Should You Buy the Panic?

Date Posted: March 13, 2020

Read time: 58 min

If anyone has the right to say "I told you so," it's Bill Gates.Two years ago, the co-founder, former CEO and now former board member of Microsoft urged governments to step up their preparedness in the event of a modern global pandemic. Such an event, Gates warned, could conceivably be more dangerous than any other threat facing humanity today, including nuclear proliferation, due mainly to the fact that we've become so interconnected.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

If anyone has the right to say “I told you so,” it’s Bill Gates.

Two years ago, the co-founder, former CEO and now former board member of Microsoft urged governments to step up their preparedness in the event of a modern global pandemic. Such an event, Gates warned, could conceivably be more dangerous than any other threat facing humanity today, including nuclear proliferation, due mainly to the fact that we’ve become so interconnected.

Because new vaccines take time to develop and deploy, the U.S. in particular needed to invest in “antiviral drugs and antibody therapies that can be stockpiled or rapidly manufactured to stop the spread of pandemic diseases or treat people who have been exposed,” Gates said in a speech at the time.

And in a 2018 interview with STAT, he said he found it “strange… that the world isn’t doing more” to brace itself for a potential pandemic.

“We think the idea of spending what would be a tiny part of the budget to be ready for a pandemic makes sense,” he added.

The 10 Percent Golden Rule Remains Prudent

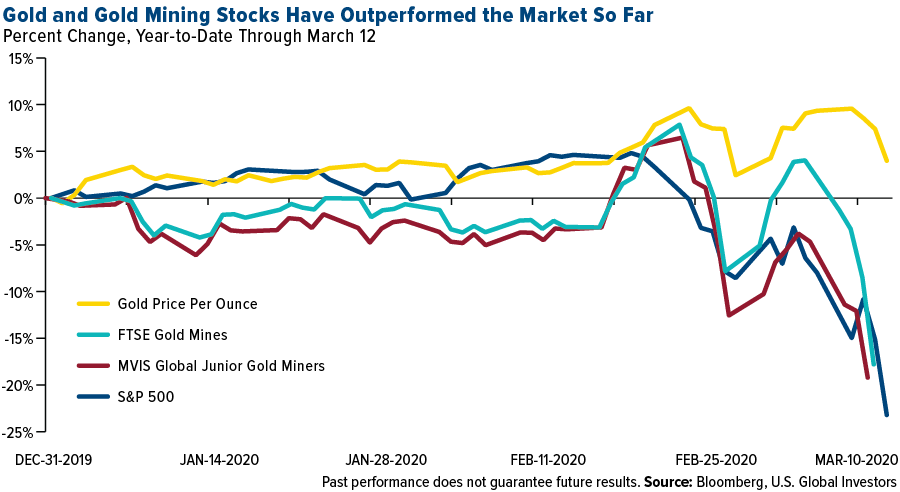

This last comment reminds me why it’s so important to allocate 10 percent of your portfolio in gold and gold mining stocks. It “makes sense” to be ready for a market crash such as the one we’re seeing now as a result of the spread of COVID-19, which the World Health Organization (WHO) just this week declared a pandemic and, today, President Donald Trump declared a national emergency.

Gold bullion went negative for the year as of Friday, as investors liquidated their holdings to ride out the volatility. And although they haven’t sold off as deeply as the rest of the market, gold mining stocks look cheap now, meaning it may be time to consider adding to your exposure.

As of Friday, gold prices were up about 3.5 percent for the three-month period and up 18 percent from a year earlier. What this means is that we could see very attraction revenue and cash flow from gold mining stocks this quarter.

The yellow metal could also continue to benefit with additional monetary accommodation. Yesterday the Federal Reserve announced as much as $1.5 trillion in capital injections to calm liquidity issues. How much extra liquidity will be needed to calm markets before all is said and done? Five trillion dollars? Ten trillion? I’ve discussed the relationship between excessive money printing and the price of gold before, and suggested it could easily surge to $10,000 an ounce, especially with government bonds around the world still offering negative yields.

Silver Coins Sell Out

Meanwhile, 2020 America Silver Eagle coins temporarily sold out, the U.S. Mint announced yesterday.

“Our rate of sale in just the first part of March exceeds 300 percent of what was sold last month,” the Mint said in a press release.

We’ve long known that silver has antibacterial and antiviral properties, which may have prompted at least some of the heavy buying. Having said that, it hasn’t been proven that the white metal is effective in preventing or “curing” the coronavirus, and in fact a couple of public figures—radio host Alex Jones and televangelist Jim Bakker—are currently being investigated by state attorneys general for claiming as much.

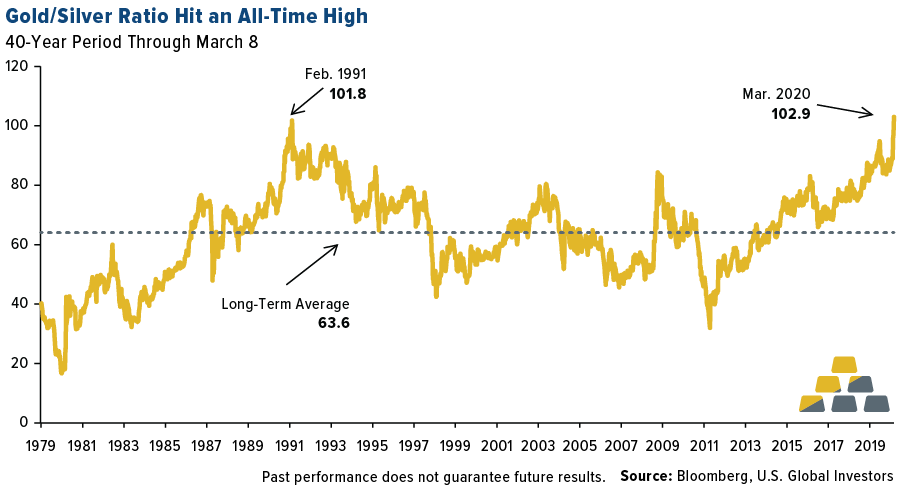

Despite investor demand, silver prices have tumbled along with other precious metals that have industrial applications, palladium included. As a result, the gold/silver ratio, which tells you how many ounces of silver it takes to buy one ounce of gold, rose to its highest level on record this week. As of March 8, the ratio was nearly 103, beating the previous record of 101.8 in February 1991.

A New Definition to “March Madness”

Is COVID-19 what Gates had in mind a couple of years ago? I’ve heard more than a few times, as I’m sure you have, that the media has overblown the risk the coronavirus poses. After all, the seasonal flu kills tens of thousands of people every year, and yet we generally don’t close schools, cancel music festivals or quarantine entire cities during flu season. The National Collegiate Athletic Association (NCAA) has cancelled March Madness, joining major league basketball, hockey, soccer, baseball and more in suspending play.

