Bitcoin Is “Right Where Oil Was in 1890”

Date Posted: May 15, 2020

Read time: 54 min

NULL

U.S. Global Investors Reports Financial Results for the Third Quarter of 2020 Fiscal Year

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

This week I was honored to participate in the first virtual Consensus cryptocurrency conference, hosted by CoinDesk. In years past, the annual gathering—attended by the world’s biggest crypto and blockchain companies, experts, entrepreneurs and investors—has been held in New York, but in an effort to curb the spread of the coronavirus, everything was moved online.

I was impressed with CoinDesk’s ability to adapt to unforeseen circumstances, and I want to thank them for the opportunity to participate.

No doubt many were disappointed to lose the in-person Consensus experience this year, but I believe it may have turned out for the better. Attendees were able to listen in to every panel and seminar for free, and from the safety of their own homes. This potentially allowed speakers’ thoughts and ideas to reach even more crypto investors than it otherwise would have. You can watch the replay by clicking here.

Paul Tudor Jones Adds Bitcoin to His Portfolio

One of this week’s biggest reveals from last week is that billionaire hedge fund manager Paul Tudor Jones became among the first institutional investors to take a stake in bitcoin, the largest digital currency by market cap, as a hedge against inflation sparked by massive money-printing.

Jones told clients that bitcoin reminds him of gold in the late 1970s when consumers prices began to go off the rails. Adjusted for inflation, the price of gold actually peaked not in 2011, but in 1980.

“The best profit-maximizing strategy is to own the fastest horse,” Jones wrote. “If I am forced to forecast, my best is it will be bitcoin.”

The 65-year-old money manager remains a fan of gold, by the way, predicting the metal could rally to $2,400 an ounce and possibly $6,700 “if we went back to the 1980 extremes.”

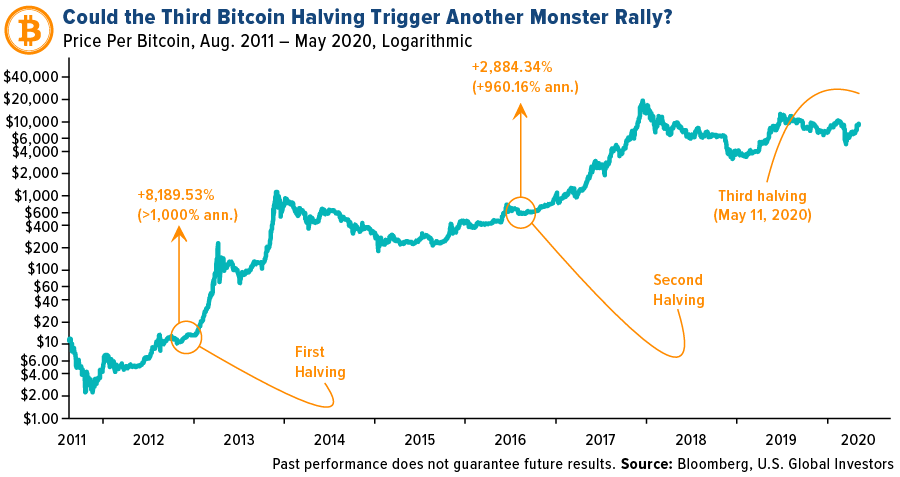

Third Bitcoin Halving Occurred This Week

Another big topic of discussion was the bitcoin halving that took place on Monday. This is only the third such halving in bitcoin’s 11-year history, the first occurring in November 2012, the second in July 2016.

In case you’re unfamiliar with the term, a “halving” is an artificial, preprogrammed means to control the supply of bitcoin. It “pumps the brakes” on the issuance and circulation of new units of the cryptocurrency.

Before the halving, crypto miners were rewarded with 12.5 bitcoin every time their powerful network of computers solved a complex math problem. Today, though, that reward has been cut in half to 6.25 bitcoin.

The next halving will limit the reward to only 3.125 bitcoin, and so on, until all 21 million bitcoin are mined. As of Thursday, about 18.4 million bitcoin were in circulation, according to Blockchain.com, meaning there’s only 2.6 million remaining up for grabs.

Act Fast, Supply Is Limited!

So what happens now? To answer that, I think it’s helpful to remember that bitcoin is like any other asset, in that it responds to the dynamics of supply and demand.

West Texas Intermediate (WTI) crude hit $140 per barrel in June 2008 when it was believed that oil exploration had peaked. But the U.S. fracking industry changed the game, allowing crude to be extracted from areas that were previously unattainable. Global oil prices collapsed in 2014 as U.S. production ramped up, and today WTI is trading just under $30 per barrel, about 80 percent off its record high.

Gold prices, as I’ve explained before, have benefited from the fact that we’re close to exhausting the world’s gold deposits, or at least those that can be feasibly developed using current mining technology. Short of a breakthrough in a similar “fracking” process, producers are looking at increasingly less reward in mineral output for the time, money and effort that they spend digging the metal out of the ground.

Sound familiar? It should, because bitcoin prices have followed the same trajectory.

In the months following the first and second halvings, bitcoin prices surged as it became abundantly clear that at some point in the near future, new bitcoin issuances will come to a halt. Time will tell if the same will happen this time, but I’m very bullish.

Just Like Oil in 1890?

That’s just the supply side. What about the demand side? If few to no people have any use for or interest in an asset, then it doesn’t have much value.

Conversely, the more people that use something, the greater its value has generally become. In economics, this is what’s known as Metcalfe’s Law. Consider oil in the 19th century. Humans had been aware of and indeed using raw petroleum for centuries, but it wasn’t until the advent of the automobile that the scramble for “black gold” really began, making some early oil barons like John D. Rockefeller incredibly wealthy.

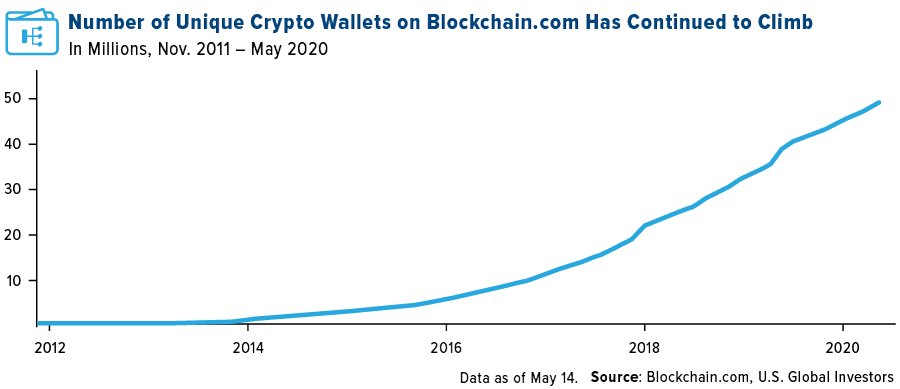

Again, bitcoin—and cryptocurrency as a whole—is no different. It’s a nascent industry, but we’re seeing more and more users are finding their way into digital currencies, which raises the total value. According to Blockchain.com data, just under 50 million unique crypto wallets have been created as of May 2020, a change of 10 million from just a year earlier.

