The Race for Copper, the Metal of the Future

Date Posted: May 27, 2021

Read time: 47 min

The International Energy Agency (IEA) was founded in 1974 in response to oil embargos the previous year that caused the global price of oil to surge 300% from $3 per barrel to $12 per barrel. From the start, the IEA's mission has been to help member nations deal with major oil supply disruptions.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

The International Energy Agency (IEA) was founded in 1974 in response to oil embargos the previous year that caused the global price of oil to surge 300% from $3 per barrel to $12 per barrel. From the start, the IEA’s mission has been to help member nations deal with major oil supply disruptions.

Over the years, the group’s purview has broadened to include more than just oil security, and in its most recent report, the IEA sounds the warning bell on the global supply of key minerals—particularly copper.

“Today’s supply and investment plans for many critical minerals fall well short of what is needed to support an accelerated deployment of solar panels, wind turbines and electric vehicles,” IEA Executive Directive Faith Birol writes.

Many of these minerals are produced by a very small number of companies in a small number of jurisdictions. Take rare earth metals, used in everything from semiconductors to smartphone batteries.

China controls between 80% and 95% of the world market, depending on the mineral.

Or look at copper. Chile and Peru are responsible for a combined 40% of global output. The largest copper mine in the world, Chile’s Escondida, is believed to have reached peak production. Meanwhile, the Chilean government has threatened to shut down the mine—57.5% of which is owned by BHP—for its water usage. Oh, and did I mention there’s a strike at Escondida?

These are only near-term risks to global supply. Looking more long-term, the risks increase and could be more severe.

Copper Supply Constraints as Demand Surges

Like gold, fewer and fewer large copper deposits are being discovered, and the time between discovery and production has lengthened over the years as costs rise. S&P Global Kevin Murphy called last decade “dismal” in terms of new discoveries. Of the 224 copper deposits that were discovered between 1990 and 2019, only 16 were found in the past 10 years. Although the earth’s surface still has an abundance of the red metal, most new deposits are of low grade.

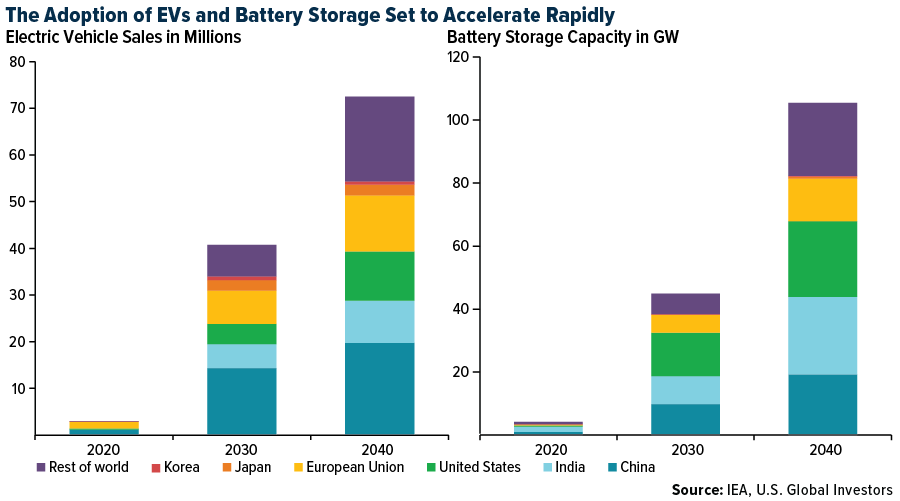

This could be a problem going forward. As I’ve written about before, the adoption of electric vehicles (EVs) and battery storage technology—both of which rely heavily on copper—is set to accelerate rapidly over the coming decades. Last year, EV sales were around 3 million. By 2040, they could be as high as 70 million.

According to the IEA, copper will remain the most widely used metal in renewable energy technologies.

