The Optimist’s Guide to Airlines, Crypto Mining and Gold

Date Posted: October 11, 2019

Read time: 56 min

If that's the case--and I happen to believe that it is--then I'm extremely bullish about the future, especially with respect to U.S.-China relations.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

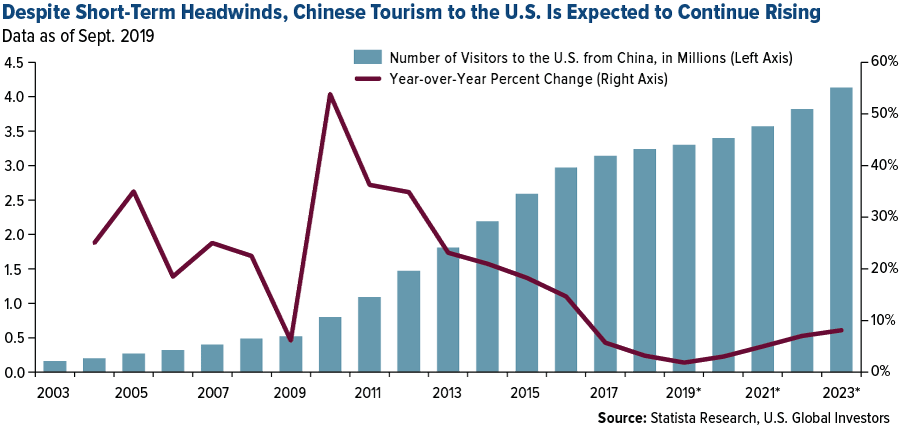

“Travel,” Mahatma Gandhi once said, “is the language of peace.”

If that’s the case—and I happen to believe that it is—then I’m extremely bullish about the future, especially with respect to U.S.-China relations. This week I was in Lower Manhattan, and the number of Chinese tourists I observed visiting the New York Stock Exchange (NYSE) and Federal Hall National Memorial—the epicenter of American capitalism and birthplace of the U.S. government—was encouraging. Everyone wanted their picture taken with the statue of George Washington, the father of the country with which their own government has been locked in a trade war for more than 18 months now.

The trade war’s days may be numbered, however. It’s being reported that both sides of the skirmish reached a partial agreement today, laying the groundwork for Presidents Donald Trump and Xi Jinping to sign a trade deal later this year.

Tourism has traditionally helped peace and understanding spread across borders, and I’m hopeful that it will do the same today. It’s also good for commerce, especially for airlines and the travel industry in general, as I told CNBC Asia on Thursday.

It’s Airline Earnings Season. Are You Participating?

Delta Air Lines, in particular, had a phenomenal third quarter as we head into the fourth, and historically most profitable, quarter. The carrier reported the best sales in company history as well as impressive earnings per share of $2.32, a 29 percent increase over the same period last year. CNBC reports that Delta is hiring as many as 12,000 new employees—including pilots, flight attendants and ground staff—through 2020 to meet surging demand.

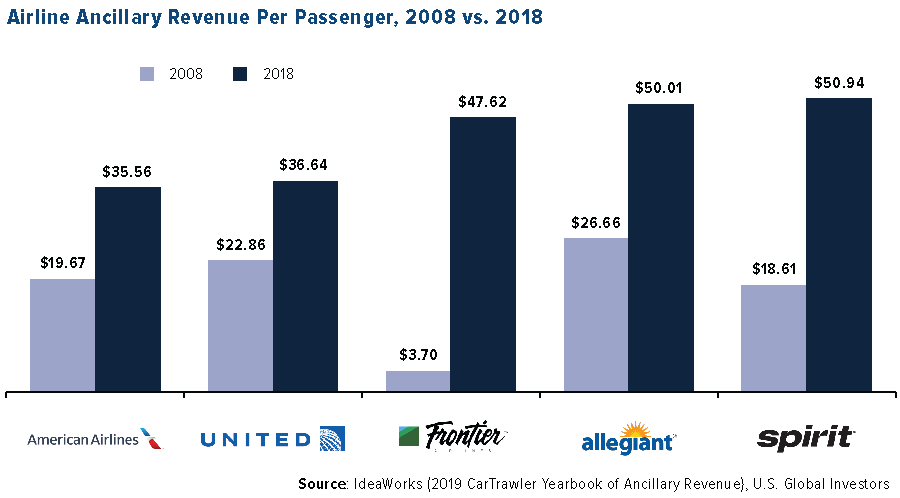

Supporting this growth are rising ancillary fees. Those are the non-ticket fees and upgrades you may end up having to pay when you fly, for everything from meals to preferred seating to credit cards. Delta recently inked a new deal with American Express, which is forecast to generate a mind-boggling $7 billion in revenue for the carrier by 2023, up from $3 billion today.

But Delta’s not the only one that’s joined the party. In the chart below, you can see a comparison of the amount of ancillary fees select U.S. airlines collected in 2018, on a per-passenger basis, with what they collected a decade earlier. Low-cost carrier Frontier saw an unbelievable 1,187 percent jump in such fees, while Spirit topped the list with an average $50.94 per passenger.

If you’re not participating, now might be a good entry point. The busy Thanksgiving and Christmas travel seasons are fast approaching, and according to recent analysis by the Wall Street Journal, the fourth quarter has typically seen the highest returns, with shares rising 8 percent on average every period going back to 1990.

HIVE Blockchain: $5.6 Million in Net Income

Another company that reported a spectacular quarter was HIVE Blockchain Technologies, which is back to generating positive net income and cash flow. In case you’re unaware, I’ve been serving as HIVE’s interim executive officer. After having to defend ourselves against a proxy battle in the spring, we’re now benefiting from improved transparency and financial controls. What’s more, we expect continued improvements throughout the fiscal year.

HIVE reported $5.6 million in net income in the first quarter of fiscal year 2020, having mined some 1,331 newly minted bitcoin during the period, as well as 35,000 Ethereum Classic and 3,200 newly minted Ethereum. You can read the full press release here.

Since HIVE’s debut a little over two years ago, investors have used it as a proxy to trade cryptocurrencies. That’s precisely why we took it public. I wasn’t able to open a bitcoin ETF for regulatory reasons—indeed, this is unlikely to change any time soon, as the SEC just rejected the latest attempt at creating such an ETF—so the next best thing was to create a world-class crypto miner and bring it to market.

I’m proud of how far HIVE has come these past two years, and even prouder that we managed to make money in what could have been a disastrous quarter. I’m very excited to see what’s in store.

