Cuba and Venezuela Offer Cautionary Tales of Socialism

Date Posted: July 23, 2021

Read time: 46 min

For the past decade, citizens of Latin American countries have grown bolder in protesting their governments' failed socialist policies. We've seen unrest in, among other states, Venezuela, Chile and Colombia, but until last week, we hadn't heard a peep from Cuba, which has been under communist rule since Fidel Castro's revolution in 1959.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

For the past decade, citizens of Latin American countries have grown bolder in protesting their governments’ failed socialist policies. We’ve seen unrest in, among other states, Venezuela, Chile and Colombia, but until last week, we hadn’t heard a peep from Cuba, which has been under communist rule since Fidel Castro’s revolution in 1959.

It’s hard to exaggerate the significance of Cubans taking to the streets to air their grievances against the government. Protests of this scale are unprecedented in the Caribbean island-state’s history.

But living conditions are deteriorating fast, due to President Miguel Díaz-Canel’s mishandling of the economy during the pandemic. Echoing dismal scenes from past failed socialist-communist regimes, Cubans must stand in line for hours to buy food. Power outages can last for hours at a time.

As many others have pointed out, the protests offer hope that change may be right around the corner for the people of Cuba. Its young people—for whom the Castro revolution is fading in relevance—are well educated, active on social media and not shy about taking risks, even in the face of police violence and persecution.

What have they got to lose anyway that socialism hasn’t already stolen from them and their families?

Venezuela to Redenominate Its Currency… Again

Indeed, if you want to see a once-prosperous country’s economy destroy itself, there are few more effective ways than to install a hardline socialist government. Before the revolution, Cuba’s economy was larger than Singapore’s. But whereas the former’s decayed, the latter’s thrived under the free market policies of Lee Kuan Yew, who came into power the same year as Castro. Today, Singapore has one of the world’s highest GDPs per capita and ranks number one on the Heritage Foundation’s Index of Economic Freedom.

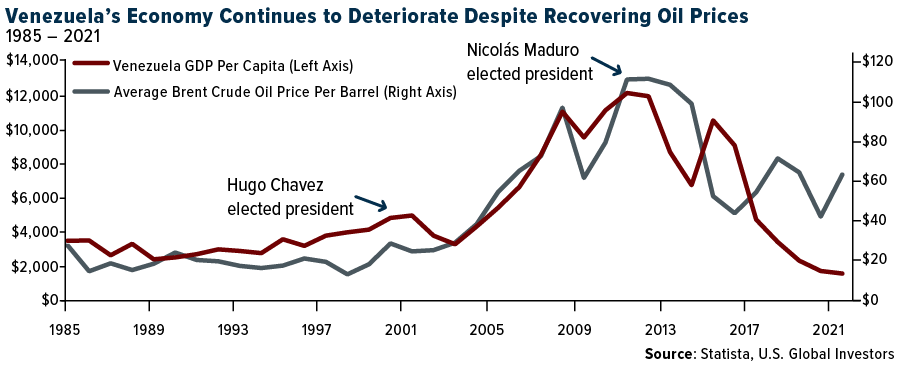

And then there’s Venezuela, once the wealthiest country in South America thanks to its fossil fuel reserves, the largest in the world. High oil prices may have helped keep Venezuela’s coffers well stocked during Hugo Chavez’s administration, but conditions tanked dramatically in 2014 when the bottom fell out of the oil market. Even when prices began to recover, the economy continued its downward spiral, fueled by unchecked government spending and rampant money-printing. GDP per capita is lower today than it was in 1985.

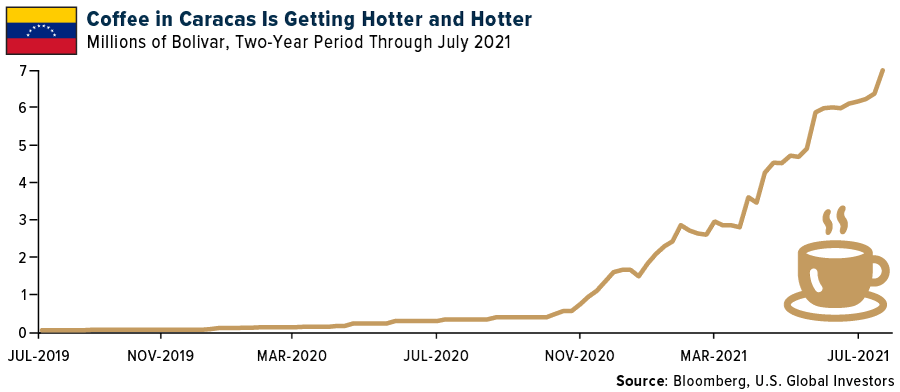

I’ve written extensively about hyperinflation in Venezuela, which continues to pummel people’s pocketbooks and savings. You think cash is trash? The Venezuelan bolivar is effectively worthless, a point well illustrated at this year’s Bitcoin 2021 conference in Miami when someone hauled in a dumpster full of 50-bolivar notes, which went ignored by attendees and passersby. According to Bloomberg’s Venezuela Café con Leche Index, a cup of hot coffee in the capital of Caracas now costs a little under 7 million bolivars, a 2,289% increase from just a year ago.

