Don’t Be Fooled by the Politics of Envy

Date Posted: March 8, 2019

Read time: 56 min

Here at U.S. Global Investors, we're politically agnostic. We believe there's money to be made no matter which party is calling the shots. That's why we focus on government policy instead of partisan politics.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

Here at U.S. Global Investors, we’re politically agnostic. We believe there’s money to be made no matter which party is calling the shots. That’s why we focus on government policy instead of partisan politics.

Having said that, I think most of you would agree that there’s lately been a change in some American voters’ appetite for socialist-leaning policies.

Need proof? A Gallup poll from August of last year found that, for the first time in modern memory, Americans aged 18 to 29 are more positive about socialism than they are about capitalism. Fifty-one percent preferred the former compared to 45 percent for the latter.

I don’t need to remind you that socialist policies are naturally anti-business and anti-private property, and they create all sorts of friction in the formation of new capital. A “threat to U.S. equity valuations is emerging in the form of left-wing populism in America,” writes Christopher Wood in his widely read GREED & fear newsletter.

Again, we believe extremism at either end can raise huge obstacles for business and investors. The difference, though, is that hard-left legislators seek to punish wealth and prosperity through politics of envy. Amazon, one of the world’s most valuable companies, was driven out of New York as if it were the plague. The online retail company came under additional fire this week when Massachusetts senator Elizabeth Warren said she would break up giant tech firms if she were elected president.

At their worst, socialist policies can destroy entire economies. Just look at Venezuela. It’s hard to believe now that the beleaguered country was once the wealthiest in South America.

“There is the dark side of it,” Canadian psychologist Jordan Peterson once said of socialism, “which means everyone who has more than you got it by stealing it from you… ‘Everyone who has more than me got it in a manner that was corrupt, and that justifies not only my envy but my actions to level the field,’ so to speak… There is a tremendous philosophy of resentment that I think is driven now by a very pathological anti-human ethos.”

Still Strong Pushback Against Socialism in the U.S.

“America will never be a socialist country,” President Donald Trump proclaimed during last month’s State of the Union address. The remark appeared to have been directed squarely at the raft of newly elected lawmakers who seem to be cut from the same cloth as “democratic socialist” Bernie Sanders.

The 77-year-old Vermont senator, by the way, just announced that he would be seeking the White House for a second time—and raised a whopping $6 million within the first 24 hours.

Despite his success in 2016, Sanders’ candidacy might be a hard sell for most Americans this year, as a recent NBC News/Wall Street Journal Survey showed that a majority of voters wouldn’t be too keen on having a socialist president or one who was over the age of 75. Close to three quarters of respondents either had “total reservations” or were “very uncomfortable” about the idea of voting for someone who self-identified as a socialist, as Sanders does.

At the same time, Sanders’ highly publicized bid for the White House during the last cycle appears to have galvanized some lawmakers and encouraged them to creep even further left. The Green New Deal (GND) is one such example.

The $93 Trillion Green New Deal

The GND resolution, if passed and signed into law, would radically transform day-to-day life here in the U.S. Reforms include “zero-emission” transportation, universal health care, guaranteed jobs and guaranteed “green” housing.

These goodies might sound appealing to some, but they won’t come cheap. Universal health care alone would cost the U.S. government as much as $36 trillion between 2020 and 2029, according to calculations made by the American Action Forum (AAF). That amounts to $260,000 per household.

And the price tag for the entire package? An unfathomable, eye-watering $93 trillion.

Many of you are no doubt aware that the GND is co-sponsored by Alexandria Ocasio-Cortez, the 29-year-old freshman representative from New York’s 14th district who was among the most vocal critics of Amazon moving into her neighborhood.

Like Sanders, she identifies as a democratic socialist.

As some people have pointed out, “AOC,” as she’s often called, has no financial licenses or MBA. She’s not a fiduciary. And yet if she and other socialist-minded lawmakers get their way, the American taxpayer could be saddled with the single largest spending package the world has ever seen.

Further, did you know that AOC recently won a seat on the powerful House Financial Services Committee? The committee, chaired by Representative from California Maxine Waters, has oversight over all things Wall Street—from banks to insurance, from money to credit, from securities to exchanges.

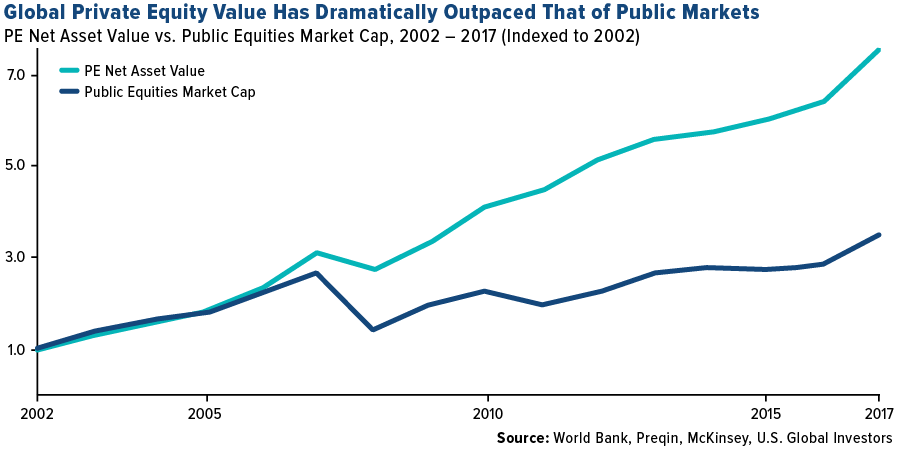

Private Equity Has Grown Twice as Fast as Public Markets

According to the AAF, the regulatory cost of the GND would be at least $1 trillion. And that’s on top of the trillions that already-in-place rules and regulations sap from American companies every year.

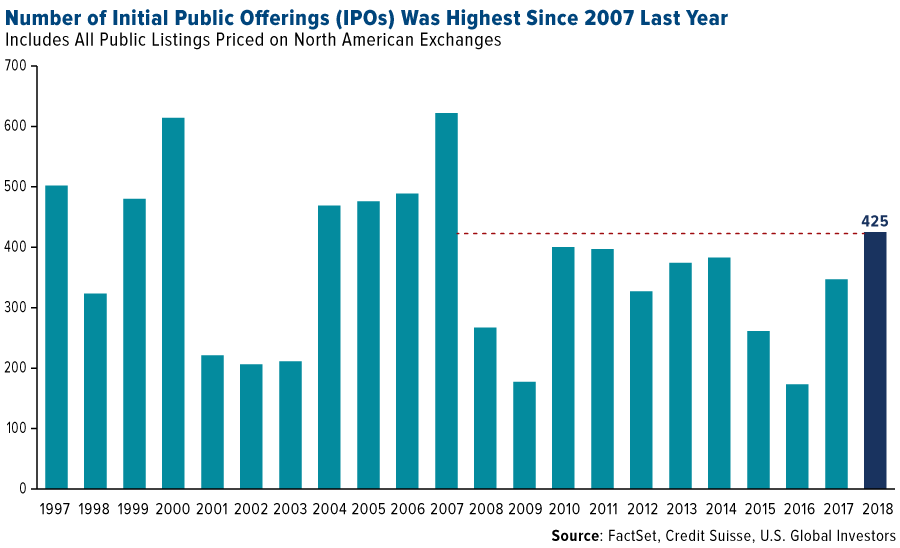

It’s little wonder, then, that more and more companies are choosing not to list on public markets. I’ve written about this a number of times before. Simply put, tougher and costlier regulations have largely contributed to the boom in private equity (PE)—not just in the U.S. but across the globe. According to a recent McKinsey report, private markets have grown 7.5 times so far this century, or twice as fast as public market capitalization.

