Follow the Trend Lines, Not the Headlines

Date Posted: July 26, 2019

Read time: 54 min

It was quite an eventful week! I was honored to speak alongside some of the best and brightest in the investment industry at the Oxford Club's Private Wealth Seminar held in New York City. I enjoyed hearing from all the speakers at this year's event, especially Alexander Green, chief investment strategist at The Oxford Club.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

It was quite an eventful week! I was honored to speak alongside some of the best and brightest in the investment industry at the Oxford Club’s Private Wealth Seminar held in New York City. I enjoyed hearing from all the speakers at this year’s event, especially Alexander Green, chief investment strategist at The Oxford Club.

Alex spoke to a theme I think most investors can relate to—the importance of remaining positive and looking past the gloom-and-doom headlines that often weigh on the market. I’m a firm believer that your thoughts manifest your future. It’s very hard to make money and be successful when you’re always expecting the worst to happen.

“Follow the trend lines, not the headlines,” President Bill Clinton once said. I’m a news junkie myself, but I guarantee you I wouldn’t be where I am today had I based every one of my investment decisions on what the talking heads tell me.

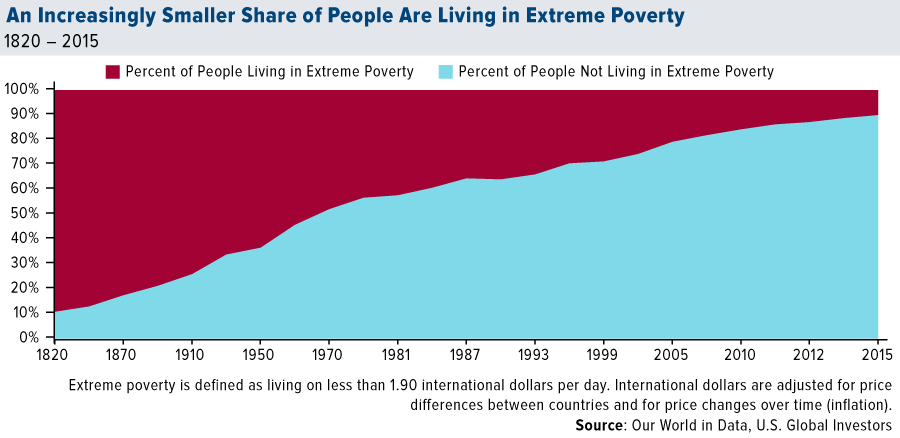

Alex recommended a few positive books that I plan on picking up at some point. Among them are Steven Pinker’s Enlightenment Now, Matt Ridley’s Rational Optimist and Peter Diamandis’ Abundance. All three books, in their own ways, take on the popular misconception that our lives are progressively getting worse. The headlines might make it feel this way sometimes, but the trend lines tell a different story. We’re living longer, healthier and freer lives than we were in years past.

Don’t believe me? Take a look at the chart below, courtesy of research website Our World in Data. It shows that an increasingly smaller percentage of people are now living in extreme poverty compared to earlier times. As recently as 1820, a vast majority of people—close to 90 percent—were living on less than 1.90 international dollars a day. Comfort and abundance were the rare exception, not the rule. Today, thanks to industrialization and liberalization, millions upon millions of people have been lifted out of poverty.

“Unfortunately, the media is overly obsessed with reporting single events and with things that go wrong, and does not nearly pay enough attention to the slow developments that reshape our world,” writes economist Max Roser, founder and editor of Our World in Data.

A Quarter of All Bonds in the World Now Trade at Negative Interest Rates

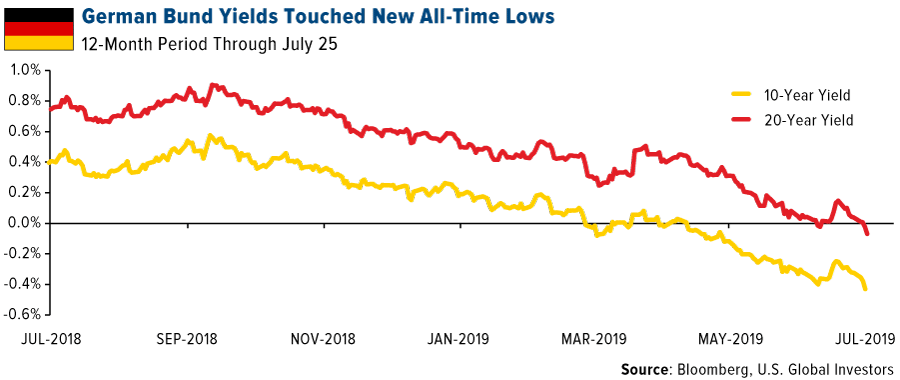

My last day in New York was well spent at the New York Stock Exchange (NYSE), where I was able to speak to a group of media and investment advisors about the world of gold. The yellow metal has been trading above $1,400 for more than a month now as bond yields around the world continue to plumb new all-time lows. As much as $13.64 trillion, equal to 25 percent of all sovereign and corporate bonds, currently have negative yields, meaning investors are paying the issuers for the pleasure of holding their debt.

This week, in fact, German Bunds touched new record lows on manufacturing weakness due to global headwinds such as trade tensions and Brexit. The 10-year Bund yield dropped to minus 0.43 percent on Thursday, while the 20-year Bund fell below zero.

The Bund rally was sparked by the release of factory data that shows that Germany’s manufacturing sector contracted at a faster pace in July. The country’s preliminary purchasing managers’ index (PMI) hit 43.1, down sharply from 45.0 in June and a seven-year low. Output slipped to 44.1, its steepest decline since 2009.

Outgoing president of the European Central Bank (ECB) Mario Draghi called Europe’s economic outlook “worse and worse,” signaling a rate cut next month, as well as a possible new round of quantitative easing (QE).

“It’s getting worse and worse in manufacturing, especially, and it’s getting worse and worse in those countries where manufacturing is very important,” Draghi said.

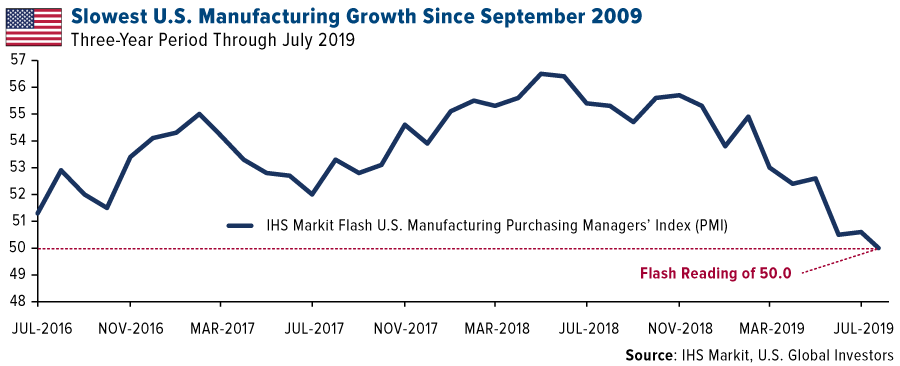

Anticipating a U.S. Rate Cut

A rate cut is also widely expected by the Federal Reserve next week, following similarly disappointing manufacturing and economic news. The U.S. economy slowed in the second quarter, falling to 2.1 percent from 3.1 percent in the previous three-month period. Meanwhile, the U.S. flash PMI sunk to a neutral 50.0, a 118-month low, on lower production volumes, a drop in employment and reduced stocks of purchases. A reading of 50.0 means factories neither expanded nor contracted.

