weaknesses

- Hungary was the worst performing country this week, losing 1.2 percent. It was a short week for the stocks trading on the Budapest exchange with the market closed Monday and Tuesday. MOL, a Hungarian oil and gas producer and distributor, was the weakest equity, losing 4 percent.

- The Turkish lira was the worst performing currency in the region this week, losing 3.3 percent against the U.S. dollar. The lira came under pressure after gaining 11 percent in the past three months. Further prospects of rate cuts in Turkey may push the currency lower against the U.S. dollar.

- Industrial was the worst performing sector among eastern European markets this week.

Opportunities

- The market value of Pandora, a Danish jewelry maker that produces more jewelry than any other company in the world, jumped $1 billion in one day after the company reported better than expected second quarter earnings. Shares of the company hit a six-year low last month, but the brand relaunch under a new CEO may turn the company around. This week a few analysts raised their price estimates. Pandora’s CEO has purchased 49,568 shares for DKK 12.3 million and the CFO purchased 24,400 shares worth DKK 6 million.

- There was more optimism in Europe this week over the U.K. reaching a deal with Europe before the October 31 Brexit deadline. Leaders from the U.K., Germany and France agreed to work toward a deal. However, the UK’s Boris Johnson once again pointed out that for the deal to happen the EU previsions aimed at preventing a hard border of Ireland will have to go – or Britain will leave the bloc without an agreement. The British pound soared on the news.

- Minutes from the most recent meeting of the European Central Bank (ECB) suggest that the bank favors a large package of stimulus being announced at once, instead of gradual stimulus being applied. No details were provided, but the bank’s minutes revealed that rate cuts and asset purchase plans can be reintroduced as soon as September.

Threats

- The Italian Prime Minister resigned on Tuesday, after Matteo Salvini’s far-right League party withdraw its support for the government, creating political uncertainty. It is not clear if a new government can be formed without the country holding a snap election. However, if Italy holds early elections, Salvini’s far right, anti-immigration and Eurosceptic League party could win the outright majority in parliament.

- Three democratically elected mayors from the main southeastern municipalities in Tukey were removed and accused of supporting terrorism. Many observers see this as further attempts by the government to fight opposition and a violation of voters’ rights. It is the second time that elected mayors in the southeastern part of the country have been removed and replaced with Ankara appointees.

- Barclays forecasts a no-deal Brexit will result in a mild recession in the U.K. next year and predict two rate cuts, with one this year and one in 2020. The bank also cut its euro-area growth outlook to 0.6 percent from 1 percent.

China Region

Strengths

- The best performing index in the region for the week was the Shanghai Composite, which climbed 2.63 percent on the week (granted, prior to President Trump’s late-Friday announcement of new tariff hikes), while Hong Kong’s Hang Seng Composite climbed 2.31 percent.

- The best performing sector in Hong Kong’s Hang Seng Composite Index was consumer goods, which gained 6.25 percent.

- Taiwan’s year-over-year export orders declined by less than expected, dropping only 3.0 percent, below an expected drop of 5.9 percent and up from the prior reading of -4.5 percent.

Weaknesses

- The worst performing indices in the region for the week were India’s Nifty and Sensex Indices, which fell 1.92 percent and 1.71 percent, respectively. Jakarta’s JCI dropped 49 basis points.

- The poorest performing sector in Hong Kong’s Hang Seng Composite Index this week was utilities, which declined by 2 basis points amid positive week for the Index.

- Thailand’s quarter-over-quarter, second-quarter GDP reading missed expectations slightly, coming in at a gain of only 0.6 percent, below estimates of 0.7 percent and down from the prior reading of 1.0 percent.

Opportunities

- It remains possible that the recent announcements of a very real U.S.-China trade war escalation could somehow bring the two sides to the table in search of a deal, which may, after all, simply be a part of the negotiating ploys between the sides. Obviously given the size and scale of the two major economies, any reprieve in the trade war could swing sentiment in a major way as well. There remains some time left before the new escalation is set to kick in, and while it does seem increasingly likely that both sides are attempting to put some teeth into their talks, talks reportedly remain scheduled for September.