“We’re right where oil was in 1890,” commented Alex Leigl, CEO of Layer1, during our panel discussion on Monday.

The analogy is a compelling one. It suggests not only that we’re at the forefront of something new and bold, but that there could be many years of maturation and innovation ahead of us.

What an exciting time to be an investor!

Gold Market

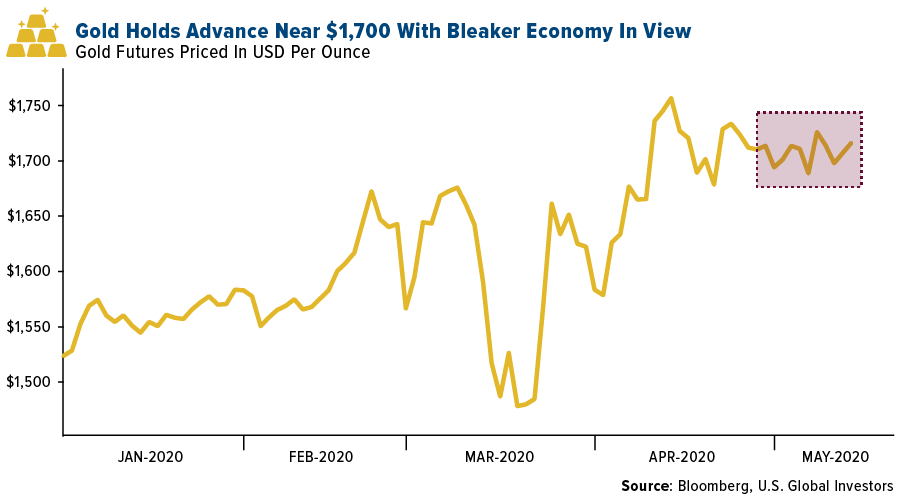

This week spot gold closed at $1,743.67, up $40.97 per ounce, or 2.41 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 4.37 percent. The S&P/TSX Venture Index came in up 3.39 percent. The U.S. Trade-Weighted Dollar rose 0.65 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| May-12 | CPI YoY | 0.4% | 0.3% | 1.5% |

| May-13 | PPI Final Demand YoY | -0.4% | -1.2% | 0.7% |

| May-14 | Germany CPI YoY | 0.8% | 0.9% | 0.8% |

| May-14 | Initial Jobless Claims | 2500k | 2981k | 3176k |

| May-14 | China Retail Sales | -6.0% | -7.5% | -15.8% |

| May-19 | Germany ZEW Survey Expectations | 32.0 | — | 28.2 |

| May-19 | Germany ZEW Current Situation | -88.6 | — | -91.5 |

| May-19 | Housing Starts | 929k | — | 1216k |

| May-20 | Eurozone CPI Core YoY | 0.9% | — | 0.9% |

| May-21 | Initial Jobless Claims | 2400k | — | 2981k |

Strengths

- The best performing precious metal was silver, up 7.30 percent. Gold had a strong week and held above $1,700 an ounce. Bullion rose the most in a week on Wednesday after Fed Chairman Jerome Powell said that the U.S. economy is facing unprecedented downside risks that could do lasting damage. Powell pushed legislators to take more action to support the economy. The possibility of negative interest rates and continued near-zero rates is supportive for the yellow metal. By the end of the week bullion was holding near $1,750 an ounce. Goldman Sachs’ global head of commodities Jeffrey Currie said in a Bloomberg TV interview this week that gold is his favorite commodity trade right now. “There are a lot of reasons to still hold gold. Foremost is that you are still seeing the debasement effects of all the stimulus measures.”

- Everyone knows the FANG stocks – Facebook, Amazon, Netflix and Google. But do they also know the BANG stocks – Barrick Gold, Agnico Eagle, Newmont and Goldcorp. Axios notes that these big gold miners have dwarfed the returns of the major tech companies. Since early May 2018, BANG stocks have nearly tripled the gain of FANG stocks, reports Jesse Felder of the Felder Report.

- The World Gold Council (WGC) expects the number of central banks buying gold to increase substantially in 2020. Bloomberg reports that based on the recent WGC survey, 20 percent of central banks intend to boost gold reserves over the next 12 months. This is up from just 8 percent of respondents in a 2019 poll. 22 central banks were net buyers of gold in 2019, up from only 8 in 2010.

Weaknesses

- The worst performing precious metal was palladium, down 0.54 percent. Norilsk Nickel, the world’s biggest palladium producer, said in a report this week that it expects consumption of the metal to fall 16 percent in 2020. Palladium prices have fallen by a third since hitting a record high in late February. The coronavirus crisis prompted automakers to curb output and the metal’s rise was in large part due to increased use in autocatalysts.

- First Majestic announced that it temporarily postponed the sale of 292,000 ounces of silver and 700 ounces of gold worth $5.3 million at the end of the first quarter, reports Bloomberg. The company will carry over inventory to next quarter in hopes that prices will improve. “We temporarily suspended our silver and gold sales as paper prices dropped significantly below true physical prices,” said CEO Keith Neumeyer.

- S&P Global Market Intelligence wrote in a report that during the past three years there were no major new gold discoveries and in the past decade there were only 25. Kevin Murphy wrote in the report “while there are still plenty of gold assets to be developed, the lack of new major deposits being discovered means that the project pipeline is increasingly short of large, high-quality assets needed to replace aging major gold mines.” Kitco News notes that a major factor in the decline of discoveries is the drastic drop in exploration budgets over the last decade. On the other hand, tighter gold supply could further support higher metal prices and exploration stocks will be bid up in price as they hold the keys to many of our future mines.

Opportunities

- Based on the GTI VERA Convergence Divergence Indicator, which detects trend exhaustion, silver just triggered a buy signal. Bloomberg reports that silver had far underperformed gold and was recently trading at its lowest relative to the yellow metal. However, as economies restart there is growing support for silver’s industrial demand component, according to George Gero, managing director at RBC Wealth Management.