The economy “started the third quarter on a disappointingly soft footing,” commented Chris Williamson, chief business economist at IHS Markit. “Manufacturers are shedding workers at the fastest rate since 2009 and service sector job creation is now down to its lowest since April 2017.”

Williamson added that companies, responding to geopolitical worries, trade tensions and expectations of slower international growth, “may look to tighten their belts further in coming months, dampening spending, investment and jobs growth.”

Chinese Investment Dries Up

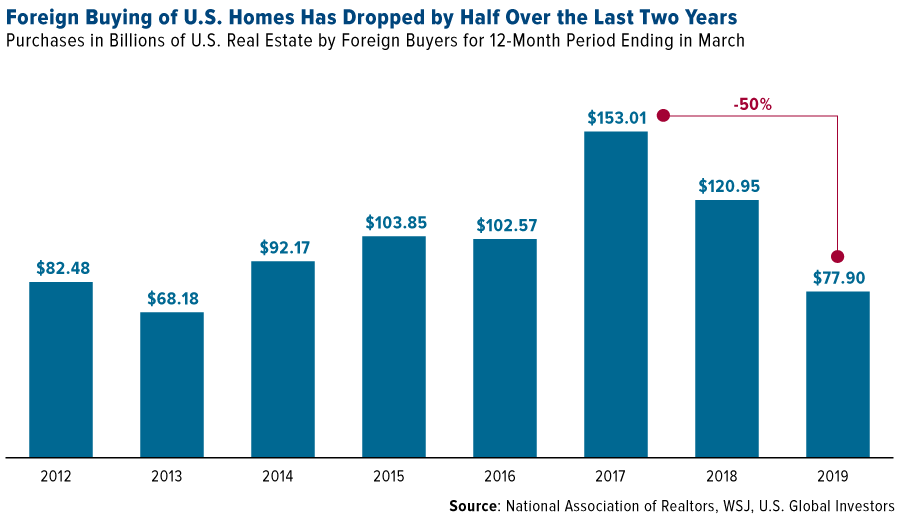

A lot of the slowdown, of course, stems from the very disruptive U.S.-China trade war. Tensions between the two economies have hit supply chains and are affecting nearly every part of the economy, from technology to agriculture to real estate. And this week, economic research firm Rhodium Group released data showing that Chinese foreign direct investment (FDI) in the U.S. has plummeted an incredible 90 percent since President Donald Trump took office. From its peak of $46.5 billion in 2016, Chinese FDI shrank to only $5.4 billion last year.

Again, this is being felt in all corners of the economy. The Wall Street Journal reports that foreign buying of U.S. residences has dropped a record 50 percent in the past two years, from $153 billion to almost $78 billion, the smallest amount since 2013. The pullback, according to the WSJ, is driving price cuts in coastal cities such as New York, Miami and cities in California, and causing new condos to sit empty.

“Generally speaking, we are in the largest market correction since the Great Recession in New York City,” said Martin Eiden, a New York-based realtor. “The foreign buyers have pretty much all but disappeared.”

Follow the Smart Money

Going back to the beginning of my comments, it’s important to stay positive, but it’s just as important to be prepared. A number of trend lines right now—from manufacturing PMI to FDI to the inverted yield curve—point to imminent risks, including a potential economic recession.

One of the ways some big-name money managers are hedging against these risks is with gold. Billionaire investor Paul Tudor Jones told Bloomberg last month that gold was his favorite trade in the next 12 to 24 months as recession fears loom. Ray Dalio, founder of Bridgewater Associates and the most successful hedge fund manager ever, recommended gold in a LinkedIn post earlier in the month, saying that the metal could help investors have a “better balanced portfolio to reduce risk.”

It’s also important to get exposure with high-quality gold stocks. Bridgewater, for instance, holds significant positions in gold across all tiers in the industry, from senior miners to junior miners to royalty and streaming companies (Franco-Nevada, Wheaton Precious Metals and Royal Gold).

What’s good for the goose…

Why are billionaires hungry for gold? Find out by clicking here!

Gold Market

This week spot gold closed at $1,418.80, down $6.57 per ounce, or 0.46 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 2.04 percent. The S&P/TSX Venture Index came in up just 0.16 percent. The U.S. Trade-Weighted Dollar rose 0.87 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Jul-24 | New Home Sales | 658k | 646k | 604k |

| Jul-25 | Hong Kong Exports YoY | -2.3% | -9.0% | -2.4% |

| Jul-25 | ECB Main Refinancing Rate | 0.000% | 0.000% | 0.000% |

| Jul-25 | Durable Goods Orders | 0.7% | 2.0% | -2.3% |

| Jul-25 | Initial Jobless Claims | 218k | 206k | 216k |

| Jul-26 | GDP Annualized QoQ | 1.8% | 2.1% | 3.1% |

| Jul-30 | Germany CPI YoY | 1.5% | — | 1.6% |

| Jul-30 | Conf. Board Consumer Confidence | 125.0 | — | 121.5 |

| Jul-31 | Eurozone CPI Core YoY | 1.0% | — | 1.1% |

| Jul-31 | ADP Employment Change | 150k | — | 102k |

| Jul-31 | FOMC Rate Decision (Upper Bound) | 2.25% | — | 2.25% |

| Jul-31 | Caixan China PMI Mfg | 49.6 | — | 49.4 |

| Aug-1 | Initial Jobless Claims | 215k | — | 206k |

| Aug-1 | ISM Manufacturing | 52.0 | — | 51.7 |

| Aug-2 | Change in Nonfarm Payrolls | 166k | — | 224k |

| Aug-2 | Durable Goods Orders | — | — | 2.0% |

Strengths

- The best performing metal this week was platinum, up 2.24 percent on hedge funds cutting short positions and flipped the futures composite to a net long. Gold traders and analysts in the weekly Bloomberg survey are split between a bullish and a neutral outlook on the yellow metal ahead of the Fed’s meeting next week. Gold gained on Thursday after the European Central Bank (ECB) signaled low interest rates are ahead. Just like last week, Turkey saw its gold reserves rise. According to the central bank, holdings rose $58 million from the prior week.