- One upside of ongoing uncertainty on the trade situation remains opportunities created by shifting supply chains, like we’ve highlighted in Vietnam or Taiwan.

- Another upside of negative sentiment and selling may be valuation. Hong Kong’s blue chip Hang Seng Index now trades at a P/E ratio of 10.20.

Threats

- In keeping with what remains a very real threat, we again reiterate that trade war escalation remains a threat until it isn’t. China announced on Friday that it plans to impose additional tariffs on some $75 billion of U.S. imports, including on soy beans and crude oil, as well as resume tariff hikes on U.S. auto imports beginning in December. China is thus attempting to match the scheduled timeline that President Trump announced of U.S. tariff hikes on Chinese imports for September and December. Again, talks are reportedly still scheduled for September as top advisor Larry Kudlow reminded us yesterday after what he said was a “very productive” call. And as of late afternoon Friday, President Trump announced the new 10 percent levy would go to 15 percent, and the existing tariffs on $250 billion of goods already in effect will rise to 30 percent beginning in October. Bear in mind that September has not yet happened, and of course neither has October nor December, so all of this remains very much a schedule of hikes, which have been postponed or modified before. Of course, both sides now also appear to be digging in their heels. Is this all the art of the deal? Perhaps. But both sides are nonetheless raising the rhetoric—and the scheduled levies on imports—in the meantime.

- Once again, unrest continues in Hong Kong, which could perpetuate negative sentiment and attention. While we would note it appears to be more positive and peaceful protesting this week in an about-face from some of the recent weeks, still the protests go on without an immediate resolution. Protesters appear to have rejected a move from HK CEO Carrie Lam to meet, several large corporations have voiced concerns over the lack of resolution, and U.S. media outlets from Twitter to YouTube shut down hundreds of accounts, posts, and videos that appear to have been backed or directed by the mainland in HK for purposes of misinformation.

- A Bloomberg survey of economists suggests that the “new tariffs that President Donald Trump has threatened on $300 billion of Chinese goods would drag China’s annual economic growth below 6 percent … [to] the slowest expansion since 1990,” the results of the poll suggested. And as of last writing, the President announced that 10 percent levy would be hiked to 15.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended August 23 was Swace, up 218.96 percent.

- Cryptocurrency trading platform Bakkt, launched by the Intercontinental Exchange (ICE) is finally opening for business after nearly a year of delays, reports Decrypt. It has received approval from the Commodity Futures Trading Commission (CFTC) and the New York State Department of Financial Services to launch in late September. Crypto analyst and trader Scott Melker says the news is “arguably the most bullish event for institutional investors in the history of bitcoin.”

- A VC-based blockchain firm that helped curate courses as Harvard, Oxford and Cambridge is officially rolling out its programs at three California universities, writes CoinDesk. MouseBelt’s Blockchain Accelerator, backed by over $40 million in funding from NueValue Capital, launched Wednesday at UC Davis, UC Los Angeles and UC Santa Barbara.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended August 23 was BitBall, down 73.29 percent.

- Local hydropower plants and bitcoin miners in China’s Sichuan province have been forced to halt operations after a prolonged rainstorm has caused land- and mudslides in the region, reports CoinDesk. The mudflows have disrupted local power supply and communications infrastructure, a China Daily report explained, and have also resulted in at least seven deaths.

- On Wednesday, the White House issued two advisories on drug purchases in the U.S., reports CoinDesk, using the communications to make specific references to the role of cryptocurrencies in such transactions. “Convertible virtual currencies” can be and have been used for illicit substance purchases on the clear, deep and dark nets, the article continues. Specifically noted is the drug fentanyl, which is 80 to 100 times stronger than morphine, according to the Drug Enforcement Agency.