Here in the U.S. and Canada, the number of companies that publicly listed rose to an 11-year high in 2018, thanks to more business-friendly policies. The initial public offering (IPO) market looks as if it might do just as well this year, if not better, with huge tech unicorns such as Uber, Lyft, Airbnb and Pinterest expected to list.

But the overall trend has been down, and that’s really hurt small investors who don’t generally have access to private equity.

Is Gold the Solution?

All of this is ample reason to ensure that you have some gold in your portfolio. I always advocate the 10 percent Golden Rule. That means I think you should have half of that 10 percent in gold coins, bars and 24-karat jewelry. The other half should be in high-quality gold mining stocks and funds. Make sure you rebalance at least once a year.

One of the biggest proponents of gold is the Austrian school of economics, which emphasizes self-reliance and individualism. Because fiat currencies are solely based on the faith and credit of the economy, they have no intrinsic value and are prone to huge swings, according to Austrian economic thought.

Gold, on the other hand, is nobody’s liability. As destructive as socialist policies can be to business and capital, they can’t reduce the value of your gold. In fact, the inverse is true. Historically, the more debt that the government accrues, and the higher inflation gets, the more valuable the yellow metal has become.

Did you miss it? This week I spoke with Small Cap Power’s Jim Gordan on a range of topics, from newcomer GoldSpot Discoveries to the U.S.-China trade war. Watch it now by clicking here!

Gold Market

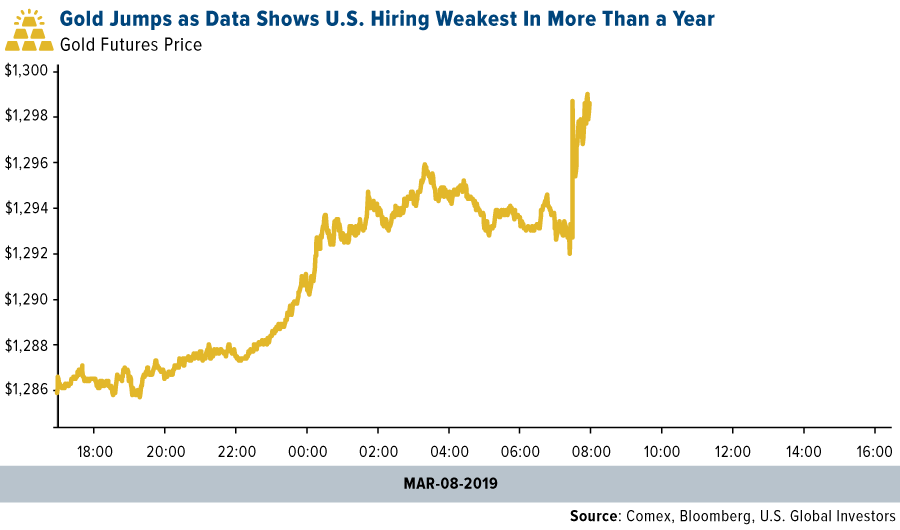

This week spot gold closed at $1,298.40, up $5.00 per ounce, or 0.39 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 1.80 percent. The S&P/TSX Venture Index came in off 1.13 percent. The U.S. Trade-Weighted Dollar rose 0.88 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Mar-5 | New Home Sales | 600k | 621k | 599k |

| Mar-6 | ADP Employment Change | 190k | 183k | 300k |

| Mar-7 | ECB Main Refinancing Rate | 0.000% | 0.000% | 0.000% |

| Mar-7 | Initial Jobless Claims | 225k | 223k | 226k |

| Mar-8 | Housing Starts | 1195k | 1230k | 1037k |

| Mar-8 | Change in Nonfarm Payrolls | 180k | 20k | 311k |

| Mar-12 | CPI YoY | 1.6% | — | 1.6% |

| Mar-13 | PPI Final Demand YoY | 1.9% | — | 2.0% |

| Mar-13 | Durable Goods Orders | -0.6% | — | — |

| Mar-14 | Germany CPI YoY | 1.6% | — | 1.6% |

| Mar-14 | Initial Jobless Claims | 225k | — | 223k |

| Mar-14 | New Home Sales | 625k | — | 621k |

| Mar-15 | Eurozone CPI Core YoY | 1.0% | — | 1.0% |

Strengths

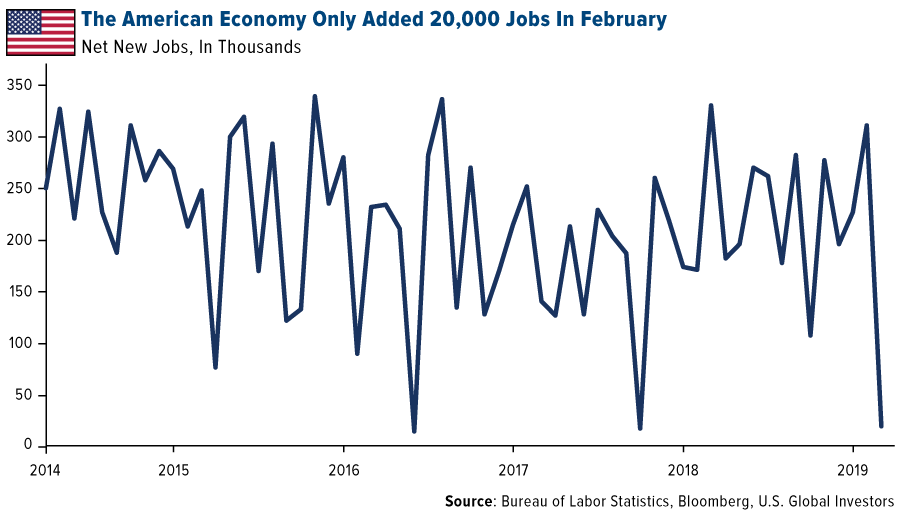

- The best performing metal this week was silver, up 0.87 percent and rallying strong on Friday alongside gold. Gold traders were again split this week on their outlook for gold as U.S.-China trade talks remain in the headlines. The yellow metal advanced the most in two weeks on Friday morning as investors awaited the release of the February jobs report for clues on the health of the economy, according to Bloomberg data. The jobs report showed that hiring slowed in February, with the economy only adding 20,000 jobs.

