Gold Is Catching a Bid on Pandemic and Inflation Fears. Are You Participating?

Date Posted: July 9, 2021

Read time: 43 min

Gold notched its third straight week of higher prices as the yield on the 10-year Treasury dipped below 1.3% for the first time since February. The highly transmissible Delta variant was also ruled the most dominant strain of coronavirus in the U.S., threatening economic growth and raising uncertainty about the next interest rate hike.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

Gold notched its third straight week of higher prices as the yield on the 10-year Treasury dipped below 1.3% for the first time since February. The highly transmissible Delta variant was also ruled the most dominant strain of coronavirus in the U.S., threatening economic growth and raising uncertainty about the next interest rate hike.

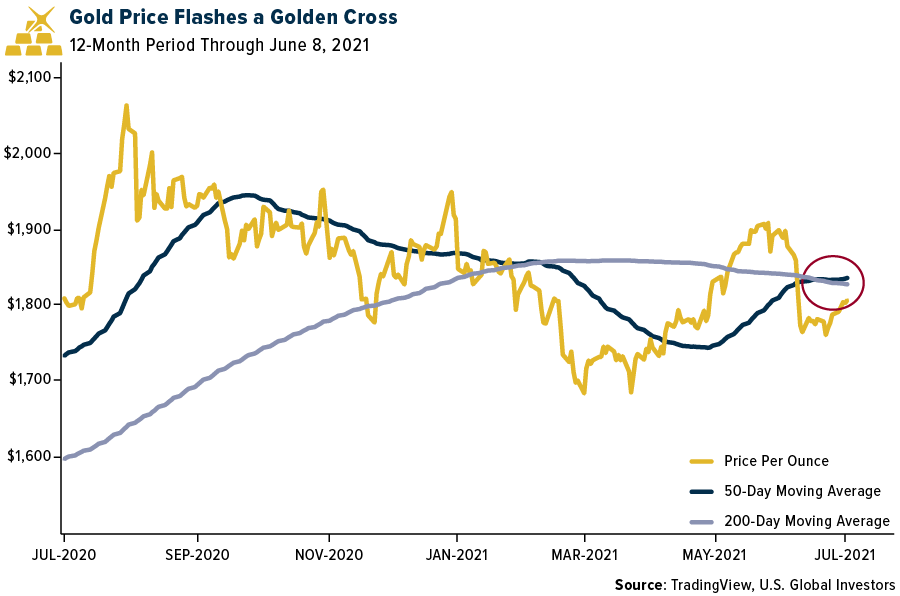

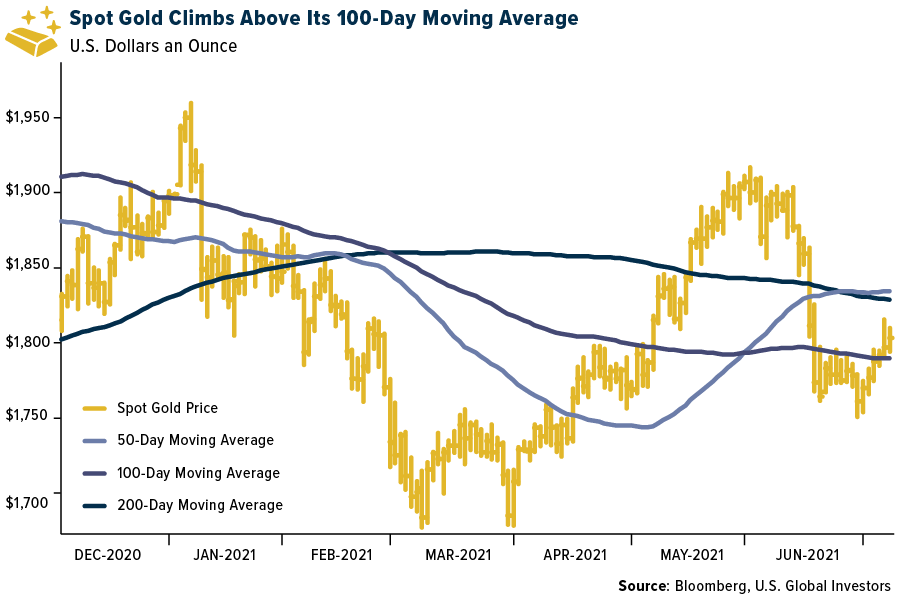

Against this backdrop, the yellow metal is now flashing a golden cross, meaning the 50-day moving average is trading above the 200-day moving average. In the past, this has been a bullish indicator for gold prices, which are still off some 12% from their all-time highs set last summer.

In the short to medium term, it appears as if gold demand will continue to be driven by central bank policy, which should remain accommodative even as inflation fears increase. According to the CME Group’s FedWatch Tool, there’s a 75% probability that interest rates will stay in the 0.00% to 0.25% range a year from now, leaving plenty of time for gold to test $2,000 an ounce or more.