Besides destroying the value of the local currency, inflation has made making simple purchases absurdly complex. Calculator screens often cannot display entire figures, and credit cards must be swiped multiple times to complete a transaction.

That’s why, to simplify things, Venezuela announced it will be lopping off as many as six zeros from the bolivar’s value. So instead of one American dollar converting to 3,219,000 bolivars at present, it will convert to 3.2 bolivars.

This isn’t the first time the country has had to redenominate its currency. In 2018, Venezuela began printing a 1 million-bolivar note, the largest in country history, which isn’t even enough to buy you a single cup of coffee in 2021.

Gold and Bitcoin Could Be the Solution

Both Cuba and Venezuela are cautionary tales of hardline socialism, an ideology that, at its core, has no respect for civil liberties or private property. Citizens of these countries are tragically denied ownership over their own livelihoods, largely as a result of being locked into using disastrously mismanaged currencies.

Gold and Bitcoin could be the solution. These assets transfer ownership directly from governments and central banks to individual holders. When you buy a gold coin or a Bitcoin, you are granted access to real money that transcends borders, jurisdictions and regimes. This is what’s known as self-custody.

Historically, gold has literally saved people’s lives. Consider the Vietnamese “boat people” in the 1970s and 80s, who were forced to flee the country after the communists took control. Had it not been for gold, which became the de facto currency with the collapse of South Vietnam, many families wouldn’t have been able to make their escape past the Vietcong, Cambodian soldiers and even Thai pirates.

Today, Bitcoin is likewise extending a lifeline to desperate people in desperate circumstances.

Many allies of the Cuban protestors have been able to show their support by sending them Bitcoin. As I’ve pointed out before, Bitcoin adoption in Venezuela has been remarkably fast. Because there’s no third-party risk, the crypto “has become a tool to send remittances, protect wages from inflation and help businesses manage cash flow in a quickly depreciating currency,” according to reporting by Reuters.

Gold Continues to Look Undervalued

As for gold, it traded down this week, marking the first loss in five weeks, but support held at around $1,800 an ounce. I see this as an attractive entry point as the metal looks undervalued compared not only to equities but bonds as well. Ordinarily gold has traded inversely to bond yields, but as you can see below, it’s been underperforming. I’ve inverted the Treasury yield line so you can see the relationship more clearly.

On a final note, I’ll be participating in a webcast on gold and Bitcoin, and I will be joined by none other than Bitcoin evangelist Michael Saylor, founder and CEO of MicroStrategy. To get the link to book your spot for this exclusive conservation, email me at info@usfunds.com with subject line “Michael Saylor webcast.” Demand has been higher than even I anticipated, so don’t hesitate to register!

Index Summary

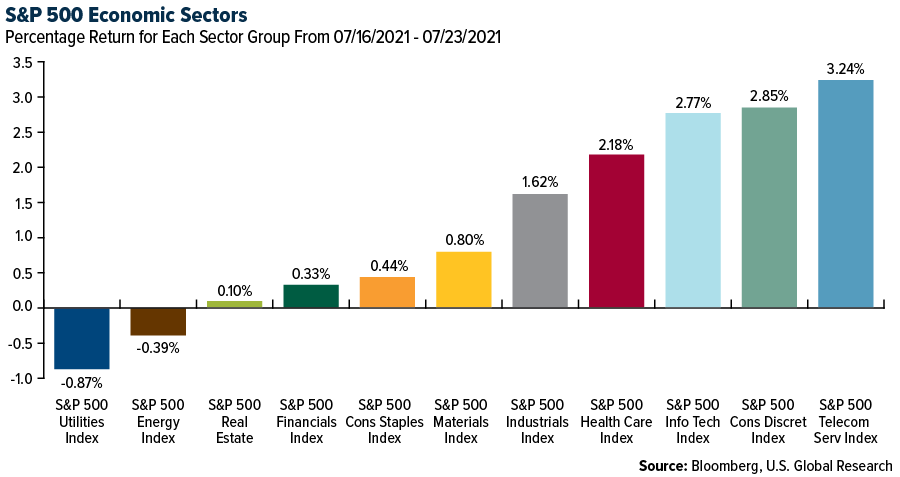

- The major market indices finished up this week. The Dow Jones Industrial Average gained 1.08%. The S&P 500 Stock Index rose 1.96%, while the Nasdaq Composite climbed 2.84%. The Russell 2000 small capitalization index gained 2.15% this week.