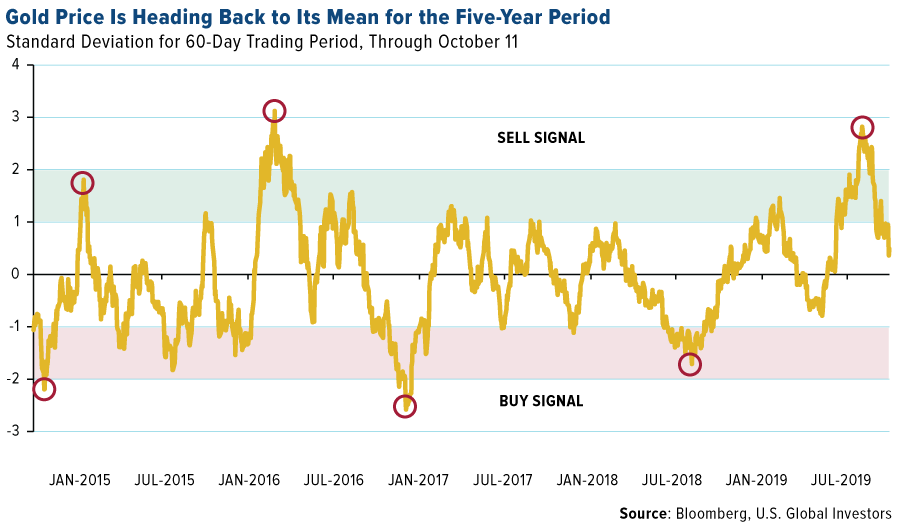

Time to Buy the Gold Dip?

The same goes with gold, which is headed back to its mean after hitting nearly three standard deviations in August. As CLSA analysts said recently, these price dips look like attractive buying opportunities “in anticipating of a resumption of the initial base breakout.”

This week our office was visited by the legendary economist Nancy Lazar, co-founder of Cornerstone Macro, who commented that the growing mountain of global debt, not to mention the proliferation of low to negative-yielding debt, makes the yellow metal very attractive right now.

I agree. During my interview with Kitco News’ Daniela Cambone, I reiterated my call for $10,000 gold. Some critics believe only a major event, such as a war or famine, would be enough to push the metal up that high, but really all it takes is monetary and fiscal mismanagement. That’s exactly what we’re seeing right now in Europe, where growth is slowing because of business-killing regulations. But instead of getting rid of these rules, interest rates have been allowed to dip below zero. In Denmark, banks are actually paying borrowers to take out a mortgage, which is contributing to what Nancy sees as a European housing bubble.

Conditions aren’t much better in the U.S.—or at least they weren’t, until President Trump began rolling back unnecessary regulations.

According to Steve Forbes, there are 773,000 words in the Bible, which sounds like a lot until you learn that there are around 10 million words in the federal income tax code. Similarly, there are more than 185,000 pages in the Federal Register of rules and regulations. That’s up 17 percent from 158,000 pages in 2008. But in 2018, the number of pages actually fell almost 1,000 pages, or 0.5 percent, meaning Trump is keeping his word.

Register now for our upcoming webcast!

Mark your calendars! Pierre Lassonde, co-founder of Franco-Nevada, agreed to participate on our upcoming webcast scheduled for October 31. We’ll be discussing opportunities in gold mining, as well as our outlook for the gold price. (If you recall, Pierre says it could hit $25,000 by 2049!) It’s sure to be an interesting conversation—I look forward to you joining us!

To register, send us an email at info@usfunds.com.

Gold Market

This week spot gold closed at $1,489.10, down $15.65 per ounce, or 1.04 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 2.54 percent. The S&P/TSX Venture Index came in off 3.22 percent. The U.S. Trade-Weighted Dollar fell 0.46 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Oct-8 | PPI Final Demand YoY | 1.8% | 1.4% | 1.8% |

| Oct-10 | CPI YoY | 1.8% | 1.7% | 1.7% |

| Oct-10 | Initial Jobless Claims | 220k | 210k | 220k |

| Oct-11 | Germany CPI YoY | 1.2% | 1.2% | 1.2% |

| Oct-15 | Germany ZEW Survey Current Situation | -23.0 | — | -19.9 |

| Oct-15 | Germany ZEW Survey Expectations | -26.8 | — | -22.5 |

| Oct-16 | Eurozone CPI Core YoY | 1.0% | — | 1.0% |

| Oct-17 | Housing Starts | 1320k | — | 1364k |

| Oct-17 | Initial Jobless Claims | 215k | — | 210k |

| Oct-17 | China Retail Sales | 7.8% | — | 7.5% |

Strengths

- The best performing metal this week was palladium, up 1.98 percent. Even after a weekly loss, gold traders and analysts stayed bullish on their outlook for prices in the weekly Bloomberg survey. Stocks continue to swing and currencies fluctuate ahead of continued U.S.-China trade talks. Just like last week, palladium hit a fresh all-time high this week of $1,707.51 an ounce, according to Bloomberg data. September marked the 10th straight month of gold buying for the People’s Bank of China, adding 5.9 tons and bringing total holdings to 62.64 million ounces. China has added over 100 tons to its reserves in the last 10 months, demonstrating that it sees value in the metal.

- President Trump announced on Friday that the U.S. is deploying around 3,000 troops to the Middle East to enhance the defense of Saudi Arabia from Iran. The announcement came just after news broke that an Iranian tanker was hit by two missiles near the Saudi Arabia coast. The deployment of more troops sends a conflicting message as earlier in the week Trump announced pulling back U.S. forces in northern Syria in order to bring troops home. Increased geopolitical tension has historically been good for gold as it can raise its appeal as a perceived safe haven asset.

- In a sign of good shareholder activism and a push for better corporate governance, Marlin Sams Fund, a long-term Torex Gold Resources shareholder, sent a letter to the company’s board. Marlin wrote that it is concerned with the interlocking relationship between Torex and TMAC Resources. Torex is reportedly considering an acquisition of TMAC. However, three of the directors of Torex also serve on the TMAC board. The letter says Marlin “calls into question the ability of the current Board to evaluate any important strategic matter.”

Weaknesses

- The worst performing metal this week was gold, down 1.01 percent. Gold sales in India, the world’s second largest consumer of the metal, continue to weaken. Around the Dhanteras holiday, gold buying usually increases for jewelry. However, weak demand due to higher prices might decrease sales by 50 percent this year, according to the national secretary of the India Bullion and Jewellers Association. Gold imports fell 68.18 percent in September compared to a year earlier. Jewelers are struggling to find buyers because of the higher prices and companies are giving big discounts. On the other hand, imports of silver, the poor man’s gold, jumped 72 percent in India from a year earlier to 543.21 tons in August, reports Bloomberg. Increased silver buying could make up for the decreases in gold.