Compared to aluminum, nickel and zinc, its importance is rated high for most new energy-related projects. That’s mainly because its electrical conductivity is the second best after silver and 60% higher than aluminum. Goldman Sachs predicts that by 2030, copper demand will grow nearly 600% to 5.4 million tons.

Commercial Production Begins at Ivanhoe’s Kamoa-Kakula

Although large copper discoveries are becoming fewer and farther between, there are notable exceptions. The IEA mentions Peru’s Quellaveco, majority-owned by Anglo American, and Ivanhoe’s Kamoa-Kakula in the Democratic Republic of the Congo (DRC).

I’ve written about the developing Kakula project several times before. This week, Ivanhoe announced that copper concentrate production officially began at the world-class discovery, several months ahead of schedule.

“Discovering and delivering a copper province of this scale, grade and outstanding ESG credentials, ahead of schedule and on budget, is a unicorn in the copper mining business,” commented Ivanhoe founder and co-chair Robert Friedland, who added that Kakula was discovered only five years ago. This represents “remarkable progress by the mining industry’s glacial standards from first drill hole to a new major mining operation.”

Kakula, Robert says, is now on path to become the world’s second largest copper mining complex and perhaps even the largest. Further, the project is estimated to be the world’s highest grade major copper mine. Further still, Ivanhoe pledges that Kakula will be a net-zero greenhouse gas generator, making the company an attractive ESG play.

Record Copper Price by Year-End?

This week, analysts at CIBC announced that they adjusted their end-of-year copper price forecast to $5.25 a pound, Kitco reports. The estimates are now 22% and 32% above 2021 and 2022 consensus estimates.

The supporting factors include “positive economic data, USD weakness, continued Chinese demand and tight global inventory levels,” CIBC wrote.

If true, this should be supportive of copper miners such as Ivanhoe going forward.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 0.94%. The S&P 500 Stock Index rose 1.24%, while the Nasdaq Composite climbed 2.06%. The Russell 2000 small capitalization index gained 2.44% this week.

- The Hang Seng Composite gained 1.56% this week; while Taiwan was up 3.49% and the KOSPI rose 1.02%.

- The 10-year Treasury bond yield fell 2 basis points to 1.596%.

Airline Sector

Strengths

- The best performing airline stock for the week was Avianca, up 17.2%. In a travel survey, Bank of America for the first time recorded that sales are above pre-pandemic levels for leisure travel. Domestic leisure travel is continuing to surge in the U.S., with ticket sales up 4.4% over 2019 levels. Sales of tickets through travel agents and online were up 4.4% versus 2019 levels as well. Flights will be full, as Stifel notes that current schedules are indicating capacity will be at 88% and 92% of 2019 levels, respectively.

- An index tracking consumer confidence in air travel from Morning Consult continues to trend upward. The index is derived by weighting results from survey respondents to a variety of questions related to airline purchase consideration, usage frequency, trust in and awareness of different U.S. airlines.

- UBS’ Airline Fare Tracker is showing a 29% increase year-over-year in ticket prices. Fares are now up 6% from 2019, according to UBS. United Airlines noted that yields on tickets booked since the start of May for flights in the June quarter are in line with 2019 levels on a consolidated basis, and that domestic leisure yields are higher than 2019 yields over the same period.

Weaknesses

- The worst performing airline stock for the week was Norwegian Air Shuttle, down 56.0%. The stock plunged after capital that was raised to exit bankruptcy became tradable. EasyJet earnings are being reduced by 14% due to new capacity guidance that is 15% of 2019 levels, which is down from 20% previously for the current quarter.

- LATAM Airlines Group and Azul have terminated their code share agreement. This is a negative for both carriers as they represented around 5% of traffic for each other. It is believed that Azul was hoping to purchase LATAM out of bankruptcy, however, the discussions did not work out, leading to the termination of this codeshare.