- The Hang Seng Composite lost 2.98% this week; while Taiwan was down 1.80% and the KOSPI fell 0.69%.

- The 10-year Treasury bond yield fell 11 basis points to 0.85%.

Airline Sector

Strengths

- The best performing airline stock for the week was Global Crossing Airlines, up 24.8%. Bank of America’s proprietary Flight Signals indicator improved to -19.8 from -29.6 last quarter (and -46.1 in the fourth quarter of 2020), showing a continued rebound in industry domestic unit revenues in the second quarter.

- Airline earnings generally have been strong. Alaska Air reported a small loss in the second quarter, which was ahead of consensus, and guided toward double-digit margins in the third quarter. Earnings for Southwest Airlines were also ahead of expectations due to lower-than-guided costs. American Airlines also reported surprisingly high earnings due to demand, particularly corporate. Volaris had a very strong second quarter. Volaris revenue increased 38% in the second quarter versus 2019, (ahead of the +24% consensus).

- Restrictions on international travel continue to loosen. President Biden noted that the U.S. potentially lifting the European Union (EU) travel ban is "in process" with a possible answer in the next few days. Prime Minister Trudeau noted that Canada could begin allowing vaccinated tourists from the U.S. as early as mid-August, and other countries by early September.

Weaknesses

- The worst performing airline stock for the week was Great Lakes Air, down 33.3%. Intra-Europe bookings took a step down in the week. Analysts think the easing of U.K. travel restrictions is positive, as the U.K. travel recovery has lagged the EU. Intra-Europe net sales fell 7 ppts. to -49% of 2019 levels (versus -42% in the prior week) and declined 3% on a week-by-week basis.

- The delta variant may be having an impact on the airline industry. System net sales took a step back to down -50.3% versus 2019 for the week compared to -41.2% last week (and -44.1% the week prior). The most surprising datapoint to UBS is domestic tickets sold decelerated down to a negative 24.4% versus 2019 this week (versus -9.3% last week) with domestic tickets sold through OTA channels (UBS’s proxy for leisure travel) decelerating to up +7.9% versus 2019 after being up double digits the past four weeks.

- The delta variant is also having an impact on the corporate sector. This week, tickets booked through small and large corporate channels both declined to -33.6% (from -18.6%) and -59.9% (from -47.4%), respectively, versus the second quarter of 2019.

Opportunities

- U.S. President Biden signed an executive order to increase transparency within the airlines industry and ensure both safety and competition within the Urban Air Mobility (UAM) space. The Executive Order directs the Department of Transportation (DOT) to increase transparency around add-on fees and refunds for airline customers.

- Qantas is well positioned, according to some analysts, both from a balance sheet and competitive position to come out of the crisis stronger. Qantas derives 70-75% of its earnings from the domestic and loyalty businesses, limiting risk around the opening of international borders. Qantas expects to resume broader international flights at year end when most of the Australian population will have been vaccinated.

- The Chinese air travel market is improving. The data shows a recovery in Chinese domestic traffic and pricing in the first half of July as Guangdong travel restrictions have eased. Domestic seat loads have reached a post-COVID high of 79% suggesting healthy demand going into the peak summer season. Chinese international travel continues to languish, tracking at 3% of normal demand given China’s tight border controls with the Chinese government staying vigilant in controlling imported cases given new COVID variants.

Threats

- Airlines may not be immune from labor shortages. As travel demand surges towards pre-pandemic levels, some airlines continue to face labor shortages. Alaska Airlines called for managers and back-office personnel at the Seattle-Tacoma International Airport to volunteer to help move baggage over the holiday weekend and through August. However, Alaska Air is not the only airline facing labor shortages. Earlier in the summer, American Airlines announced it will trim its schedule by 1% to ease some of the summer travel disruptions.

- The EU is also proposing a minimum tax applicable to aviation fuel used for intra-EU flights, which will increase over a ten-year period. Furthermore, under ReFuelEU it is proposed that sustainable aviation fuel (SAF) should be a minimum of 5% of fuel by 2030, 32% by 2040 and 63% by 2050. These proposals (ETS, fuel tax and SAF) will lead to higher costs for the aviation industry, which is likely to result in the industry trying to increase ticket prices or otherwise see headwinds to margins and/or reduced volumes.

- Latin American airlines are still under pressure. Capacity recovery has been subject to mobility restrictions, which has been gradually removed, stimulating demand, but still well below pre-pandemic levels. Added to that, yields remain under pressure, also impacted by a poorer mix with less corporate travel.

Emerging Markets

Strengths

- The best relative performing country in emerging Europe for the week was Poland, losing 0.21%. The best performing country in Asia this week was Indonesia, gaining 0.40%.

- The Russian ruble was the best performing currency in emerging Europe this week, gaining 0.56%. The Pakistani rupee was the best performing currency in Asia this week, gaining 0.95%.