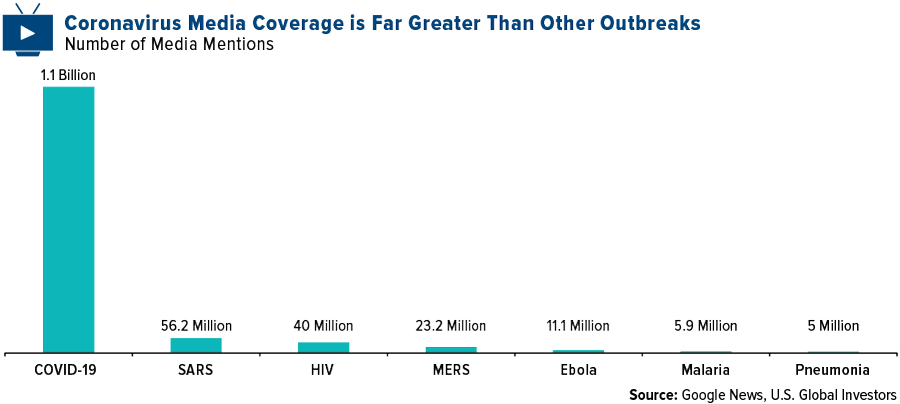

Compared to past viral outbreaks—SARS, MERS and certainly Ebola—COVID-19 appears to be less fatal, and yet has received far more media coverage.

Perhaps paradoxically, that’s part of the reason why COVID-19 has had a much bigger impact on public health and the economy relative to those other diseases. Its spread “is promoted by the combination of a less abrupt onset of symptoms and the virus’s ability to replicate rapidly in the upper respiratory tract at the early onset of the illness when individuals are asymptomatic,” according to a research report by the National Bank of Canada. People, therefore, “carry on with their usual activities while unknowingly infecting others.”

This, in turn, has the potential to put “sudden and tremendous pressure” on our health systems. Just look at Italy, which is currently on lockdown with over 15,000 confirmed cases, the most of any country outside China. Hospitals there are completely overwhelmed, with some doctors reportedly having to make tough decisions about who does and does not get treatment.

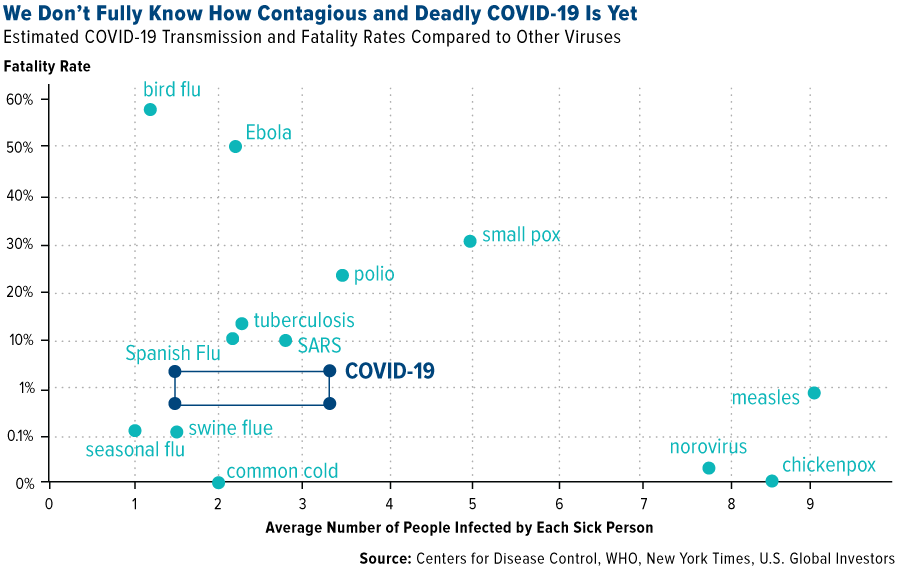

To make matters worse, we don’t fully know just how contagious and deadly COVID-19 is yet. It’s a novel, as in “new,” coronavirus. I have no doubt in my mind that we’ll eventually demystify the virus and develop new treatments and vaccines, but for now, the uncertainty can be paralyzing for some.

The 9/11 attacks ushered in the creation of the Department of Homeland Security, the Transportation Security Administration (TSA) and more. What will this pandemic bring in? My guess is that it may lead to better innovations to detect if people are running high temperatures in airports, schools and other public places, not to mention stronger border controls for right of entry to prevent the spread of disease.

The Virus of Fear

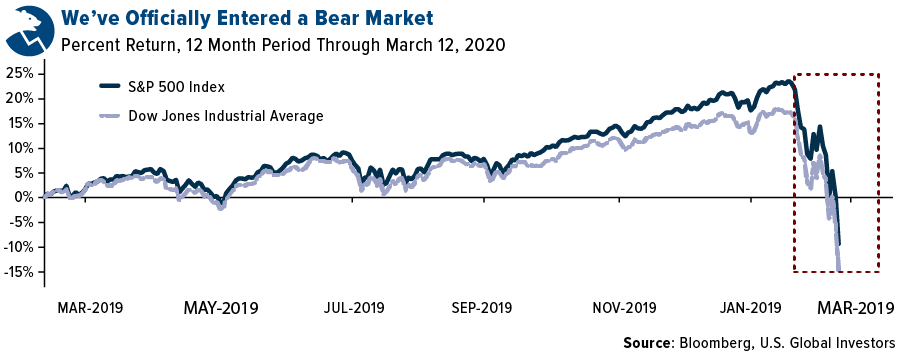

You may believe the fear over COVID-19 is unwarranted, but you can’t deny that there have been some serious ramifications, not least of which is the end of the historic U.S. stock bull market. In as little as 20 days, major averages fell more than 20 percent off their highs, wiping out nearly all of the gains since January 2019.

The U.S. wasn’t alone, of course. The world aggregate exchange market cap has lost a mind-boggling $16.1 trillion. Meanwhile, CLSA reported an all-time record correlation in the degree to which global stocks sold off, “even surpassing that of 2008, reflecting that global selloffs are taking place together with an unprecedented synchrony.”

This has created some very attractive buying opportunities, as I mentioned last week. Global airline stocks were most oversold since September 2001, following the attacks on 9/11, and with Brent crude oil trading at just under $35 a barrel, carriers have received a substantial cut to their fuel costs. Warren Buffett and other deep value investors have bought, and our airline ETF has exploded in volume and new assets. According to JPMorgan, North American airlines produce 21 percent of global capacity and 65 percent of global profitability, so they are well equipped to weather this downturn.

On a final note, bond investors—particularly in tax-free municipal bonds—have been rewarded as yields fell and prices surged, helping to offset weakness in their equity positions.

Watch my interview with Small Cap Power on money printing and gold mining by clicking here!

Gold Market

This week spot gold closed at $1,529.83, down $144.00 per ounce, or 8.60 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 28.99 percent. The S&P/TSX Venture Index came in off 22.79 percent. The U.S. Trade-Weighted Dollar rose 2.63 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Mar-11 | CPI YoY | 2.2% | 2.3% | 2.5% |

| Mar-12 | PPI Final Demand YoY | 1.8% | 1.3% | 2.1% |

| Mar-12 | Initial Jobless Claims | 220k | 211k | 215k |

| Mar-12 | ECB Main Refinancing Rate | 0.000% | 0.000% | 0.000% |

| Mar-13 | Germany CPI YoY | 1.7% | 1.7% | 1.7% |

| Mar-17 | ZEW Survey Expectations | -27.2 | — | 8.7 |

| Mar-17 | ZEW Survey Current Situation | -30.0 | — | -15.7 |

| Mar-18 | Eurozone CPI Core YoY | 1.2% | — | 1.2% |

| Mar-18 | Housing Starts | 1500k | — | 1567k |

| Mar-18 | FOMC Rate Decision (Upper Bound) | 0.75% | — | 1.25% |

| Mar-19 | Initial Jobless Claims | 220k | — | 211k |

Strengths

- The best performing metal this week was gold, with its 8.60 percent drop. Central banks around the world joined the Federal Reserve in injecting cash into stressed markets and seeking to calm panicked companies and investors. The Fed pledged to provide more than $5 trillion of cash and stem a surge in short-term financing rates as the dollar surged on a demand for liquidity.