- U.S. regulators downgraded Mexico’s aviation safety rating, reports the Associated Press, a move that prevents Mexican airlines from expanding flights to the United States. The downgrade from Category 1 to Category 2 by the Federal Aviation Administration (FAA) is due to a shortage of technical and specialized labor forces. Aero Mexico is the most impacted airline, as 82% of capacity is focused on international routes. In addition, the downgrade means that U.S. airlines won’t be able to sell tickets on flights operated by Mexican airlines.

Opportunities

- Breeze Airways officially announced its launch debuting in 39 markets starting in late May. The new airline focuses on underserved markets with limited competition. Tampa International Airport and Breeze will make history together next week as they launch their inaugural flight departing from Tampa to Charleston, SC.

- European bookings showed a large improvement last week. Sales improved to -69% of 2019 levels, which is better than the -75% from the previous week. This is the first full week since the U.K.’s “green list” announcement. EU ambassadors agreed on proposals to ease travel restrictions for non-EU countries, which would allow vaccinated tourists and loosen the safe country criteria.

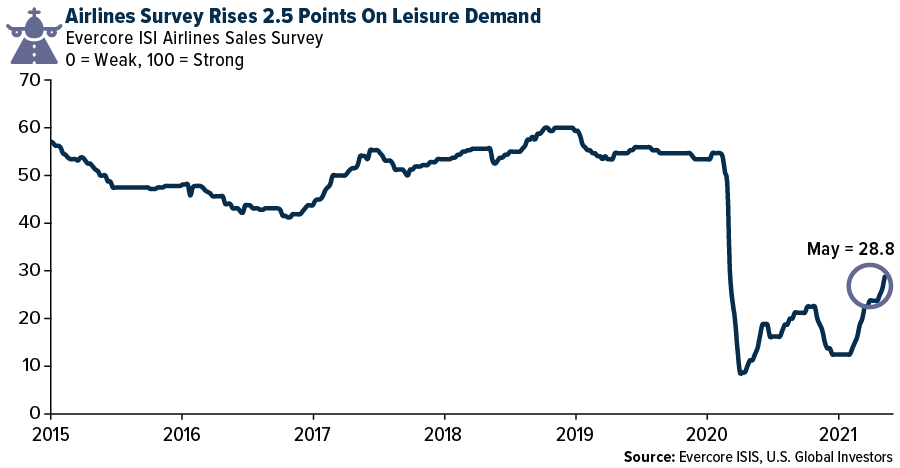

- Evercore ISI’s Airlines Sales Survey rose three points in May, from 26 to 28.8, based primarily on improved leisure demand. This is now the highest level since March 2020.The survey increased 10 points in the first quarter and is up six points so far in the second quarter. Comfort levels with getting on a flight and traveling again continues to improve.

Threats

- Transatlantic and transpacific travel has not shown many positive signs of a recovery due to the slow reopening of borders. In a statement on Tuesday, Lufthansa executive board member Harry Hohmeister commented that falling infection rates and a rising number of vaccinations should allow for a cautious increase in transatlantic air travel, reports Reuters, urging Germany to come up with a clear plan to make this possible.

- Air traffic between the U.S. and Canada is significant to both countries. This week Canada extended its border closure with the U.S. for the fourteenth time, through June 21. Canadian Prime Minister Trudeau expects border reopening to commence when 75% of U.S. citizens are vaccinated, which may take a very long time.

- Singapore Airlines is expected to report losses for at least two more years due to a slow recovery of long-haul international flights and slow border reopening. The airline is also very popular among business travelers, and with business travel very slow to recover, this adds to the forecast losses. In Australia, international borders are likely to remain closed until at least the end of 2021, and Qantas has cancelled all international flights through December of 2021.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Poland, gaining 4%. The best performing country in Asia this week was the Philippines, gaining 8%.

- The Russian ruble was the best performing currency in emerging Europe this week, gaining 0.60%. The South Korean won was the best performing currency in Asia this week, gaining 1.2%.