- On Monday, SSR Mining and Alacer Gold Corp announced an at-market merger of equals. The new entity will continue as SSR Mining and will be headquartered in Denver. The new board will be comprised of five directors from each of the current companies’ boards. Paul Benson, President and CEO will step down from SSR Mining and Rod Antal, the current President and CEO of Alacer Gold will be the new leader at SSR Mining. Rod is highly respected for his track record at Alacer and kudos to SSR Mining for preparing for the future versus practicing a protect entrenched management strategy. Despite logistical problems the pandemic has created, M&A is still growing in the gold sector, while broader M&A across the globe has slumped.

- AngloGold announced that it will continue its dividend payments as higher metal prices have boosted the miner’s cash levels. CEO Kelvin Dushinsky said in a conference call that gold prices could rise to higher than $2,000 an ounce. Sibanye Stillwater said it has sufficient cash to weather to coronavirus pandemic after record earnings helped the mine meet its debt target, reports Bloomberg. The South African miner had a strong first quarter due to higher metal prices. CEO Neal Froneman said in a statement that “the group is in a solid financial position.”

Threats

- Although the surge in unemployment and weak economic data is a positive driver for gold, it is still a negative overall. On Thursday the Labor Department reported that 2.98 million Americans filed for weekly unemployment benefits – the fourth straight week of above expected numbers. 36 million American workers have now lost their jobs in just two months. U.S. retail sales fell 16.4 percent in April, following the March decline of 8.3 percent. In a Reuters poll of economists, U.S. GDP is forecast to shrink 35 percent in the second quarter after contracting by 4.8 percent last quarter.

- Billionaire investor Stanley Druckenmiller questions the optimism of a strong “V-shaped” recovery for the global economy. Although equity markets have seen a sharp recovery since bottoming out in March when the world just began to feel the economic impact of the coronavirus, there is doubt it will last, reports Kitco News. Druckenmiller said on a webcast this week that “the risk-reward for equity is maybe as bad as I’ve seen it in my career.”

- The U.S.-China tensions ramped back up this week. In a Fox news interview on Thursday, President Trump said that he was disappointed with China’s failure to contain the coronavirus and said he does not want to speak with President Xi Jinping right now. President Trump even threatened to cut off the relationship entirely: “We could do things. We could cut off the whole relationship.” Undoubtingly, this is a bargaining ploy to gain leverage over China, but the wildcard is the uncertainty this introduces in the meantime, which may lower investor confidence.

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 2.65 percent. The S&P 500 Stock Index fell 2.38 percent, while the Nasdaq Composite fell 1.17 percent. The Russell 2000 small capitalization index lost 5.58 percent this week.

- The Hang Seng Composite lost 0.87 percent this week; while Taiwan was down 0.79 percent and the KOSPI fell 0.95 percent.

- The 10-year Treasury bond yield fell 4 basis points to 0.64 percent.

Domestic Equity Market

Strengths

- Healthcare was the best performing sector of the week, increasing by 0.88 percent versus an overall decrease of 2.64 percent for the S&P 500.

- Nvidia was the best performing S&P 500 stock for the week, increasing 8.68 percent.

- McCormick & Co. was upgraded to outperform from neutral at Credit Suisse. The company will be “the biggest long-term beneficiary” in the food sector from the pandemic, with more at-home cooking for “economic reasons, safety concerns, and health and wellness,” notes the analysts at Credit Suisse.

Weaknesses

- Energy was the worst performing sector for the week, decreasing by 7.61 percent versus an overall decrease of 2.64 percent for the S&P 500.

- Coty was the worst performing S&P 500 stock for the week, falling 36.73 percent.

- Shares of Coty sank this week as investors reacted to a disappointing earnings report along with news that the company was selling a majority stake in its professional beauty business. Revenue in the third quarter fell 23.5 percent to $1.53 billion, due to the impact of COVID-19. Organic sales, which exclude the impact of acquisitions and divestitures, were down 19.5 percent, slightly below analyst estimates at $1.55 billion. In addition, Coty sold a 60 percent stake in its professional beauty and hair-care business to private-equity firm KKR for $4 billion.

Opportunities

- Apple purchased virtual-reality startup NextVR. The virtual reality entertainment market is a high growth area with a global addressable market. The deal may be valued at $100 million.

- Cannabis firm Aurora’s stock jumped 19 percent in pre-market trading on Friday as sales surge during coronavirus.

- Nissan expects equal contributions to global car sales from China, the United States and elsewhere in coming years, reports Reuters, as the struggling Japanese carmaker strategizes to recover profitability, two people with knowledge of the issue said.

Threats

- Companies fear coronavirus liability lawsuits, reports Reuters. So far, few exist. Businesses are urging U.S. lawmakers to shield companies from what they fear could be a flood of lawsuits by workers and consumers, the article reads, blaming employers for exposing them to the new coronavirus.

- Global stocks dropped this week after Fed Chairman Jerome Powell struck a dovish tone during a speech mid-week. Powell cautioned that the pandemic could cause long-term damage to the U.S. economy, warning that "the path ahead is both highly uncertain and subject to significant downside risks."

- The Fiat Chrysler/Peugeot deal is in the spotlight after Exor setbacks, reads one Reuters headline this week. Fiat Chrysler’s decision to scrap its dividend marked another setback for plans by the Agnelli family’s Exor arm to raise cash after a $9 billion sale of its reinsurer unit PartnerRe collapsed this week.

The Economy and Bond Market

Strengths

- The University of Michigan’s consumer sentiment index came in at 73.7 for May – up from 71.8 in April and well above a Dow Jones estimate of 65. “The CARES relief checks improved consumers’ finances and widespread price discounting boosted their buying attitudes,” said Richard Curtin, chief economist for the Surveys of Consumers.

- Home-purchase applications advanced for a fourth straight week and are up more than 33 percent from mid-April, the largest increase since November 2008, Mortgage Bankers Association data showed this week. Buyers are taking advantage of cheap borrowing costs as the average rate on a 30-year fixed mortgage hovers near the lowest level in records going back to 1990.

- Only 2 million of the more than 20 million to lose their job in April indicated their dismissals were permanent, according to Labor Department data. That means that about 18 million Americans on temporary layoff have the potential of returning to work more quickly, provided that their former employers bring them back as the economy re-opens.