- China grew its gold reserves for the third straight month to 60.26 million ounces, up from 59.94 million ounces in January, according to data on the People’s Bank of China website. Robin Bhar, head of metals research at Societe Generale SA said: “Ongoing efforts to diversify total reserves – away from the U. S. dollar – have prompted gold purchases by the PBOC, which we believe will continue.” Physical gold demand also picked up in major Asian hubs this week, as bullion was sold at a premium for the first time in more than three months in India, the world’s second largest consumer, according to Reuters.

- Rhodium, palladium’s lesser known sister, rose to a nine-year high this week. Demand for all platinum-group metals mostly comes from autocatalysts used in gasoline cars, which are benefiting as the world steers away from diesel vehicles. Bloomberg writes that palladium has jumped 20 percent so far this year while rhodium is up 19 percent. Australian gold output hit an all-time high in 2018, according to mining consultant Surbiton Associates. The second biggest gold producing nation mined 317 tons of the yellow metal, worth around A$17.3 billion.

Weaknesses

- The worst performing metal this week was platinum, down 4.81 percent as a forecast for wider surplus added to the price erosion. Gold fell to its lowest since January early this week as investors weighted the prospects of a U.S.-China trade deal that could lift tariffs and lessen the appeal of safe haven assets. The Perth Mint reported that gold coin and minted bar sales dropped to an eight-month low in February. Sales fell to 19,524 ounces, down from 31,189 ounces in January. BullionVault’s gold index, that measures the balance of gold buyers against sellers, fell to 52.2 in February, down slightly from the 52.6 reading in January.

- Commodity ETFs saw outflows for the fifth straight week, with investors pulling out $904 million in the week ended March 7, compared with $410 million in the previous period. The VanEck Vectors Junior Gold Miners fund saw outflows of $142.5 million on one day, reducing the fund’s assets by 3.4 percent. ETFs cut 355,901 troy ounces of gold from their holdings and brought this year’s net purchases to 942,406, according to data compiled by Bloomberg.

- De Beers, a major diamond seller, is having the worst start to a year since 2016, selling just $990 million of diamonds in January and February. Bloomberg writes that sales are usually the biggest at the start of the year. The World Platinum Investment Council said in its quarterly report that the platinum surplus will persist for a third year as stronger demand is offset by increasing global supply of the metal. The expected surplus this year is 680,000 ounces, up from 645,000 ounces in 2018.

Opportunities

- RBC says that gold’s recent sell-off “is a buying opportunity for those looking to make medium- to longer-term gold allocations.” The group continues by saying that the gold price risk is skewed to the upside in 2019 and likely in 2020 as well. Goldman Sachs raised its gold and silver forecasts, predicting that late-cycle worries will continue. The bank raised its gold forecasts by $25 an ounce to $1,350, $1,400 and $1,450 an ounce for the three-, six- and 12-month periods. Bank of America forecasts that palladium will extend its rally to $1,800 an ounce by the end of this year and could even go to $2,000.

- According to Ned Naylor-Leyland, manager of the $330 million Merian Gold & Silver Fund, gold’s rally is just the beginning and could take off once investors fully factor in the Fed’s more dovish tone, writes Bloomberg. “I don’t think many investors have probably realized the prime beneficiary of dovish forward guidance is monetary metals,” says Naylor-Leyland. He also says that silver is the best way to drive a return profile in the metals asset class. Economic concerns grew this week on the news that the U.S. trade shortfall grew by more than $100 billion. Bloomberg reports that government revenues, compared with the same month a year earlier, have declined for 10 months in the past year since the Tax Cuts and Jobs Act took effect in January 2018. The Trump administration had promised that the tax cuts would essentially pay for themselves with higher revenue generated by a stronger U.S. economy.

- The government in Zimbabwe is reversing rules that require locals to hold at least a 51 percent stake in platinum mines and will allow foreigners to own a 100 percent stake. This measure is to help stimulate foreign investment. Zimbabwe has the world’s second-largest known reserves of platinum group metals and established deposits of gold, diamonds, lithium and more.

Threats

- Venezuela’s central bank president had been gone for weeks and no one knew where he went. Turns out he was on a tour meeting with officials in ally nations Turkey, China and Russia to discuss financing and banking. The longer the Maduro regime is in power, the longer the potential threat of more selling of gold reserves, which has shown to negatively affect the gold price globally by adding more supply to the market as in the prior week.

- The drama surrounding Barrick Gold Corp’s attempt to woo Newmont Mining Corp continues. Barrick’s biggest shareholder, Joe Foster of the VanEck International Investors Gold Fund, opposes the acquisition and instead is pushing for a joint venture between the two gold mining giants. Additionally, Newmont’s board unanimously rejected Barrick’s $17.8 billion takeover bid, saying that the previously announced takeover of Goldcorp would be better for the company. Barrick CEO Mark Bristow said that they will “definitely not” withdraw the hostile offer for Newmont.

- Sibanye Gold, South Africa’s top gold miner, said this week that the nation’s double-digit electricity price increase could pose a threat to even more jobs as the viability of mines comes into question. South Africa’s power regulator approved a 13.8 percent hike in tariffs by the state-owned utility, which is higher than the 9 percent increased planned on by Sibanye, writes Bloomberg. A spokesman for the company said that “these kinds of increases, well above inflation, pose a risk to the sustainability of the industry and to job creation.” The price of gold would need to increase to keep up mine viability. Sibanye is already considering cutting more than 6,000 jobs amid unprofitable gold shafts.

Index Summarys

- The major market indices finished down this week. The Dow Jones Industrial Average lost 2.21 percent. The S&P 500 Stock Index fell 2.16 percent, while the Nasdaq Composite fell 2.46 percent. The Russell 2000 small capitalization index lost 4.26 percent this week.

- The Hang Seng Composite lost 2.19 percent this week; while Taiwan was down 1.42 percent and the KOSPI fell 4.36 percent.

- The 10-year Treasury bond yield fell 12 basis points to 2.63 percent.

Domestic Equity Market

Strengths

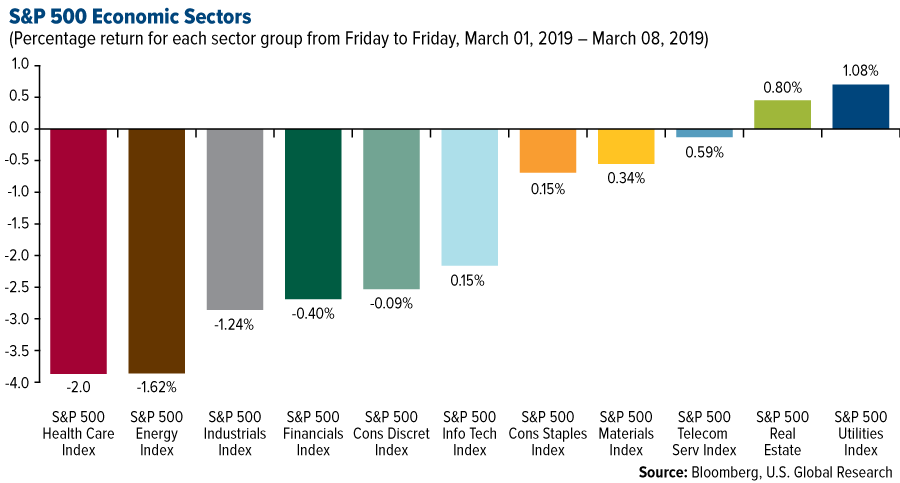

- Utilities was the best performing sector of the week, increasing by 0.70 percent versus an overall decrease of 2.13 percent for the S&P 500.