- Ecuadorian President Linin Moreno accused his opponents of attempting a coup as the government moved outside of the capital city Quito. Violence and protesting erupted last week when Moreno announced an ending of long-standing fuel subsidies. Instability in the country could be negative for miners by disrupting operations and higher fuel prices could hurt margins. Bloomberg reports that indigenous communities have blocked off some main roads and that demonstrators caused the shutdown of production at an oilfield.

- Bloomberg reports that the sale of Iamgold Corp. has stalled after the miner failed to reach an agreement with several Chinese suitors. Resolute Mining’s Syama Gold mine is facing a production stall after a crack in the roaster, a key component in sulfide processing, was found and is being evaluated.

Opportunities

- UBS continues to support gold and forecasts prices to reach $1,650 over the next 12 months. Dominic Schnider, head of commodities and APAC macro, rates and foreign exchange at UBS, told Bloomberg TV in an interview that “we expect the Fed to cut several times, and so real rates are in negative territory: why would you not own gold?” Schnider added that gold can help balance a portfolio.

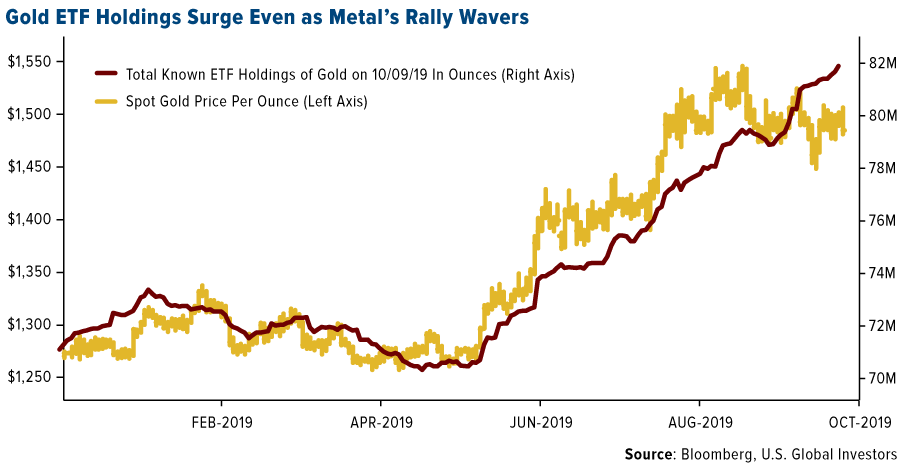

- Even as the gold price appears to have stalled, money is still flowing into ETFs backed by the metal. Inflows have increased for 18 sessions in a row, the longest run since 2009. Citigroup says that inflows are “likely to persist” and sticks with its forecast for a rally to $1,700 an ounce over six to 12 months, writes Bloomberg.

- Impala Platinum Holdings agreed to acquire 100 percent of the outstanding shares in North American Palladium Ltd. for $758 million in cash, reports Bloomberg. The deal highlights the attractiveness of palladium, which is seeing higher prices due to growing demand for its use in catalytic converters. For valuing the assets of North American Palladium, a base price of $1,100 per ounce of palladium was used. With spot palladium prices around $1,700 an ounce, there is certainly room for an interloper to make a higher bid.

Threats

- The Federal Reserve announced on Friday that it will begin buying $60 billion of Treasury bills per month to improve its control over the benchmark interest rate it uses to guide monetary policy, reports Bloomberg. Turmoil rocked money markets in September when the rate on overnight general collateral repo jumped to 10 percent, which is four times the usual level. Concerns are growing on whether or not the Fed can serve as a conduit for liquidity in times of stress and growing debt levels.

- Federal Reserve Bank of Dallas President Robert Kaplan said in a Bloomberg TV interview this week that rate cuts “should be limited, restrained and modest” and that right now we are “in a fragile period.” The comments could dampen investor enthusiasm that has sent inflows into gold-backed ETFs soaring. UBS also sent a warning this week that U.S. households are struggling financially. According to a quarterly UBS survey, 44 percent of consumers reported that incomes do not cover expenses, or barely cover them. Additionally, just 17 percent of households reported in the survey that their financial condition had improved in the last six months, which is 3 percentage points down from a year earlier.

- Although mining stocks are up in the region, output of platinum-group metals in South Africa, the world’s largest producer, shrank the most in 18 months in August, reports Bloomberg. Production contracted 12.5 percent from a year earlier, according to Statistics South Africa. As supply tightens, holdings in palladium ETFs have expanded almost every day in the past two weeks.

October 11, 2019Bad News Is Good News For Gold |

October 8, 2019Ralph Aldis’ Top Precious Metal Stock Picks |

September 30, 2019U.S. Global Investors Continues GROW Dividends |

|||

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 0.91 percent. The S&P 500 Stock Index rose 0.62 percent, while the Nasdaq Composite climbed 0.93 percent. The Russell 2000 small capitalization index gained 0.75 percent this week.

- The Hang Seng Composite gained 1.99 percent this week; while Taiwan was down 0.04 percent and the KOSPI rose 1.18 percent.

- The 10-year Treasury bond yield rose 20 basis points to 1.736 percent.

Domestic Equity Market

Strengths

- Materials was the best performing sector of the week, increasing by 1.83 percent versus an overall increase of 1 percent for the S&P 500.

- Fastenal Co was the best performing stock for the week, increasing 13.47 percent.

- "Joker" had the biggest October opening weekend ever, taking in $93.5 million. The record-breaking weekend intake means Warner Bros has already made back the movie’s production budget, which was north of $60 million.

Weaknesses

- Utilities was the worst performing sector for the week, decreasing by 1.42 percent versus an overall increase of 1 percent for the S&P 500.

- Hormel Foods Corp was the worst performing stock for the week, falling 5.72 percent.

- Nektar Therapeutics bull Goldman Sachs is calling it quits after recommending shares since December despite the stock’s slide and subsequent removal from the S&P 500 Index. Goldman’s Paul Choi downgraded shares two notches, to a sell from buy, citing a lack of near-term catalysts amid drug quality issues and a narrower investor focus for its cancer drug among recent pressures on the stock. Choi cut his price target to $16 from $54. Nektar fell as much as 10 percent Tuesday, its biggest drop since August 12. The shares have lost more than half their value since Choi initiated coverage in December, compared to a 10 percent rise for the S&P 500 Index.