Weaknesses

- Consumer spending fell a record 16.4 percent in April – following March’s 8.3 percent dive that already had set a record for data going back to 1992. Some 68 percent of the nation’s $21.5 trillion economy comes from personal consumption expenditures, which tumbled 7.6 percent in the first quarter just as social distancing measures aimed at containing the coronavirus began to take effect.

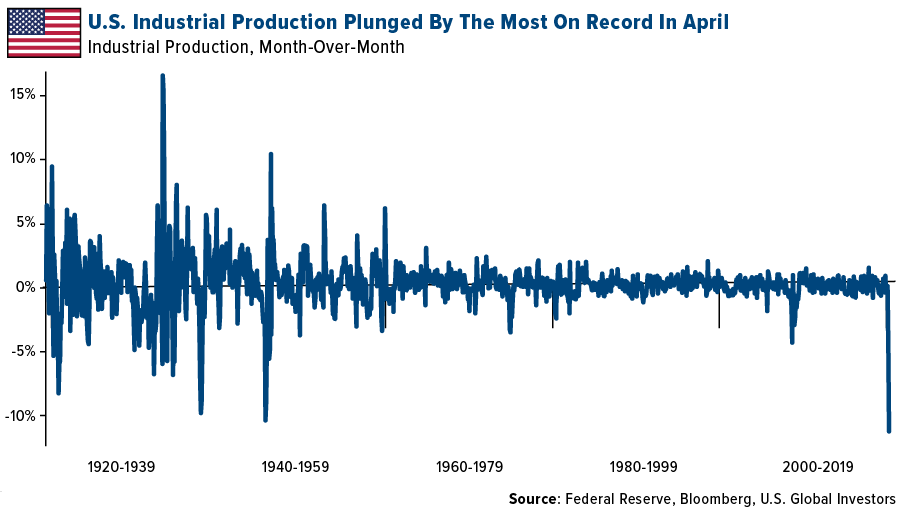

- Industrial production, which includes output at factories, mines and utilities, fell 11.2 percent in April, the steepest monthly drop in the 101-year history of the measure, according to Federal Reserve data released Friday. Manufacturing output plunged by 13.7 percent, also a record.

- Another 2.981 million Americans filed for unemployment benefits in the week ending May 9, surpassing economists’ estimates for 2.5 million jobless claims for the week. The prior week’s figure was revised higher to 3.18 million from the previously reported 3.17 million jobless claims. Over the past two months, more than 36 million Americans have filed unemployment insurance claims.

Opportunities

- Next Thursday will bring the weekly jobless claims and the preliminary Markit PMIs for May. With both seeing disastrous numbers in April, investors will be eager for how May begins to shape up as states begin to reopen.

- The Fed is quietly suggesting more stimulus will be needed from the fiscal side. That was the implied takeaway from Chairman Powell’s comments this week, even though he naturally pledged that the Fed will also do whatever is necessary to aid the recovery.

- The shortest-dated state and local government debt rallied the most since late March as near-zero Treasury yields drove investors to hunt for higher payouts elsewhere. While yields on benchmark municipal securities maturing in a year or less have tumbled, they are yielding about four times higher than those on similar Treasuries.

Threats

- Several states have partially re-opened already, but if one excludes New York from the nationwide numbers, the outbreak elsewhere doesn’t seem to have reached its peak. Opening up too soon could set off second waves of infection and force the U.S. into future shutdowns, derailing an economic recovery.

- U.S.-China relations were already strained before the pandemic, but things have escalated to a new level lately as Trump attempts to pin the blame for the COVID-19 outbreak on Beijing.

- States and cities cut their payrolls by 981,000 to 18.9 million in April, according to the latest U.S. Bureau of Labor Statistics data. The drop, while small compared with the nearly 20 million private sector jobs lost last month, is significant because governments didn’t start laying off employees until well after the onset of the last recession.

Energy and Natural Resources Market

Strengths

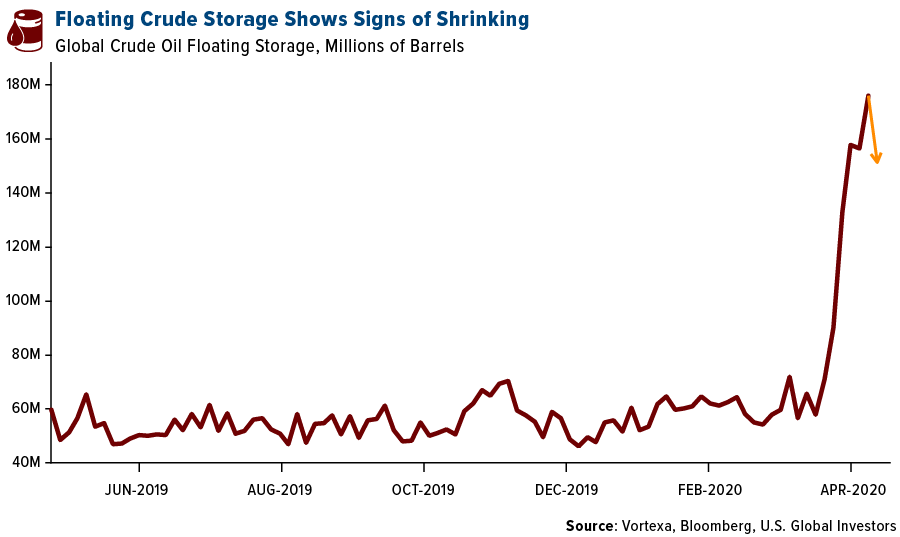

- The best performing major commodity for the week was again crude oil, which gained 19.12 percent. Oil is set for a third weekly gain as demand rebounds and supply cuts take hold. Futures in New York rose as much as 5.8 percent on Friday, reports Bloomberg. Saudi Arabia is planning even deeper oil production cuts. OPEC’s largest producer told Saudi Aramco to cut May production if possible and will cut an extra million barrels a day in June – the lowest level since 2002 according to Bloomberg data. Although a massive supply glut remains, fuel demand is starting to grow in China and India. The amount of crude stored on ships globally is tentatively showing signs of falling, with the amount at 155 million barrels on Thursday, down from 176 million barrels last week. Floating storage is typically the most expensive form of storage and “is likely to fall first and fastest upon any demand strength,” says Jay Maroo, senior analyst at Vortexa.