- Dollar Tree was the best performing stock for the week, increasing 6.27 percent.

- Shares of Target jumped earlier in the week after the retailer reported that last year saw the highest comparable sales growth since 2005, reports Business Insider. Its comparable sales grew at a rate of 5 percent last year, and by 5.3 percent in the fourth-quarter. According to the article, digital sales continue to be a fast-growing area for the retailer as well.

Weaknesses

- Health care was the worst performing sector for the week, decreasing by 3.87 percent versus an overall decrease of 2.13 percent for the S&P 500.

- Kroger was the worst performing stock for the week, falling 12.67 percent.

- Blue Apron, a popular meal-kit maker, saw its shares tumble over 12 percent earlier this week to below $1, reports Business Insider. The stock has tumbled more than 27 percent since Wednesday, when Bessemer Venture Partners sold a block of 15 million shares at an 11percent discount to the prior day’s closing price, the article continues.

Opportunities

- Late last week Lyft kicked off the final sprint of the IPO process, publicly filing its S-1. According to a previous article from Reuters, the company expects to be valued between $20 billion and $25 billion in its IPO. We could see the Uber competitor go public as soon as April.

- Apex Legends, a challenger video game to the popular Fortnite, has reached 50 million players in its first month. The company behind the new game is Electronic Arts. During its first day of being released, more than 2 million players downloaded Apex Legends, reports Business Insider.

- With seven of the 11 indicators in Bloomberg Intelligence’s (BI) market-health checklist in the green following a sour fourth quarter, the research group thinks the U.S. stock-price recovery has a solid foundation, write strategists Gina Martin Adams and Michael Casper. A likely EPS trough and steady growth in domestic cyclicals aid the profit backdrop. Technical sentiment remains cautious despite robust price momentum and breadth. Bond-market indicators are generally supportive, albeit imperfect, with a portion of the yield curve inverted and volatility signaling rates complacency, the two strategists explain.

Threats

- According to a recent study commissioned by Facebook, more than half of people do not feel confident in regards to their privacy online. A look at the Inclusive Internet Index reveals that fewer people are sharing details about themselves online. For firms like Facebook that relay on such data to target advertising, this trend could be a threat.

- Southwest began selling tickets to Hawaii – good news for consumers and travelers, and not so great for Hawaiian Airlines. Shares of Hawaiian Airlines fell nearly 11 percent at the start of the week. Deutsche Bank analyst Michael Lindberg called the new Southwest option to the island state a “direct threat” to its competitor’s business model, reports Business Insider.

- The bull case for Tesla might be a bit shaky these days, according to Barclays. “Much of the bull narrative has rested on Tesla being the next Apple, selling high-volume EVs at premium price point and at high gross margins, in part aided by a unique branded retail presence — a narrative we see as undermined by the recent price cuts and closing of most of the stores,” Barclays analyst Brian Johnson wrote Tuesday.

The Economy and Bond Market

Strengths

- Average hourly earnings increased by 3.4 percent year-over-year, the greatest increase since the economic recovery began. Economists expected a wage increase of 3.2 percent. That compares with a 1.5 percent increase in the consumer price index (CPI) for all urban consumers from January 2018 to January 2019.

- The unemployment rate fell to 3.8 percent in February, according to the Labor Department. The unemployment rate had been projected at 3.9 percent, a small decrease from January’s 4 percent.

- Housing starts in January saw an 18.6 percent increase from December, providing some hope that the market is recovering from a lackluster 2018. Building permits also rose, up 1.4 percent from the previous month.

Weaknesses

- Job growth came to a near standstill in February after a big start to the year, with nonfarm payrolls increasing by just 20,000. It was the worst month for job creation since September 2017, when two major hurricanes hit the employment market. February disappointed modest expectations of 180,000 from economists surveyed by Dow Jones.

- The trade war with China cost American consumers $1.4 billion each month last year. “The entire incidence of the tariffs fell on domestic consumers and importers up to now, with no impact so far on the prices received by foreign exporters,” economists Mary Amiti, Stephen Redding and David Weinstein wrote in a study by the New York Federal Reserve, Princeton and Columbia.

- After years of rapid growth, year-over-year increases in construction spending slowed to 0.85 percent in December, the lowest rate of increase since 2011, according to federal data. While construction spending growing, the industry is no longer experience the double-digit year-over-year increases that were common between 2014 and 2016. Both residential and commercial construction spending fell. Only $39 billion was spent on residential projects in December, compared to $41 billion the year before. Commercial spending declined 3 percent.

Opportunities

- U.S. officials are preparing a final trade deal that President Trump and his Chinese counterpart Xi Jinping could sign in the coming weeks, people familiar with the matter said, even as the debate continues in Washington over whether to push Beijing for more concessions. The U.S. is eyeing a summit between the two presidents as soon as mid-March.

- Moody’s said New York’s strengthening and diversified economy has made the biggest U.S. city less reliant on the volatile financial services industry. The rating company also noted decreased costs for debt service, pensions and retiree health care. As a result, the rating on about $38 billion in outstanding New York City general-obligation bonds was raised one step to Aa1, the second highest level.

- Solid income results in the latest personal income and spending data supply a compelling signal that consumption will rebound in the near term, write BE’s Carl Riccadonna and Tim Mahedy. Consumers appeared to recoil in December in response to financial market turmoil and concerns related to the government shutdown. A pullback in spending amid solid income gains resulted in a spike in the household savings rate, which is consistent with a drop in consumer attitudes recorded around that time. Since then, metrics of consumer sentiment and confidence have rebounded. This is an encouraging signal that the savings rate will retrace.

Threats

- The Organization for Economic Cooperation and Development (OECD) cut its global growth forecast to 3.3 percent from 3.5 percent, saying the global economy is “facing increasingly serious headwinds.”

- Signs on global growth at the start of 2019 flag the possibility of a sharper slowdown, writes Bloomberg Economic’s Tom Orlik. Europe is weaker than expected, with Italy in recession and Germany stumbling. Leading indicators on global trade point to a slump.

- President Trump has announced his plans to end key trade preferences for India and Turkey in the latest move by the U.S. to counter what it calls unfair trade practices. Trump notified Congress yesterday in letters of his “intent to terminate” trade benefits for both countries under the generalized system of preferences. The notification starts a 60-day countdown before the president can take the action on his own authority, the U.S. Trade Representative’s Office said in a statement.