Opportunities

- A smaller, less expensive iPhone could drive sales in early 2020, according to a prominent Apple analyst. According to CNBC, TF Securities analyst Ming-Chi Kuo thinks Apple’s iPhone shipments could go up ’10 percent year-over-year.’

- Callaway Golf’s shares rose on a report of a potential TopGolf IPO. According to Reuters, TopGolf International is in talks with banks about hiring underwriters for an IPO. Callaway’s 14 percent stake in TopGolf could be worth over $360 million.

- Startup investors are discussing the appeal of direct listings after disappointing returns from some of the industry’s most anticipated tech IPOs, and blamed big banks for overhyping private companies on public markets. Investors at TechCrunch Disrupt discussed the merits of direct listings to avoid flops like WeWork and Uber.

Threats

- Silicon Valley is losing its war against paying tax on big-tech revenues. The Organization for Economic Cooperation and Development (OECD) outlined a massive overhaul of tax rules which would hit tech giants with bigger tax bills.

- The U.S. blacklisted some of China’s most valuable artificial intelligence (AI) startups over human rights issues in a dramatic trade war escalation. Among the 28 blacklisted were eight major tech companies, including three AI startups valued at over $1 billion.

- Citi’s Keith Horowitz sees reduced earnings forecasts as bank stock valuations are “flashing red.” He expects bank management teams may add lower rates to their 2020 outlooks for net interest income, or NII, which will “come in substantially lower than consensus.” At Jefferies, analyst Ken Usdin also flagged slower earnings and “sentiment hurdles.” The 2020 presidential elections may return the “spotlight back to regulation and taxes,” he wrote.

The Economy and Bond Market

Strengths

- Federal Reserve Chairman Jerome Powell reiterated that the economy is well positioned despite some risks and that it’s the central bank’s task to keep it that way. While “the economy faces some risks, overall, it is — as I like to say — in a good place,’’ he said in the text of remarks to be delivered to a “Fed Listens’’ event in Kansas City on Wednesday. “Our job is to keep it there as long as possible.”

- American financial experts may be worried about trade wars, tariffs and talk of a recession, but ask a small-town banker and economic conditions are pretty good. Across the country, people are building and buying homes. Small businesses are borrowing money to expand. Most families are earning and spending money. Those are the findings from the Conference of State Bank Supervisors (CSBS), a group that represents the local regulators who oversee the 5,500 U.S. banks with less than $10 billion. This year the CSBS released a new measure of economic health – a new index based on the opinions of more than 500 community bankers. The first results, released in June, showed “an overall positive outlook.” Many of those questioned said they expect continued or improved business conditions and profit. The second reading had similar results.

- Sentiment among American consumers posted a surprise jump in October amid expectations for rising incomes and lower inflation, indicating households will continue to extend the longest-running U.S. expansion. The University of Michigan’s preliminary sentiment index advanced to a three-month high of 96 from September’s 93.2. The gauge of current conditions climbed to the highest level this year while the expectations index improved.

Weaknesses

- U.S. producer prices unexpectedly fell in September, leading to the smallest annual increase in nearly three years. The weak producer inflation readings reported by the Labor Department on Tuesday came against the backdrop of a slowing economy amid trade tensions and cooling growth overseas. The producer price index (PPI) for final demand dropped 0.3 percent last month, weighed down by decreases in the costs of goods and services. That was the largest decline since January and followed a 0.1 percent gain in August. In the 12 months through September, PPI increased 1.4 percent, the smallest gain since November 2016, after rising 1.8 percent in August. The Fed, which has a 2 percent annual inflation target, tracks the core personal consumption expenditures (PCE) price index for monetary policy. The core PCE price index rose 1.8 percent on a year-on-year basis in August and has undershot its target so far this year.

- Optimism among small business owners fell in September largely due to the impact of tariffs and uncertainty about the future state of the economy, according to a survey from the National Federation of Independent Business. The NFIB Small Business Optimism Index had a September reading of 101.8, down 1.3 points from 103.1 in August. About 30% of owners surveyed said they were negatively impacted by tariffs.

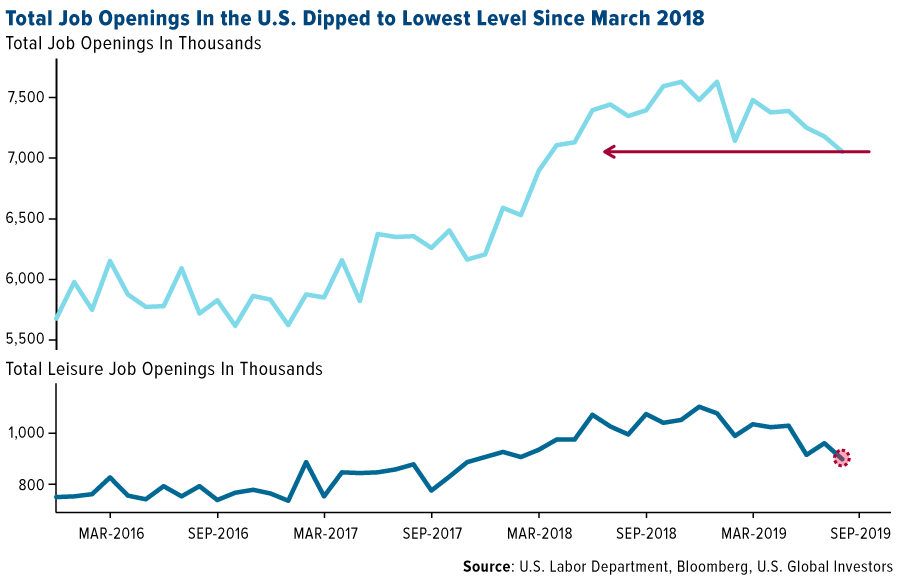

- U.S. job openings unexpectedly declined in August to the lowest level since March 2018, underscoring the slowdown in hiring across American employers even as the labor market remains generally tight. The number of positions waiting to be filled fell by 123,000 to 7.05 million, according to the Labor Department’s Job Openings and Labor Turnover Survey.

Opportunities

- French President Emmanuel Macron will meet German Chancellor Angela Merkel at the Elysee on October 13 to discuss European matters ahead of next week’s EU Summit. The two leaders will prepare for the Franco-German summit, in addition to the European Union summit next week, where Britain’s plans to leave the EU will be a big topic. The EU could delay Brexit until next summer to allow for a second referendum. Officials in Brussels reportedly believe it would provide enough time for the fallout from a general election to play out, or to legislate for a second referendum.