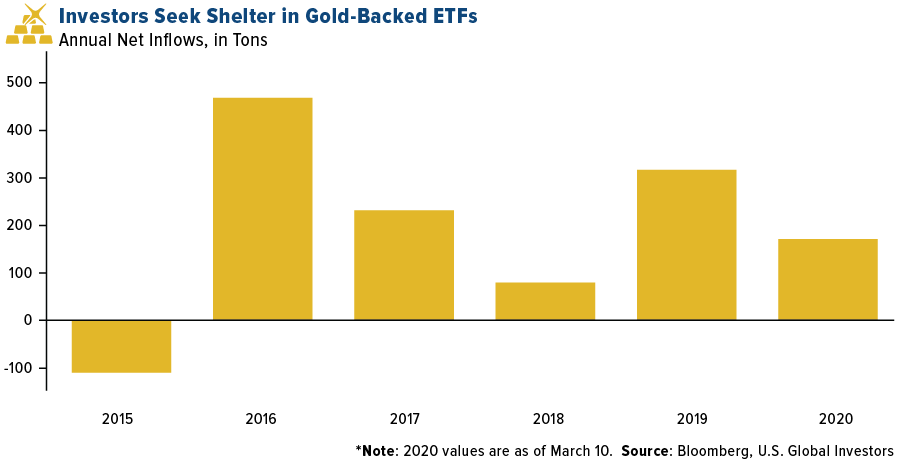

- Investors continue to pile into gold as fears of the coronavirus intensify. Holdings in gold-backed ETFs already total more than half of the 323.4 tons added in 2019, according to Bloomberg data. ETFs added 55 tons of gold in the three days ended March 11. Indian investors are also buying gold. Net inflows into gold-backed ETFs totaled 14.83 billion rupees, or about $201 million in February – the biggest increase since the funds first launched in 2007. The U.K.’s Royal Mint said that weekly precious metals sales quadrupled from the same period a year earlier last week. The U.S. Mint reported that it has sold out of American Eagle silver coins. St. Joseph Partners noted in their weekly letter the drop in prices has triggered a retail run in the physical precious metals market: “In a matter of hours, while 99 percent of America has yet to buy its first ounce of physical gold for diversification, the system has largely been cleaned out of secondary monetary metals.” Gold trading tracked by the London Bullion Market Association’s LBMA-i service reached almost $100 billion on Monday – the highest ever daily volume.

- Mark Mobius, veteran emerging markets investor, said in a Bloomberg TV interview that “with this fear crisis, people want to get into cash so they sell everything, including gold. But I think the trend for gold is going to continue to go up.” Mobius added that if there is a price correction he might add to his gold position.

Weaknesses

- The worst performing metal this week was palladium, down 29.85 percent. As investors scramble for liquidity in this market panic, they are selling gold. Gold jumped above $1,700 an ounce early this week, then fell below $1,600 an ounce on Thursday and ended the week at $1,529.83. The yellow metal has been one of the only assets to outperform, leading to investors selling to take profits or were subject to margins calls. ABM Amro issued a cautious price forecast of gold averaging $1,500 an ounce in the second quarter of this year.

- BASF announced that it has developed tri-metal catalyst technology that would enable partial substitution of palladium for cheaper platinum in light-duty gasoline vehicles, reports Bloomberg. Although positive for platinum demand, this is negative for palladium, whose recent rally is largely due to demand for use in catalysts. Palladium was one of 2019’s best performing commodities, but it has been caught in the rout.

- The Bureau of Labor Statistics, the Census Bureau and the Bureau of Economic Analysis could all face trouble collecting reliable figures on key data including jobs and inflation, according to Bloomberg. Because of the coronavirus impact, Americans and businesses might be unwilling to respond to surveys and surveyors might find stores closed or be unable to work from home.

Opportunities

- Suki Cooper, precious metals analyst at Standard Chartered Bank, said in a Bloomberg TV interview this week that “global monetary conditions are going to be key for the next move higher in gold.” This comes as central banks globally prepare fiscal stimulus and additional interest rate cuts to support economies. UBS raised its 2020 average gold price forecast to $1,650 an ounce, up from $1,600 an ounce previously. They also think that gold has the potential to test the high $1,700s in the first half of this year. Australia & New Zealand Banking Group Ltd. said in a report this week that there’s a high probability of gold reaching $2,000 an ounce in the second quarter depending on the extent of the coronavirus impact, reports Bloomberg.

- Scotiabank analyst Tanya Jakusconek wrote in a note to clients this week that gold miners are trading at levels cheaper than those seen in the 2008 financial crisis. Gold equities are trading at around a 16 percent discount to gold prices – lower than the 10 percent discount in 2008. Gold miners could be one of the few sectors to report positive quarterly earnings next month, as spot prices have averaged at least $100 more per ounce than in the fourth quarter of 2019. Desjardins wrote in a note than linear regression suggests a further 12 percent increase to cash flow in the first quarter for gold miners. Oil crashed this week, which could be a positive for miners, as fuel is a big cost and lower prices will increase their margins.

- How might gold perform during this market crisis? Looking back to the 2008 financial crisis, gold rebounded and hit bottom long before the S&P 500 did. From mid-July 2008 to October 24, the GLD fell nearly 30 percent and the GDX sank 70 percent. However, the GLD slide was mostly over by September 2008, before Lehman Bros. even came down. From October 24 to March 6, 2009, the S&P fell another 21 percent, after falling 40 percent the six weeks prior, while GLD surged 34 percent and the GDX more than doubled, writes Jed Graham in Investor’s Business Daily. This could mean that again, gold could recover before the wider stock market this time around. The surge in retail buying of physical metals this week with the drop in prices may signal retail demand for gold mining companies could be next.

Threats

- The dollar rose as investors scrambled to get their hands on cash in what some are calling an irrational “fear trade”. If the stress in the dollar funding market continues, it could lend further support for higher prices. A stronger dollar has historically been negative for the price of gold. This week the historically liquid bond market turned illiquid. Buyers had been steadily pouring money into bond and municipal bond mutual funds for over a year, then abruptly pulled back over the last two weeks. For municipal bond funds, their yields which are typically tax-free are now trading above Treasury bond yields. Even bond ETFs that just buy U.S. Government debt are redeeming units at significant discounts to their net asset value if an investor is demanding liquidity.

- The Fed announced $1.5 trillion of liquidity injections in the Repo markets. However, this is concerning since the balance sheet last stood at a whopping $4.24 trillion. For all practical purposes, QE has just started again with the Fed buying $33 billion of Treasuries across the curve just on Friday. Because of these liquidity concerns, the latest reading for Bloomberg Economics’ U.S. recession probability model shows the chances of a downturn in the next 12 months rising to 53 percent. Expect even more stimulus should a recession emerge.