Energy and Natural Resources Market

Strengths

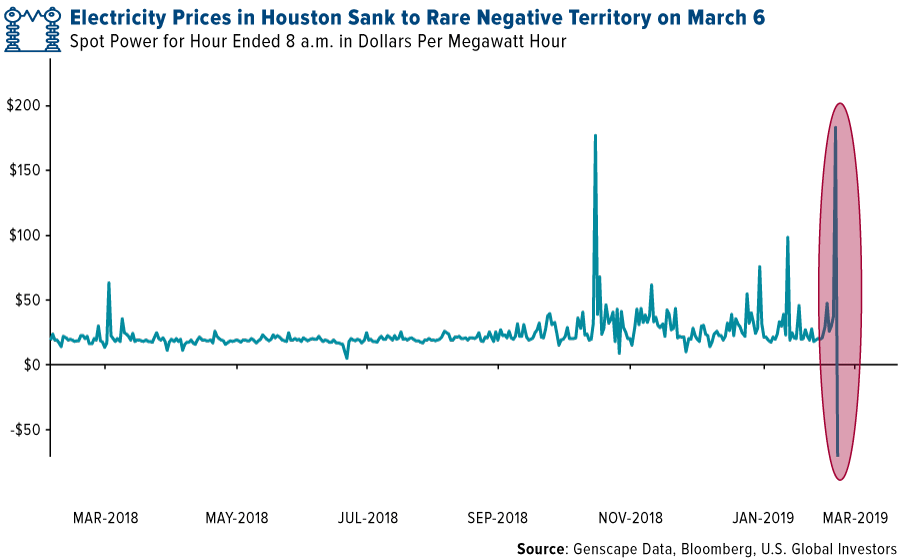

- The best performing major commodity for the week was lumber, which gained 2.69 percent on Thursday. On Wednesday morning, electricity generation was so abundant in Texas that wholesale power prices at a hub in Houston fell below zero to average negative $71.06 per megawatt-hour, reports Bloomberg, looking at Grenscape data. This is due to the growing amount of wind power, which has led to more frequent instances of negative pricing as the grid trying to get rid of power it can’t store. In other wind power news, Microsoft is set to sign two 15-year contracts to buy output from a wind farm in Ohio run by EDP Renovaveis. This amounts to about 1.4 gigawatts of renewable energy.

- In the solar energy world, the Australian market for consumer technology is beginning to form an “S-curve,” which is a sign of growing adoption. About one in five households have rooftop solar, with sales growing significantly since 2010. China plans to ease its solar subsidy program to help keep its market intact, according to JinkoSolar Holding, a top producer. The company is increasing its production capacity by 20 percent this year to keep up with growing demand.

- Argentina’s Mining Secretary Carolina Sanchez said that she expects lithium output to soar in 2021 when output from new projects is expected to hit the market. The country’s lithium production last year was 37,000 tons and is expected at 40,000 to 41,000 tons in 2019. Morgan Stanley has raised its price forecast for iron ore by 30 percent to $81 per ton due to near-term market tightness after Vale slashed its production by 75 million tons.

Weaknesses

- The worst performing major commodity for the week was wheat, which fell 4.68 percent on signs that favorable weather from Russia to North America may make for abundant supplies. On Monday, China’s import premium over the LME price for purchases of refined copper dropped to the lowest level in 22 months, writes Bloomberg. Most base metals declined on Wednesday after the Organization of Economic Cooperating and Development (OECD) said that it downgraded almost every growth forecast for Group of 20 nations and the European Central Bank (ECB) official announced they are going to cut inflation and economic projections. Bloomberg writes that nickel and copper led the declines. China’s top producer of aluminum, Aluminum Corp of China, says that demand growth for the metal will be down in 2019. On the other hand, a top Russian producer, Rusal, sees faster global aluminum growth this year despite the Chinese slowdown. Zinc had its worst week in four months as weak Chinese trade data sparked concerns about growth.

- Oil demand in China is set to rise 13.2 million barrels per day in 2019, which is up from 12.9 million from last year. However, this is the slowest pace of growth in a decade. According to Morgan Stanley, oil consumption in China will peak in 2025 due to the growing shift to electric cars. Although negative for the oil industry, this is positive for electric car makers and miners of metals used in renewable energy. The Trump administration is trying to make big cuts to the U.S. Energy Department division charged with renewable energy and energy efficiency research. A proposed 2020 budget would cut its $2.3 billion budget by 70 percent to $700 million.

- After speculation for weeks that China had placed a ban on Australian imports of coal, Australia reports that coal processing times are slower than normal and China maintains that there are no country-specific restrictions in place. Could China be tightening supply to boost prices? Bloomberg reports that spot thermal coal at one of its ports rose 4.7 percent to 628 yuan per ton in a week to March 4, the biggest increase since mid-August, according to China Coal Resource. China’s coal imports fell 42 percent in February from the previous month.

Opportunities

- China’s top gold producer, Jiangxi Copper, is set to acquire a 29.99 percent stake in Shandong Humon Smelting in order to treat it as its gold business development platform and increase its position in copper. Ernst & Young predicts that copper will follow gold’s path with a rise in merger and acquisition activity due to growing demand for the metal. Analysts at Sanford C. Bernstein write that the nickel supply will not meet demand from electric vehicles by the mid-2020s without significantly greater investment in new capacity. They add that a global deficit will deepen every year until at least 2025.

- Cheniere Energy, one of the pioneers of U.S. natural gas exports, could end up a big winner from a potential trade deal with China, writes Bloomberg’s Simon Casey, as there could be an agreement from China to buy $18 billion of fuel from the company. ExxonMobil plans to boost capital spending by 24 percent to about $32 billion as it searches for oil, constructs natural gas plants and expands refineries, writes Bloomberg’s Kevin Crowley. The company also plans to raise $15 billion through asset sales by the end of 2021.

- Britain plans to construct an industry-leading car battery factory to boost its exposure to the electric vehicle market. Bloomberg writes that this move would help bring new jobs, as local automakers have announced they would cut jobs amid the slump in diesel. According to a director at Japan’s Ministry of Economy, Trade & Industry, public and private sectors have committed $6 billion to U.S. shale projects or a Mozambique LNG export venture. This is part of the $10 billion investment over five years that the country pledged in 2017 to help nations build infrastructure to spur demand for LNG. About $4 billion of the money is already helping finance developments in Bangladesh and Indonesia.

Threats

- According to an assessment by the Environmental Integrity Project, Earthjustice and other groups, the power industry’s own data shows widespread groundwater contamination near sites that store coal ash. These groundwater wells used by 265 coal power plants reveal unsafe levels of arsenic, lithium and other pollutants in most of them. Bloomberg writes that every year U.S. power plants alone produce around 100 million tons of coal ash that is normally stored in landfills and disposal ponds. Argentina is set to present a long-considered bill that would regulate mining waste treatment, reports Bloomberg. Mining Secretary Carolina Sanchez said that the legislation will establish good mining practices and regulate mine closures. This is positive from an environmental and worker safety perspective, but negative for miner costs. Ultimately, higher metal prices will be needed.