- Confidence data in the Eurozone is improving as vaccinations are allowing the reopening of economies throughout the region. On Friday, the consumer confidence came in at negative 5.1 for May, up for the fourth month in a row and reaching the highest level since October 2018. Economic sentiment was reported at 114.5 versus an expected reading of 112.3. Service confidence spiked to 11.3 from 2.1, and above the expected reading of 6.3.

Weaknesses

- The worst performing country in emerging Europe for the week was Romania, losing 2.2%. The worst performing country in Asia this week was South Korea, losing 1%.

- The Turkish lira was the worst performing currency in emerging Europe this week, losing 1.7%. The Pakistani rupee was the worst performing currency in Asia, losing 0.70%.

- China brought only $10.4 billion of American goods in April, taking the total amount to $147 billion. China agreed to purchase $378 billion from America over two years and is running behind schedule, with eight months remaining.

Opportunities

- The White House announced that U.S. President Joe Biden will meet with Russian President Vladimir Putin in Geneva on June 16. The leaders will have the opportunity to openly discuss a range of issues face-to-face. The U.S. recently said that it would like to see a more predictable and stable relationship with Russia. No big breakouts are expected, but the meeting could set the stage to improve communication between both parties.

- Hungary, who last year threatened to veto the EU’s next budget, unanimously ratified the EU’s largest ever stimulus package, paving the way for 800 billion euros ($980 billion) to be distributed among EU members. All members must approve the stimulus plan before disbursements can be made. Austria is the last to approve the plan but is expected to do so this week.

- Poland released details of its previously proposed plan to spend a $19 billion-per-year stimulus package on innovation. As part of the proposed measure, companies would be able to deduct 150% of the cost of introducing industrial robots. The proposed relief measures are much needed in Poland, as they will increase the attractiveness of the country as a place to invest and relocate production. If the plan is passed in the parliament, it will take effect January 2022.

Threats

- This week Belarus rerouted and forced landing of a Ryanair jet in the country’s capital Minsk, detaining an opposition journalist aboard the plane. Airlines are suspending flights over Belarus after EU leaders urged EU-based airlines to avoid Belarus airspace and banned the country’s airline from the 27-nation bloc. Belarus is a small eastern European country, and although it may seem insignificant standing alone, its biggest trading partner is Russia who supports the country’s president Alexander Lukashenko.

- Bloomberg reported that $1.3 trillion worth of debt will be maturing over the next 12 months in China, just as defaults are surging. That is 30% more than what U.S. companies owe and 63% more than in all of Europe. The country’s onshore defaults have swelled from negligible levels in 2016 to exceed 100 billion yuan ($15.5 billion) for four straight years. That milestone was reached again last month, putting defaults on track for another record annual high.

- Public support for the President of Turkey Recep Tayyip Erdogan fell to an all-time low last month as people are dissatisfied with the way the government is handling the pandemic, high inflation, and the weakening of the lira. The lira is the world’s worst performing currency, losing 14% year-to-date. According to Bloomberg, 17% of people who voted for AKP (the ruling party) in the 2018 general elections said they will never vote for them again. The next general election is scheduled for 2023, but if it takes place sooner the AKP party will not receive as many votes this time

Energy and Natural Resources Market

Strengths

- The best performing commodity for the week was coffee, up 8.16%. Arabica coffee reached its highest levels since late 2016 due to the world’s top supplier Brazil issuing a water emergency alert for key growing areas, raising concerns about tight coffee supply.

- Oil prices, buoyed by the optimism over U.S.-led demand, reached the highest in more than two years. West Texas Intermediate (WTI) settled at the strongest level since October 2018, while market volatility on the global Brent benchmark fell to the lowest level since August 2020. Traders expect a bullish summer as the Memorial Day weekend marks the beginning of the summer driving boom in the U.S., adding that the national stockpiles are already depleting. There are still concerns regarding Iranian crude entering the market just as the Organization of Petroleum Exporting Countries (OPEC) and its allies lift self-imposed curbs on exports. During the week, WTI and Brent crude rose 4.78% and 4.80%, respectively.