- The Eurozone PMIs remain strong. Preliminary July Manufacturing PMI was reported at 62.6. The Service PMI increased to 60.4 supported by summer travel and market reopening, while the Composite PMI jumped to 60.6 from 59.5 in June.

Weaknesses

- The worst performing country in emerging Europe for the week was Hungary, losing 1.1%. The worst performing country in Asia this week was the Philippines, losing 2.6%.

- The Czech koruna was the worst performing currency in emerging Europe this week, losing 0.75%. The Pakistani rupee was the worst performing currency in Asia, losing 0.75%.

- Turkish consumer confidence declined to 79.5 points in July from 81.7 a month earlier. A confidence level below 100 reflects a pessimistic outlook, while a reading above 100 indicates optimism. Next week confidence data will be coming out for many other emerging countries.

Opportunities

- Oil production in Russia is on track to reach pre-crisis levels in May of 2022, Russian Deputy Prime Minister Alexander Novak said this past Sunday. The OPEC organization and non-OPEC nations, which have been cutting production to stabilize the market, agreed last weekend to extend the deal until the end of 2022, but five countries, (Russia, Saudi Arabia, the United Arab Emirates, Kuwait, and Iraq), will have a possibility to increase production after May of 2022.

- Bloomberg reports that Singapore is facing the biggest threat to its status of being the dominant bunker fuel supplier in Asia as China expands its refining and port facilities. China’s marine fuel sales have almost doubled in the past five years, with the center of the trade located in Zhousgan, south of Shanghai. Singapore sold around 50 million tonnes of bunker fuel in 2020, 20% of the global total, with China’s sales rising to around 17 million tonnes, a fifth consecutive year of increased sales.

- Reuters reports that U.S. Deputy Secretary of State Wendy Sherman will visit China on July 25 to 26 to meet with State Councilor and Foreign Minister Wang Yi and other officials in the city of Tianjin. This could help set the stage for further exchanges and a potential meeting between U.S. President Biden and China’s President Xi Jinping later this year, possibly on the sidelines of the G20 summit in Italy sometime in late October.

Threats

- Euronews reports data showing the European Union (EU) has now vaccinated more people against COVID-19 with a first jab than the United States; 55.7% of EU citizens, as of Saturday, have received their first dose compared with 55.5% of Americans. However, the U.S. remains ahead of the EU when it comes to full vaccinations with 48.1% and 42.5% vaccinated, respectively. This new data comes after months of criticism over the slow start of a vaccination campaign in Europe and at a time when concerns are growing over the delta variant of this virus. A pickup in coronavirus infections may lead to more restrictive measures to stop the spread of the delta variant. There has been a pickup in COVID-19 cases in Asia as well.

- Emerging market investors have been pouring money into bonds and cutting back on stocks in a trend that’s set to intensify as the delta variant of the coronavirus ravages developing economies with low vaccination rates, Bloomberg reported. Bonds have seen net inflows for eleven-straight months, the longest streak in the Institute of International Finance data going back to early 2018. They surged to a net of $99.2 billion in the past six months through June, versus net equity withdrawals of $2.2 billion, which tallies emerging markets, excluding China.

- A rights group in Russia announced that it was shutting down, citing fear of prosecution of its members and supporters after Russian authorities blocked its website for allegedly publishing content from an “undesirable” organization. Pressure mounts on opposition supporters, independent journalists, and human rights activists in Russia ahead of the September’s parliamentary election.

Energy and Natural Resources Market

Strengths

- The best performing commodity for the week was lumber, rising 18.20%. Wildfires raging in the West are threatening an important swath of the U.S.’s wood supply, explains the Wall Street Journal, lifting lumber prices. European natural gas prices have been well above consensus, driven by further increases in coal generation costs in recent weeks combined with incremental tightening of northwestern European gas balances. British wholesale gas prices rose as outages at facilities on the U.K. continental shelf reduced flows, and wind power output remained very low.

- Copper prices fluctuated significantly in the second quarter, from a low of $3.99 per pound on April 1 to a record high of $4.74 per pound on May 11. More recently, copper prices have cooled from record levels to $4.30 per pound. Copper is still trading at the highest level in a decade, with the second quarter average copper price at a near-record $4.38 per pound. The persisting drought in Chile could hit production at Antofagasta’s Los Pelambres copper mine, one of the world’s largest, the London-listed copper producer warned recently.

- Following a 70% decline in U.S. drilling activity to an August 2020 trough, the U.S. rig count has nearly doubled, and now stands at 60% of pre-pandemic rig count levels. Meanwhile, OPEC drilling activity, which fell 45- 50% to a December trough, has yet to show signs of a meaningful uptick, as rig counts in these markets are up only 5- 10% since December.