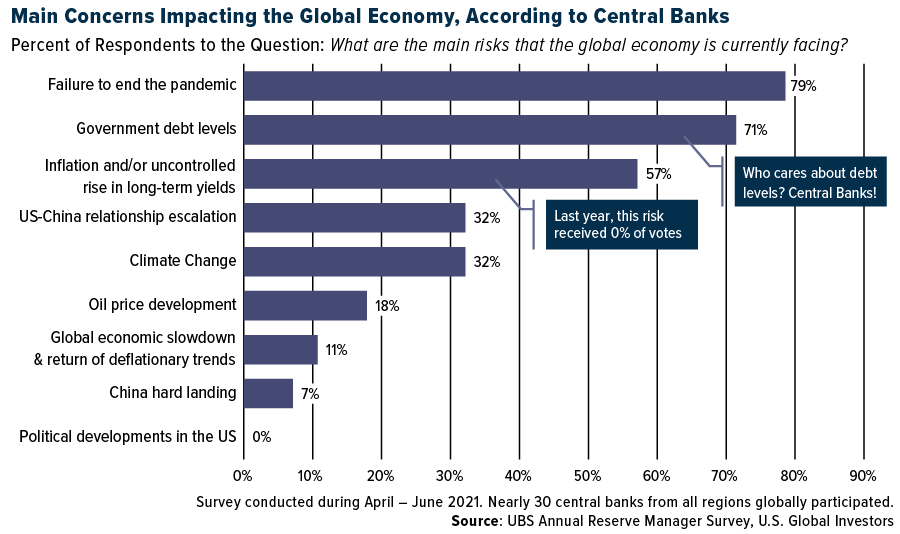

Pandemic Still Tops Central Bankers’ List of Worries, with Inflation Not Too Far Behind

Speaking of central banks, UBS released the results of its annual reserve management survey this week, which show that managers are still very much concerned with the handling of the pandemic.

Nearly 80% of respondents cited failure to end the pandemic as their number one concern impacting the global economy right now, with more than half of them saying they believed it would be over only after 2022. Here in the U.S., the rate of vaccination has slowed considerably in certain populations, allowing Canada, the United Kingdom, Italy and Germany to catch up. In low-income countries, meanwhile, only 1% of people have received one dose of the vaccine.

Central bankers’ concern is not unfounded. IHS Markit’s chief business economist published an article this week showing there’s a strong correlation between vaccination rates and economic growth. The higher a country’s vax rate, the higher its PMI reading was in June; the reverse was also true.

Rounding out the top three concerns impacting future growth were government debt levels (71% of respondents), something I’ve written a lot about, and inflation (57%). I should point out that inflation did not even appear on the list of concerns one year ago when the last survey was taken. The London Bullion Market Association (LBMA) also notes, in its review of the second quarter, that there were more than 100,000 press articles published about inflation in May, far more than on COVID-19.

Gold Can Help Manage Risk

All of these concerns, I believe, favor gold as a portfolio diversifier. Low bond yields have pushed investors into riskier assets, including stocks. This has been a winning strategy as major indices have been hitting all-time highs, but it’s important to maintain a position in gold to help manage risk. I recommend a 10% weighting, with 5% in physical gold and 5% in gold stocks. A 1% to 2% allocation in Bitcoin and Ether, not to mention crypto mining stocks, also makes sense right now.

HIVE Blockchain Technologies (HVBT) Featured in Times Square

|

|

As many of you are aware, HIVE Blockchain Technologies, the world’s first publicly traded cryptocurrency mining company, listed on the tech-heavy Nasdaq on July 1, four years after its debut on the TSX Venture Exchange.

I was very happy this week to see HIVE featured on Nasdaq’s Times Square marquee, which reaches 1,000,000 a day.

I’m also grateful that HIVE team members and I have the opportunity this coming Monday to participate in the closing bell ceremony at Nasdaq. We’re only getting started!

Read the latest HIVE press release by clicking here.

Index Summary

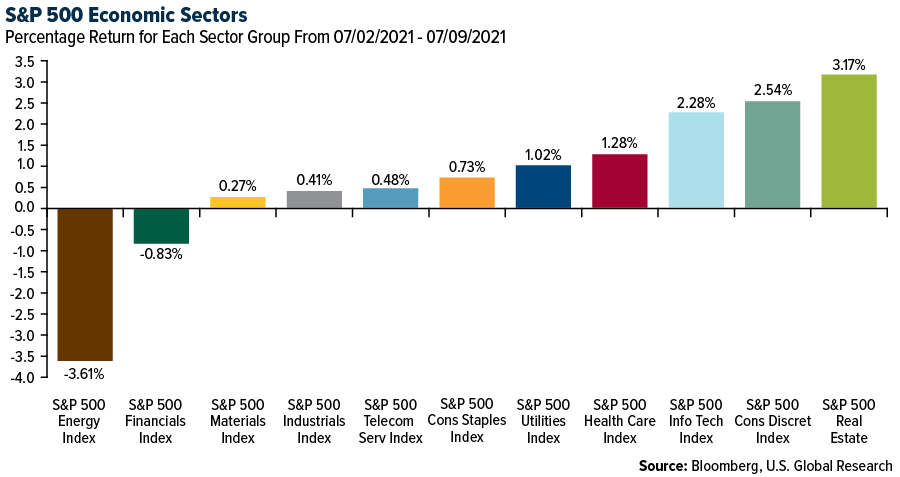

- The major market indices finished mixed this week. The Dow Jones Industrial Average gained 0.24%. The S&P 500 Stock Index rose 0.43%, while the Nasdaq Composite climbed 0.43%. The Russell 2000 small capitalization index lost 1.13% this week.