- Silver went on a tear last week and investors sure noticed. Bloomberg reports that investors have flooded into ETFs backed by silver, with holdings surging to the highest on record. The iShares Silver Trust saw $146.5 million in inflows on Monday, the most since 2013. Then on Tuesday, assets rose 818.8 tons, which is the largest daily increase on record.

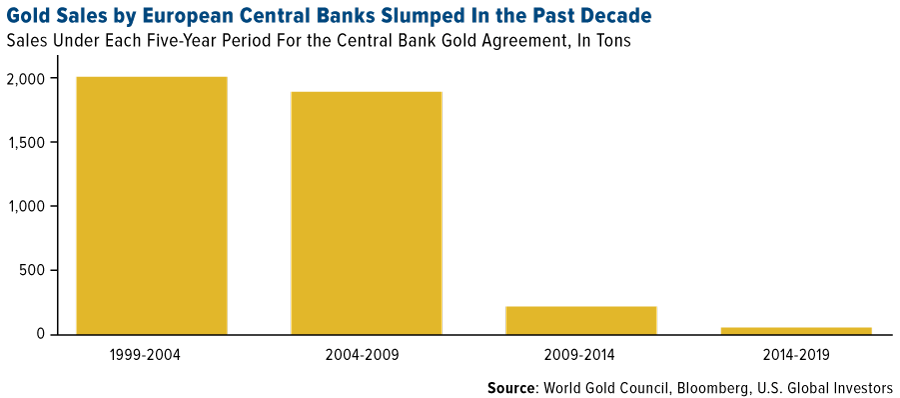

- European central banks have been slowing gold reserve selling for years. This week the ECB and its peers decided to allow an agreement on coordinating gold sales to expire, saying that it has become obsolete, reports Bloomberg. The pact is scheduled to end on September 26 and member institutions said they don’t currently have plans to sell “significant amounts” of the yellow metal.

Weaknesses

- The worst performing metal this week was gold, down 0.46 percent, partly on some stronger economic data and how that might affect the interest rate decision at the FOMC meeting next week. Gold is heading for its first weekly drop in three weeks as investors weigh on solid U.S. economic data, reports Bloomberg. According to Commerce Department figures, orders placed with U.S. factories for business equipment posted the biggest gain in more than a year. Holdings in gold-backed ETFs fell for a third day on Thursday.

- On Tuesday President Trump rejected aggressive moves to weaken the dollar that would boost trade during a meeting. Trump’s economic advisor Larry Kudlow told CNBC that the administration had “ruled out” a currency intervention. A weaker dollar has historically been positive for gold and just weeks ago there was talk of weaker dollar policy. From the news reporting, it is not clear that President Trump even attended the meeting; he has been a vocal proponent of lowering the value of the dollar.

- Newmont Goldcorp, the recently-crowned world’s largest gold miner, reported lower than expected second quarter adjusted profits and saw its shares fall 3.4 percent pre-market on Thursday. The company said costs rose amid shutdowns at two newly acquired mines.

Opportunities

- Chirage Mehta, senior fund manager at Alternative Investments, Quantum AMC, wrote a piece outlining reasons why gold should be an essential part of a portfolio. Those four reasons are: rising economic nationalism, the detiorating quality of reserve assets, central banks buying gold and non-dollar trade agreements. Mehta writes that gold is a strategic asset because it has low correlation to other asset classes, is liquid and has a history of improving portfolio risk-adjusted returns.

- Citigroup also praised gold this week. The group says it is bullish on bullion due to the possibility of the Fed cutting rates next week. “We think late second quarter may have represented a structural regime shift for the yellow metal” and that “gold should benefit in this environment” of easing monetary policy. The report says that a sustainable push above $1,500 an ounce this year and a $1,600 target in late 2020 seems plausible.

- JPMorgan research shows that no reserve currency lasts forever and many are questioning how long the U.S. dollar’s reign will last. Reserve currencies tend to be a reflection of markets that have the best prospects. JP Morgan sees the younger demographics and proliferating technological know-how of the Asian economic zone as having the best prospects with 50 percent of global GDP and two-thirds of global economic growth being the strongest contender. With $30 trillion in middle-class consumption growth forecast between 2015 to 2030, only $1 trillion is expected to come from Western economies. The bank sees the dollar deprecating over the medium term due to these structural reasons as well as cyclical impediments, which is why they recommend diversifying into developed markets and in Asia, as well as precious metals.

Threats

- UBS strategist Joni Teves wrote this week that gold investors should be cautious going into the FOMC meeting next week. Teves said “there is a risk that recent gold positions could come under pressure in the near term if the Fed is perceived to be more hawkish than the market is currently expecting.”

- Newcrest Mining and Harmony Gold Mining have hit a snag in the development of a key $5.4 billion mine in Papua New Guinea, reports Bloomberg. The permitting of the companies’ gold-copper project has been delayed for an unknown duration. This could be largely due to the fact that the nation’s newly elected prime minister is a critic of resource deals signed with multi-national corporations.

- Despite a big rally in gold in the last few weeks, mining companies likely won’t see that reflected in earnings for the second quarter. Gold is up 11 percent this year, but those benefits won’t show up until third quarter earnings, due to pricing lags, according to Bloomberg.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 0.14 percent. The S&P 500 Stock Index rose 1.65 percent, while the Nasdaq Composite climbed 2.26 percent. The Russell 2000 small capitalization index gained 2.01 percent this week.

- The Hang Seng Composite lost 1.09 percent this week; while Taiwan was up 0.17 percent and the KOSPI fell 1.34 percent.

- The 10-year Treasury bond yield rose 2 basis points to 2.073 percent.

Domestic Equity Market

Strengths

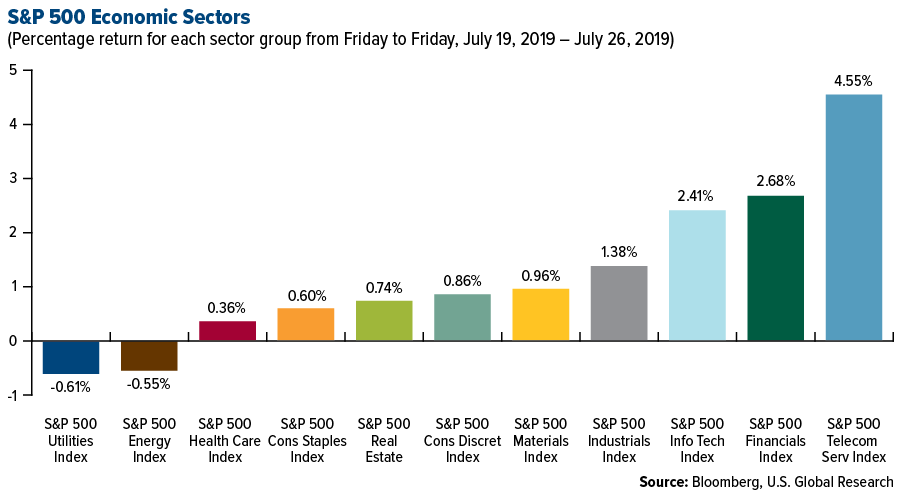

- Communication services was the best performing sector of the week, increasing by 4.55 percent versus an overall increase of 1.67 percent for the S&P 500.