Weaknesses

- The worst performing commodity for the week was iron ore, falling 9.41%, due to concerns about a slowdown in demand. Bank of America is bearish on oil. The bank believes OPEC has forgotten that money is still cheap and U.S. shale oil wells have exceptional returns at $70 per barrel. Public E&Ps are remaining capital disciplined, but the Private E&Ps, who still react to price signals, are in full-blown growth mode with oil north of $70 per barrel and exceptionally low service costs. This week’s petroleum inventories update was bearish relative to consensus. Inventories rose by 0.6 million barrels, versus consensus estimates for a draw of 3.8 million barrels. Turning to crude, total inventories rose by 2.1 million barrels, versus consensus calling for a draw of 3.9 million barrels.

- China should release 170,000 tons of metals from state reserves on July 29. China will sell another 30,000 tons of copper, 90,000 tons of aluminum and 50,000 tons of zinc from its state reserves on July 29, the National Food and Strategic Reserves Administration said on Wednesday. The auction marked the second sale by the world’s top metals consumer this month as Beijing aims to rein in skyrocketing commodity prices. Additionally, China offered millions of barrels of oil from its strategic state reserves this month in an unprecedented move to try and quell inflation brought on by rising costs of everything from food to fuel. The country will supply about 3 million tons — or 22 million barrels.

- Oil in London declined to the lowest level in five weeks after OPEC agreed to boost production into 2022, while a surge of the delta coronavirus variant threatened the rebound in the global economy. Brent futures lost as much as 2.9%. OPEC and its allies will add 400,000 barrels a day each month from August until all halted output is revived.

Opportunities

- The EU announced its “Fit for 55" emissions reduction plan Wednesday, detailing numerous carbon curtailment initiatives and mandates. In addition to ending internal combustion vehicle sales by 2035, the EU estimates that by the same year roughly 80% of all European air travel will be powered by sustainable fuel.

- Fresh catalysts have emerged in aluminum’s market, including the 15% Russia export tax, further power constraints in China, and the first release of 50 kilo tons of inventory from China’s State Reserve. These add to the gradual recovery of the automotive sector through the second half from semiconductor shortages, the return of the aerospace sector, ongoing constraints on container freight, and China’s 45 million tons per year capacity cap.

- Goldman is bullish on Alcoa. First, the company has significant leverage to a positive commodity price outlook, where they estimate every 10% increase in aluminum prices corresponds to a 20% increase in EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization). Second, Alcoa has been successful in its deleveraging strategy, which they expect to free up balance sheet capacity for capital returns. Third, Alcoa screens favorably relative to the global industry, given the company’s lower carbon footprint and green growth initiatives.

Threats

- Low refining margins are driving further acceleration in capacity closures. Goldman believes another 2.0 million barrels per day of closures are required to drive a refining upcycle as seen in 2017-2018, as large new refining capacity is still ramping up in the Middle East and China. Goldman revised its estimates lower for refiners to account for weaker June refining margins relative to expectations, elevated RINs (renewable identification numbers) costs, and rising crude prices driving headwinds to capture rates. The group continues to recommend investors stay selective among the refiners.

- Lumber pricing experienced an eighth consecutive week of heavy downward pressure as buyers remained on the sidelines working down higher cost inventories, despite growing wildfire threats. Interesting enough, it was the top performing commodity for the week.

- Solar energy is facing two main concerns: commodity cost inflation from polysilicon and the uptick in the interest rate environment. However, Raymond James indicates it is very rare for projects to be canceled due to the recent cost inflation, while delays are more common though by no means universal. They also indicate that interest rates are even less of a concern; if anything, the cost of capital for solar continues to trend lower.

Domestic Economy and Equities

Strengths

- Manufacturing PMI remains strong in the United States. July’s preliminary reading was released at 63.1, above the expected 62. However, Service PMI in July declined to 59.8 from 64.6 in June and below the expected reading of 64.5. The Composite PMI remains at an expansionary level of 59.7, well above the pre-pandemic reading.

- Housing starts in the U.S. rose by 6.3% monthly in June after increasing by 2.1% in May; the data was published jointly by the U.S. Census Bureau and the U.S. Department of Housing and Urban Development on Wednesday. The housing starts reading was reported higher for the third-straight month in a row and is at the highest since March.

- Moderna Inc., a biotechnology company, was the best performing S&P 500 stock for the week, increasing 21.7%. The shares surged after European regulators cleared the company’s COVID-19 shot for children aged 12 to 17.

Weaknesses

- July’s National Association of Home Builders (NAHB) sentiment missed expectations and fell to an 11-month low, with NAHB’s Chairman saying that builders continue to face elevated building material prices and supply shortages.

- FactSet reported that many people are worried about the recent COVID-19 resurgence, driven by the highly transmissible delta variant, and concentrated largely in the unvaccinated portion of the population. Weekly reported new cases in the U.S. are now around 26,000, up 70% week-over-week, with hospitalizations up 36% week-over-week and deaths up around 26%. The Centers for Disease Control and Prevention (CDC) estimates that over 97% of those hospitalized for severe cases are unvaccinated.