- Gold has been one of the few strong performers since the pandemic began. Goldman Sachs’ global head of commodities Jeffrey Currie said in a Bloomberg TV interview this week that gold is his favorite commodity trade right now. “There are a lot of reasons to still hold gold. Foremost is that you are still seeing the debasement effects of all the stimulus measures.” The yellow metal had held above $1,700 an ounce and ended the week near $1,750 – nearing its all-time high of $1,900 in 2011.

- Economies are slowly returning to business globally. Peru said that 11 large mines will ramp up production this week following two months of closed operations due to a nationwide quarantine. Electricity production in China increased 0.3 percent in April – an improvement from the 6.8 percent contraction in the first quarter. The Stoxx Europe 600 Basic Resources Index rose as much as 2.1 percent Friday morning after positive economic data was released from China. Factory output increased in April for the first time since the coronavirus outbreak began, boosting base metals, reports Bloomberg.

Weaknesses

- The worst performing major commodity for the week was natural gas, which fell 10.04 percent on milder weather in the Northeast region of the U.S. Oil fell early in the week on fears of a second wave of coronavirus cases hampering the demand recovery. China is now testing every citizen in Wuhan, the original epicenter of the virus, and is locking down cities close to the North Korean border. South Korea also reported an increase in infections, sparking fears of a second wave of the virus. The International Energy Agency (IEA), OPEC and the U.S. Energy Information Administration (EIA) – the three major forecasting agencies – now agree that the world is facing the biggest-ever slump in oil consumption. The IEA predicts the world will use about 1.7 billion barrels less oil in the second quarter than it did during the same period last year, reports Bloomberg. All three agencies do see demand picking up dramatically in the second half of this year. Massive cuts to production have helped stabilize the oil market, but the resurgence in demand is contingent upon governments successfully reopening economies.

- Norilsk Nickel, the world’s biggest palladium producer, said in a report this week that it expects consumption of the metal to fall 16 percent in 2020. Palladium prices have fallen by a third since hitting a record high in late February. The coronavirus crisis prompted automakers to curb output and the metal’s rise was in large part due to increased use in autocatalysts.

- According to Goldman Sachs, the global iron ore market will have a surplus of 4 million tons in 2020 due to higher shipments and lower steel demand outside of China. Bloomberg notes that the previous expectation was for a 30 million ton deficit. The bank sees iron at $70 a ton in the second quarter and that iron’s marginal cost support is around $65.

Opportunities

- Deutsche Bank says that any meaningful copper price pullback is a buying opportunity given tight scrap supply, weak mine supply and strong demand in China, reports Bloomberg. Analysts including Liam Fitzpatrick said in a note this week that demand outside of China for the red metal will gather momentum in the second half of the year. The bank sees prices averaging 5,800 per metric ton in 2021.

- Investments in U.S.-listed commodity ETFs grew 73 percent last week for an eighth straight week of inflows. Bloomberg notes that energy ETFs saw the biggest change from the previous week. Net inflows to ETFs that focus on commodities totaled $2.82 billion in the week ended May 14. Growth in investments is a positive sign that investors are returning to the space after a very rough first quarter for commodity prices.

- Norway’s $1 trillion sovereign wealth fund cut fossil fuel holdings by $3 billion. Bloomberg reports that the fund blacklisted Glencore, Anglo American, RWE AG, Sasol and others. BHP Group, Vistra Energy, Enel SpA and Uniper SE were put under observation. This is very positive for the movement away from fossil fuels and could open up more investments in renewable energy. Norway’s fund owns around 1.5 percent of the world’s publicly traded stocks and its decisions can have a big ripple effect. This is, however, very negative for oil producers, those miners with poor environmental stewardship track records.

Threats

- Texas was one of the hottest U.S. solar markets, but that is changing after oil’s price crash. BloombergNEF reports that developers including Cypress Creek Renewables and 8minute Solar Energy have scrapped plans to build at least 13 solar farms in the state since crude plummeted in March. Texas is the nation’s second largest economy and was a boom for solar since the state needed more power. Power use is expected to fall across Texas and Genscape cut its forecast for peak power use by 20 percent for the year as oil drilling slows.

- Bloomberg reports that as Diamond Offshore Drilling Inc was heading toward bankruptcy, it took advantage of a little-known provision in the stimulus bill to get a $9.7 million tax refund. The company then asked a bankruptcy judge to authorize that amount as bonuses to nine executives. This company is one of dozens of oil producers and contractors claiming hundreds of millions in tax rebates – employing a provision in the CARES act that gives more latitude to deduct recent losses from the collapse in oil prices. Jesse Coleman, a senior researcher with Documented, says the provision allows companies that have been losing money over the past few years to “get that money back as a check from the taxpayers.” However, Diamond Offshore has demonstrated extremely egregious corporate governance to line management’s pockets at the expense of shareholders and taxpayers.

- Tensions with China and other global superpowers are heating back up again. Australia called for an independent investigation into the origins of the coronavirus outbreak – poking a “large dragon” as Bloomberg’s Michael Heath refers to China. Australia is heavily dependent on China for trading and any pullback in supporting the economy comes at a very bad time. Australia’s central bank forecasts the economy will contract 10 percent from peak to trough this year. Separately, President Trump ordered the main pension plan for U.S. federal government employees not to invest in Chinese companies, the Financial Times reports.

Emerging Europe

Strengths

- Turkey was the best performing country this week, gaining 2 percent. Equites trading on the Istanbul Stock Exchange ignored this week’s weaker economic data and moved higher. Selcuk Ecza Deposu Ticaret ve Sanayi, a pharmaceutical company that is held in the iShares MSCI Turkey ETF, gained 31 percent over the past five days. Turkey relaxed more travel restrictions as new cases of the coronavirus drop.

- The Turkish lira was the best performing currency this week, gaining 2.7 percent. The currency bounced from last week’s record low level. On Monday, Turkey removed foreign transaction bans on three foreign banks: BNP Paribas, Citibank and UBS, after imposing these last week, saying that banks were engaged in manipulative transactions, buying large amounts of foreign currency with lira they do not own.

- Industrials was the best performing sector among eastern European markets this week.

Weaknesses

- Romania was the worst performing country this week, losing 2.5 percent. Banks sold off despite the country posting stronger-than-expected gross domestic product. According to data released on Friday, the economy expanded by 30 basis points in the first quarter versus estimated contraction of 90 basis points. BRD-Groupe Societe Generale lost 3.8 percent of its market share in the past five days and Banca Transylvania was the worst performer among stocks trading on the Bucharest Stock Exchange, losing 6.6 percent.