- The German government has selected 62 proposals from various companies in a bid to increase its hydrogen production capacity as it eyes climate neutrality by 2045. The projects include 2 gigawatts of electrolysis capacity, 1,056 miles of hydrogen pipelines and 12 mobility projects. The German Economy and Energy Minister, Peter Altmaier, said at a news conference that the government will subsidize the projects with $9.8 billion to promote the nascent technology and accelerate the nation’s transformation toward a greener economy, and noted that the proposal could increase investments in the whole hydrogen value chain by $40.2 billion in the coming years.

Weaknesses

- The worst performing commodity for the week was lumber, down 9.77%. Demand for lumber is slowing down and new supply is coming to the marketplace.

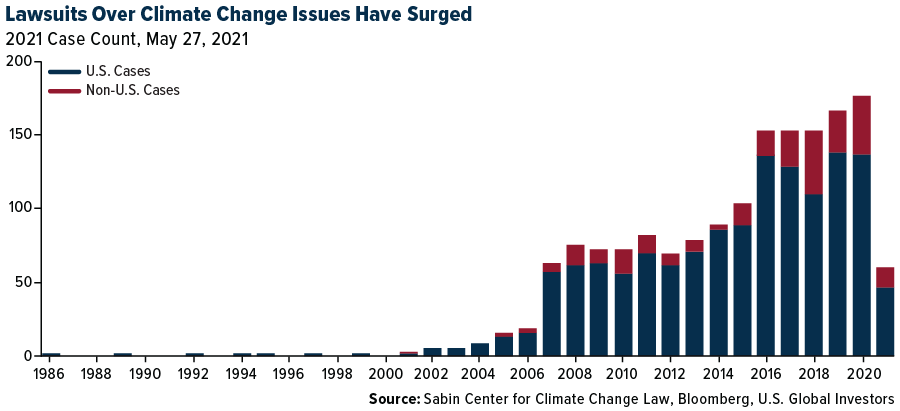

- Big oil companies faced a tough week as Exxon Mobil lost a historic proxy fight, Chevron investors split from management and backed a stringent climate proposal, and Royal Dutch Shell lost a lawsuit in a Dutch court regarding the company’s emission targets. Engine No. 1, an activist hedge fund which owns 0.02% of Exxon, won at least two board seats at the oil giant’s annual meeting, showcasing the increasing concerns regarding climate change amongst its shareholders. The Chief Investment Officer for the California State Teacher’s Retirement System (CalSTRS), the second largest U.S.-state pension fund, mentioned that it was an early backer of Engine No. 1’s push for Exxon board seats as the western world’s biggest oil company had been “throwing money down the drill hole” and that a change was needed since the company reported its first yearly loss in over four decades. Additionally, the chart below shows that the number of lawsuits over climate change concerns have been increasing in the past decade and could pose threats to more companies that are involved with fossil fuels.

- Goldman Sachs and Citigroup believe that China’s efforts to curb the rally in commodities prices over concerns of inflation could be in vain as the speed of economic recovery and increasing demand in advanced economies means that the real supply-demand balance will prevail, and that China is no longer the buyer dictating prices. Goldman Sachs analysts added that the recent price dip after the Chinese government warned about speculation can be seen as a clear buying opportunity as commodities prices remain on an upward trajectory due to tight supply. Furthermore, CEO of Freeport-McMoRan, the world’s largest publicly traded producer of copper, said in an interview that China’s curbing efforts could have a short-term impact on the market, but the strong demand and supply scarcity are the real factors that will dictate long-term prices.

Opportunities

- U.S. automotive giant Ford Motor Co. announced that it is set to boost its spending on electric vehicles by 36% to $30 billion over the next four years and will have 40% of its models battery-powered by the end of this decade. The bulk of the investment will be focused on producing its IonBoost batteries and development of solid-state batteries that are touted as the next breakthrough in a bid to lower prices and increase driving range on a single charge. Jim Farley, Ford’s CEO, mentioned that this is the biggest opportunity for growth and value creation that the company has seen since Henry Ford scaled Model T production.