- Ball Corporation, a container/packaging maker, was the worst performing S&P 500 stock for the week, losing 6.7%. RBC cut its price target on Ball Corporation from $113 to $100, but maintained an outperform rating.

Opportunities

- The annualized GDP, released by the U.S. Bureau of Economic Analysis (BEA), should be revealed as stronger once the data comes out next week. Bloomberg economists now see the United States economy growing at an 8.1% rate, higher than the prior reading of 6.4%.

- A Federal Reserve meeting will take place next week. The rates will most likely stay unchanged, and banks will continue to support the economy, especially in the face of growing concerns around another COVID-19 wave due to the delta variant.

- A bipartisan group of senators is closing in on a $579 billion infrastructure deal after agreeing to pay for it in part by delaying a costly Trump-era Medicare regulation, but they don’t expect to announce details until at least Monday. Delaying the medical ruling reduces expenditures through the Medicare program by roughly $177 billion over a decade; the funds will be used to help pay for roads, bridges, and other projects.

Threats

- U.S. health officials said the contagious delta variant has rapidly become the most dominant strain of coronavirus in the country. Rochelle Walensky, director of the CDC, told a Senate health committee hearing on Tuesday that her agency now estimates that the strain accounts for 83% of sequenced cases.

- The Consumer Confidence Index, which is administered by The Conference Board and measures how optimistic or pessimistic consumers are regarding their expected financial situation, may decline next week when data is released. In July, the index may fall to 124.5 from 127.3 in June.

- Local Chinese governments are launching rescue funds to bail out state-owned enterprises (SOEs) due to increased bond defaults. According to FactSet, six provinces committed at least CNY110 billion ($17 billion) since the end of last year. Distressed bonds issued by state-owned enterprises totaled CNY119 billion last year, the highest since China started allowing SOEs to default in 2014.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was EIFI Finance, gaining over 2 million percentage points.

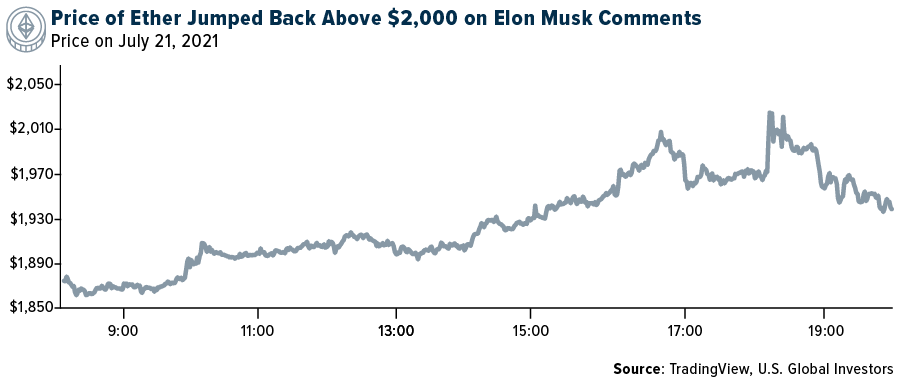

- On Wednesday, the price of Ethereum rose following comments from Tesla CEO Elon Musk stating that he owns the popular cryptocurrency. Musk also repeated his support for cryptocurrencies in general, reports CNBC, despite potential environmental risks he has noted before. Musk added that as Bitcoin mining is increasingly powered by renewable energy, Tesla will likely move to accept the popular digital currency for transactions once again.

- Only July 20, Viridi Funds announced the launch of the Viridi Cleaner Energy Crypto-Mining & Semiconductor ETF (ticker symbol RIGZ). The fund is focused on investments within the cryptocurrency mining and mining infrastructure industries, explains the company’s press release. “We launched RIGZ to provide investors with an ETF that attempts to align purpose and profit by investing in the infrastructure that underpins the entire ecosystem with sustainability in mind,” said CEO Wes Fulford. HIVE Blockchain Technologies is currently around 4% of the ETF’s holdings.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was Golden Ratio Token, falling 93%.

- On Bloomberg Markets this week, Guggenheim Investments Chairman Scott Minerd said Bitcoin could drop to $15,000. In his interview with reporter Sonali Basak, Minerd explained that the standard bear market for Bitcoin has been about an 80% retracement, and given all the uncertainty in the space, along with all of the new competition (in terms of new coins, etc.), he thinks there is more downside to go in the price.

- In the futures market DeFi Pulse, where financial initiatives like lending take place on the blockchain, notes that trading activity has fallen to $54 billion compared to $89 billion at its peak in May. A big driver of staking coins was to earn more attractive yields than on treasuries, but that advantage has now narrowed.