- The Hang Seng Composite lost 3.62% this week; while Taiwan was down 0.27% and the KOSPI fell 1.94%.

- The 10-year Treasury bond yield fell 6 basis points to 1.36%.

Airline Sector

Strengths

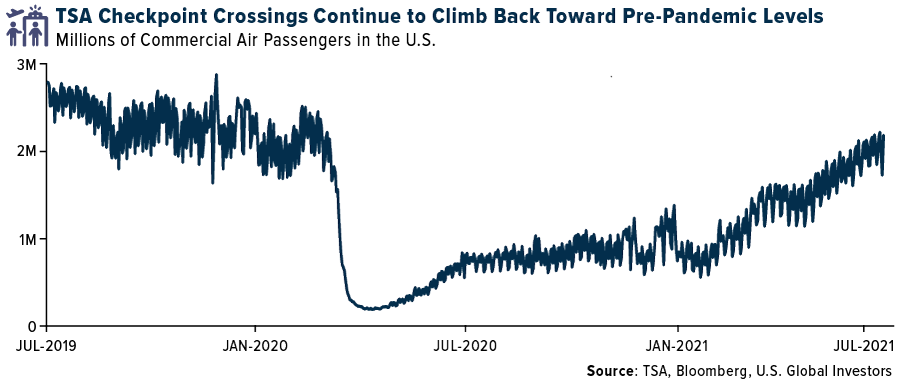

- The best performing airline stock for the week was Sydney Airport, up 33.1%. There was news of a potential acquisition offer by Macquarie Group. United States domestic air traffic turned positive for the first time, contrasted with air traffic recorded in 2019. Last week, the TSA checkpoint travel numbers hit 2.14 million compared to 2.08 million in 2019, a record high since the start of the pandemic. This was the first time the current year’s traveler numbers were higher than 2019’s levels.

- According to UBS, the latest weekly datapoint for June domestic traffic booked shows a 3% gain versus the same week in 2019, which is the first positive pre-pandemic datapoint seen from the group. This compares to the 22% loss witnessed last week.

- Ryanair transported 5.3 million passengers in June with a load factor of 72%. Credit Suisse expects the company to operate near 80% of capacity in July through September. The firm estimates that there are 100 million pounds of weekly cash inflows.

Weaknesses

- The worst performing airline stock for the week was Hainan Air, down 13.8%. UBS is seeing a plateau in yields with the most recent datapoints for June and August seeing modest improvement, while July was a bit lower; the cumulative June yields finished at -19% for domestic and -24% for international.

- Future booking trends appear to be softening. UBS says June booking trends improved nicely in the most recent week, but the group did see a step back for July and August with domestic at -27% and -26%, respectively, versus -23% and -8% last week, while international came in at -49% and -58%, versus -49% and -47% last week.

- In June, airline equities have historically underperformed the market 70% of the time. This month, airline stocks declined 12% compared to the S&P 500’s 2% return, as positive earnings revisions remained muted and concerns around COVID-19 variants increased. While the group remains up 16% year-to-date versus the S&P 500 up 14%, we note that most of this outperformance came in the month of February in conjunction with the vaccine rollout, and airlines are down an average of 12% since April 1 versus the S&P 500 up by 8.2%.

Opportunities

- The Financial Times highlights the proposed £100 million pounds award to Wizz Air CEO Jozsef Varadi should the share price rise to 12,000 pence in the next five years. This implies 10% to 20% annual share price growth that would trigger £20 to £100 million pounds in reward.

- A corporate travel rebound signals the first signs of recovery in the industry. According to the Financial Times, hotels, airlines, and travel companies reported a rise in bookings over recent weeks as executives return to the road. Globally, 41% of business travelers expect their next trip in 2022 or beyond, up from 30% in Bank of America’s last survey. Similarly for international, 51% said they would not take a long-haul fight until 2022 versus 39% that said they would take a long-haul flight now.

- Alaska Air Group aims to become the most fuel-efficient U.S. airline in five years. During an interview with the Washington Post last week, Alaska Air Group’s CEO Ben Minicucci outlined a five-point strategy that included upgrading its fleet, achieving operational efficiencies, using sustainable aviation fuels, investing in innovative technology, and carbon offsets.

Threats

- China’s domestic air traffic has stabilized at 86% of normal rates in the second half of June (from 81% in the first half of June) with the COVID situation in Guangdong largely under control. Domestic unit revenues weakened to 83% of normal in the second half of June with weaker yields offsetting better seat loads. Guangzhou Airport remains hard hit by travel restrictions with domestic traffic at 19% of normal rates in the second half of June, slightly better than 15% in the first half of June, while other airports have seen some improvement (Shanghai) or largely stabilization (Hainan and Beijing).

- June scheduled flights finished at 62% of 2019 levels while available seat miles (ASMs) were 51% (both 5% below late May expectations) which was up slightly from May’s 58% to 48%. While July was reduced 1% from last week, we continue to see notable improvement with scheduled flights and ASMs at 70% versus 59% of 2019 levels, which would be twice the improvement rate in June. There were reductions across most regions for August and September, which moved 1% lower from last week.