- The Hungarian forint was the worst performing currency in the region this week, losing 2 percent. The currency sold off due to political noise and more clashes between leaders of Hungary and Brussels. European Parliament lawmakers demanded Thursday that EU leaders punish Hungary’s government for using COVID-19 to grab power through a controversial emergency law that allowed Prime Minister Viktor Orban to sidestep parliament and rule by decree during the pandemic.

- Financials was the worst performing sector among eastern European markets this week.

Opportunities

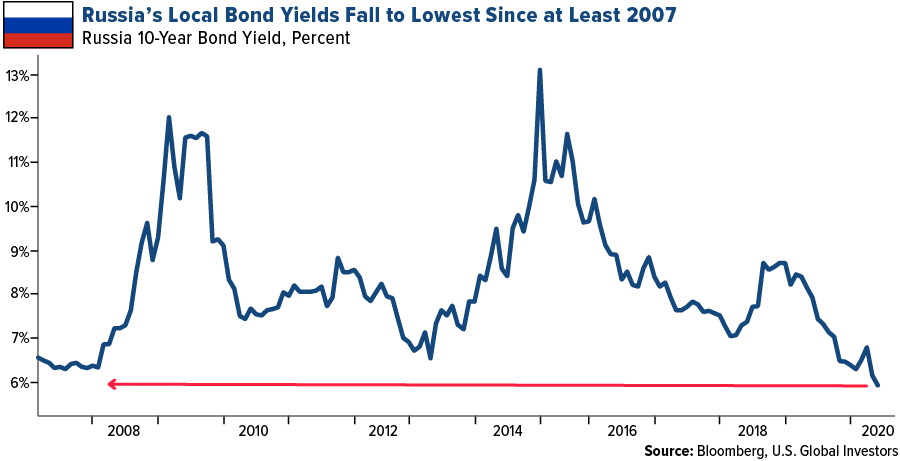

- Yields on Russian 10-year government bonds dropped to 5.9 percent, the lowest level since records began in 2007. Low borrowing costs are good news for the government, which plans to borrow as much as 4.5 trillion rubles ($62 billion) this year. Demand for Russian bonds remains high due to the country’s vast international reserves and low debt level. Moreover, an investment grade rating makes it easier for foreign investors to buy.

- The Turkish current account posted a deficit of $4.9 billion in March versus the expected deficit of $3.9 billion. Wood & Company expects that to be the trend in the following months. Its research team believes that going forward, the current account will be impacted positively by lower oil prices and an additional decline in imports, supported also by new government regulations, aimed at limiting imported goods.

- The Polish government has announced the third stage of de-lockdown including re-opening of hairdressers, beauty salons, gyms and restaurants. Importantly, the latter will enjoy much deeper loosening of restrictions than anticipated. While the local newswires were speculating on opening of restaurant gardens only, the actual change goes further and allows to open all restaurants (including dine-in and food courts). Still under the new relaxed rules, social distancing will apply, and restaurants will not operate at their full capacity yet.

Threats

- Kepler Cheuvreux predicts that Northern Europe will outperform Southern Europe, as economies of the South are more indebted and have inflexible labor markets. Greece and Italy stand out as countries with the highest debt-to-GDP ratios, Greek debt-to-GDP is 177 percent and Italy’s is 135 percent. The level of debt will increase further as governments across Europe keep providing more stimulus in order to shield their economies from the negative effect of COVID-19.

- For the first time since May 2, Russia reported less than 10,000 new coronavirus cases per day. Russia is now the second most infected country after the United States, reporting 252,245 cases as of Thursday, with 2,305 deaths. The number of cases and deaths may keep growing. Italy and the U.K. so far reported similar numbers of cases and have reported more than 13 times the Russian level of fatalities.

- The German economy, the biggest in Europe, contracted by 2.2 percent in the first quarter, the worst period in 11 years, the Federal Statistical Office said Friday. The numbers are expected to get worse before they get better. The German Statistical Office has forecast a 10 percent plunge in GDP for the second quarter, dependent on the success of lifting lockdown measures. GDP in the euro-area contracted by 3.8 percent in the first quarter, in-line with Bloomberg’s forecast.

China Region

Strengths

- Pakistan was the best performing country this week, gaining 2.3 percent. Pakistan’s central bank for the fourth time in a row cut its key interest rate to support the economy. On Thursday, the day before the rate cut decision, Pakistan reported 1,452 new cases of COVID-19 for a total of 35,788. TRG Pakistan, an information technology company, was the best performing equity among stocks trading on the Karachi Stock Exchange, gaining 22 percent in the past five days.

- The Thailand baht was the best performing currency this week, gaining 1.8 percent. The baht continues to recover as government lifts more lockdown restrictions imposed to contain the spread of the coronavirus. Thailand will allow shopping centers and retail businesses to re-open from May 17. As of Friday, Thailand reported just 7 new coronavirus cases.

- Healthcare was the best performing sector among equites trading on the Hong Kong Stock Exchange.

Weaknesses

- Indonesia was the worst performing country this week, losing 2 percent. Indonesia’s exports fell in April by 7 percent from a year ago, versus a median estimate for a shortfall of 4 percent. Imports declined 18.6 percent, resulting in a trade deficit of $345 million. Indonesia recorded 490 new cases of COVID-19 on May 15, taking the total to 16,496. Cardig Aero Services, a transportation company, was the worst performing equity among stocks trading on the Jakarta Stock Exchange, losing 29 percent in the past five days.

- The South Korean won was the worst performing currency this week, losing 60 basis points. South Korea’s President Moon Jae-in said that under the base case scenario, the country’s debt-to-GDP ratio will rise to 44 percent in 2020 and 46 percent in 2021. These figures are up from 37 percent in 2019, but well below the G-20 average of 84 percent. South Korea and China have both reported an uptick in coronavirus cases after restrictions were eased. More than hundred new cases were reported and linked to a nightclub in Seoul.

- Telecommunication was the worst performing sector among equites trading on the Hong Kong Stock Exchange.