Opportunities

- Fund managers are pushing ahead to get the first American Bitcoin ETF approved, writes CoinTelegraph. This week, New York-headquartered fund manager Global X Digital Assets filed an application for a BTC ETF with the SEC. The application indicates that the Global X Bitcoin Trust would, if approved, trade on the CBOE BZX exchange.

- A survey conducted by Goldman Sachs on family offices found that nearly half of respondents plan to add digital currencies to their portfolio of investments. A breakdown of the survey participants shows that 22% had assets totaling more than $5 billion and 15% of family offices are already investing in cryptocurrencies.

- Most major central banks trail China in the trials of rolling out a digital currency, which has already taken place in several cities. India is also looking to phase in a digital currency but is struggling on whether their system would provide anonymity or non-anonymity on currency transactions. Meanwhile, the U.S. Federal Reserve and the Bank of England are looking into possibilities of a digital currency.

Threats

- NatWest has followed some of its U.K. banking peers in blocking debit and credit card payments to crypto exchange Binance, writes CoinDesk. The move from NatWest comes following the warning from the Financial Conduct Authority last month that Binance was operating in the country without permission. A further blow to crypto in the U.K., the article explains, came on Thursday as the CEO of Starling Bank Anne Coden described some cryptocurrency exchanges as “quite dangerous,” while on a call to reporters.

- The European Union is proposing to prohibit anonymous cryptocurrency transactions as part of a broader plan to combat money laundering and terrorism financing, writes Bloomberg. The plan unveiled Tuesday would ban anonymous crypto asset wallets, with the European Commission saying systems like Bitcoin should be governed by the same rules as regular bank wire transfers.

- The U.S. Senate is set to investigate crypto’s use in the numerous ransomwares attacks that have crippled infrastructure. Both the Homeland Security branch and the Judiciary Committee will be conducting dual probes and the tone of the discussions seem to focus more on cryptocurrencies rather than on the attacks themselves.

Gold Market

This week spot gold closed the week at $1,802.15, down $9.90 per ounce, or 0.55%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 2.49%. The U.S. Trade-Weighted Dollar rose 0.25%.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Jul-20 | Housing Starts | 1,590k | 1,643k | 1,546k |

| Jul-22 | ECB Main Refinancing Rate | 0.000% | 0.000% | 0.000% |

| Jul-22 | Initial Jobless Claims | 350k | 419k | 368k |

| Jul-26 | Hong Kong Exports YoY | 24.6% | — | 24.0% |

| Jul-26 | New Home Sales | 800k | — | 769k |

| Jul-27 | Durable Goods Orders | 2.0% | — | 2.3% |

| Jul-27 | Conf. Board Consumer Confidence | 124.1 | — | 127.3 |

| Jul-28 | FOMC Rate Decision (Upper Bound) | 0.25% | — | 0.25% |

| Jul-29 | Germany CPI YoY | 3.2% | — | 2.3% |

| Jul-29 | Initial Jobless Claims | 378k | — | 419k |

| Jul-29 | GDP Annualized QoQ | 8.5% | — | 6.4% |

| Jul-30 | Eurozone CPI Core YoY | 0.6% | — | 0.9% |

Strengths

- The best performing precious metal for the week was palladium, up 1.74%. Following the initial announcement of the agreement in principle (in June 2020), Kinross Gold has officially signed a definitive agreement with the Government of Mauritania, providing greater certainty on the fiscal terms and the economics of the Tasiast mine. The agreement confirms the same terms as stated in the previous announcement June 15, 2020, including tax exemptions on fuel duties, an updated sliding scale royalty rate, and payment from Kinross to the Government of Mauritania of $10MM to resolve previously disputed matters.

- The gold industry continues to increase its output as it recovers from the impact of COVID-19. The industry’s aggregate gold equivalent output is forecast to increase 13.4% year-over-year in the second quarter of 2021. In the second quarter of 2020, gold output was impacted negatively as mines operated at reduced levels and were being placed on care and maintenance.

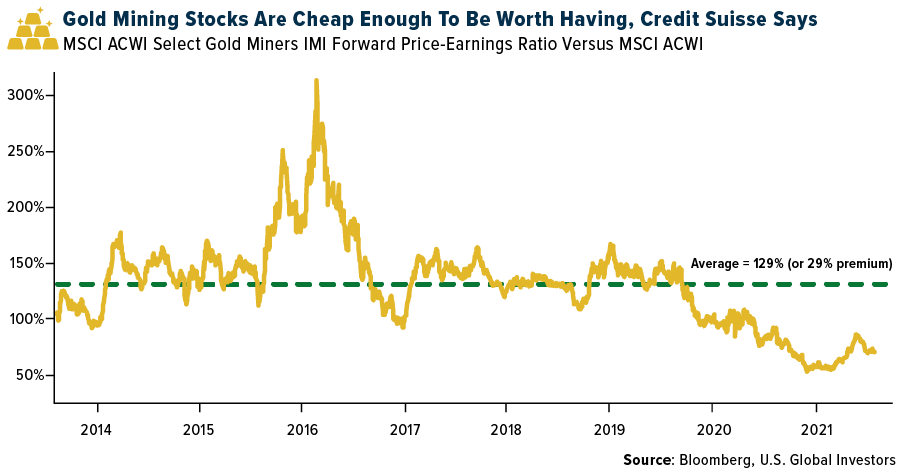

- Credit Suisse is bullish on gold stocks. The bank feels they are 25-30% undervalued on a price-to-earnings metric. The recent fall in TIPS (treasury inflation-protected securities) should help the price of gold by 5.5%. Should there be unsustainable debt levels, gold can be a protector against this. Gold is 20% below its prior peak and cheap compared to other commodities.