- With the delta variant of the coronavirus sweeping through many regions in the world the past few weeks, parts of Asia, Australia, and Europe are re-introducing travel restrictions. The Sydney metro area recently went back into lockdown for the first time in a year, while Germany reinstated a 14-day quarantine for travelers arriving from delta variant areas.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Hungary, gaining 1.34%. The best performing country in Asia this week was Indonesia, gaining 0.37%.

- The Turkish lira was the best performing currency in emerging Europe this week, gaining 0.36%. The Vietnamese dong was the best performing currency in Asia this week, gaining 0.02%.

- Retail sales in Europe remain strong. Year-over-year sales increased by 9% versus 8.2% expected and month-over-month sales increased by 4.6% versus 4.3% expected. Many European countries opened their borders for summer travel and vacationers brought money along to spend.

Weaknesses

- The worst performing country in emerging Europe for the week was Russia, losing 1.49%. The worst performing country in Asia this week was the Philippines, losing 4.08%.

- The Russian ruble was the worst performing currency in emerging Europe this week, losing 1.55%. The Philippine peso was the worst performing currencies in Asia, losing 2.08%.

- China’s services activities slowed notably in June. The Caixin Services PMI was reported at 50.3 in June below the expected reading of 54.9, versus 55.1 in May. The latest reading was the lowest in the past 14 months and reflected slower growth in output and new orders.

Opportunities

- Donald Turks, who served as prime minister of Poland from 2014 to 2019 and currently is the President of the European Peoples Party, will leave Brussels and move to Poland to head the biggest opposition party, the conservative-liberal Civic Platform. The right-wing national-conservative Law & Justice party, led by Jaros?aw Kaczy?ski since 2015, put Poland on a collision course with the EU; Tusk wants to step in and reverse the process.

- Chinese President Xi Jinping held a virtual summit with French President Emmanuel Macron and German Chancellor Angela Merkel in Beijing last weekend. He called for China and Europe to expand consensus and cooperation between both sides. The discussion covered talks on trade, climate protection, and fights against the pandemic.

- The Polish central bank will most likely leave the main rate unchanged when it meets next week at the record low of 10 basis points. Inflation recently eased in the country; rate hikes may be put on the side for now. The country will continue to focus on economic growth and pandemic recovery.

Threats

- Russia may introduce additional taxes on metals and oil. The Russian government is discussing a new increase of its metals extraction tax, as well as adjustments of taxes for oil companies and some other industries, seeking to raise 400 billion rubles from 2022 to 2024. Russia increased metal extraction tax last year but did not include gold producers. This time, tax increases may also apply to precious metal producers.

- China’s internet regulator blocked Didi from app stores just days after its initial public offering in the United States. On Sunday, the Cyberspace Administration said, without giving details, that there had been serious violations with the company’s collection and use of personal information. China pledged to increase scrutiny of data practices at listed companies.

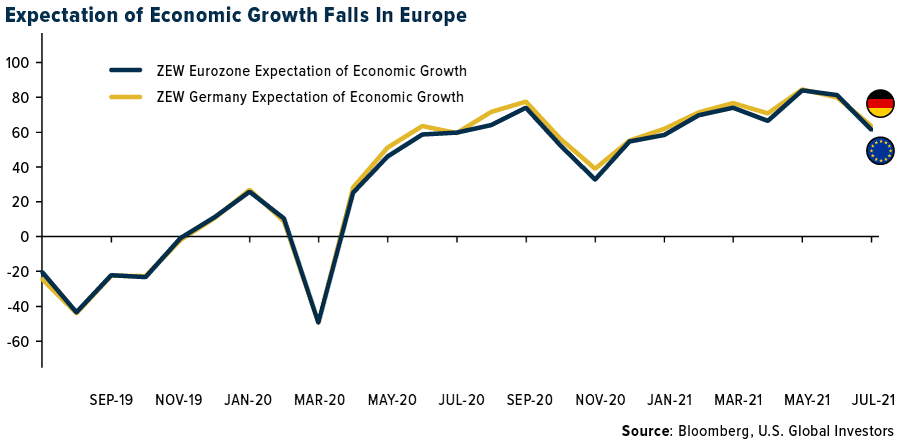

- Expectations for growth in Europe’s largest economy, Germany, fell from 79.8 in June to 63.3 in early July. The reading missed economists’ forecast of 75.0 points. The Eurozone ZEW Economic Sentiment for July fell to 61.2 for the current month compared to 81.3 the previous month, versus the 84.4 consensus forecast. The ZEW Index fell for a second consecutive month, and it may continue to move lower from the two-decade high reached back in May.

Energy and Natural Resources Market

Strengths

- The best performing commodity for the week was palm oil, up 2.72%. Palm oil climbed to its highest level in a month this week as a weaker Malaysian ringgit raised the appeal of the commodity, while prices for palm oil traded in China posted their third weekly advance.

- Liquified natural gas (LNG) prices in the U.S. are posting their longest winning streak since May 2000, as LNG rose 1.21% this week, bringing its year-to-date gains to 120.03%. The gains are being driven by an increase in global demand amidst blistering temperatures, as climate change has triggered more frequent and extreme weather events. European gas futures hit records as Asian buyers raised their bids for LNG spot cargoes to the highest seasonal levels since 2014.