- United Parcel Service was the best performing stock for the week, increasing 16.72 percent.

- Anheuser-Busch InBev (AB InBev) beat earnings expectations as beer sales grew at their fastest pace in over five years, reports Reuters. The maker of Budweiser, Corona and Stella Artois said on Thursday that beer volumes rose by 2.1 percent year-on-year in the April to June period.

Weaknesses

- Utilities was the worst performing sector for the week, decreasing by 61 basis points versus an overall increase of 1.67 percent for the S&P 500.

- Align Technology was the worst performing stock for the week, falling 29.29 percent.

- Big tech saw an antitrust wipeout as $33 billion was erased from the value of Amazon, Apple, Facebook and Google, reports Business Insider, after the U.S. Department of Justice (DOJ) announced a probe. The DOJ said Tuesday that it’s launching a broad probe into whether online platforms are illegally harming their competitors and stifling innovation.

Opportunities

- AT&T impressed with quarterly phone subscriber estimates. The company beat Wall Street estimates for net wireless subscribers who pay a monthly bill, as the telecommunications titan grinded out growth in a saturated market and bundled media content from Time Warner into new wireless plans.

- Volkswagen on Thursday said its first half operating profit rose 10.3 percent to $10.02 billion, pushed higher by a jump in demand for Porsche vehicles. Higher demand for VW, Porsche and Skoda cars helped to offset a drop in Audi sales, the carmaker said.

- WeWork is reportedly expected to IPO in September, earlier than investors had thought. A Wall Street Journal report said WeWork has plans to shore up a $5 billion to $6 billion asset-backed loan in the coming weeks that will decrease the amount it needs to raise in its IPO.

Threats

- Nissan announced Thursday it will axe 12,500 jobs after first quarter profit dropped 98.5 percent, reports Reuters. The changes would take place by 2022, as Japan’s no.2 auto maker aims to rein in costs as it suffers from sluggish sales and rising costs and tries to recover from a scandal surrounding ousted Chairman Carlos Ghosn.

- Deutsche Bank posted a bigger loss than expected after taking a $3.8 billion charge to slash jobs and overhaul the bank. Credit Suisse analysts said the loss was wider than the $2.8 billion loss the bank previously flagged to the market, and called the results "disappointing" in a note to clients.

- Tesla’s shares crashed in premarket trading — falling as much as 12 percent after a disappointing second quarter earnings report. The company lost over $400 million in the second quarter despite record sales, especially of its new Model 3. This throws the carmaker’s plan to become profitable by selling a high volume of Model 3 cars into doubt.

The Economy and Bond Market

Strengths

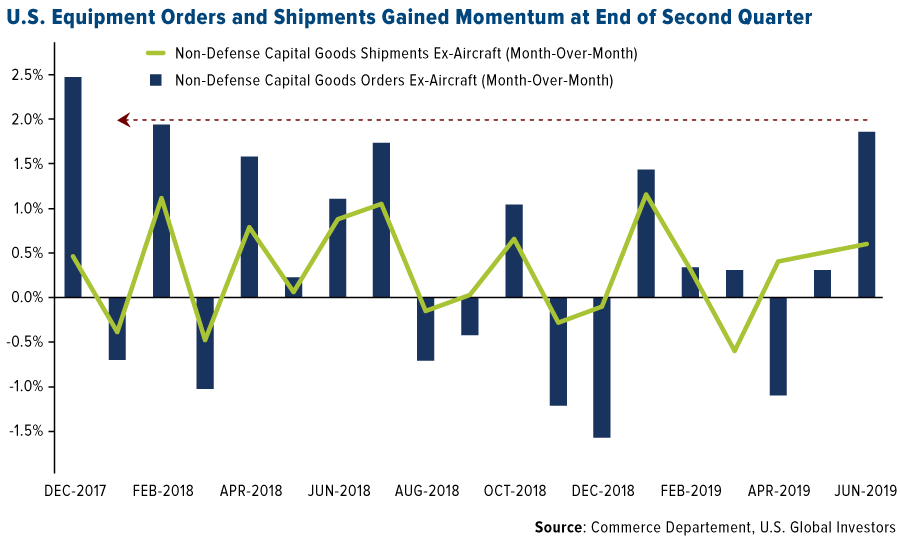

- Orders placed with American factories for business equipment in June registered the biggest gain in more than a year and shipments unexpectedly increased; suggesting corporate investment is regaining momentum. A proxy for business investment —non-military capital-goods orders excluding aircraft — jumped 1.9 percent in June, while shipments climbed 0.6 percent, Commerce Department data showed Thursday.

- The number of people who applied for unemployment benefits last week fell to the lowest level in more than three months, writes MarketWatch, reflecting the persistent strength of a U.S. labor in which layoffs have fallen to the lowest level in decades. Initial jobless claims dropped 10,000 to 206,000 in the seven days ended July 20, the government said Thursday.

- The IHS Markit US Services PMI rose to a three-month high of 52.2 from 51.5 in June. In the report, Executives said consumer spending remains fairly strong, though some companies had to resort to discounting to boost sales.

Weaknesses

- According to IHS Markit’s Flash U.S. purchasing managers’ index (PMI) report, business activity in the manufacturing sector stagnated in July with the Manufacturing PMI dropping to 50 from 50.6 in June. That caused the gauge to slump to its worst level in nearly a decade, reports MarketWatch.

- U.S. home sales fell more than expected in June as a persistent shortage of properties pushed prices to a record high, writes Reuters, suggesting the housing market was struggling to regain its footing since hitting a soft patch last year. The National Association of Realtors said existing home sales dropped 1.7 percent to a seasonally adjusted annual rate of 5.27 million units last month.

- The IMF has downgraded its outlook for the world’s economic output. It warned that U.S. tariffs on European cars, a no-deal Brexit or a trade war with China could tank the global economy. The organization said it expects the world economy to expand by a "sluggish" 3.2 percent in 2019 after it expanded by 3.6 percent in 2018.