Opportunities

- MasterCard, who recently partnered with Facebook on its Libra cryptocurrency, is now putting together its own crypto team, writes MarketWatch. According to analyst Ted Rossman with CreditCards.com, MasterCard is making the move because “it wants to be known as more than a card company; it wants to be a technology company.” In a recruitment listing, the company says those hired for the new team will “monitor cryptocurrency ecosystem trends” and “develop new products and solutions,” the article continues.

- Commonwealth Bank of Australia has partnered up with BioDiversity Solutions Australia to co-develop a blockchain marketplace that could support sustainable development while rewarding landowners for protecting the environment. According to the article on CoinDesk, the prototype platform uses digital tokens, dubbed BioTokens, to facilitate trading of biodiversity credits for the New South Wales Government’s Biodiversity Offsets Scheme.

- Sometimes blockchain technology is used for entertainment purposes. Popular U.S. beer brand Miller Lite has teamed up with a blockchain marketing company for the latest iteration of its “Know Your Beer” program, reports CoinDesk. Vatom Labs built a mobile “edutainment game” serving a 12-question quiz to cellphones, geo-targeting customers in over 230,000 bars and restaurants across the U.S.

Threats

- According to project creator Vitalik Buterin, the increased cost of transacting on the ethereum blockchain is hurting the software’s adoption, reports CoinDesk. Buterin told the Toronto Star this week that projects considering whether to build on the technology will likely be butted out as the blockchain is overloaded with transactions, or as he called it “almost full.” In other crypto news this week, Bank of England governor Mark Carney laid out a radical proposal for an overhaul of the global financial system that would eventually replace the dollar as the reserve currency, reports Bloomberg. It’s replacement? A Libra-like virtual one.

- A document obtained by Bloomberg suggests that Facebook’s Libra cryptocurrency is already facing a probe by the European Union (EU), reports CoinDesk. According to the report, the European Commission is “currently investigating potential anti-competitive behavior” by the Libra Association. The Commission is also concerned that Libra could give rise to “possible competition restrictions” on the use of information including user data, the article continues.

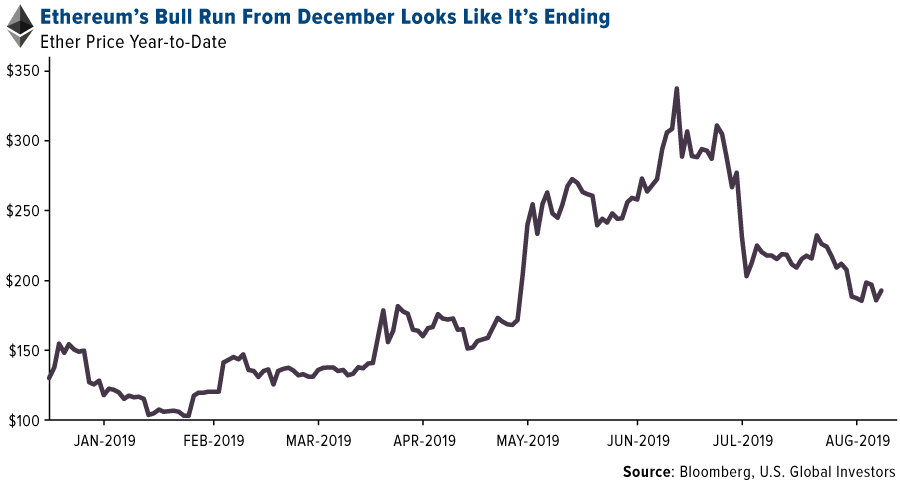

- Ether’s losing altitude, writes CoinDesk, with signs suggesting that the asset has ended a bull market from December lows with a drop below $200 last week. Mid-week, the second-largest cryptocurrency by market cap was trading at $183 on Bitfinex, which shows a 7.3 percent drop on a 24-hour basis.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| S&P/TSX Global Gold Index | 260.33 | +11.44 | +4.60% |