- Demand of gasoline surged in the U.S. to a record high as during the July 4th holiday weekend. The Energy Information Administration (EIA) reported that gasoline supplied, which is used as a proxy for demand, reached 10 million barrels a day for the week ending July 2, the highest figure going back to 1990. Moving average for gasoline demand also edged higher, reaching the levels seen in late 2019. The market still has room to recover, as on a seasonal basis gasoline demand was 150,000 barrels a day short of July 2019’s levels.

Weaknesses

- The worst performing commodity for the week was corn, down 11.38%. Corn declined due to lower Chinese demand.

- The Organization of Petroleum Exporting Countries and its allies (OPEC)+ failed to reach an agreement on a proposal for hiking the supply of crude in August, sending the oil market into its first weekly loss since May 2021. United Arab Emirates (UAE) disagreed over how the cartel is measuring production cuts and is keeping an unfair production baseline for UAE’s quota for longer. Saudi Arabia increased its official selling price, of the Arab Light crude, for the Asian market by 80 cents a barrel to $2.70 above the regional benchmark, the largest month-over-month increase since January 2021. The oil market is set to tighten as global economies reopen, prompting demand to increase, while supply lags.

- Corn futures slid this week to their lowest level since January on the back of decreased demand from China and better-than-expected rain in the U.S. Traders await clarity on future demand from China, which has been buying a record amount of corn from the U.S. and is expected to reduce its purchases as its own harvest nears and local prices drop. Corn futures declined by 11.38% this week, while soybean futures, wheat futures, and coffee futures declined 4.94%, 7.59%, and 3.13%, respectively.

Opportunities

- The European Commission, European Union’s (EU) regulatory arm, revised its renewable energy law to set targets for the use of sustainable fuels in transport, heating, and cooling. The plan requires emissions from new cars and vans to fall by 65% by 2030 and by 100% by 2035, compared to 2021 levels. These tougher pollution standards are accompanied by rules for national governments to bolster vehicle charging infrastructure. The revisions also include a proposal to boost the share of power that EU receives from renewable energy to 40% from the current 32% by 2030. This law can provide guidelines to other countries that are shifting towards net zero emissions and will encourage investments in the sectors pushing innovation in renewable energy.

- Vestas Wind Systems A/S received a pre-order from German utility company EnBW for a 900-megawatt offshore wind farm. EnBW would be Vestas’ first customer for its new 15-megawatt machines, which it unveiled earlier this year. Vestas has dominated the business of wind farms on land and is striving to scale up designs to increase efficiency as it seeks to become the top supplier of offshore turbines as well.

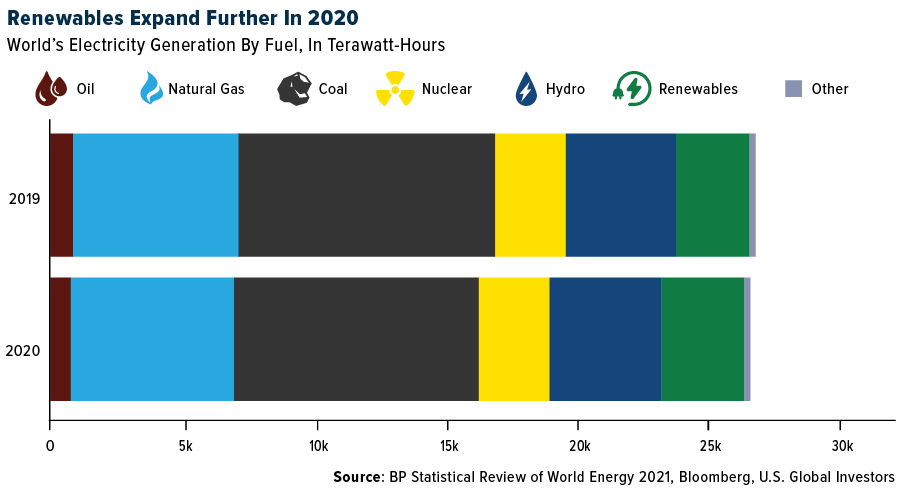

- The U.S. Energy Information Administration (EIA) reported that growth in large-scale solar capacity in the country is projected to exceed that of wind in 2022, for the first time. EIA’s short-term energy outlook estimates that wind and solar capacity will reach 15% of total U.S. generation by next year, compared to 11% in 2020. A forecasted 17 gigawatts of solar capacity will be added in 2022, compared to 6 gigawatts for wind. The following chart shows that renewable energy generation across the world increased in 2020 compared to 2019, with decrease in usage of oil, natural gas, and coal for electricity generation.

Threats

- Container shortages have led to higher freight rates as a 40-foot container, from Shanghai to Rotterdam, now costs $12,000. This rate has doubled from December 2020 and has increased five-fold since January 2020. Disruptions, like the lockdown measures in southern China, are upending global market dynamics, making trades from the East to the West more expensive. Furthermore, exports of plastic resins from Asia, where polymers trade at a discount compared to Europe, have reduced. Polymer prices in Europe reached record-high levels in second quarter of 2021 due to limited inflows from the Asian markets, forcing European producers to turn to pricier U.S. imports.

- Analysts expect that a slowdown in China’s economic recovery would do more to keep copper prices in check than the country’s supply-side intervention. The State Council in China reported that the economy might need additional support from the People’s Bank of China (PBOC), hinting at providing more liquidity to banks to boost lending. Factors worrying traders and analysts tracking copper are the lackluster domestic demand and global demand pivoting from goods to services. Copper had a mix week, rising 0.01% after gaining as much as 2.65% earlier this week.