- The non-partisan U.S. Government Accountability Office found that there are more than 215,000 abandoned hardrock mine sites that pose either a physical safety risk or an environmental risk to the public. Taxpayers could face an $11.6 billion cleanup bill on these mines, on top of the $1.9 billion that was spent from 2008 to 2017 to clean sites. Senator Tom Udall released the report to underscore why Congress must act swiftly to update the outdated 1872 hardrock mining law that keeps mining companies from being liable for cleaning mine sites.

Index Summary

- The major market indices finished sharply down this week. The Dow Jones Industrial Average lost 10.36 percent. The S&P 500 Stock Index fell 8.80 percent, while the Nasdaq Composite fell 8.17 percent. The Russell 2000 small capitalization index lost 16.57 percent this week.

- The Hang Seng Composite lost 8.61 percent this week; while Taiwan was down 10.54 percent and the KOSPI fell 13.17 percent.

- The 10-year Treasury bond yield rose 21 basis points to 0.979 percent.

Domestic Equity Market

Strengths

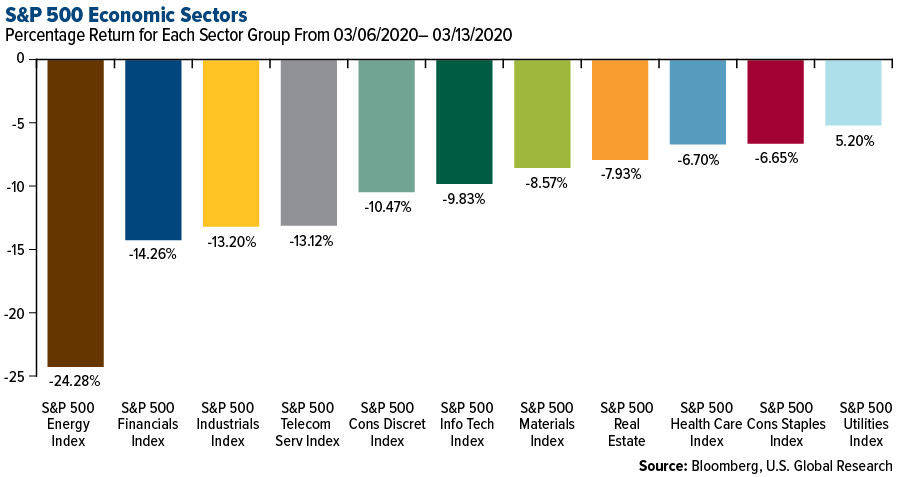

- Information Technology was the best performing sector of the week, decreasing by 5.2 percent versus an overall decrease of 10.72 percent for the S&P 500.

- Cabot Oil & Gas Corp was the best performing S&P 500 stock for the week, increasing 11.18 percent.

- U.S. stocks rebounded from the worst day since 1987 on Friday amid signs policy makers around the world are taking action to stave off the economic fallout from the coronavirus. The European Union prepared to suspend government spending rules, and regulators in Italy and Spain banned short-selling on some stocks. China’s central bank said it would pump in $79 billion to bolster the economy.

Weaknesses

- Energy was the worst performing sector for the week, decreasing by 24.28 percent versus an overall decrease of 10.72 percent for the S&P 500.

- Apache Corp was the worst performing S&P 500 stock for the week, falling 61.59 percent.

- The stock market has now wiped out the entire $11.5 trillion of value it gained since President Trump’s 2016 election victory. The Trump administration initially downplayed the virus, with top economic adviser Larry Kudlow calling the outbreak "contained" on February 25.

Opportunities

- Businesses plan to spend more money on Amazon and Microsoft and less on Oracle, IBM and VMware, according to a new survey. Cloud services are claiming a big slice of corporate IT budgets.

- Jack Dorsey will remain the CEO of Twitter as part of a truce it struck with an activist hedge fund pushing for change. Activist investor Elliott Management has reached a deal with Twitter alongside $1 billion in investment from Silver Lake.

- Magic Leap, the smart-glasses startup that raised over $2.6 billion from investors like Google, is reportedly exploring a sale. Magic Leap is also exploring options including partnerships and a possible stock market listing, Bloomberg reports.

Threats

- Global airline stocks plunged after President Trump announced a surprise travel ban from Europe to the U.S. Airlines are expected to miss out on $113 billion in revenue from the virus travel disruptions.

- Adidas expects a $1 billion coronavirus hit to China sales. "The virus hit looks worse than feared," Jefferies analyst James Grzinic wrote in a note.

- Coronavirus shock is pushing highly indebted companies toward financial ruin — and a risky $1 trillion market is already showing the damage a recession would do.

The Economy and Bond Market

Strengths

- The number of Americans who applied for unemployment benefits in early March fell slightly and remained near a 50-year low, indicating the coronavirus has not caused an influx of layoffs so far. Initial jobless claims dropped 4,000 to 211,000 in the seven days ended March 7.

- The Federal Reserve took aggressive steps Thursday to ease what it called “temporary disruptions” in Treasuries, flooding the market with liquidity and widening its purchases of U.S. government securities in a measure that recalls the quantitative easing it used during the financial crisis. The Federal Reserve Bank of New York said in a statement that the “changes are being made to address highly unusual disruptions in Treasury financing markets associated with the coronavirus outbreak” and had been done at the direction of Fed Chairman Jerome Powell in consultation with the Federal Open Market Committee. The New York Fed offered $500 billion in a three-month repo operation and said it would repeat the exercise tomorrow, along with another $500 billion in a one-month operation, and continue on a weekly basis for the rest of the monthly calendar. This adds a massive jolt of liquidity to financial markets that will also expand the Fed’s balance sheet for the duration of operations.

- The NFIB Small Business Optimism Index increased to 104.5, a reading in the top 10 percent of all readings in the history of the survey. February’s survey responses were collected prior to the escalation of coronavirus outbreak and Fed rate cut.

Weaknesses

- U.S. producer prices fell by the most in five years in February, pulled down by declines in the costs of goods such as gasoline and services. This could be an initial sign that the coronavirus pandemic is beginning to suppress demand for services like transportation, hotel accommodation, entertainment and recreation.

- S&P economist Beth Ann Bovino notes that “with the material headwinds to growth in the near term, we now think annual GDP growth for 2020 will be 0.3 percent lower than our 1.9 percent pre-virus forecast.”

- Oil fell 21 percent, its biggest drop in decades, following the outbreak of a Saudi Arabia-Russia price war. Goldman Sachs cut its Brent forecast to $30 a barrel.