Opportunities

- Former Federal Reserve Chairman Alan Greenspan endorsed the idea that the U.S. central bank should be open to an insurance interest-rate cut, writes The Bond Buyer. The idea is to counter risks to the economic outlook, even if the probability of the worst happening was relatively low. “Forecasting is very tricky. Certain forecast outcomes have far more negative effects than others,” he told David Westin in a Bloomberg Television interview Wednesday. “It pays to act to see if you could fend it off.”

- The U.S. government will pay a minimum of $15 per acre to farmers hurt by President Donald Trump’s trade war with China, reports Reuters. Agriculture Secretary Sonny Perdue said on Tuesday the plan is estimated to total about $16 billion.

- Second-quarter growth in the U.S .was better than expected, while it represented a deceleration from the pace of the past few years, it was broadly in-line with the long-term trend. Latest consumer spending data was also reported stronger.

Threats

- Mario Draghi has set the stage for a radical round of additional European Central Bank easing to combat the euro area’s severe economic slowdown, writes Bloomberg. While there are still signs of strength in the economy, “this outlook is getting worse and worse,” the ECB president said in Frankfurt after the Governing Council met. “It’s getting worse and worse in manufacturing, especially, and it’s getting worse and worse in those countries where manufacturing is very important. But because of value chains this propagates all over the euro zone. And so this must be taken into account.”

- The White House and Congress just reached a deal that would avert a major fiscal crisis in Washington this fall. The Trump administration and congressional Democrats forged an agreement to add billions to government spending and lift the debt limit for two years. While the agreement averts an immediate fiscal shutdown, the gargantuan amount of deficit spending poses serious risks for the economy longer term.

- Jody Lurie, corporate credit analyst at Janney Investment Strategy Group said that investors should reduce junk bond exposure while there is still liquidity as market risks are rise. “Reducing high yield exposure now while high yield corporate bonds remain in favor will better suit many investors long-term,” she wrote in her research note.

Energy and Natural Resources Market

Strengths

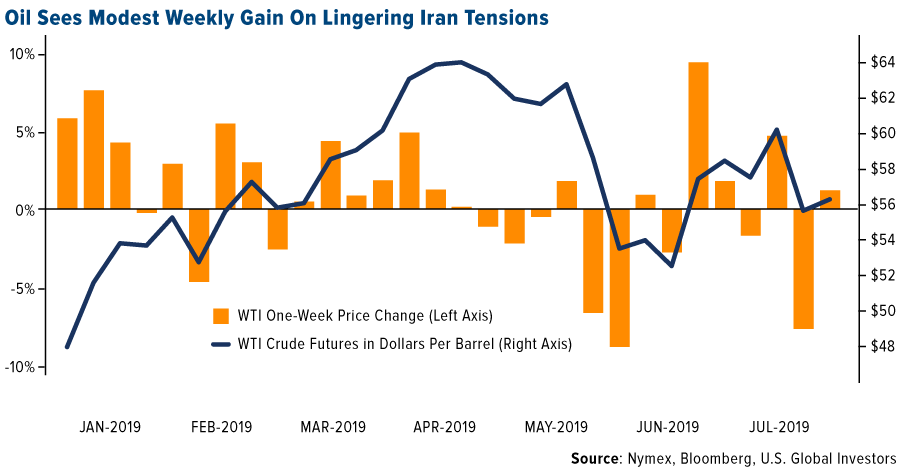

- The best performing major commodity for the week was palm oil, which gained 7.78 percent on delayed planting of oilseed in India, due to a poor monsoon season and escalating dryness in the U.S. that may impact soybean crops. Oil is set for a weekly gain after a big drop last week. American crude inventories declined for six days as of Friday. Also giving a boost to crude are the ongoing tensions with Iran that have stoked concerns of disrupted energy flows from the Middle East.

- According to analysts from Wood Mackenzie, China is set to surpass Japan to become the world’s top buyer of liquefied natural gas (LNG) by 2022. Japan’s annual LNG imports are forecast to fall 12 percent from last year to 72.8 million tons by 2022, while China’s imports will jump 38 percent to 74.1 million tons.

- Saudi Arabia is taking steps to diversify its economy away from just oil and into wind power. Bloomberg reports that EDF Renewables and Masdar Clean Energy won a contract in January to build a 400-megawatt facility that is expected to begin producing electricity in early 2022. The project will be the largest wind power plant in the Middle East.

Weaknesses

- The worst performing major commodity for the week was lumber, which fell 6.11 percent. Canfor Corp. CEO Don Kayne noted on a conference call that timber bids have softened and more shutdowns or curtailments are needed at British Columbia lumber mills. Nickel is heading for its biggest weekly loss since October. The metal fell 3.3 percent on Thursday after China’s top stainless steel producer, Tsingshan Holding Group Co., was said to have cut prices, which hurts the outlook for demand, reports Bloomberg. Analysts have warned that nickel prices could retreat after spiking on low inventories, strong Chinese steel output and tightening supply.

- Iron ore took a few blows this week. Posco, a top Asian mill, said on Tuesday that it expects prices to drop back below $100 in the fourth quarter due to supplies picking back up after disruptions in Brazil earlier this year. Brazil’s Vale SA is beginning to restart some operations, which will allow the return of 5 million tons of production. UBS Group forecasts that prices will fall, with Wayne Gordon saying “as we get into the fourth quarter, we think prices will dip below $100, back down toward $80.”

- Chemical companies are suffering from the ongoing trade war between the U.S. and China. Two big players, Dow Inc. and Eastman Chemical Co., warned of further slowdowns in the second half of this year. Eastman CEO Mark Costa said this week that they “continue to operate in a difficult global business environment due to the impact of the U.S.-China trade dispute and other factors.” Bloomberg reports that Eastman fell as much as 3.7 percent Friday morning and Dow fell 1.5 percent after being downgraded by Bank of America.

Opportunities

- Although there are some short-term price concerns surrounding nickel, investors are still betting on the metal due to battery demand. BloombergNEF reports that demand for nickel from battery electric vehicles will grow 16-fold by 2030. Vale SA’s Indonesian unit and partners plan to spend $5 billion on nickel projects in the coming years. Bloomberg reports that nickel is still the best performer on the London Metals Exchange so far this year. Nickel miners saw a spark on Monday when Nemaska Lithium Inc. announced it had received a letter of intent from Pallinghurst Group to help finance its lithium mine project in Canada.

- China’s Photovoltaic Industry Association says that it expects demand to be better in 2020 than in this year for solar power due to a clear development plan. Deputy Secretary-general Liu Yiyang said “2019 is a year of policy adjustment, while next year will be a continuation of policies” and that now “the industry knows what to expect for next year so demand will be better.”

- More research out of BloombergNEF shows that China and India are neck and neck in leading the charge to deploy renewable energy globally. Both nations have awarded 100 gigawatts of clean energy capacity in auctions between 2003 and 2019 – accounting for 42 percent of renewables auctioned globally. BNEF’s Emma Champion writes that India is set to extend its lead over China in 2019, with a 26 gigawatt pipeline of auctions announced.