Weaknesses

- The worst performing precious metal for the week was platinum, down 3.74%. Gold edged lower, extending its retreat from a one-month high, as the dollar and Treasuries rallied amid a deterioration in risk sentiment across markets. Gold prices also reacted in response to stocks continuing their rebound following a sharp drop driven by concerns over COVID-19 flare-ups.

- Yamama Gold’s Wasamac project timelines have been delayed by one year and the company now outlines initial production by the end of 2026. Post-acquisition in January 2021, Yamana outlined initial construction by late-2023 and production in 2025 within its 10-year plan. Timelines have been delayed one year to reflect initial construction in mid-2024, production by the end of 2026, and commercial production by the end of 2027. Permits are not expected to be received until mid-2024.

- The Kyrgyx government violated U.S. bankruptcy rules when it took legal action against Kumtor Gold Company, according to a recent federal ruling. The ruling related to a violation of the automatic stay.

Opportunities

- Bloomberg highlighted that gold mining stocks, based on their forward price-to-earnings ratio, are abnormally cheap in comparison with the relative value of global stocks. While the prior year’s return for gold mining stocks was strong, this year’s price action has been mixed, with current levels suggesting a better entry point for a global portfolio would be timely.

- Stifel anticipates production for B2Gold to be much stronger in the latter half of the year, due to better grades expected at Fekola and the Wolfshag pit at Otjikoto. Fekola continues to offer production upside opportunities, with mill throughput now expected to exceed nameplate capacity and Cardinal offering a new source of mill feed. With Fekola mill throughput at 8.5MM tons per year, analysts see a positive boost to B2’s 2022-2023 production estimates of 3-4%.

- Marathon Gold announced it has entered into an exclusive, non-binding, indicative term sheet with Sprott Resource Lending Corp. for a US$185 MM senior secured project financing facility. The facility is structured as a term loan with a 6.5-year tenor. Closing is scheduled for no later than March 31, 2022.

Threats

- The question of who controls more than $1 billion of Venezuelan gold stored in the Bank of England’s (BOE) vaults took another twist after the British government said that it continues to recognize the leadership of opposition figure Juan Guaido. A U.K. Supreme Court hearing that started Monday will decide whether the BOE must release the bullion to the Venezuelan central bank, controlled by the government of Nicolas Maduro.

- Two countries, Kazakstan and Turkey, have reduced their gold reserves. Reserves in Kazakstan fell to 12.4 million ounces from 31.1 million ounces. Reserves in Turkey fell from 23.2 million ounces to 22.9 million ounces.

- “Definitely there has been some distraction and tarnish taken as a result of the interest in cryptocurrencies,” Evolution Mining co-founder and CEO Jake Klein said in a Bloomberg TV interview, when asked if the surge in interest in the new asset class had impacted the gold market. “Cryptocurrencies do have a lot of energy — we need Elon Musk tweeting about gold rather than cryptocurrencies,” said Klein, while questioning whether they would ever replace gold as a store of value. “Maybe I’m old school, but I’m not sure how you wake up every morning and create an asset that is going up by 5% or 10% each day and you’re not sure why, and that’s cryptocurrencies”.

Leaders and Laggards

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (06/30/2021):

Alaska Air Group Inc.

American Airlines Group Inc.

Southwest Airlines Co.

Qantas Airways Ltd.

Goldman Sachs Group Inc.

Evolution Mining Ltd.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The MSCI ACWI Select Gold Miners Investable Market Index (IMI) aims to focus on companies in the gold mining industry that are highly sensitive to underlying prices of gold. Housing starts is an economic indicator that reflects the number of privately owned new houses on which construction has been started in each period. These data are divided into three types: single-family houses, townhouses or small condos, and apartment buildings with five or more units.

The Index of Economic Freedom is an annual index and ranking created in 1995 by conservative think-tank The Heritage Foundation and The Wall Street Journal to measure the degree of economic freedom in the world’s nations.

The Consumer Confidence Index (CCI) is an indicator which measures consumer confidence in the Economy. The Bloomberg Venezuela Café con Leche Index tracks the price of a cup of coffee served hot at a bakery in eastern Caracas