- The Greek government announced its plans to allocate part of its European Union (EU) COVID-19 relief package to accelerate the nation’s transition to a greener economy with the help of the private sector. Government advisers from the National Resilience and Recovery Plan reported that they are budgeting $7.55 billion for green energy projects and that the private sector will invest $14.13 billion. Additionally, the Bank of Greece expects this new proposal for using EU funds will increase real economic output by 7% by 2026 and create 180,000 new jobs.

- Australia-based BHP Group is planning a potential partnership with Canadian firm Nutrien Ltd., which is the world’s biggest fertilizer distributor, to bring its Jansen potash mine, which is in Canada, into production. Although a certain deal has not been announced, the two companies are exploring options including Nutrien becoming the operator of the mine and selling potash through its existing channels or Nutrien taking a stake in the Jansen mine. BHP would gain from this partnership as it would reduce its financial and operational risk, and as it is a new entrant in the potash space, it would benefit from Nutrien’s industry knowledge. BHP also noted that it expects potash to become a cornerstone of its future operations, monetizing on the increased pressure on agricultural land to feed the growing global population.

Threats

- Prices of solar modules are on the rise just as governments throughout the world started gearing up to reduce their emissions to reach carbon neutrality. After falling 90% over the past decade, solar module prices have risen 18% since the beginning of the year, partly driven by a 400% increase in the cost of polysilicon, a key raw material in the production of solar panels, and the overall rally in the commodities market. Analysts covering the solar energy sector believe that large-scale projects might get delayed due to rising costs, making 2021 the first year of negative growth in global solar power installations in 17 years.

- Norilsk Nickel PJSC, the world’s largest producer of palladium, reported that flooding at its Arctic mines has caused significant disruptions and it expects the market deficit will be around 900,000 ounces. The Russian mining company was projecting a balanced market by December but flooding at its Oktyabrsky and Taimyrsky mines and an incident at its concentrator has upended Norilsk’s operations. Palladium reached record highs this month on the back of growing demand from the auto sector, which is the biggest consumer of the metal as it is used in devices to curb pollution from the vehicles.

- Moody’s Investor Services, which provides credit ratings for companies, noted that the events that transpired at big western oil companies this week could mean that the industry faces a higher credit risk. Referencing Exxon Mobil, Chevron Corp., and Royal Dutch Shell, Moody’s analysts believe that there could be a substantial shift in the landscape for oil companies, which had previously avoided shareholder votes on climate-related issues. Moody’s added that stricter regulations over emissions means that the oil industry must fast-track its transition from fossil fuels, which could reduce companies’ debt capacity at a time when they need to increase capital expenditures. Moreover, the companies that lag in their transition might face increased capital costs and restricted access to capital.

Domestic Economy and Equities

Strengths

- Weekly initial jobless claims came in at 406,000, below consensus for 428,000 and down from the prior week’s 444,000. This is the lowest level since March 14, 2020. The largest drops were seen in Florida, New Jersey, Ohio, Texas and Washington. Continuing claims were 3.6 million this week versus expectations for 3.7 million, and below last week’s downwardly revised 3.73 million.

- A measure of business conditions in the Chicago region had another strong reading in May, reaching its highest level in 47 years, a trade group said Friday. The Chicago Business Barometer, also known as the Chicago PMI, jumped to 75.2 in May from 72.1 in April, which was the highest reading since December 1983.

- Royal Caribbean Cruises Ltd. was the best performing S&P 500 stock for the week, increasing 13%. Shares gained after company announced it will resume cruises in the U.S. starting on June 26.

Weaknesses

- U.S. orders for big-ticket manufactured goods dropped unexpectedly in April for the first time in 11 months, pulled down by plunging orders for cars and automobile parts. Orders for auto parts, disrupted by a shortage of computer chips, dropped 6.2% in April. Orders for military aircraft and aviation parts fell 8.5%.