- A fresh heatwave this week in California and neighboring states could push power supplies to the brink and is adding to high wildfire risk amid record droughts. The California Independent System Operator, which operates most of the state’s grid, issued an alert to customers, asking them to voluntarily scale back on power usage. California, which is issued its first rolling outages in two decades last year, is expecting that meeting consumer demand will be tougher with long-range forecasts predicting above-average temperatures through September. The U.S. Drought Monitor reported that 85% of California is experiencing the highest combined extreme and exceptional drought coverage in the agency’s 21-year history.

Domestic Economy and Equities

Strengths

- Economic activity in the United States service sector continued to expand in June, but at a softer pace than it did in May. The ISM Services PMI declined to 60.1 from 64. This reading missed the market expectation of 63.5. May’s reading was an all-time high.

- The Financial Times, citing data from EPFR (Emerging Portfolio Fund Research) Global which provides fund flows and asset allocation data to financial institutions, reported that global equity funds saw $580 billion of inflows in the first half of 2021, putting the category on track for a record high. Bank of America has estimated that if the pace of inflows continues at the same clip for rest of the year, equity funds will take in more money in 2021 than in the previous 20 years combined.

- Oracle Corp. was the best performing S&P 500 stock for the week, increasing 10.33%. This week it was reported that the company will meet with the Pentagon to assess its eligibility for the government cloud contract called “Joint Warfighter Cloud Capability” (JWCC).

Weaknesses

- The number of job openings on the last business day of May peaked at 9.2 million, announced the U.S. Bureau of Labor Statistics in its latest Job Openings and Labor Turnover Summary (JOLTS) on Wednesday. This reading came in slightly below the market expectation of 9.38 million.

- The U.S. has experienced another ransomware attack. The attack, which private researchers say was carried out by REvil – a group of Russian-speaking hackers believed to be operating inside Russia – struck hundreds of American companies specifically, and more than a thousand companies in as many as 30 countries, experts say.

- Diamondback Energy Inc. was the worst performing S&P 500 stock for the week, losing 10.22%. The share price fell this week as the price of oil dropped from multi-year highs, along with a strengthening of the U.S. dollar, while investors await further signals from OPEC+ alliance.

Opportunities

- Bond yields have technically broken out to the downside. Rich Ross, Senior Managing Director and Head of Technical Analysis at Evercore ISI thinks they can move to 1.25% or lower. If they do, that will provide significant new stimulus for the housing sector and stock prices.

- The United States will release inflation data for June next week; it should be coming down. Bloomberg economists predict a drop in CPI from 5% in May to 4.9% in June on a year-over-year basis.

- According to FactSet, the bottom-up consensus for second quarter S&P 500 earnings per share increased by 7.3% from $41.97 to $45.03 over the course of the quarter. This represents the largest increase in the bottom-up S&P 500 earnings per share estimate since FactSet began tracking in the second quarter of 2002. Companies should continue to record strong profits supported by massive fiscal and monetary stimulus.

Threats

- Chinese ADRs are losing value as China is expanding its focus on companies listing their shares abroad. Shares of ride-hailing company Didi sold off on Tuesday after Chinese internet regulator banned Didi from app store just days after its IPO, due to the company’s serious violations with data collection and use of personal information. If China continues to crackdown on ADRs, then more weakness in their share price could follow.

- The Federal Open Market Committee (FOMC) minutes revealed on Wednesday a substantial dispersion of opinions among Committee members. While the United States continues to provide a massive fiscal and monetary stimulus, it is hard to ignore an improvement in the domestic economic environment, as well as the better virus/vaccine-related conditions. The big question remains, when will the Fed start tightening?

- The NFIB Small Business Optimism Index may fall again in June once the data is released next week. It declined 0.2 points last month to 99.6. May saw a slight pause in the recovery of small business optimism after steadily increasing each month in 2021. As reported in NFIB’s monthly jobs report, a record-high 48% of business owners reported unfilled job openings.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Axie Infinity, rising 136.77%.

- Circle, a payments infrastructure company which also focuses on stablecoin development, announced its plan to go public via a special purpose acquisition company (SPAC). The company is set to merge with blank-check company Concord Acquisition Corp. in a deal valued at $4.5 billion and is expected to be listed on the New York Stock Exchange (NYSE) under the ticker “CRCL.” Circle is the principal developer of the USD Coin (USDC), the second largest stablecoin after Tether (USDT), and is backed by Goldman Sachs, Fidelity Management, and Adage Capital Management.

- Tetra Trust became Canada’s first regulated custodian for cryptocurrencies after being registered by the government of Alberta. The company’s CEO, Eric Richmond, mentioned that there was a pressing need for a regulated custody provider in Canada as the country has become a hotspot for cryptocurrency-related companies, exchange-traded funds (ETFs), and trading platforms. The firm is backed by Coinsquare, which is a Toronto-based crypto trading platform, Coinbase Ventures, and the Canadian Securities Exchange, among others.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performer for the week was Telcoin, down 22.42%.

- The Bank of Thailand (BoT) stressed that cryptocurrencies like Bitcoin and Ethereum are not legal tender in the country and that it will coordinate with Thailand’s Securities and Exchange Commission to mitigate any risks to the country’s financial system if cryptocurrency payments become widespread. Officials from the bank also noted that parties involved in such transactions could face risk of price volatility and cyber theft.