Opportunities

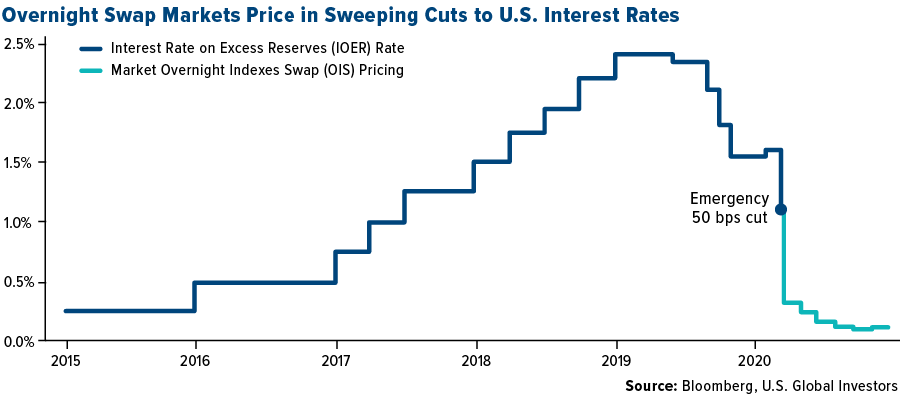

- After the Fed’s emergency 50 basis point cut last week, markets are pricing in almost 75 basis points of further easing at its March meeting next week, with a return to the 0 percent lower bound expected by the end of the year, according to data compiled by Bloomberg. Central banks around the world, already facing pressure to blunt the economic fallout from the coronavirus outbreak, must now contend with a full-blown crude oil price war after the dramatic breakdown of talks between OPEC and Russia.

- Democrats are preparing to post a plan to mitigate some of the economic blows from the coronavirus outbreak after multiple rounds of negotiations between House Speaker Nancy Pelosi and Treasury Secretary Steven Mnuchin. That would be followed by a vote in the House, sending it to the Senate for action likely early next week.

- The Bank of England cut rates by 0.5 percent in an emergency coronavirus response, mirroring the Fed. The central bank said the cut would "support business and consumer confidence at a difficult time" as well as boost the cash flows of businesses and households and improve access to credit.

Threats

- ‘Headed for permanent recession’: Paul Krugman sounds the alarm after Treasury yields tumbled and interest rates plunged. "Markets are implicitly predicting not just a recession, but multiple years of economic weakness."

- Christine Lagarde reportedly warned the coronavirus could cause the worst economic disaster since the financial crisis. The European Central Bank president told European leaders that they risk "the collapse of part of your economies" if they don’t take urgent action, Bloomberg reported.

- Infrastructure projects that depend on consumer spending could face financial strains as people choose not to travel and attend events due to the coronavirus outbreak, according to S&P Global Ratings.

Energy and Natural Resources Market

Strengths

- The best performing major commodity for the week was natural gas, which surged 11.71 percent as shellacked oil prices will discourage future drilling in the U.S. shale play. The Stoxx Europe 600 Basic Resources Index rose as much as 9.3 percent on Friday morning, the most since April 2009, as base metals bounced, reports Bloomberg. BHP was up more than 9.5 percent while Anglo American was up 9 percent. Commodity ETFs saw 2.7 billion of inflows last week, led by energy ETFs, which had 2.18 billion of inflows.

- In a week filled with negative news, one positive development is in diversity in the boardroom. Goldman Sachs Group Inc.’s fund management unit said that it wants a woman on every corporate board and that it will vote against nominating committees globally that don’t have a single woman on the board. Katie Koch, who leads Goldman’s global stewardship team, said in an interview that “we know diversity drives better performance” and “we’ve seen it in our own business, therefore we are demanding it of our portfolio companies.”

- Although the oil war between Russia and Saudi Arabia is negative for many, Russian producers are ready to survive the flood of Saudi crude. The production costs of Rosneft, Lukoil and Gazprom – Russia’s majors – were below $12 a barrel in 2019. Bank of America analysts wrote in a note this week that Russia has some of the world’s lowest production costs, a flexible tax system and a free-floating ruble – enabling producers to keep pumping until oil hits $15 to $20 per barrel.

Weaknesses

- The worst performing major commodity for the week was crude oil, which fell 17.97 percent. It was a terrible week for most assets and commodities globally, but one of the hardest hit was oil. The spread of COVID-19 hurting demand for crude was already a huge negative, and then over the weekend Russia and Saudi Arabia began a dispute over oil production. The OPEC+ coalition failed and oil crashed 31 percent. Natural gas also fell to a 21-year low. American shale drillers already had a massive profitability problem, and it just got worse thanks to oil’s price collapse. Bloomberg News writes that more defaults and bankruptcies among shale producers are all but certain. According to data from Rystad, certain wells drilled by Exxon, Occidental, Chevron and Crownquest Operating can turn profits at $31 per barrel. Almost all wells now lose money, and if oil falls further, the wells drilled by those four companies could also become unprofitable.

- Copper formed a bearish death cross on Tuesday, where the 50-day moving average fell below the 200-day moving average. This is especially troubling as copper is seen as a gauge of expectations for global growth. Copper finished the week down 2.79 percent. Caterpillar, a company also seen as a gauge of economic activity, posted its worst machine sales since 2016, citing the coronavirus outbreak as hurting industries that the company supplies. Bloomberg reports that Caterpillar shares are down 38 percent so far this year.

- Sasol, a South African fuel and chemical producer, fell by a record 50 percent on Monday after news of the Saudi Arabia-Russia feud hit markets and oil prices. The company was already facing high debt levels and cost overruns, and then the biggest drop in oil prices since 1991 hit. According to data from the London Metal Exchange, cancelled warrants for nickel fell by 17,100 tons – the biggest daily drop since data going back to 1997.

Opportunities

- Los Angeles has a goal to become the first city in the nation to use renewable hydrogen to produce electricity. Bloomberg writes that the city has a two-step plan to replace 1,900 megawatts of coal-fired generation with natural gas and then slowly expand to hydrogen. Mitsubishi Hitachi Power Systems won the contract for turbines and says the new plant will help make a faster transition from gas to renewable hydrogen.

- Oil is crashing and was less than $35 a barrel on Monday, which could was positive for natural gas prices. According to Goldman Sachs Group, the lower oil prices should reduce shale drilling, of which natural gas is a byproduct. Natural gas has suffered for months due to an overproduction, but now there is the opportunity for production to finally slow.

- According to a study by a group of international scientists, a new filtration technique could reduce the time it takes to produce lithium raw materials in South America’s evaporation ponds from months to just hours. Bloomberg writes that the study indicates about 90 percent of contained lithium can be recovered using this new filter system, compared to just 30 percent when producers use the existing process of pumping brines into a series of ponds and waiting for the sun to evaporate the liquid.

Threats

- As mentioned above, Saudi Arabia and Russia are in an oil price war. After hoping to get Russia to reduce production in an effort to curb supplies and support prices, the OPEC+ coalition failed after Russia decided not to cooperate. Now Saudi Arabia is flooding the market with cheap crude. In February, Saudi Arabia produced 9.7 million barrels a day, and now wants to boost supply to 12.3 million a day. Then on Wednesday Saudi Arabia escalated further by saying it will produce 13 million a day. Major Russian producer Rosneft said it could start increasing output as soon as April 1. Russia’s finance minister said that the country is prepared for a price slump and has sufficient reserves to cover lost revenue for six to 10 years with oil prices at $25 a barrel. The price war is also seen as a move by Russia to hurt the U.S. oil industry. America is now at risk of losing its status as a net exporter as falling oil prices give a leg-up to foreign oil and hurt domestic shale drillers. The Energy Information Administration said that U.S. oil production will average 12.7 million barrels per day in 2021, the first annual drop since 2016. A long-term price war could have a long-lasting negative impact on the oil industry globally, and on the economies of Saudi Arabia and Russia, which are closely tied to oil prices.