- The Personal Consumption Expenditure Deflator, which is a measure of inflation based on changes in personal consumption, spiked to 3.1% from a revised 1.9%. The consensus was for 2.9%.

- Dollar Tree Inc. was the worst performing S&P 500 stock for the week, losing 10.2%. Shares of Dollar Tree declined sharply on Friday after the retailer’s full-year earnings-per-share guidance came in below expectations due to higher freight costs.

Opportunities

- Senate Republicans delivered a new spending proposal worth $928 billion, including $506 billion for roads, bridges, and major infrastructure, $98 billion for public transit, and $72 billion for water systems. Washington still struggles to strike a deal on a broader infrastructure package. Republicans rejected the White House’s offer of a $1.7 trillion package, down from the original request of $2.25 trillion.

- The U.S. dollar has already declined 13% over the past 14 months and is close to making a technical downside breakout. Dollar weakness supports commodity prices, lifts inflation, spurs growth, and most importantly, lifts S&P earnings, Ed Hymen said in his daily market update this week.

- The second estimate for first-quarter gross domestic product remained unchanged at a 6.4% annual rate of increase, as expected. The Organization for Economic Cooperation and Development (OECD) expects the U.S. economy to expand 6.5% this year, up sharply from a forecast of 3.2% in December.

Threats

- Reuters said that strategists in its latest poll see the S&P 500 ending the year at 4,300, up only 2.5% from current levels. Many strategists in the poll commented that a correction in stocks over the next three months is likely, and several viewed the market as overvalued at current levels. Inflation, peak growth, Federal Reserve tapering, along with stretched valuation and sentiment indicators are among the higher-profile areas of concern.

- U.S. President Joe Biden is set to propose a budget that would increase federal spending to $6 trillion in the coming fiscal year, with an annual deficit of more than $1.3 trillion over the next decade. Spending would rise to $8.2 trillion by 2023, while the federal debt would rise to 117% of gross domestic product over the next decade.

- The average rate on a 30-year mortgage fell below 3% again this week. However, home buyers are still having a difficult time finding properties they can afford. Sales of new homes declined in April by more than forecast, as higher prices constrained demand.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Helium, rising 35.82%.

- Ripple is set to use its RippleNet blockchain technology to process the first real-time payments between Oman and India. Oman’s second-largest bank, BankDhofar, and Pune-based IndusInd Bank are partnering with Ripple, allowing BankDhofar’s customers to use its app to transfer up to $2,600 to accounts in India, which is the world’s largest receiver of remittances. This news comes a week after National Bank of Egypt announced that it is joining RippleNet to set a remittance corridor with the United Arab Emirates.

- The volume of Ethereum futures traded on various exchanges reached record levels in May, with contracts worth more than $1.6 trillion exchanging hands during the month. This is almost a 50% increase from the volume seen in the previous month, buoyed by the second-largest cryptocurrency by market capitalization reaching a new high of $4,362.35 in May. Although the cryptocurrency market has seen a short-term correction, trading activity in the futures market has remained strong.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performer for the week was Terra, down 33.26%.

- Binance Smart Chain (BSC), the world’s largest cryptocurrency exchange’s smart contract blockchain, has come under scrutiny recently as decentralized finance (DeFi) protocols built on the blockchain suffer an increasing number of hacks and exploits, with the recent hack of bEarn Fi resulting in an $11 million loss. Binance representatives suggest that it cannot do much to roll back the exploits and that it is common in DeFi to see such exploits, even though the exchange has significant control over the BSC and is far more centralized than competing blockchains. Furthermore, another flash loan attack this week on the BSC led to a loss of $7.2 million from the BurgerSwap DeFi protocol.

- Senior officials at the United Kingdom Financial Conduct Authority (FCA) reported that cryptocurrency businesses in the nation are struggling to meet Anti-Money Laundering (AML) standards set by the regulators. According to the FCA, only five crypto-related businesses have received registration from the regulatory body and over 90% of the businesses have withdrawn their applications as they failed to adopt robust AML control frameworks as well as employ proper staff. The FCA has expanded its oversight on the crypto industry this year, and in March, it announced that crypto firms will have to submit yearly financial crimes reports.