- Scott Minerd, the chief investment officer at Guggenheim, believes that there is no reason for institutional investors to buy Bitcoin now and that the largest cryptocurrency could plummet to $10,000-$15,000 range. The latest tumble in Bitcoin’s price is attributable to increasing regulatory scrutiny from China to the U.K. and the environmental impact of mining the cryptocurrency. Currently, Bitcoin is trading around $33,500, almost 50% lower than its all time high of more than $64,000.

Opportunities

- The Banque de France (BdF) and the Monetary Authority of Singapore partnered to test a cross-border central bank digital currency (CBDC) transaction using a permissioned version of Ethereum called Quorum, which is developed by JPMorgan. This marked the first use of a smart contract-based, automated liquidity pool for the digital EUR/SGD currency pair. After the experiment, the BdF stated that the automated liquidity pool and market-making service for EUR/SGD currency pairs could be scaled up to support participation of multiple central and commercial banks in different jurisdictions.

- Square Inc. announced that the company is working on building a Bitcoin hardware wallet and service to make Bitcoin custody more mainstream. Although the project is in still in its early stages, the U.S. based financial services firm will continue to take input from stakeholders as it tries to bring a mobile-friendly, “assisted-self-custody” wallet to a global audience. Square’s foray into Bitcoin custody could increase attention and investment into the industry.

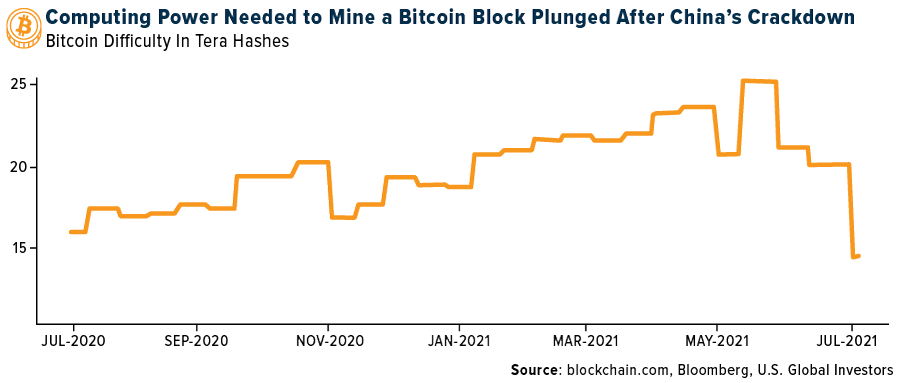

- Osprey Funds, a digital asset management firm, filed to register its Osprey Bitcoin Trust (OBTC) as a Securities and Exchange Commission (SEC) reporting company. The registration would increase OBTC’s transparency and liquidity and will require it to file audited financial statements with the SEC. OBTC has an annual management fee of 0.49% and an additional 0.3% in other expenses from services like crypto custody, while the Grayscale Bitcoin Trust (GBTC) has a management fee of 2%. Meanwhile, Bitcoin mining difficulty decreased 28% after China’s crackdown, increasing the profitability of miners. It reached levels last seen more than a year ago when Bitcoin was trading around $9,000. The chart below shows the progression of Bitcoin mining difficulty over the last 12 months.

Threats

- A survey of 1,233 El Salvador’s citizens, conducted by pollster Disruptiva, suggests that majority of the country’s people are wary of the implementation of the legislated Bitcoin Law, which makes the cryptocurrency a legal tender within the country. Around 54% of respondents viewed the law as “not at all correct”, while only 20% totally supported it. Further, 46% responded that they do not know anything about Bitcoin, and 65% would not be keen on being paid in the crypto. Although the Bitcoin Law is set to come into effect on September 7, 2021, there seems to a hesitancy amongst El Salvadorians regarding using the cryptocurrency for everyday purposes.

- Santander Bank in the U.K. announced that it will no longer allow its customers to send payments to Binance, following the footsteps of Barclays and Natwest, citing warnings from U.K.’s Financial Conduct Authority (FCA). FCA warned consumers that Binance Markets Limited, which is a separate entity from Binance exchange, could not operate and engage in any regulated activity in the U.K.

- The Economic Commission for Latin America and the Caribbean (ECLAC) warned that El Salvador’s Bitcoin Law poses several systemic risks as well as money laundering risks. ECLAC, which is a United Nations’ regional commission to encourage economic cooperation, added that Bitcoin does not fulfil some basic functions of money and is subject to extreme volatility. This warning comes on back of the International Monetary Fund stating that accepting Bitcoin as legal tender could pose legal and financial concerns, and the World Bank refusing to assist El Salvador in the country’s transition to adopting the cryptocurrency.