Opportunites

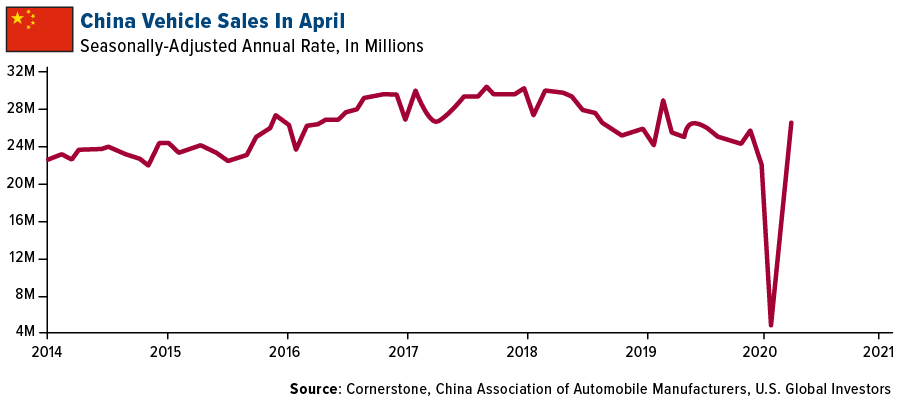

- Several positive economic data points were released from China on Monday, from credit growth to sales. The country’s vehicle sales have rebounded and demonstrated a “V-shaped” recovery, as seen in the chart below. China has enacted several measures to encourage car buying such as easing purchase restrictions, extending subsidies and reducing value-added tax on vehicles. Cornerstone Macro noted that the M2 money supply rose 11.1 percent year-over-year in April, the fastest pace in three years, and an important support for nominal GDP growth.

- Tencent reported strong first quarter revenue on increases in mobile games and social advertising revenue. The company’s revenue from January to March was up 26.4 percent year-over-year and 9.9. percent above CLSA’s estimate. Mobile games and social ad revenue were up 64 percent and 48 percent year-over-year, respectively. The massive increases were likely due to lockdown orders that kept people at home and online for several weeks.

- In Hong Kong and China, thousands of bankers have returned to the office. HSBC said 30 percent of its Hong Kong staff can return this week, according to Bloomberg, and Goldman Sachs now has a third of its employees back in the office. Workers at Bank of Communications in Shanghai wear masks all day at the office and are required to pass through an infrared temperature screen before entering the building. This is positive that workers are returning to the office and could be a model for how other countries slowly open back up the workplace.

Threats

- Wuhan, the original epicenter of COVID-19, reported six new cases of the virus last weekend after not reporting any new cases since April 3. Wuhan will be testing all 11 million residents for the virus in an effort to stem another outbreak. The city was on strict lockdown for 11 weeks and began re-opening on April 8. Jilin, a city in northeastern China with four million people, partially shut its border this week. After a cluster of infections were reported, the city is only allowing residents to leave if they have tested negative for COVID-19 in the past 48 hours. This is igniting fears that a second wave of infections is likely globally.

- The U.S.-China trade war ramped back up this week into a financial war. President Trump ordered the main pension plan for U.S. federal government employees not to invest in Chinese companies, the Financial Times reports. The Federal Retirement Thrift Investment Board manages close to $600 billion for 5.5 million federal employees and had been preparing to shift the international component of the fund into an index that includes Chinese stocks. The Trump administration argues that certain companies pose a national security risk to the U.S. such as Hong-Kong listed AviChina Industry and Technology.

- Although China released positive economic data for the month of April, there are questions about the labor market. Analysts from BNP Paribas SA say the real unemployment rate including non-urban residents could have reached 12 percent in the first quarter and as many as 130 million people could have suffered some kind of job disruption. Liu Peiqian, a China economist at Natwest Marketing in Singapore, says that the outlook for China’s labor market is “not optimistic” as the recovery in some sectors will have to wait until a global reopening. Bloomberg notes that the official jobless data leaves out a considerable part of China’s workforce. UBS forecasts the worst job market for China in more than two decades and that the number of jobs will shrink by more than 10 million in 2020.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended May 15 was Lux Bio Cell, up 349.07 percent.

- Bitcoin just experienced its third halving, reports CoinTelegraph, a one-in-four-year event. The halving has cut the miner block reward from 12.5 BTC to 6.25 BTC. Having overcome the event, the cryptocurrency traded at $8,500, with market dominance of 67 percent as of press time on Monday, the article continues.

- A Wall Street Journal report from May 12 highlights that JPMorgan Chase, the United States’ largest bank, is taking on U.S. cryptocurrency exchanges Coinbase and Gemini as customers. As reported by CoinTelegraph, the move is the first time the banking giant has served clients from the crypto industry. “JPMorgan Chase is not processing bitcoin or other cryptocurrency transactions on behalf of the exchanges but is providing cash-management services and handling dollar transactions for their U.S.-based clients,” the article reads.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended May 15 was UFO, down 65.03 percent.

- Over the weekend bitcoin appeared to be running out of steam just before one of the most anticipated milestones among crypto enthusiasts, reports Bloomberg. The largest digital token declined around 13 percent to $8,675, but on Monday rebounded to $8,840 as of 10am in New York.

- In his public channel Tuesday, Telegram founder Pavel Durov wrote that the Telegram Open Network (TON) project would be discontinued due to the company’s ongoing legal fight with the U.S. Securities and Exchange Commission (SEC), reports CoinDesk. The SEC’s winning of a preliminary injunction in a U.S. court led to the decision because it barred Telegram from launching TON or distributing its gram tokens, the article continues.

Opportunities

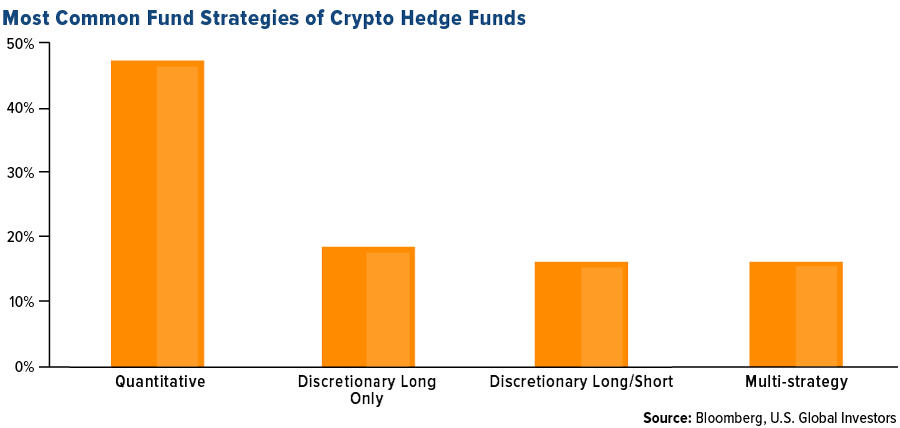

- According to a new survey, crypto-focused hedge funds’ assets under management in 2019 jumped, reports Bloomberg, but there were some big differences in performance during the year. Discretionary long-only funds, for example, had the best median performance at 40 percent, while multi-strategy funds increased a median 15 percent. Below you can see the most common crypto strategies used by hedge funds.