- Next Wednesday’s U.S. retail sales advance will be pivotal to determine if consumer strength continues to hold up amid global turmoil.

- The Leading Index reading out next Friday is forecast to nudge up to 0.1 percent, projecting continued growth in the economy.

Threats

- President Trump’s trade war means America is no longer the world’s most competitive country. Singapore has now taken the top spot, according to a 666-page report from the World Economic Forum, which cited trade and geopolitical tensions.

- Iran is planning to take legal action against the U.S. for alleged cyber-attacks and threats on its networks, according to Bloomberg. The plans were first reported by semi-official Iranian publication Tasnim News, after an interview with an Iranian general.

- A bipartisan group of senators have reportedly called for ‘sweeping action’ to prevent social media from being used to meddle in the upcoming presidential election. According to the Washington Post, a Senate Intelligence Committee report urges the White House and executive branch to warn U.S. citizens about the ways in which dangerous misinformation can spread.

Energy and Natural Resources Market

Strengths

- The best performing major commodity for the week was cotton, which gained 5.43 percent on risks of crop damage from early winter freezes overnight. After news that U.S.-China trade talks on Thursday went “very well,” commodities and metals rallied. Zinc prices jumped 4.2 percent. News also broke Thursday night that an Iranian oil tanker was hit by missiles near Saudi Arabia, which sent Brent crude above $60 a barrel.

- Nickel inventories in LME warehouses had their second biggest drop on record on Monday, then fell again on Tuesday to post the biggest ever drop. It didn’t stop there. Inventories fell by even more on Wednesday, dropping by 8,898 tons to 108,624 tons and surpassing the record set the day prior. Inventories continue to decline as companies are stocking up on the metal before a potential Indonesia ban on exports. Lower inventories should support higher prices and benefit miners of the metal.

- Bloomberg reports that ConocoPhillips is hiking its dividend 38 percent in an effort to attract investors back to oil. Conoco, the largest independent crude explorer, was down 14 percent for the year, which is one of the weakest performances in the S&P’s oil sector. The new dividends will mean more than $500 million in extra annual payouts to investors. The company also announced a reduction in stock buybacks, which have been unsuccessful in impressing investors.

Weaknesses

- The worst performing major commodity for the week was natural gas, which fell 5.40 percent on rising U.S. stockpiles delivered from shale gas. The number of iron bears continues to grow. Barclay’s forecasts iron ore at $75 a ton in 2020 and $60 a ton in 2021 due to ample supply and weaker demand from steelmakers. Morgan Stanley has a similar prediction of $70 a ton iron in 2020 driven by a fall in China’s steel production.

- According to the Association of American Railroads, the decline in carloads for U.S. railroads widened to 5.5 percent in the third quarter, the biggest drop in three years and the third straight quarter of declines. Bloomberg’s Thomas Black says that railroad are already in recession and that “it’s a dramatic turn from a year ago when rising shipments of autos, coal, lumber, chemicals and other commodities spurred U.S. rail carload to rise 3.6 percent in 2018.”

- Bloomberg reports that the quality of Russia’s crude oil exports is deteriorating. According to data from the state-owned pipeline company that transports most of Russia’s oil, Transneft, crude is nearing the maximum permissible sulfur level of 1.8 percent and is currently at 1.64 percent. Transneft says the deterioration of Russia’s resource base is the main cause of the issue.

Opportunities

- A new market is emerging in LNG: small ships that are one seventh the size of a typical tanker. Smaller ships allow companies to serve customers whose ports or budgets are too small to handle regular tankers. Bloomberg reports that this could spur production capacity growth of 58 percent over the next five years. LNG is a growing and attractive fuel source as it burns more cleanly than coal and is more easily accessible through a terminal versus a pipeline.

- Zijin Mining announced that it plans to boost its stake in Ivanhoe Mines to 13.9 percent from 9.8 percent. In a statement to the Shanghai stock exchange the company says it will buy 48.7 million shares for 1.03 billion yuan. Glencore Plc signed a five-year deal to sell cobalt to Chinese battery maker GEM Co., a sign that demand is returning after a plunge last year, reports Bloomberg. Petra Diamonds surged as much as 13 percent on Monday after announcing a special tender of the 20.08 carat blue diamond from its South African mine last month – a positive sign from the struggling diamond industry.

- Japanese chemist Akira Yoshino and two others were awarded the Noble Prize in Chemistry for their work on modern lithium-ion batteries. Yoshino says that battery recycling is key to securing supply for electric vehicle demand, reports Bloomberg. “The ideal style for the future is people don’t own a car and a self-driving vehicle is coming whenever anyone wants to use the service,” Yoshino added

Threats

- In an effort to prevent power lines from sparking massive blazes, PG&E, the California utility giant responsible for last years’ deadly Camp Fire, is cutting power to up to 2.7 million residents. Intentional blackouts could become a regular ordeal as California’s climate warms and dries, reports Bloomberg. The economic impact could reach $2.6 billion. Marc Chenard, senior branch forecaster with the U.S. Weather Prediction Center in College Park, Maryland, says that “there is a pretty significant fire risk across California.”

- South America produces around 70 percent of the global lithium supply, but doesn’t have the infrastructure necessary to put the metal to work in batteries. Several countries’ economies are highly dependent on revenue from mining the metal and are at risk of big price swings without a way to manufacture lithium into another product. Bloomberg’s Laura Millan Lombrana writes that so far “public and private initiatives in Argentina, Bolivia, Brazil and Chile have failed to deliver even a single lithium cell factory.” James Ellis, head of Latin America research at BloombergNEF adds that “the size of the opportunity is huge.”