Gold Market

This week spot gold closed at $1,808.32, up $21.02 per ounce, or 1.18%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 0.12%. The S&P/TSX Venture Index came in off 3.09%. The U.S. Trade-Weighted Dollar fell 0.13%.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Jul-6 | Germsny ZEW Survey Expectations | 75.2 | 63.3 | 79.8 |

| Jul-6 | Germany ZEW Current Situation | 5.5 | 21.9 | -9.1 |

| Jul-8 | Initial Jobless Claims | 350k | 373k | 371k |

| Jul-13 | Germany CPI YoY | 2.3% | — | 2.3% |

| Jul-13 | CPI YoY | 4.9% | — | 5.0% |

| Jul-14 | PPI Final Demand YoY | 6.7% | — | 6.6% |

| Jul-14 | China Retail Sales YoY | 10.9% | — | 12.4% |

| Jul-15 | Initial Jobless Claims | 350k | — | 373k |

| Jul-16 | Eurozone CPI Core YoY | 0.9% | — | 0.9% |

Strengths

- The best performing precious metal for the week was gold, up 1.18%. Compass Gold reported the results of the recently completed drilling at the Old Sam and Dialéké prospects, located on the Company’s Sikasso Property in Southern Mali. The first drilling results at the Old Sam target, 40 km south of Tarabala, are highly encouraging. Initial drilling has discovered a shallow zone of low-grade gold.

- Gold continued to climb above $1,800 an ounce this week as Treasury yields and the U.S. dollar fell ahead of the release of Federal Reserve minutes. Central banks may be regaining their appetite for buying gold after staying on the sidelines for the past year. Central banks from Serbia to Thailand have been adding to their gold holdings, writes Bloomberg this week, and Ghana recently announced plans for purchases, as the specter of accelerating inflation looms and a recovery in global trade provides the firepower to make purchases. A rebound in buying, which had dropped to the lowest in a decade, would bolster the prospects for gold prices as some other sources of demand falter, the article continues.

Weaknesses

- The worst performing precious metal for the week was silver, down 1.39% after two consecutive weekly gains. Exchange-traded funds cut 168,278 troy ounces of gold from their holdings in the last trading session, bringing this year’s net sales to 6.4 million ounces, according to data compiled by Bloomberg. The sales were equivalent to $299 million. Total gold held by ETFs fell 6% this year to 100.7 million ounces, the lowest level since May 2020.

- The Perth Mint says gold coin and minted bar sales totaled 72,910 ounces last month, according to figures on its website. Sales compare with 91,146 ounces in May, according to previously released data.

- Facing several headwinds (expensive valuations and pandemic travel restrictions), global gold M&A (merger and acquisition) activity in the second quarter slowed quarter-to-quarter. Just nine transactions were announced versus 14 in the first quarter.

Opportunities

- Roscan Gold reported positive results from an additional 14 diamond drilling and reverse circulation holes totaling 3,066 meters at the Southern Mankouke Zone. Mankouke Discovery Zone, or MS1, confirmed mineralization open at depth and Mankouke Discovery Zone, or MS3, shows a potential high-grade extension to the west, the company said in a news release.

- AngloGold Ashanti appointed former BHP Group executive Alberto Calderon to its top job, ending a nearly year-long head hunt that has weighed on the shares of the No. 3 gold producer. AngloGold has not had a permanent CEO since Kelvin Dushnisky’s abrupt departure last September after holding the position for just two years. The Johannesburg-based miner’s shares have underperformed its peers in the past year as the CEO hunt dragged on and the company had to suspend operations at a mine in Ghana.

- Silvercorp reported assays from the 2021 exploration program at the SGX mine at its Ying Mining District. The gold exploration results are encouraging given the geological belt hosting the Ying Mining District is known more for its gold endowment than silver and base metals. The market is not ascribing any value to the gold potential at Ying and offers investors a free option to considerable exploration upside.

Threats

- First Mining reports that a forest fire is currently active within one kilometer of the camp at the company’s Springpole Gold Project located in northwestern Ontario. Fire crews from the Ministry of Natural Resources and Forestry have been working on containment measures over the weekend, including both ground and aerial suppression using water bomber aircraft and helicopters. Due to the proximity of the forest fire, First Mining has suspended operations at Springpole, and MNRF firefighters are currently staged at the Springpole site working to contain the fire.

- Bank of America lowered its 2021 silver price forecast 3.9% to $27.71 per ounce. Despite this, they prefer silver due to rising demand in solar panels and growth in electrical applications.

- Russia’s second-biggest gold miner plans to plant a forest two-thirds the size of Manhattan to comply with new legislation as President Vladimir Putin tries to curb the nation’s carbon emissions. Russian companies must plant a new tree for every tree they cut down under new legislation that started taking force earlier this year. In addition to the forest, to offset emissions, diesel-fueled power stations and other equipment will be switched to electric.

Leaders and Laggards

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (06/30/2021):

Alaska Air Group Inc.

Ryanair Holdings PLC

Sydney Airport

Wizz Air Holdings PLC

Vestas Wind Systems A/S

Compass Gold Corp

Roscan Gold Corp

AngloGold Ashanti

Silvercorp Metals

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The ZEW Indicator of Economic Sentiment is calculated from the results of the ZEW Financial Market Survey. It is constructed as the difference between the percentage share of analysts that are optimistic and the share of analysts that are pessimistic for the German economy in six months. The National Federation of Independent Business’s (NFIB) Index of business optimism is based on responses from 1221 member firms. Frank Holmes has been appointed non-executive chairman of the Board of Directors of HIVE Blockchain Technologies. Both Mr. Holmes and U.S. Global Investors own shares of HIVE. Effective 8/31/2018, Frank Holmes serves as the interim executive chairman of HIVE.