- Natural gas is being pushed out of homes as governments battle climate change and falling renewable energy costs, reports Bloomberg. In New York a utility placed a moratorium on new residential hookups of natural gas, and the Netherlands is outlawing new service connections permanently. California and the United Kingdom are also considering similar measures. Barry Perry, CEO of utility owner Fortis, said that “we are headed toward electrifying everything.” Fracking has made natural gas abundant and global consumption is forecast to grow 17 percent by 2030. However, bans on new residential use could cut into this demand forecast.

- Norway’s $1 trillion sovereign wealth fund, the largest such fund in the world, is divesting out 134 oil and gas companies that focus purely on exploration and extraction. This amounts to about $7.5 billion in investments pulled out and is a symbolic blow to the fossil fuel industry. The director of oil and gas research at Hannam & Partners said that “this decision could also trigger other large investors to review their stance toward investing in the oil and gas sector.” Renewable energy sources are becoming increasingly popular, which has investors worrying about traditional fossil fuels.

Emerging Europe

Strengths

- Romania was the best performing country this week, gaining 2.4 percent. The country’s Finance Minister is discussing options to lower the tax on banks’ assets. The details are not out yet, but government bonds may be excluded from taxable banks’ assets. In addition, taxes linked to the Romanian Interbank Offer Rate (ROBOR) could be replaced with an annual fixed tax.

- The Russian ruble was the best relative performing currency this week, losing 70 basis points against the U.S. dollar. This week Russia successfully issued seven- and 15-year ruble bonds. February’s composite PMI reading spiked to 54.1, mostly due to a stronger services PMI number. Manufacturing PMI remains above the 50 level that separates growth from contraction.

- Information technology was the best performing sector among eastern European markets this week.

Weaknesses

- Greece was the worst performing country this week, losing 2.3 percent. Stocks trading on the Athens exchange corrected after recording strong gains over the past two months. Gross domestic product for 2018 came in at 1.6 percent, versus the prior year’s reading of 2.2 percent. On a positive note, manufacturing PMI ticked higher to 54.2 in February from 53.7 in January.

- The Turkish lira was the worst performing currency this week, losing 1.3 percent against the U.S. dollar. Central banks left the main rate unchanged at 24 percent, and as expected. Inflation declined below 20 percent. Local elections will take place on March 31.

- Utilities was the worst performing sector among eastern European markets this week.

Opportunities

- The Greek government successfully issued 10-year bonds, making this the first 10-year issuance in almost a decade, rising 2.5 billion euros. On Friday, Moody’s rating agency upgraded Greece two notches to B1 from B3; still below the investment grade, but with a positive outlook. Greece remains among the most fragile economies in the eurozone, but the situation is improving after the country’s bailout program ended last year. Greek bonds are attractive to carry traders; 10-year Greek bonds pay around 3.5 percent versus less risky German10-year bonds, which have a yield of 0.17 percent.

- Norway’s oil fund, the world’s largest sovereign fund currently worth more than $1 trillion, increased its Turkish holdings since the end of December 2018, totaling $707 million. Turkish energy companies were the most attractive to Norway’s fund managers, with the biggest investments in the refinery Turkiye Petrol Rafinerileri and Eregli Demir ve Celik Fabrikalari, a steel maker, accounting for 1.02 percent and 0.59 percent, respectively.

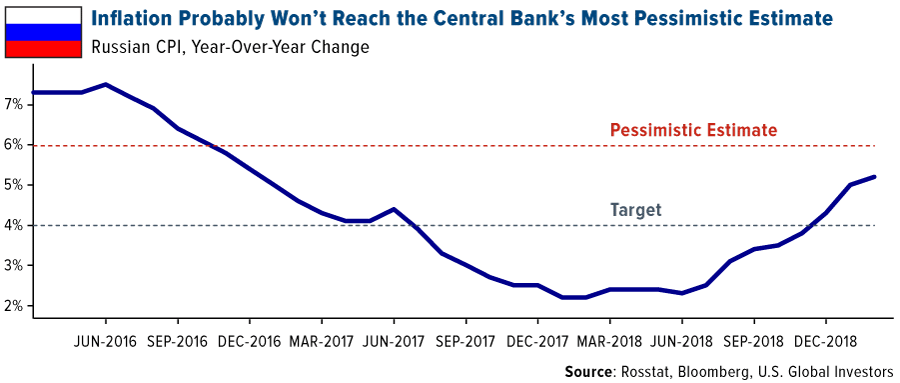

- Inflation in Russia came in slightly higher at 5.2 percent in February. A spike to 6 percent is unlikely, although previously predicted due to tax increases. Weak consumer demand keeps inflation stable and may allow the central bank to cut rates at the end of the year.

Threats

- President Donald Trump said on Monday that he plans to end key trade preferences for India and Turkey. He intends to end trade benefits for both countries under the generalized system of preference, which allows duty-free entry of about 2,000 products including auto parts, industrial valves and textile materials. Turkey was the fifth largest beneficiary of the program with $1.7 billion in covered imports. Trump said that Turkey is no longer a developing country, based on the level of its economic development, and no longer needs to utilize the generalized system of preference program in its trades in the U.S.

- A ban on new Russian debt could have a long-term negative effect on the ruble rate, as foreign investors likely will not reinvest the funds they receive from redemptions and coupon payments, according to Bloomberg. On the other hand, Maxim Orlovsky, managing director at Renaissance Capital, estimates that a potential U.S. ban on purchases of new sovereign debt could lift the rate on ruble bonds by as much as 2 percent to 10 to 10.5 percent. At the same time, due to the concentration of foreign investors, Eurobond yields could climb by further by 1 to 2 percent, depending on the maturity date.

- The European Central Bank (ECB) lowered the eurozone’s growth forecast for this year from 1.7 percent to 1.1 percent, citing weakness in Italy and uncertainties surrounding Brexit. To help the economy, the bank announced that it will launch another stimulus plan. A new series of quarterly targeted longer-term refinancing operations will be launched in September 2019 and end in March 2021. The mechanism was previously introduced for the first time in 2014 and a second time in March of 2006. Concerned with the economic slowdown, the ECB also left all rates unchanged and pushed forward the date for future rate hikes.

China Region

Strengths

- The Philippines Stock Exchange Index jumped 2.03 percent on the week, while India’s Nifty and SENSEX Indices climbed 1.58 and 1.68 percent, respectively.

- Information technology was the only sector in the Hang Seng Composite Index to close out the week in the green, rising 1.48 percent.

- The Philippines saw inflation continue to drop from its latter-2018 scorching levels, down to 3.8 percent for the February measurement period, below expectations for 4.0 percent and down from the prior month’s 4.4 percent reading.

Weaknesses

- The Hang Seng Composite Index fell by 2.19 percent for the week, while Indonesia’s Jakarta Composite declined by 1.80 percent. Korea’s KOSPI, which did not trade last Friday, dropped 2.64 percent since last Thursday.

- The materials sector was the worst-performing one in the Hang Seng Composite Index for the week, dropping 4.57 percent.