Threats

- South Africa’s Petra Diamonds Ltd. dropped to a 17-year low this week as the miner struggles to repay debts without asking shareholders for more money, reports Bloomberg. Diamond producers globally are facing challenges of staying profitable amid a slump in both prices and demand.

- One of Russia’s largest energy companies, Novatek PJSC, reported that revenue fell 6.7 percent in the second quarter from a year earlier due to lower LNG prices. Novatek was one of the first major producers to publish quarterly results and could prove to be a bellwether for other European peers and signal weakness in the global natural gas market.

- According to research from IHS Markit, U.S. oil production growth will slow over the next four years. Estimates show that output will continue to increase, but just by 800,000 barrels a day for each year through 2023 – less than half of 2018’s 1.9 million increase. IHS Markit’s Raoul LeBlanc says “now that productivity has hit a plateau, the chief governor of production growth is money, and investors are putting pressure on producers to cut back.”

Emerging Europe

Strengths

- Greece was the best performing country this week, gaining 2.6 percent. The Bank of Greece announced another month of increases in corporate lending, which should allow for a full abolition of capital controls. Public Power Corporation (PPC), an electricity producer and distributor, was the best performing stock trading on the Athens exchange, gaining more than 24 percent in the past five days after the new government announced its plan to find a strategic investor to buy its stake in Hellenic Electricity Distributor Network Operator, which is fully owned by PPC.

- The Turkish lira was the best relative performing currency this week, losing 29 basis points against the U.S. dollar. Despite the central bank’s rate cut of 425 basis points, the currency was supported by bond inflows. Turkey’s real rates are one of the highest in the world and this week’s dovish ECB tone sent bond investors looking for higher yielding instruments.

- Health care was the best performing sector among eastern European markets this week.

Weaknesses

- Hungary was the worst performing country this week, losing 1.8 percent. The EU took Hungary to court over a law that makes it a crime to help asylum seekers, the latest in many running battles between Brussels and Budapest on immigration, human rights and democracy. Shares of OTP bank, the largest index holding with a weight of almost 40 percent, declined 3 percent.

- The Polish zloty was the worst performing currency in the region this week, losing 1.4 percent. The zloty trades closely with the euro, which was down 70 basis points on prospects of future rate cuts and the reintroduction of the quantitative easing program.

- Finance was the worst performing sector among eastern European markets this week.

Opportunities

- The Cornerstone Macro team in a report titled “German Locomotive Lost Steam” said that the strength of Germany as a leading economy is stalling due to global trade worries, manufacturing, auto sluggishness and a lack of structural reform. They see France and Italy picking up and assuming Germany’s former role as the eurozone’s locomotive.

- The European Central Bank (ECB) left its main rates unchanged this week, but the bank had a dovish tone revising its forward guidance and indicating rate cuts as soon as September. Policy makers may also reintroduce its quantitative easing program to stimulate economic growth.

- Sberbank, Russia’s largest bank, and internet giant Mail.ru are launching a $1.6 billion joint venture investing in taxi and food delivery markets. Food and transportation purchases account for more than half of Russian household spending, according to Mail.ru’s CEO Boris Dobrodeyev. This is part of Sberbank’s plan to move away from traditional banking, which chief executive Herman Gref fears will be disrupted by online payment services.

Threats

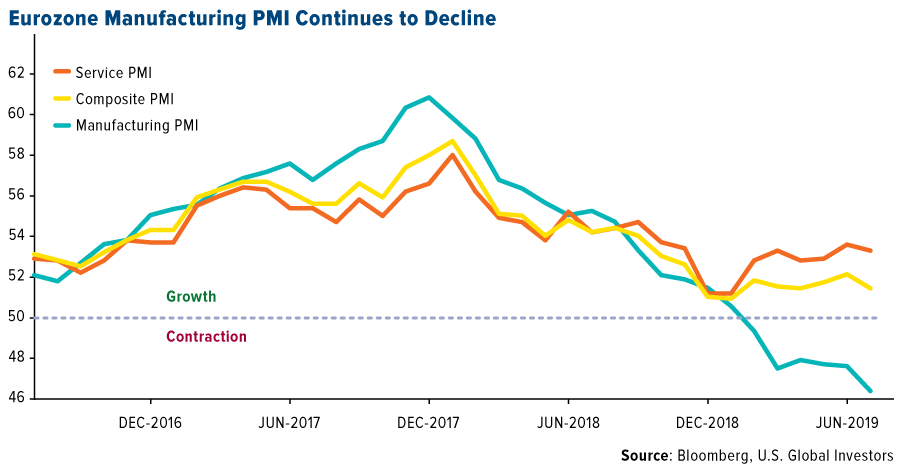

- Eurozone’s preliminary manufacturing data for July was reported lower than expected, at 46.4 versus 47.7. Geopolitical worries, Brexit, growing trade frictions and the deteriorating performance of the auto sector in particular have pushed manufacturing into a deeper downturn. Service PMI remains strong, keeping the Composite PMI above the 50 level that separates growth from contraction.

- Boris Johnson is Britain’s next prime minister, replacing Theresa May. He is a former finance minister and the mastermind behind the Brexit referendum. He wants to take the UK out of the EU with or without a deal. The current Brexit deadline is set for October 31, but another extension to the departure date is possible, especially with a new government forming.

- Ukraine sized a Russian tanker anchored in the Black Sea on Thursday, freeing the crew but keeping the vessel. It looks like a retaliation for Russia’s capture of Ukrainian ships and sailors last year. Twenty-four Ukrainian crewmembers remain under detention in Russia. Russia-Ukraine relations are under long-term tension, but with Russia’s annexation of Crimea 5 years ago and recent developments in the Black Sea, the tension between neighboring countries is escalating.

China Region

Strengths

- The best performing index in the region for the week was Vietnam’s Ho Chi Minh Stock Index, which climbed 1.13 percent. China’s Shanghai Composite rose 0.80 percent, and Taiwan’s TWSE was up 0.73 percent. Other regional indices were in the red on the week.

- The best-performing sector in Hong Kong’s Hang Seng Composite Index since last Friday was information technology, which rose 1.58 percent.