| Gold Futures | 1,536.40 | +12.80 | +0.84% |

| Natural Gas Futures | 2.16 | -0.04 | -1.95% |

| S&P/TSX VENTURE COMP IDX | 581.13 | +10.70 | +1.88% |

| 10-Yr Treasury Bond | 1.53 | -0.03 | -1.80% |

| Nasdaq | 7,751.77 | -144.23 | -1.83% |

| Oil Futures | 53.90 | -0.97 | -1.77% |

| Hang Seng Composite Index | 3,516.50 | +79.32 | +2.31% |

| S&P 500 | 2,847.20 | -41.48 | -1.44% |

| DJIA | 25,628.90 | -257.11 | -0.99% |

| Korean KOSPI Index | 1,948.30 | +21.13 | +1.10% |

| Russell 2000 | 1,459.52 | -34.12 | -2.28% |

| S&P Energy | 410.68 | -8.35 | -1.99% |

| S&P Basic Materials | 343.54 | -10.80 | -3.05% |

| XAU | 97.78 | +4.94 | +5.32% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.16 | -0.06 | -2.84% |

| S&P/TSX Global Gold Index | 260.33 | +21.09 | +8.82% |

| 10-Yr Treasury Bond | 1.53 | -0.52 | -25.33% |

| Oil Futures | 53.90 | -1.98 | -3.54% |

| Gold Futures | 1,536.40 | +99.90 | +6.95% |

| S&P 500 | 2,847.20 | -172.36 | -5.71% |

| S&P Energy | 410.68 | -58.53 | -12.47% |

| Hang Seng Composite Index | 3,516.50 | -277.37 | -7.31% |

| DJIA | 25,628.90 | -1,641.07 | -6.02% |

| Korean KOSPI Index | 1,948.30 | -134.00 | -6.44% |

| Nasdaq | 7,751.77 | -569.73 | -6.85% |

| S&P Basic Materials | 343.54 | -29.30 | -7.86% |

| Russell 2000 | 1,459.52 | -120.90 | -7.65% |

| S&P/TSX VENTURE COMP IDX | 581.13 | -12.02 | -2.03% |

| XAU | 97.78 | +4.85 | +5.22% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.16 | -0.42 | -16.33% |

| 10-Yr Treasury Bond | 1.53 | -0.79 | -34.15% |

| DJIA | 25,628.90 | +138.43 | +0.54% |

| Oil Futures | 53.90 | -4.01 | -6.92% |

| S&P 500 | 2,847.20 | +24.96 | +0.88% |

| Gold Futures | 1,536.40 | +233.70 | +17.94% |

| S&P Energy | 410.68 | -40.85 | -9.05% |

| Nasdaq | 7,751.77 | +123.48 | +1.62% |

| Korean KOSPI Index | 1,948.30 | -111.29 | -5.40% |

| S&P Basic Materials | 343.54 | +8.88 | +2.65% |

| Russell 2000 | 1,459.52 | -41.86 | -2.79% |

| Hang Seng Composite Index | 3,516.50 | -94.54 | -2.62% |

| S&P/TSX Global Gold Index | 260.33 | +80.78 | +44.99% |

| S&P/TSX VENTURE COMP IDX | 581.13 | -20.89 | -3.47% |

| XAU | 97.78 | +31.57 | +47.68% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (06/30/2019):

BHP Group Ltd.

SPDR Gold Shares

National Bank of Greece SA

MOL Hungarian Oil & Gas PLC

Pandora A/S

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

M2 Money Supply is a broad measure of money supply that includes M1 in addition to all time-related deposits, savings deposits, and non-institutional money-market funds. Standard deviation is a measure of the dispersion of a set of data from its mean. The more spread apart the data, the higher the deviation. Standard deviation is also known as historical volatility. The Conference Board index of leading economic indicators is an index published monthly by the Conference Board used to predict the direction of the economy’s movements in the months to come. The index is made up of 10 economic components, whose changes tend to precede changes in the overall economy. The Bloomberg Consumer Comfort Index is a weekly, random-sample survey tracking Americans’ views on the condition of the U.S. economy, their personal finances and the buying climate. The "core" PCE price index is defined as personal consumption expenditures (PCE) prices excluding food and energy prices.