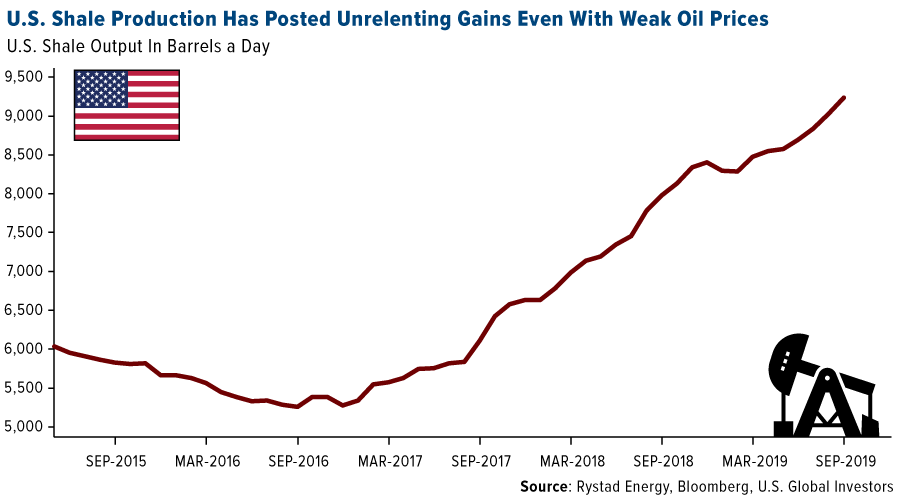

- U.S. shale production continues to boom even with weak oil prices and slowing global demand. Seaport Global Securities downgraded its rating on 13 oil and gas producers to neutral from buy saying that producers must slow production. BloombergNEF says that shale producers are “riding the edge of profitability” at current prices and could face a big slowdown if crude falls before $50 a barrel for a long period. An industry overproducing is natural gas in the Permian Basin. Producers are flaring off gas at record levels due to a lack of pipeline capacity to carry the gas away.

Emerging Europe

Strengths

- Greece was the best performing country this week, gaining 3.84 percent. The country’s new government is expecting economic growth at a faster pace next year of 2.8 percent versus 2 percent in 2019. The draft budget for 2020 includes a reduction of the corporate tax rate to 24 percent, down from 28 percent.

- The Polish zloty was the best performing currency this week, gaining 97 basis points against the U.S. dollar. The World Bank revised up GDP growth for Poland to 4.3 percent from 4 percent for this year citing strong consumer spending and a rebound in investment. Poland’s growth is one of the fastest in Europe and Central Asia.

- Materials was the best performing sector among eastern European markets this week. KGH, a Polish copper producer, was the best preforming equity, gaining almost 4 percent in the last five days.

Weaknesses

- Turkey was the worst performing country this week, losing 4.29 percent. Investors took profits after the U.S. administration pulled out its troops from Northern Syria and Turkish forces entered the region.

- The Turkish lira was the worst performing currency in the region this week, losing 3.29 percent. After the Turkish incursion into Northern Syria, the U.S. is drafting a bill to put sanctions on the country’s energy sector. The sanctions could cover any foreign person or entity who supplies goods, services, technology, information or other support that maintains or supports Turkey’s domestic petroleum and natural gas production for use by its armed forces.

- Industrials was the worst performing sector among eastern European markets this week. Aselsan Elektronik Sanayi, a Turkish military and civil telecommunications equipment producer, was the worst preforming equity, losing almost 6 percent in the past five days.

Opportunities

- Nancy Lazard from Cornerstone Macro visited our offices in San Antonio, Texas on Thursday said that she believes Eurozone growth is sluggish, but is no longer a drag on global growth. Moreover, she pointed out that growth in the Eurozone has potential to bounce once fiscal policy is implemented, in addition to monetary easing. France cut taxes, Greece cut taxes and if Germany follows suit, the Euro area as a good chance of recovering quickly, assuming there is no hard Brexit.

- Russian Finance Minister Anton Siluanov has signed an agreement with Turkey that allows both countries to pay each other in respective local currencies. The nations intend to organize national financial message transmission systems and possibly connect other countries to their systems in the future.

- Inflation in Russia slowed to 4 percent in September, down from 4.3 percent in August. Food inflation ticked slightly higher, but core inflation components were lower. JPMorgan expects the central bank to cut rates again this year with a 25 basis point cut in October and another cut of 25 basis points in December, followed by two cuts next year in the same amount. This would bring the policy rate to 6 percent by mid-2020.

Threats

- Poland will hold parliamentary elections this weekend. The Polish ruling party, PiS (conservative, right wing and Eurosceptic Law & Justice), still enjoys 44.3 percent voter support and has extended its lead over main rival, Civic Coalition (KO), to 21.6 percent. An overwhelming victory could give PiS two-thirds of parliament’s seats, enough to change the constitution. Such a change would likely be met with political unrest and lead to further criticism from EU leaders, who already threatened Poland with sanctions over breaking the rule-of-law.

- Romanian Prime Minister Viorica Dancila’s center-left government collapsed on Thursday after losing a no-confidence vote in parliament, raising the prospect of prolonged political uncertainty due to a fragmented opposition. The opposition now has ten days to nominate a new premier who will need the approval of centrist President Klaus Iohannis. Romania is also due to hold a presidential poll next month.

- The Turkish lira has been highly volatile and it could depreciate further against the U.S. dollar as geopolitical risk is increasing in the region. The U.S. and EU are preparing a fresh set of sanctions on Turkey for attacking Syria. France’s Minister of State Montchalin says Turkey’s NATO membership will be discussed next week.

China Region

Strengths

- The best performing index in the region was the Shanghai Composite, which jumped 2.36 percent since reopening following Golden Week holidays. Thailand, the Philippines and Hong Kong all gained between 1 and 2 percent on the week as well, as did India’s NIFTY and SENSEX indices.

- Energy was the best performing sector in the Hang Seng Composite for the week, rising 3.08 percent.

- Singapore’s retail sales did slightly better than expected, declining only 4.1 percent year-over-year and beating analysts’ consensus. Retail sales ex-autos declined only 1.0 percent year-over-year.

Weaknesses

- The worst performing index in the region was Malaysia’s FTSE Bursa Malaysia Kuala Lumpur Compsite, which declined by 5 basis points, failing to participate in what was a green week for the rest of the region.

- Information technology was the laggard HSCI sector this week, rising only 1.22 percent.

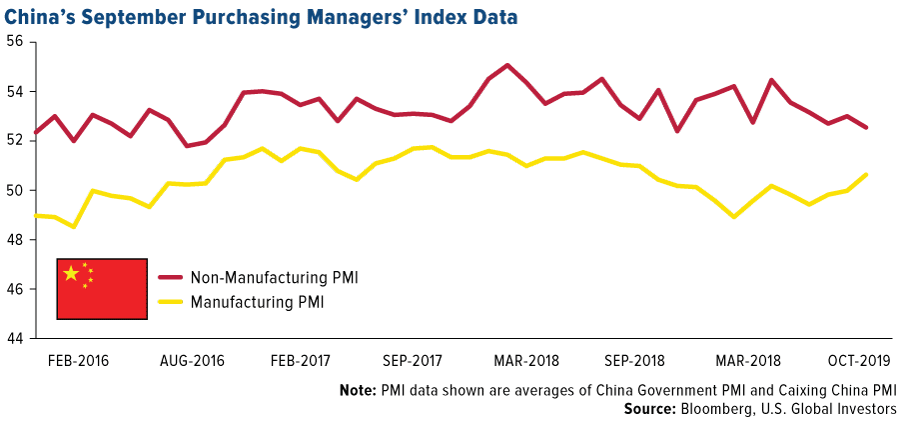

- The Caixin China services PMI came in a bit lighter than expected at only 51.3, short of consensus 52.0 and down from the prior 52.1 reading. While manufacturing PMIs did come in a bit better prior to the Golden Week holidays, non-manufacturing and the above Caixin services were both a little light.