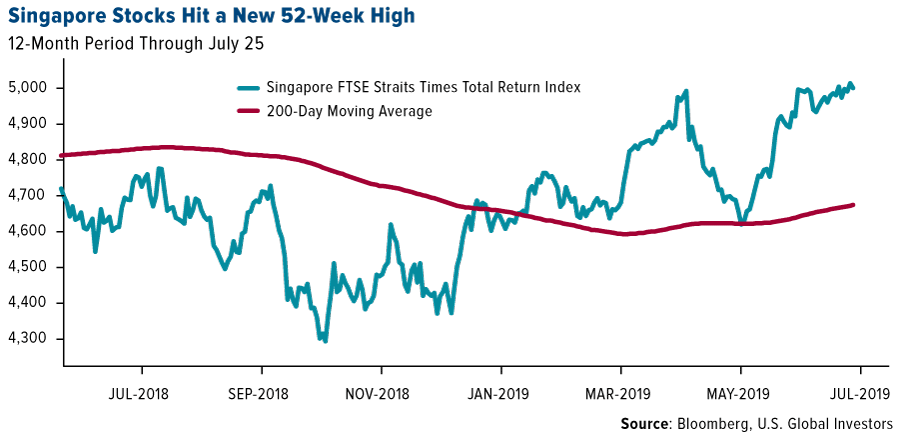

- Singapore’s FTSE Straits Times Total Return Index rose to hit new 52 week highs over the course of the week. Industrial production numbers also beat in Singapore this week for the June reading as well, as both month-over-month and year-over-year data came in ahead of consensus.

Weaknesses

- The worst-performing index in the region for the week was Indonesia’s Jakarta Composite, which fell 2.03 percent since last Friday.

- The poorest-performing sector in Hong Kong’s Hang Seng Composite Index this week was telecommunications, which declined by 4.04 percent.

- Hong Kong’s imports and exports missed, with year-over-year exports for the June measurement period dropping 9.0 percent, worse than expected and down from the prior reading of a drop of only 2.4 percent, while imports also missed, dropping 7.5 percent, below expectations for a 3.0 percent drop and down from the prior reading of -4.3 percent.

Opportunities

- U.S.-China trade talks—in a collective Trade Truce 2.0—are slated to continue next week, with tariff escalation on hold but both sides posturing heading into the talks. While U.S. President Donald Trump hinted that no grand bargain is to be expected next week, and while adviser Larry Kudlow indicated rather vaguely that the U.S. would “like” to return to the May framework that reportedly had around 90-95 percent of an agreement in place, we still don’t have much clarity. But talk, while perhaps “cheap,” is nonetheless good in the midst of otherwise-escalating tariffs, and provides a degree of optimism. Stay tuned.

- While there has indeed been a degree of negativity in sentiment in and perhaps toward Hong Kong amid protests against the recent extradition bill (exacerbating the situation, given the already relatively high-profile attention on the city and region due to the ongoing nature of the trade spat between the U.S. and China), it is nonetheless worth observing that the city’s blue chip Hang Seng Index stands currently at a price-to-earnings ratio of 11.12 (the S&P 500 in the United States stands at 19.79). From a contrarian standpoint, ask what can go right; ask whether Hong Kong is expected to disappear from the map overnight; ask whether the present protests or headlines necessarily change everything or whether, indeed, one just might consider it a buying opportunity. Surely this is something each investor must decide, but the present situation ought to provide food for thought for global investors as to one’s style and investment philosophy, if nothing else. Even if one decides not to invest, it’s a great situation to make one stop and take stock of things with a degree of reflection.

- The new Shanghai STAR Market concluded its first day of trading with stocks up an average of some 140 percent, and in a volatile week of trading for the new Science and Technology board, the 25 debut IPOs that comprise the present index closed up an average of just about that amount on the week, gaining 139 percent over the first five days. The new board aims to serve to raise capital at home in China for earlier-stage or even money-losing companies, keep listings in Shanghai rather than losing out to New York or Hong Kong, for instance, and continue to internationalize the Chinese economy with this Nasdaq-like new board.

Threats

- The threat of U.S.-China trade war escalation must remain a threat until resolved with more certainty. And in the meantime, however positive it is that talks remain ongoing, the inherent uncertainty may be considered an inherent threat. Late on Friday U.S. President Trump suggested that China may want to delay signing a trade deal until after his—assumed, by him—victory in the 2020 election. “I think that China will probably say, ‘let’s wait,’” the President said. “When I win, like almost immediately, they’re all going to sign deals.” What this suggests is that while a framework may possibly be in the works, the president is also comfortable keeping his options open and lowering expectations for anything soon. The election is November 2020. That’s a long time from now…but that being said, perhaps by lowering expectations it is also easier to make any progress in the meantime seem that much more positive. Is it The Art of the Deal?

- The International Monetary Fund recently slashed its global growth outlook, cutting expectations for the world economy to a 3.2 percent growth pace this year and 3.5 percent for next year, both numbers down 0.1 percent from the prior estimate. The IMF statement suggested that, “The principal risk factor to the global economy is that adverse developments—including further U.S.-China tariffs, U.S. auto tariffs, or a no-deal Brexit—sap confidence, weaken investment, dislocate global supply chains, and severely slow global growth below the baseline.” The IMF also slashed its China outlook to 6.2 percent this year and 6.0 percent next.

- Once again, the U.S. dollar is just a stone’s throw from new 52-week highs, crossing 98 again today. A stronger U.S. dollar could pose EM headwinds.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended July 26 was Proton Token, up 512.56 percent.

- Utah County—yes, a county in Utah—is set to become the third U.S. jurisdiction to allow residents to vote using blockchain technology. Next month, the municipality will be piloting Voatz, a blockchain-powered voting app that has previously been trialed in Denver as well as West Virginia, according to reporting by CoinDesk.

- The Securities and Exchange Commission (SEC) has issued a no-action letter to Pocketful of Quarters (PoQ), which is a gaming startup looking to issue tokens on the ethereum blockchain, reports CoinDesk. In its second no-action letter, the SEC Division of Corporation Finance wrote that PoQ may legally sell its Quarters tokens to consumers without registering them as securities.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended July 26 was Big Bang Game Coin, down 58.23 percent.

- The price of bitcoin fell below key support of $10,000 on Tuesday and “could suffer a deeper drop” based on volume analysis, CoinDesk writes. The news agency adds that crypto “bears are expected to dominate proceedings in the short term.”

- Facebook’s proposed Libra coin is many months away from being launched, but scams involving the digital currency are already proliferating on the social media giant, according to an investigation by the Washington Post. “Roughly a dozen fake accounts, pages and groups scattered across Facebook and its photo-sharing app Instagram present themselves as official hubs for the digital currency, in some cases offering to sell Libra at a discount if viewers visit potentially fraudulent, third-party websites,” the article reads. Lawmakers in particular were quick to rebuke Facebook, seeing the scams as even more reason why the tech company should delay Libra’s release until regulators have had a change to examine it thoroughly.

Opportunities

- Potentially good news for retail crypto investing: This week, Grayscale Investments released its “Bitcoin: 2019 Investor Study” publication, which alleges, among other things, that more than a third of U.S.-based investors are interested in bitcoin. Contrary to the belief that bitcoin is a niche investment, a survey conducted by Grayscale found that around 36 percent of investors expressed interest in bitcoin as an investment. This represents a “potential market of more than 21 million investors in the general population,” the firm writes. Also, an incredible 83 percent of respondents said they are strongly motivated “by the idea that they could invest small amounts in bitcoin today, see how their investments performed and add to their positions later.”