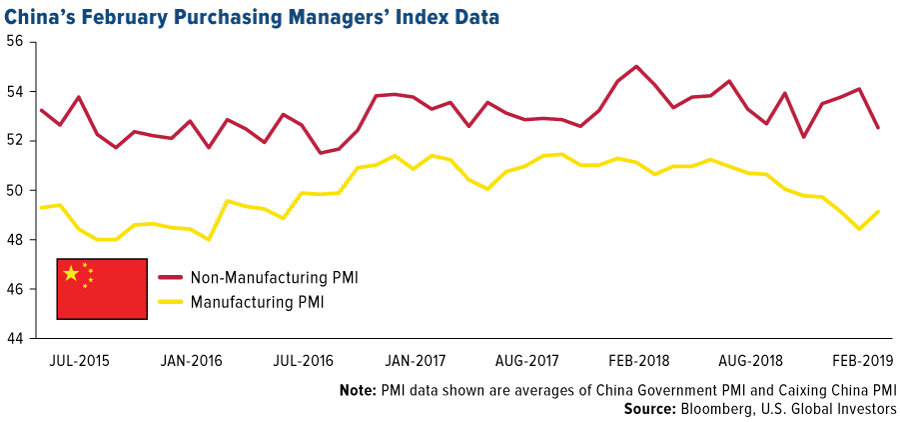

- The Caixin Services PMI missed expectations, coming in at only 51.1 for the February period, well below the expected consensus print of 53.5 and down from the prior month’s 53.6 reading. The reader may also recall that last week’s data showed China’s official Manufacturing PMI gauge at only 49.2, short of expectations, and an official Non-manufacturing PMI at 54.3, also slightly short of expectations. The Caixin Manufacturing PMI did beat, however, last week, when it came in at the mildly contractionary 49.9 level.

Opportunities

- This week we are now officially past the original tariff deadlines set (and now extended) by President Donald Trump as China and the U.S. continue to work toward resolving the trade disputes. While the high-profile international back-and-forth of high-ranking personnel has fallen off the radar this week without photo-ops between capitals, talks remain ongoing with reported progress. A trade deal, done right, remains a potential positive for markets, as is any removal of uncertainty around the tariff situation.

- The Wall Street Journal reported this week that Southeast Asian ride-hailing company Grab Holdings raised $1.46 billion in fresh funding from SoftBank, bringing the total fundraising for the past year to more than $4.5 billion, and valuing the company at some $14 billion, up from $11 billion last year. Grab is now one of the region’s most valuable startups, and the company has stated it intends to deploy “a significant portion of fresh proceeds” into Indonesia, where rival PT Go-Jek Indonesia is also growing rapidly.

- Chinese travel booking site Ctrip.com International had its biggest gain in more than three years earlier in the week after fourth quarter results led to a round of rapid analyst upgrades.

Threats

- U.S.-China trade talks remain ongoing and tariffs remain delayed in implementation; the collapse of the former and the commencing of the latter remain a collective threat until resolution one way or the other.

- It must be noted that on Friday, China’s massive (and state-backed) CITIC Securities issued a sell rating on large insurer PICC (which, to be fair, had soared in recent days). The Shanghai Composite declined by 4.4 percent on the day, and the sell ratings are being interpreted in some corners and by some brokers and research houses as a possible warning from state officials not to let the market (or, perhaps, at a more granular level, individual stocks) get too far ahead of itself (themselves). Indeed, such market sentiment—whether merited or not—may well pose an obvious near-term threat.

- A recent study from the Chinese University of Hong Kong and the University of Chicago argues that China “over-reported its economic growth between 2008 and 2016 by an average of 1.7 percentage points,” Bloomberg News reported the paper as saying. The authors contend that, “Local statistics increasingly misrepresent the true numbers after 2008, but there was no corresponding change in the adjustment made by the NBS” [China’s National Bureau of Statistics, which attempts to revise local numbers to adjust for localities hitting potentially rewarding economic thresholds]. The paper argues that in the authors’ investigation and research, their own revisions to numbers “indicate that the slowdown in Chinese growth since 2008 is more severe than suggested by the official statistics.”

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended March 8 was BitMax Token, up 244.45 percent.

- Bitcoin prices moved higher mid-week, reports MarketWatch, pushing the digital currency closer toward $3,900. “The $4K level is considered by experts as an important resistance and [a move higher] will open the way for further market growth,” wrote Alex Kuptsikevich, financial analyst at FXPro.

- Crypto Facilities, a cryptocurrency futures provider, has seen “tremendous growth,” since being acquired by U.S.-based exchange Kraken last month, writes Coindesk. Sui Chung, the subsidiary’s head of indices and pricing products, explained that trading volume has increased more than 500 percent since the acquisition. In total, that is close to $1 billion in crypto futures traded over the past month, the article continues.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended March 8 was ODUWA, down 52.03 percent.

- Cryptocurrency exchange WEX, successor to the shuttered BTC-e exchange, has once again been linked to Iranian ransomware operators, reports Coindesk. Two Iranians said to have created the SamSam ransomware variant are reportedly tied to the exchange, notes a bulletin from consulting firm PwC, and may have used it to launder their millions in illegal earnings.

- On Monday it was reported that Starbucks could soon be installing Bakkt software to allow customers to pay using bitcoins. Although the option might sound tempting to some, as MarketWatch reports, the “crypto-for-coffee transaction has one glaring pain point: tax reporting.” James Foust, senior research fellow at Coin Center, says “If you were to use bitcoin to buy coffee it is technically feasible, but it would be extremely burdensome for tax purposes.”

Opportunities

- According to data from Canaccord Genuity Capital Markets, there seems to be a close resemblance in trading patterns for bitcoin between the periods 2011-2015 and 2015-2019, reports MarketWatch. “Looking ahead, if bitcoin were to continue following the same trend as in the years 2011-2017, the implication is that bitcoin would be bottoming approximately now and would soon begin climbing back toward its all-time high of ~$20,000, theoretically reaching that level in March 2021,” wrote Michael Graham and Scott Suh of Canaccord Genuity.

- Bitcoin miners in China are buying used equipment and making deals with mining farms and hydroelectric plants, writes Coindesk, betting for a cheap power boom soon. A significant amount of excess electricity is expected to be generated by hundreds of hydropower stations. “This level of excess power results in competitive electricity costs for bitcoin miners, making it perhaps one of the rare opportunities to earn profits in the current bear market that has already impacted the mining sector,” the article continues.