Opportunities

- To Phase Two and Beyond! In what has of late developed into a regularly weekly comment, there remains a viable opportunity for concrete steps toward resolution in the U.S.-China trade war, and this week we saw this most clearly after the conclusion of the week’s trade talks in Washington when U.S. President Donald Trump announced that the U.S. and China had reached “Phase One” of a trade deal. The partial deal could be signed as soon as next month. As part of the deal, the Chinese would boost U.S. agricultural purchases, will agree to certain intellectual property measures and will also grant some concessions around the issues of financial services and currency. In return, Secretary Mnuchin announced that the U.S. will not hike tariffs as initially slated for October 15. The U.S. will also consider lifting the currency manipulation label it has slapped on China.

- While “IPO” seems to have been a bit of dirty three-letter word in the U.S. financial media recently, China’s new STAR board encouraging domestic tech and innovation listings continues to crank out new IPOs—one recent report noted that some eight additional companies are scheduled for listing hearings next week in Shanghai. Bloomberg points out that the retail portion of an average Star Market IPO was oversubscribed by more than 1,800 times.

- The U.S. dollar declined over the course of the week as it continued its retreat from 52-week highs on October 1. A weaker dollar may help ease pressure on emerging markets.

Threats

- In keeping with this section’s views, we once again reiterate that trade war escalation must remain a threat until it isn’t. The tone of the week certainly ended on an optimistic note. A trade truce has been reached before, and a truce is hardly a lasting peace.

- Unrest continues in Hong Kong, although markets there did shake off the latest issues on Friday amid some optimism on U.S.-China relations and with reports that protestors may attempt to ratchet down vandalism and violence.

- Related to Hong Kong’s own direct concerns at this point are increasing pressures on companies and organizations to take sides in one fashion or another with respect to the protests. An individual tweet from, say, a Houston Rockets GM can lead to a massive popular and corporate backlash against the NBA in China, force the NBA commissioner to take an official stance of nothing official but free speech in America, cause individual players to have to speak out to salvage fandom, prompt companies like Tencent to shut down streaming preseason games in China, solicit questions from reporters to other coaches on their own respective stances and eventually elicit direct responses from the President of the United States. That being said, as the U.S. Congress increasingly considers bills subjecting Hong Kong’s special trading status to more regular Congressional reaffirmations, perhaps the idea begins to hit home even further. Every individual may have their own spoken—or unspoken—opinion, or may not feel qualified yet to form one, at least publicly, but at the end of the day, when these issues begin snowballing (as the NBA snafu demonstrated, it sometimes happens quickly!), major economic and corporate stakes may end up on the line one way or the other.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended October 11 was TouchCon, up 337.63 percent.

- Bitcoin was down over the weekend as much as 4.9 percent, but erased the declines as the U.S. morning progressed at the start of the week, reports Bloomberg. Rival digital coins, which had declined earlier as well, tracked bitcoin’s Monday recovery, with XRP being the biggest gainer on the day, advancing nearly 9 percent.

- In what the firm is calling an important evolution in the safe-haven asset trading space, crypto liquidity and OTC provider B2C2 has launched a gold derivatives product that synthetically trades against bitcoin. B2C2 told Coindesk that the benefit of the setup is that “it’s simpler than the cash underlie for a variety of operational reasons, and typically represents the majority of activity in the product/asset.”

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended October 11 was Kalkulus, down 48.57 percent. Despite the Federal Reserve’s plan to restart its inflation-boosting balance sheet expansion program, bitcoin is lacking a clear directional bias mid-week, writes CoinDesk. Although the news could be seen as a long-term positive for the digital asset, it hasn’t yet buoyed the price, which continues to hold around $8,200.

- According to a document on the Securities and Exchange Commission website, the final application for an exchange-traded fund tied to bitcoin has been denied by the SEC. Bitwise’s Bitcoin ETF Trust would have tracked the spot price for bitcoin had it been approved, writes TheBlockCrypto.com.

- The Bank of Russia has been investigating the possibility of a central bank digital currency (CBDC) and the need to launch the new technology, writes CoinDesk. However, chairman of the bank Elvira Nabiullina, says she sees no strong reason to launch one that would override the potential risks. “Not only for technological reasons, but also because it is [difficult] to really estimate what advantages will the national digital currency give, for example, in comparison with existing electronic non-cash payments,” Nabiullina explained. “There are many risks, and the advantages may not be obvious enough.”

Opportunities

- As reported by CoinDesk, Binance is now accepting fiat through both Alipay and WeChat, which opens the exchange up to peer-to-peer crypto transactions from China. According to Statisa, WeChat currently has over 1.1 billion active users while Alipay has over 900 million users as well, per the China Daily.

- Hong Kong’s Securities and Futures Commission (SFC) has issued regulations for fund managers investing in “virtual assets,” writes CoinDesk.com. On October 4, the market watchdog formalized a framework put out last November aimed to regulate funds that allocate more than 10 percent of their portfolio in virtual assets.

- Commodity Futures Trading Commission (CFTC) Chair Heath Tarbert, speaking at a Yahoo! Finance All Markets Summit this week, said that he believes ether, the world’s second-largest cryptocurrency by market capitalization, is a commodity. “We’ve been very clear on bitcoin: bitcoin is a commodity. We haven’t said anything about ether – until now,” Tarbert said. “It is my view as chairman of the CFTC that ether is a commodity.”

Threats

- A class-action complaint filed in the U.S. District Court for the Southern District of New York on Sunday, accuses the companies behind Tether of “propping and popping the largest bubble in history,” leading to disappearance of $265 billion in cryptocurrency wealth, reports Bloomberg. According to the complaint on behalf of a handful of investors, the stablecoin allegedly has been used to manipulate the value of bitcoin.

- The digital payment arm of Chinese e-commerce giant Alibaba, known as Alipay, has declared that it will be banning any transactions related to bitcoin and other cryptocurrencyes, reports CoinTelegraph.