- As reported by CoinDesk, Binance.US has launched an over the counter trading portal to process orders worth $10,000 or more directly between customers. During Consensus: Distributed on Monday, CEO Catherine Coley said the launch comes at an opportune time for large value traders given increasing interest in bitcoin from well-known investors, such as Paul Tudor Jones.

- Recent reports show that the number of women involved in the crypto and blockchain space is skyrocketing this year, reports CoinTelegraph. The report, released by CoinMarketCap at the end of April, shows that the number of women in the industry has jumped around 43 percent in the first quarter of this year alone.

Threats

- In the case against an alleged crypto Ponzi scheme founder, CoinTelegraph writes that judges are not convinced that the risk of COVID-19 is enough to allow posting a bail bond for release. The accused, John Caruso, is still considered a flight risk despite pleading not guilty earlier this year. His legal team tried a COVID-19 defense, saying the spread of the virus puts the defendant at risk of infection while he stays in prison, but both judges did not cede to this tactic, the article continues.

- Although bitcoin is trading back above $9,000 again, technical indicators show its next leg higher might be harder to come by, writes Bloomberg. Coming off its historic halving event, it hasn’t been able to sustain a rally above $10,000. In addition, the article continues, the MACD gauge shows the smallest positive divergence since bitcoin’s uptrend began – which suggests bulls would need strong support in order to pass $10,000.

- Pantera Capital, one of the oldest cryptocurrency investment managers, is experiencing heavy losses that are rocking its alternative crypto-asset funds, reports CoinDesk. From inception to the end of 2019, for example, a Pantera Capital digital asset fund that trades a hodgepodge of free-floating virtual currencies (like ether, ripple and zcash), lost 72.8 percent.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| 10-Yr Treasury Bond | 0.64 | -0.05 | -6.57% |

| Oil Futures | 29.60 | +4.86 | +19.64% |

| Hang Seng Composite Index | 3,396.99 | -29.90 | -0.87% |

| S&P Basic Materials | 320.14 | -10.18 | -3.08% |

| Korean KOSPI Index | 1,927.28 | -18.54 | -0.95% |

| S&P Energy | 272.31 | -22.44 | -7.61% |

| Nasdaq | 9,014.56 | -106.76 | -1.17% |

| DJIA | 23,685.42 | -645.90 | -2.65% |

| Russell 2000 | 1,255.47 | -74.17 | -5.58% |

| S&P 500 | 2,860.19 | -69.61 | -2.38% |

| Gold Futures | 1,753.10 | +39.20 | +2.29% |

| XAU | 126.61 | +4.52 | +3.70% |

| S&P/TSX VENTURE COMP IDX | 508.78 | +16.69 | +3.39% |

| S&P/TSX Global Gold Index | 370.02 | +17.71 | +5.03% |

| Natural Gas Futures | 1.65 | -0.18 | -9.71% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Korean KOSPI Index | 1,927.28 | +70.20 | +3.78% |

| 10-Yr Treasury Bond | 0.64 | +0.01 | +1.27% |

| Gold Futures | 1,753.10 | +12.90 | +0.74% |

| S&P Basic Materials | 320.14 | +14.61 | +4.78% |

| S&P 500 | 2,860.19 | +76.83 | +2.76% |

| DJIA | 23,685.42 | +181.07 | +0.77% |

| Nasdaq | 9,014.56 | +621.38 | +7.40% |

| Oil Futures | 29.60 | +9.73 | +48.97% |

| Hang Seng Composite Index | 3,396.99 | +43.62 | +1.30% |

| S&P/TSX Global Gold Index | 370.02 | +61.73 | +20.02% |

| XAU | 126.61 | +22.32 | +21.40% |

| Russell 2000 | 1,255.47 | +71.49 | +6.04% |

| S&P Energy | 272.31 | +26.97 | +10.99% |

| S&P/TSX VENTURE COMP IDX | 508.78 | +66.07 | +14.92% |

| Natural Gas Futures | 1.65 | +0.05 | +3.00% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| XAU | 126.61 | +23.47 | +22.76% |

| S&P/TSX Global Gold Index | 370.02 | +108.88 | +41.69% |

| Gold Futures | 1,753.10 | +168.60 | +10.64% |

| DJIA | 23,685.42 | -5,737.89 | -19.50% |

| S&P 500 | 2,860.19 | -513.75 | -15.23% |

| Nasdaq | 9,014.56 | -697.41 | -7.18% |

| Korean KOSPI Index | 1,927.28 | -305.68 | -13.69% |

| Natural Gas Futures | 1.65 | -0.18 | -9.86% |

| S&P Basic Materials | 320.14 | -59.67 | -15.71% |

| Russell 2000 | 1,255.47 | -438.27 | -25.88% |

| Oil Futures | 29.60 | -21.82 | -42.43% |

| Hang Seng Composite Index | 3,396.99 | -414.50 | -10.88% |

| S&P/TSX VENTURE COMP IDX | 508.78 | -62.22 | -10.90% |

| S&P Energy | 272.31 | -140.84 | -34.09% |

| 10-Yr Treasury Bond | 0.64 | -0.98 | -60.44% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (03/31/2020):

BRD-Groupe Societe Generale

Barrick Gold Corp

Agnico Eagle Mines Ltd

Newmont Corp

MMC Norilsk Nickel PJSC

SRR Mining Inc

Alacer Gold Corp

AngloGold Ashanti Ltd

Anglo American PLC

BHP Group Ltd

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The GTI VERA Convergence Divergence Indicator measures up and down shifts and detects positive and negative trends.

The Stoxx Europe 600 Index covers the 600 largest companies in Europe and is divided into 19 supersectors and reflects the exposure to a certain sector in terms of free-float market capitalization. The Basic Resources component tracks the largest companies involved in the sector in Europe.

There is no guarantee that the issuers of any securities will declare dividends in the future or that, if declared, will remain at current levels or increase over time.

The University of Michigan Consumer Sentiment Index is a consumer confidence index published monthly by the University of Michigan. The index is normalized to have a value of 100 in December 1966. Each month at least 500 telephone interviews are conducted of a contiguous United States sample. Fifty core questions are asked.