- “There’s heightened interest again” in cryptocurrencies, says CEO of brokerage firm TD Ameritrade Tim Hockey. Speaking to TheStreet this week, Hockey explained that his company is considering plans to allow clients to trade cryptocurrencies, just as it does with traditional currencies. “Clients are asking for it,” Hockey says.

- After some delays, Bakkt quietly began testing this week “with participants from around the world,” it announced in a tweet on Monday. The much-anticipated, Intercontinental Exchange (ICE)-backed trading platform will be listing two bitcoin futures contracts, a daily settlement contract and monthly contract. Although it’s unclear right now what the testing process looks like, not to mention when Bakkt will be made widely available, but the news is nevertheless an encouraging development.

Threats

- A recent survey found that a vast majority of U.S. adults couldn’t care less about Facebook’s Libra coin, suggesting the company faces an uphill battle in terms of building trust and brand recognition. A whopping 86 percent of respondents to a CivicScience survey said they were “not at all interested” in Libra, compared to only 2 percent who said they were “very interested.” Three percent were “somewhat interested.” Moreover, 77 percent said they had zero trust in Facebook with their personal information. The survey questioned nearly 1,800 adults.

- One cryptocurrency investor’s million dollar suit against AT&T over stolen coins is allowed to move forward, reports CNBC, at the movement from a federal judge in California. The case involves the theft of millions of dollars’ worth of digital currency through a man’s phone, bringing attention to a hacking method known as “SIM swapping.” This is where criminals steal phone numbers to log into cryptocurrency accounts, then transfer the money to themselves.

- Abra, a crypto investment app, is being forced in enact changes to services to U.S. customers over “regulatory uncertainty and restrictions” within the country, reports CoinDesk. The firm explains how this will affect Abra users in a blog update on Thursday: “Specifically, for Abra users in the United States is that we have to make some system modifications around our smart contract based synthetic assets. As part of this effort we are migrating any synthetic assets to a native hosted wallet solution.”

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| S&P/TSX Global Gold Index | 234.03 | -3.53 | -1.49% |

| Gold Futures | 1,431.10 | -8.30 | -0.58% |

| Natural Gas Futures | 2.17 | -0.08 | -3.55% |

| S&P/TSX VENTURE COMP IDX | 592.89 | +0.93 | +0.16% |

| 10-Yr Treasury Bond | 2.07 | +0.02 | +0.83% |

| Nasdaq | 8,330.21 | +183.72 | +2.26% |

| Oil Futures | 56.17 | +0.54 | +0.97% |

| Hang Seng Composite Index | 3,781.07 | -41.55 | -1.09% |

| S&P 500 | 3,025.86 | +49.25 | +1.65% |

| DJIA | 27,192.45 | +38.25 | +0.14% |

| Korean KOSPI Index | 2,066.26 | -28.10 | -1.34% |

| Russell 2000 | 1,578.97 | +31.07 | +2.01% |

| S&P Energy | 461.46 | -2.55 | -0.55% |

| S&P Basic Materials | 370.11 | +3.52 | +0.96% |

| XAU | 90.65 | -1.01 | -1.10% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.17 | -0.12 | -5.24% |

| S&P/TSX Global Gold Index | 234.03 | +13.23 | +5.99% |

| 10-Yr Treasury Bond | 2.07 | +0.02 | +1.22% |

| Oil Futures | 56.17 | -3.21 | -5.41% |

| Gold Futures | 1,431.10 | +4.30 | +0.30% |

| S&P 500 | 3,025.86 | +112.08 | +3.85% |

| S&P Energy | 461.46 | -8.00 | -1.70% |

| Hang Seng Composite Index | 3,781.07 | +36.02 | +0.96% |

| DJIA | 27,192.45 | +655.63 | +2.47% |

| Korean KOSPI Index | 2,066.26 | -55.59 | -2.62% |

| Nasdaq | 8,330.21 | +420.24 | +5.31% |

| S&P Basic Materials | 370.11 | +7.35 | +2.03% |

| Russell 2000 | 1,578.97 | +61.19 | +4.03% |

| S&P/TSX VENTURE COMP IDX | 592.89 | +12.84 | +2.21% |

| XAU | 90.65 | +6.91 | +8.25% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.17 | -0.34 | -13.64% |

| 10-Yr Treasury Bond | 2.07 | -0.46 | -18.16% |

| DJIA | 27,192.45 | +730.37 | +2.76% |

| Oil Futures | 56.17 | -9.04 | -13.86% |

| S&P 500 | 3,025.86 | +99.69 | +3.41% |

| Gold Futures | 1,431.10 | +133.40 | +10.28% |

| S&P Energy | 461.46 | -35.04 | -7.06% |

| Nasdaq | 8,330.21 | +223.92 | +2.76% |

| Korean KOSPI Index | 2,066.26 | -124.24 | -5.67% |

| S&P Basic Materials | 370.11 | +15.66 | +4.42% |

| Russell 2000 | 1,578.97 | +3.36 | +0.21% |

| Hang Seng Composite Index | 3,781.07 | -176.56 | -4.46% |

| S&P/TSX Global Gold Index | 234.03 | +50.50 | +27.52% |

| S&P/TSX VENTURE COMP IDX | 592.89 | -15.98 | -2.62% |

| XAU | 90.65 | +20.02 | +28.34% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (06/30/2019):

OTP Bank Nyrt

Sberbank of Russia PJSC

Royal Gold Inc

Franco-Nevada Corp

Wheaton Precious Metals Corp

iShares Silver Trust

Newmont Goldcorp Corp

Harmony Gold Mining Co Ltd

Canfor Pulp Products Inc

Novatek PJSC

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry.

The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks.

The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months.

The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange.

The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver.

The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar.

The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500.

The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500.

The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period.

The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500.

The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500.

The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500.

The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500.

The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500.

The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500.

The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns.

The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The Straits Times Index (STI), maintained & calculated by FTSE, is the most globally-recognized benchmark index and market barometer for Singapore. Dating back to 1966, it tracks the performance of the top 30 largest and most liquid companies listed on the Singapore Exchange. The Vietnam Stock Index or VN-Index is a capitalization-weighted index of all the companies listed on the Ho Chi Minh City Stock Exchange. The index was created with a base index value of 100 as of July 28, 2000 The TWSE, or TAIEX, Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The index was based in 1966. The index is also known as the TSEC Index. The Straits Times Index comprises the top 30 SGX Mainboard listed companies on the Singapore Exchange selected by full market capitalization.