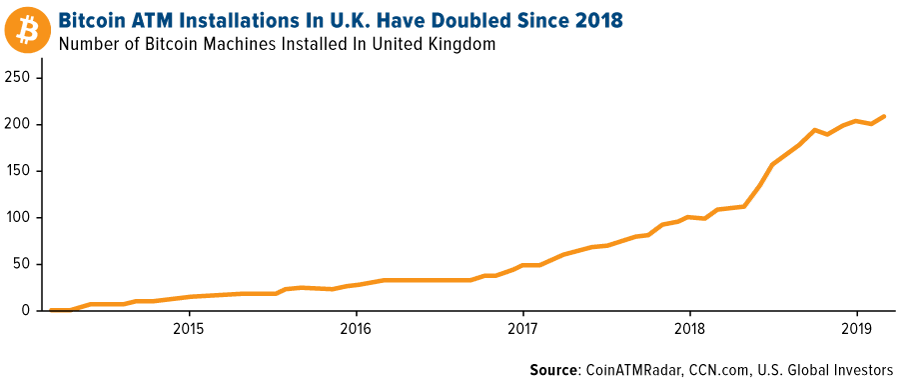

- A new report in the U.K., titled “Access to Cash Review,” says that the country’s cash system will become nearly obsolete in the next 15 years, reports CCN. This comes at a time when digital payments overtook cash for the first time in the U.K. last year. In fact, according to CoinATMRadar, there has been a 100 percent rise in bitcoin ATMs installed in the U.K. since 2018.

Threats

- In the wake of its controversial acquisition of blockchain analytics firm Neutrino (a startup linked to Hacking Team, a group that aided governments known for human rights abuses), Coinbase is now taking steps to clarify recent statements, reports Coindesk. Last Friday, Coinbase’s director of institutional sales Christine Sandler attempted to justify the acquisition in an interview with Cheddar by stating the exchange’s previous analytics provider was “selling client data to outside sources.” But now Coinbase is saying Sandler misspoke, telling Coindesk reporters on Tuesday that the exchange “never shared our customers’ personally identifiable information with any third party blockchain analysis vendors,” the article continues.

- Despite bitcoin’s modest rise this week, some analysts are saying the coin’s continuous struggle below $4,000 isn’t making the best bull case for the currency anymore, reports MarketWatch. “Adoption of cryptocurrency for handling financial transactions is slowing, not accelerating, which puts a devastating dent in the bull case,” said market analyst Jani Ziedins of the Cracked Market blog. “If BTC turns out to be nothing more than a fad, then the $4K price tag is still incredibly expensive and there is still lots of room to fall.”

- Blockchain infrastructure company SETL, based in London, has filed a notice of insolvency today with the U.K. authorities, reports Coindesk, noting that it is looking for “a larger financial services firm” to take on some of its holdings. According to the article, the announcement comes as somewhat of a shock given that, last October, the startup company was granted a license by France’s securities regulator to operate a central securities depository (CSD) system using blockchain technology.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| S&P/TSX Global Gold Index | 195.12 | +6.98 | +3.71% |

| Gold Futures | 1,298.60 | -0.60 | -0.05% |

| Natural Gas Futures | 2.86 | +0.00 | +0.14% |

| S&P/TSX VENTURE COMP IDX | 618.08 | -7.08 | -1.13% |

| 10-Yr Treasury Bond | 2.63 | -0.13 | -4.54% |

| Nasdaq | 7,408.14 | -187.21 | -2.46% |

| Oil Futures | 55.98 | +0.18 | +0.32% |

| Hang Seng Composite Index | 3,795.66 | -84.95 | -2.19% |

| S&P 500 | 2,743.07 | -60.62 | -2.16% |

| DJIA | 25,450.24 | -576.08 | -2.21% |

| Korean KOSPI Index | 2,137.44 | -97.35 | -4.36% |

| Russell 2000 | 1,521.88 | -67.76 | -4.26% |

| S&P Energy | 469.77 | -18.88 | -3.86% |

| S&P Basic Materials | 341.60 | -1.90 | -0.55% |

| XAU | 76.02 | +1.98 | +2.67% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.86 | +0.20 | +7.55% |

| S&P/TSX Global Gold Index | 195.12 | +5.01 | +2.64% |

| 10-Yr Treasury Bond | 2.63 | -0.07 | -2.45% |

| Oil Futures | 55.98 | +1.97 | +3.65% |

| Gold Futures | 1,298.60 | -15.80 | -1.20% |

| S&P 500 | 2,743.07 | +11.46 | +0.42% |

| S&P Energy | 469.77 | -7.60 | -1.59% |

| Hang Seng Composite Index | 3,795.66 | +54.41 | +1.45% |

| DJIA | 25,450.24 | +59.94 | +0.24% |

| Korean KOSPI Index | 2,137.44 | -66.02 | -3.00% |

| Nasdaq | 7,408.14 | +32.86 | +0.45% |

| S&P Basic Materials | 341.60 | +6.48 | +1.93% |

| Russell 2000 | 1,521.88 | +3.86 | +0.25% |

| S&P/TSX VENTURE COMP IDX | 618.08 | -2.44 | -0.39% |

| XAU | 76.02 | +0.66 | +0.88% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.86 | -1.46 | -33.83% |

| 10-Yr Treasury Bond | 2.63 | -0.27 | -9.19% |

| DJIA | 25,450.24 | +502.57 | +2.01% |

| Oil Futures | 55.98 | +4.49 | +8.72% |

| S&P 500 | 2,743.07 | +47.12 | +1.75% |

| Gold Futures | 1,298.60 | +49.00 | +3.92% |

| S&P Energy | 469.77 | -4.62 | -0.97% |

| Nasdaq | 7,408.14 | +219.88 | +3.06% |

| Korean KOSPI Index | 2,137.44 | +68.75 | +3.32% |

| S&P Basic Materials | 341.60 | +9.79 | +2.95% |

| Russell 2000 | 1,521.88 | +44.47 | +3.01% |

| Hang Seng Composite Index | 3,795.66 | +271.80 | +7.71% |

| S&P/TSX Global Gold Index | 195.12 | +23.56 | +13.73% |

| S&P/TSX VENTURE COMP IDX | 618.08 | +52.00 | +9.19% |

| XAU | 76.02 | +9.67 | +14.57% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (12/31/2018):

Hawaiian Holdings Inc.

Southwest Airlines Co.

Eregli Demir ve Celik Fabrikal

Barrick Gold Corp.

Newmont Mining Corp.

VanEck Vectors Junior Gold Miners Fund

Citigroup Inc.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks.

The Russell 2000 Index is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months.

The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange.

The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver.

The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar.

The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500.

The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500.

The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period.

The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500.

The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500.

The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500.

The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500.

The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500.

The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500.

The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns.

The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The Inclusive Internet Index assesses and compares countries according to their enabling environment for adoption and productive use of the Internet.

BullionVault’s Gold Investor Index measures the balance of private investors buying gold to start or grow their holding across the month over those reducing or selling them entirely. A reading of 50.0 means the number of people buying gold across the month was perfectly balanced by the number of sellers.

The NIFTY 50 Index is National Stock Exchange of India’s benchmark broad based stock market index for the Indian equity market.

The BSE SENSEX (also known as the S&P Bombay Stock Exchange Sensitive Index or simply the SENSEX) is a free-float market-weighted stock market index of 30 well-established and financially sound companies listed on Bombay Stock Exchange.

The PSE Composite Index, commonly known previously as the PHISIX and presently as the PSEi, is a stock market index of the Philippine Stock Exchange consisting of 30 companies.

The Korea Composite Stock Price Index or KOSPI is the index of all common stocks traded on the Stock Market Division—previously, Korea Stock Exchange—of the Korea Exchange.