- The biggest threat, of course, is that COVID-19 will continue to spread. Weaker economies can hurt demand for commodities, especially oil. The Bloomberg Commodity Total Return Index is heading for its worst quarterly return since the 2008 financial crisis, already down over 17 percent. President Trump addressed the nation on Wednesday night, but it failed to reassure investors and announced a 30-day travel ban on Europe that spurred confusion. A troubling development about the virus is that it can live in the respiratory tract for as long as 37 days and many infected patients have no symptoms. President Trump then declared a national emergency on Friday afternoon.

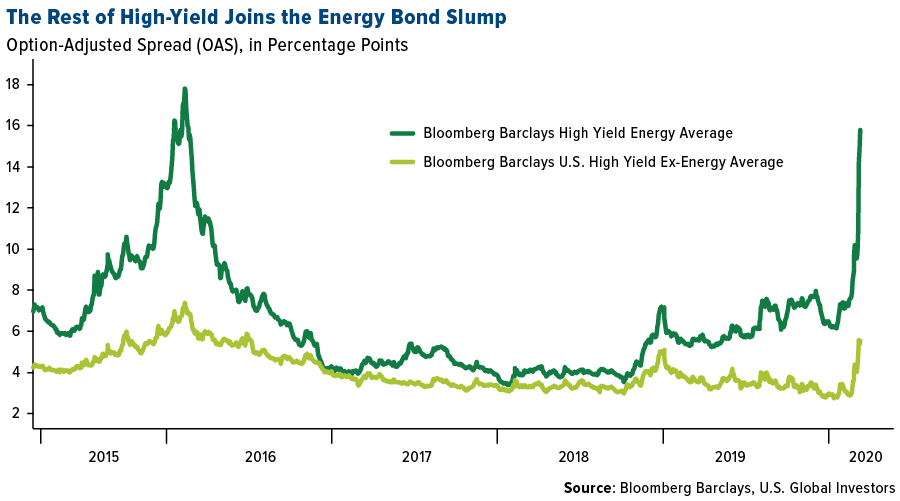

- The credit rout is far from over, and it’s swiftly moving beyond energy debt, reports Bloomberg News. High-yield junk energy bonds fell more than 18 percent this week and it’s only a matter of time before other junk bonds catch up to the distress. High-yield energy rose to 1,575 basis points and the rest of junk was at 552 basis points on average on Thursday. Oil and gas companies are in trouble and we’ll soon see if investors are up to lending to them. One example is Whiting Petroleum Corp., which has $774 million of bonds maturing in a year and not much cash. Bloomberg reports that the producer has $260 million of convertible bonds due on April 1 and only $8.6 million cash on hand. Bloomberg Intelligence data shows that U.S. distressed debt reached a new cycle high of $209 billion after the sell-off, and almost half of that was tied to energy companies.

Emerging Europe

Strengths

- Turkey was the best relative performing country this week, losing 12.8 percent. Investors observed large losses in global markets due to the coronavirus spreading rapidly and a collapse in the oil price. However, on a relative basis, Turkish equites outperformed because the government banned short selling on all stocks listed on the Istanbul exchange on February 28. That was the day 33 Turkish soldiers were killed in Syria.

- The euro was the best relative performing currency this week, losing 1.8 percent. The euro was supported by the ECB’s surprise move not to cut the bank’s deposit rate by an additional 10 basis points.

- Health care was the best performing sector among eastern European markets this week.

Weaknesses

- Poland was the worst performing country this week, losing 22 percent. CCC, a shoe-maker and distributor, lost 47.5 percent of its market share in the past five days, on the fear that shopping malls will be closed in order to contain the spread of the virus. Coronavirus cases in Poland are growing, and this week the country reported its first death.

- The Russian ruble was the worst performing currency in the region this week, losing 5.2 percent. The price of Brent crude oil dropped by 21.6 percent in the past five days, after the OPEC agreement to cut oil production broke off. Historically the ruble moves in-line with the price of oil.

- Financial was the worst performing sector among eastern European markets this week.

Opportunities

- Italy announced spending of 25 billion euros to help its economy tackle the financial fallout from the coronavirus lockdown. Last week the U.S. Federal Reserve cut its main rate by 50 basis points. On Thursday the ECB surprised the market by not cutting rates, but announced measures to support bank lending and expanded its assets purchase program by 120 billion euros. More coordinated cuts and stimulus from central banks around the world are expected.

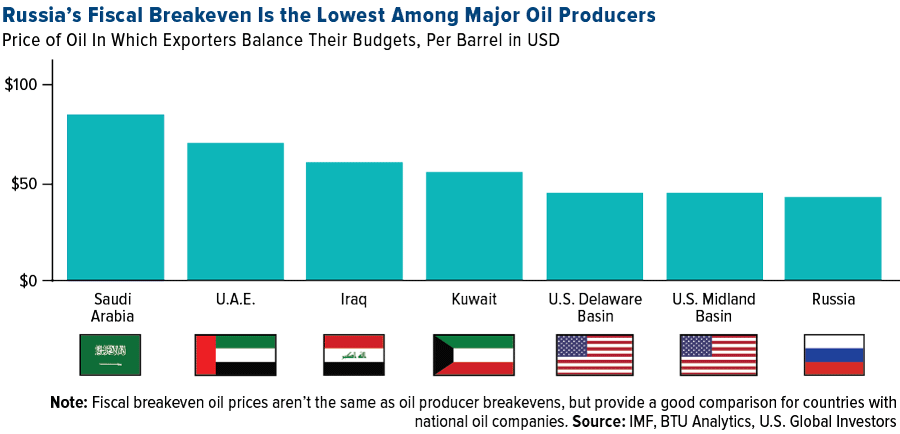

- In the short-term, Russia is well positioned to withstand lower oil prices. Russia’s fiscal breakeven is around $42 per barrel – about half of what Saudi Arabia needs to balance its budget. Russia’s Finance Minister said on Monday that it would draw from its $150 billion national wealth fund in order to boost budgetary spending. These reserves can allow for a $1.7 billion stimulus a month for the next six to 10 years.

- According to Kostas Tsigkourakos from Wood & Company, Greece and Turkey should positively surprise investors. Turkey’s energy bill is $1 billion less a month with oil prices at $35 per barrel. The other factor that makes Turkey resilient is that it is a domestic consumption-oriented economy and household debt is low. Greece is relatively safe fundamentally, as it has no funding needs until 2022, and it has a primary surplus.

Threats

- The Eurozone Sentix Investor Confidence Index fell by 22.3 points in March to a negative reading of 17.1. This is the sharpest fall within one month since the survey began, reflecting coronavirus-induced panic.

- President Erdogan announced that Turkey will activate its Russian-made S-400 missile-defense system in April. The U.S. has warned Turkey against the move in the past and the threat of sanctions may come back to the table. The last time the U.S. sanctioned the Turkish economy, pressuring the release of a detained American pastor, the lira crashed and sent the Turkish economy into recession.

- President Trump halted travel to the U.S. from 26 countries in Europe for the next 30 days as a measure to stop the spread of the coronavirus. Italy is now on a nationwide lockdown and many schools and universities are closed around Europe. More nationwide travel restrictions may follow. The Renaissance Capital macro team predicts a Western European lockdown by March 20 with the U.K. and U.S. joining by March 23 to March 25.