- Some investors might think of bitcoin as “digital gold” and believe that it can act as somewhat of a safe haven compared to other assets. However, Galen Moore from the CoinDesk research teams writes that it has not yet secured that status. In fact, bitcoin’s price has “never shown a correlation with gold, positive or negative, for any length of time, since early 2015.”

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| 10-Yr Treasury Bond | 1.74 | +0.21 | +13.46% |

| Oil Futures | 54.70 | +1.89 | +3.58% |

| Hang Seng Composite Index | 3,557.49 | +69.38 | +1.99% |

| S&P Basic Materials | 359.46 | +6.54 | +1.85% |

| Korean KOSPI Index | 2,044.61 | +23.92 | +1.18% |

| S&P Energy | 428.04 | +4.28 | +1.01% |

| Nasdaq | 8,057.04 | +74.56 | +0.93% |

| DJIA | 26,816.59 | +242.87 | +0.91% |

| Russell 2000 | 1,511.90 | +11.20 | +0.75% |

| S&P 500 | 2,970.27 | +18.26 | +0.62% |

| Gold Futures | 1,492.20 | -20.70 | -1.37% |

| XAU | 88.92 | -2.19 | -2.40% |

| S&P/TSX VENTURE COMP IDX | 540.76 | -18.00 | -3.22% |

| S&P/TSX Global Gold Index | 235.96 | -9.84 | -4.00% |

| Natural Gas Futures | 2.23 | -0.13 | -5.31% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Korean KOSPI Index | 2,044.61 | -4.59 | -0.22% |

| 10-Yr Treasury Bond | 1.74 | -0.00 | -0.23% |

| Gold Futures | 1,492.20 | -11.00 | -0.73% |

| S&P Basic Materials | 359.46 | -3.08 | -0.85% |

| S&P 500 | 2,970.27 | -30.66 | -1.02% |

| DJIA | 26,816.59 | -320.45 | -1.18% |

| Nasdaq | 8,057.04 | -112.64 | -1.38% |

| Oil Futures | 54.70 | -1.05 | -1.88% |

| Hang Seng Composite Index | 3,557.49 | -73.78 | -2.03% |

| S&P/TSX Global Gold Index | 235.96 | -4.96 | -2.06% |

| XAU | 88.92 | -3.43 | -3.71% |

| Russell 2000 | 1,511.90 | -63.81 | -4.05% |

| S&P Energy | 428.04 | -19.04 | -4.26% |

| S&P/TSX VENTURE COMP IDX | 540.76 | -45.40 | -7.75% |

| Natural Gas Futures | 2.23 | -0.33 | -12.74% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| XAU | 88.92 | +4.87 | +5.79% |

| S&P/TSX Global Gold Index | 235.96 | +11.59 | +5.17% |

| Gold Futures | 1,492.20 | +59.30 | +4.14% |

| DJIA | 26,816.59 | -149.41 | -0.55% |

| S&P 500 | 2,970.27 | -25.55 | -0.85% |

| Nasdaq | 8,057.04 | -113.19 | -1.39% |

| Korean KOSPI Index | 2,044.61 | -35.97 | -1.73% |

| Natural Gas Futures | 2.23 | -0.06 | -2.75% |

| S&P Basic Materials | 359.46 | -11.56 | -3.12% |

| Russell 2000 | 1,511.90 | -60.22 | -3.83% |

| Oil Futures | 54.70 | -2.64 | -4.60% |

| Hang Seng Composite Index | 3,557.49 | -226.84 | -5.99% |

| S&P/TSX VENTURE COMP IDX | 540.76 | -39.64 | -6.83% |

| S&P Energy | 428.04 | -38.29 | -8.21% |

| 10-Yr Treasury Bond | 1.74 | -0.40 | -18.84% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (09/30/2019):

ConocoPhillips

Ivanhoe Mines Ltd

KGH

Aselsan Elektronik Sanayi

Torex Gold Resources Inc

TMAC Resources Inc

Iamgold Corp

Resolute Mining Ltd

Impala Platinum Holdings Ltd

North American Palladium Ltd

Delta Air Lines Inc

American Airlines Group Inc

United Airlines Holdings Inc

Allegiant Travel Co

Spirit Airlines Inc

Franco-Nevada Corp

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry.

The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks.

The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months.

The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange.

The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver.

The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar.

The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500.

The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500.

The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period.

The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500.

The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500.

The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500.

The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500.

The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500.

The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500.

The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns.

The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The University of Michigan Confidence Index is a survey of consumer confidence conducted by the University of Michigan. The report, released on the tenth of each month, gives a snapshot of whether or not consumers are willing to spend money.

The Conference Board Leading Economic Index is an American economic leading indicator intended to forecast future economic activity. It is calculated by The Conference Board, a non-governmental organization, which determines the value of the index from the values of ten key variables.

Producer price index measures the average changes in prices received by domestic producers for their output. It is produced by the Bureau of Labor Statistics and measures price movements from the seller’s point of view.

The Small Business Optimism Index is compiled from a survey that is conducted each month by the National Federation of Independent Business (NFIB) of its members.

The “core” PCE price index is defined as personal consumption expenditures (PCE) prices excluding food and energy prices.

Standard deviation is a measure of the dispersion of a set of data from its mean. The more spread apart the data, the higher the deviation. Standard deviation is also known as historical volatility.

Frank Holmes has been appointed non-executive chairman of the Board of Directors of HIVE Blockchain Technologies. Both Mr. Holmes and U.S. Global Investors own shares of HIVE. Effective 8/31/2018, Frank Holmes serves as the interim executive chairman of HIVE.

The Shanghai Stock Exchange Composite Index is a capitalization-weighted index. The index tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange.

The FTSE Bursa Malaysia KLCI, also known as the FBM KLCI, is a capitalization-weighted stock market index, composed of the 30 largest companies on the Bursa Malaysia by market capitalization that meet the eligibility requirements of the FTSE Bursa Malaysia Index Ground Rules.

The Caixin China General Manufacturing Purchasing Managers’ Index (PMI) is closely watched by investors as one of the first available indicators every month of the strength of the Chinese economy.

The NIFTY 50 index National Stock Exchange of India’s benchmark broad based stock market index for the Indian equity market.

Sensex, otherwise known as the S&P BSE Sensex index, is the benchmark index of the Bombay Stock Exchange (BSE) in India. Sensex comprises 30 of the largest and most actively-traded stocks on the BSE, providing an accurate gauge of India’s economy.