China Region

Strengths

- China, perhaps logically given its stage of progression along the virus “curve” at this point (so far as we can tell), made out the “best” in a particularly difficult week, as the Shanghai Composite fell “only” 4.85 percent on the week. Hong Kong, India and Malaysia also declined in single digit percentages.

- Financials constituted the best relative sector performance in Hong Kong’s Hang Seng Composite for the week, falling “only” 6.94 percent.

- South Korea’s unemployment rate handily beat expectations for the February period, dropping to 3.3 percent from 4.0 percent and far outpacing expectations for a 4.1 percent tick up. Coronavirus infection rates in South Korea also appear to be continuing to decline, which is a positive for the country.

Weaknesses

- It was, to put it rather mildly, a rough week for global equities. But Thailand’s SET Index fared worst in the region, declining 17.10 percent.

- Energy was the clear laggard in this troubled week for markets rocked by oil shocks and travel bans. Energy was the worst performer in Hong Kong’s HSCI, falling 16.21 percent.

- Perhaps unsurprisingly, China’s lending for the February period came in short of expectations, with New Yuan Loans and Aggregate Financing numbers both well short of consensus and far below prior readings.

Opportunites

- Taiwan’s exports clocked in at a scorching 24.9 percent, well ahead of estimates for a 3.0 percent gain and ahead of last month’s decline. Part of this is likely Lunar New Year effects, and clearly coronavirus effects and the decline of global demand may be yet to come, but don’t forget that last year’s trade war concerns are still wearing off around the region.

- The People’s Bank of China (PBOC) continued its stimulus measures by lowering the reserve ratio requirements for some banks in a $79 billion injection of funding to the world’s second-largest economy. China has held off from the sorts of large-scale shock-and-awe moves seen in other central banks on the week, but it remains likely—given the poor data of late and expectation of more poor data to come—that the country will provide other forms of stimulus, perhaps through other governmental and/or fiscal means.

- One can take what position one likes on the institution of short-selling bans, but in South Korea a ban on short-selling has been set in place through September, the first time a short-sell ban has been put in place since 2011. Daily limits to company share buybacks have also been eased. These actions, obviously, are aimed at supporting markets or at least arresting declines as the crisis is dealt with both in South Korea and globally.

Threats

- Coronavirus confirmed-case concerns continue. As the rest of the world braces for virus “impact,” China continues to report consistently declining cases and returns of workers to factories—an unabashed positive for China, of course—while South Korean infections have continued to slow, and places like Singapore continue effectively to manage the crisis. In a reversal from some of the original concerns that the rest of the world may not be able to access China’s manufacturing capacities—still, obviously, a threat in many ways—the reverse threat also proves ominous: if China’s factories are up and running, but demand is down on virus concerns, then what?

- Bloomberg News reported the largest ever cancellation of U.S. pork orders from China last week. While Phase One trade agreements should continue to lead Chinese purchases of U.S. goods up, clearly coronavirus concerns and logistical hiccups will weigh on things as the world muddles through “outbreak fallout.” The U.S. administration has indicated it can be patient with the ramp up in Chinese purchases, given the global and public health situation at present.

- In the midst of massive central banking actions this week and of various countries’ developing policies toward stimulus and economic responses to the virus’s present and looming effects, there remains significant room for policy errors or market disappointment at either scope or punctuality.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended March 13 was Veros, up 4,584.76 percent.

- According to blockchain analytics firm Glassnode and as reported by CoinTelegraph, the number of crypto wallets containing at least one Bitcoin continues to rises even as prices fall. The number of holders owning one coin hit an all-time high of 795,630 on March 11.

- Blockchain Game Partners, whose founder Eric Schiermeye is also the founder of Facebook game FarmVille, announced that it is developing a blockchain-based gaming platform called the Gala Network. CoinTelegraph reports that the platform seeks to afford players full ownership over blockchain-based in-game items represented as non-fungile tokens.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended March 13 was WhiteCoin, down 93.65 percent.

- Bitcoin is down almost 40 percent so far in March and fell below $6,000 an ounce on Thursday as the negative economic impacts of the global health crisis worsen. Bloomberg reports that thousands of traders are facing liquidations on BitMex, the world’s largest Bitcoin derivatives exchange. On Sunday, the platform had the most Bitcoin-related liquidations in three months, according to Skew, and more than $190 million has been liquidated on the exchange in the last 24 hours as of March 9.

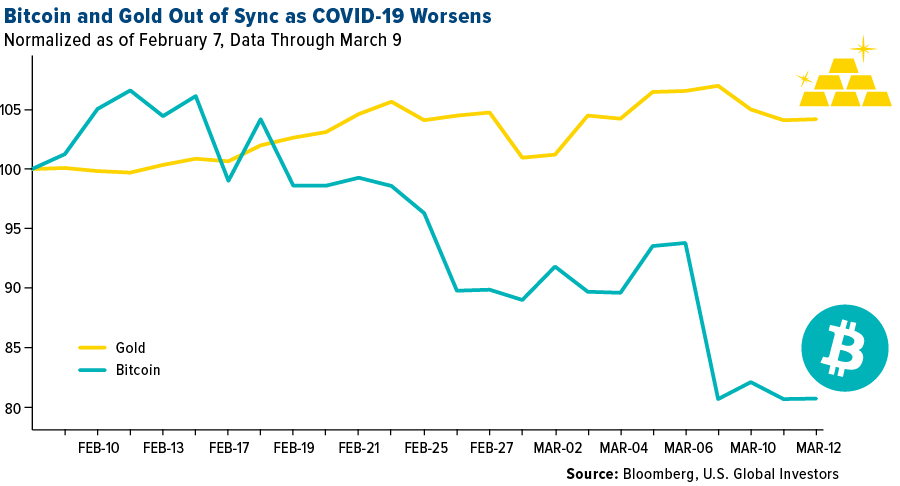

- Bitcoin and gold have moved out of sync as the COVID-19 outbreak has worsened. Over the past two years, the two assets had a correlation of 0.616, but over the past month is has reversed to minus 0.22, according to Bloomberg data. Tim Culpan writes that bitcoin was briefly seen as a winner during the equity selloff related to virus fears. However, after climbing 43 percent from the start of this year, bitcoin was down 12 percent on Monday alone.

Opportunities

- A group known as CoroHope is “biohacking” and crowdsourcing Bitcoin donations to fund its work to search for a coronavirus vaccine. CoinDesk reports that the group says it has a biologist on board with 10 years’ experience building vaccines for the FDA. A spokesperson told the news outlet via email that “cryptocurrency is uniquely able to help with this problem because, like us, it’s outside the traditional system.”

- Binance USD (BUSD), as its name suggests, is a stablecoin backed by the U.S. dollar. It has just surpassed $100 million in market capitalization and is chipping away at a market dominated by Tether’s TUSD, reports CoinDesk. The growing market cap of BUSD demonstrates investor appetite for stablecoins to trade cryptocurrencies by way of the dollar.

- Hive Blockchain Technologies announced a two-phase plan to expand its Ether mining operations at the company’s flagship facility in Sweden by more than 20 percent, reports CoinTelegraph. Interim chairman Frank Holmes says the company can now mine “at a significantly lower cost than our initial facility built two years ago.” The outlook has improved dramatically for the first publicly-traded blockchain company after management changes and the assumption of 100 percent control of its Swedish operations.

Threats

- The U.K. Financial Conduct Authority (FCA) warned the public to watch out for coronavirus-related cryptocurrency scams, reports CoinDesk. The FCA said in a March 11 warning that “these scams take many forms and could be about insurance policies, pensions transfers or high-return investment opportunities, including investments in cryptoassets.”

- CoinDesk reports that a massive decline in the price of ether is testing the feasibility of Ethereum’s entire system of lending and borrowing. MakerDAO is the largest and most important application in Ethereum’s DeFi ecosystem and it faces an emergency shutdown with $4 million of its dollar-pegged dai stablecoin not backed by an underlying crypto asset.

- According to a press release from the U.S. Attorney’s Office for the District of Columbia, a Dutch national has been indicted for spearheading a rape and child pornography website that has made over $1.6 million worth of Bitcoin selling videos since 2012. CoinDesk writes that customers allegedly sent cryptocurrencies as payment for videos or could upload their own. Over 2,000 videos were sold and the man had ties to 303 virtual currency accounts.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| 10-Yr Treasury Bond | 0.98 | +0.22 | +28.27% |

| Oil Futures | 33.19 | -8.09 | -19.60% |

| Hang Seng Composite Index | 3,323.96 | -313.30 | -8.61% |

| S&P Basic Materials | 290.78 | -44.24 | -13.21% |

| Korean KOSPI Index | 1,771.44 | -268.78 | -13.17% |

| S&P Energy | 241.29 | -77.35 | -24.28% |

| Nasdaq | 7,874.88 | -700.74 | -8.17% |

| DJIA | 23,185.62 | -2,679.16 | -10.36% |

| Russell 2000 | 1,209.07 | -240.15 | -16.57% |

| S&P 500 | 2,710.95 | -261.42 | -8.80% |

| Gold Futures | 1,520.90 | -151.50 | -9.06% |

| XAU | 70.26 | -32.75 | -31.79% |

| S&P/TSX VENTURE COMP IDX | 391.21 | -115.33 | -22.77% |

| S&P/TSX Global Gold Index | 201.37 | -77.46 | -27.78% |

| Natural Gas Futures | 1.91 | +0.20 | +11.53% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Korean KOSPI Index | 1,771.44 | -466.94 | -20.86% |

| 10-Yr Treasury Bond | 0.98 | -0.65 | -40.02% |

| Gold Futures | 1,520.90 | -50.70 | -3.23% |

| S&P Basic Materials | 290.78 | -90.48 | -23.73% |

| S&P 500 | 2,710.95 | -668.50 | -19.78% |

| DJIA | 23,185.62 | -6,365.80 | -21.54% |

| Nasdaq | 7,874.88 | -1,851.09 | -19.03% |

| Oil Futures | 33.19 | -17.98 | -35.14% |

| Hang Seng Composite Index | 3,323.96 | -487.82 | -12.80% |

| S&P/TSX Global Gold Index | 201.37 | -56.57 | -21.93% |

| XAU | 70.26 | -31.86 | -31.20% |

| Russell 2000 | 1,209.07 | -480.31 | -28.43% |

| S&P Energy | 241.29 | -173.74 | -41.86% |

| S&P/TSX VENTURE COMP IDX | 391.21 | -180.52 | -31.57% |

| Natural Gas Futures | 1.91 | +0.06 | +3.31% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| XAU | 70.26 | -29.17 | -29.34% |

| S&P/TSX Global Gold Index | 201.37 | -48.06 | -19.27% |

| Gold Futures | 1,520.90 | +43.00 | +2.91% |

| DJIA | 23,185.62 | -4,946.43 | -17.58% |

| S&P 500 | 2,710.95 | -457.62 | -14.44% |

| Nasdaq | 7,874.88 | -842.44 | -9.66% |

| Korean KOSPI Index | 1,771.44 | -365.91 | -17.12% |

| Natural Gas Futures | 1.91 | -0.42 | -18.17% |

| S&P Basic Materials | 290.78 | -89.88 | -23.61% |

| Russell 2000 | 1,209.07 | -435.74 | -26.49% |

| Oil Futures | 33.19 | -25.99 | -43.92% |

| Hang Seng Composite Index | 3,323.96 | -344.47 | -9.39% |

| S&P/TSX VENTURE COMP IDX | 391.21 | -145.31 | -27.08% |

| S&P Energy | 241.29 | -204.11 | -45.83% |

| 10-Yr Treasury Bond | 0.98 | -0.91 | -48.23% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (12/31/2019):

BHP Group Ltd.

Anglo American PLC

Gazprom PJSC

LUKOIL PJSC

Rosneft Oil Co PJSC

Occidental Petroleum Corp

CCC SA

SPDR Gold Shares

Cabot Oil & Gas Corp

Oracle Corp

adidas AG

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

An overnight indexed swap (OIS) is an interest rate swap where the periodic floating payment is generally based on a return calculated from a daily compound interest investment. The Mortgage Bankers Association (MBA) Refinance Index is a weekly measurement put together by the Mortgage Bankers Association, a nationally real estate finance industry association. The index helps to predict mortgage activity and loan prepayments based on the number of mortgage refinance applications submitted. Frank Holmes has been appointed non-executive chairman of the Board of Directors of HIVE Blockchain Technologies. Both Mr. Holmes and U.S. Global Investors own shares of HIVE. Effective 8/31/2018, Frank Holmes serves as the interim executive chairman of HIVE. Option-adjusted spread (OAS) is the yield spread which has to be added to a benchmark yield curve to discount a security’s payments to match its market price, using a dynamic pricing model that accounts for embedded options. The Bloomberg Barclays US Corporate High Yield Bond Index measures the USD-denominated, high yield, fixed-rate corporate bond market. Securities are classified as high yield if the middle rating of Moody’s, Fitch and S&P is Ba1/BB+/BB+ or below. Bonds from issuers with an emerging markets country of risk, based on Barclays EM country definition, are excluded. The SET Index is a Thai composite stock market index which is calculated from the prices of all common stocks (including unit trusts of property funds) on the main board of the Stock Exchange of Thailand (SET), except for stocks that have been suspended for more than one year. The STOXX Europe 600 Index is derived from the STOXX Europe Total Market Index (TMI) and is a subset of the STOXX Global 1800 Index. With a fixed number of 600 components, the STOXX Europe 600 Index represents large, mid and small capitalization companies across 18 countries of the European region: Austria, Belgium, Czech Republic, Denmark, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, the Netherlands, Norway, Portugal, Spain, Sweden, Switzerland and the United Kingdom. The Sentix Investor Confidence Index rates the relative six-month economic outlook for the euro zone. The data is compiled from a survey of about 2,800 investors and analysts. A reading above zero indicates optimism; below indicates pessimism. The small business optimism index is compiled from a survey that is conducted each month by the National Federation of Independent Business (NFIB) of its members. MVIS Global Junior Gold Miners Index is a pure-play, global index, tracking the performance of the most liquid junior companies in the global gold and silver mining industry that generate or intend to generate at least 50% of their revenues from this sector.