Opportunities

- PayPal Holdings Inc. announced its plan to allow users to withdraw cryptocurrencies to third-party wallets. The payments giant enabled cryptocurrency purchases on its platform in October 2020 for U.S. customers and is set to roll out the offering in select countries in 2021. Currently, users can only buy Bitcoin, Ethereum, Bitcoin Cash and Litecoin using their PayPal accounts. The company has not provided a launch date for its withdrawal feature, but the initial roll out of the third-party wallet integration is expected to be gradual and location based.

- The U.S. Securities and Exchange Commission (SEC) has begun official review of two separate Bitcoin exchange-traded fund (ETF) applications submitted by Fidelity Investments and Anthony Scaramucci’s SkyBridge Capital. Both applications were filed in March, with SkyBridge Capital partnering with First Trust Advisors to list an ETF on the NYSE Arca. Fidelity Investments reported that its ETF product will track Bitcoin’s price using a propriety index which derives prices from multiple feeds. Currently, the SEC has six ETF applications in its pipeline for review.

- VanEck, the New York-based investment management company, is set to list its cryptocurrency exchange-traded products (ETPs) on the Euronext stock exchanges in Amsterdam and Paris. Its VanEck Vectors Bitcoin exchange-traded note (ETN) and VanEck Vectors Ethereum ETN will start trading on June 1, with a total expense ratio of 1%. The company reported that the ETNs will provide exposure to investors without them holding the crypto themselves, and that VanEck’s custodian, Bank Frick, will keep the cryptocurrencies held by the ETNs in cold storage to guarantee their security. VanEck has also applied with the U.S. SEC to list a Bitcoin ETF.

Threats

- Iran’s President Hassan Rouhani announced on national television that he is enforcing a ban on cryptocurrency mining in the nation until September 22. The ban, which is set to be enforced immediately, comes on the back of an unusually dry spring season in the country, leaving Iran struggling with hydropower shortages. Rouhani also mentioned that the nation’s authorized miners use only 300 megawatts of electricity while unauthorized operations account for 2,000 megawatts of electricity usage. Iranian cryptocurrency miners account for 3.82% of Bitcoin’s total hash rate.

- Bank of Korea’s governor Lee Ju-yeol believes that excessively leveraged cryptocurrency trading poses threats to the country’s financial system as it puts households at risk of financial damages, given the instability and volatility of crypto markets. He added that the South Korean central bank expects the increasing crypto trading to have a negative impact on the financial system in any respect and has pledged to monitor transactions of the nation’s financial institutions involved with leveraged crypto trading and could curtail new loans to prevent defaults.

- The Chinese government’s latest efforts to curb cryptocurrency mining in the nation have led some investors to believe that only the biggest miners can survive as they have the resources to shift their operations underground and continue mining in other parts of the country. Even with enough capital to relocate operations overseas, the mining companies will have trouble finding suitable sites as there is little to no idle capacity in major mining hubs like Kazakhstan and Russia. Furthermore, there are growing concerns about mining power becoming too centralized and that a few miners could manipulate the market and shut out smaller miners if they gain over 50% of the network’s mining power. Chinese crypto miners account for 65.08% of Bitcoin’s total hashrate.

Gold Market

This week spot gold closed at $1,903.77m, up $22.52 per ounce, or 1.20%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher/lower by 0.06%. The S&P/TSX Venture Index came in up 0.95%. The U.S. Trade-Weighted Dollar ended the week flattish, up just 0.05%.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| May-25 | New Home Sales | 950k | 863k | 917k |

| May-25 | Conf. Board Consumer Confidence | 118.8 | 117.2 | 117.5 |

| May-27 | Hong Kong Exports YoY | 25.9% | 24.4% | 26.4% |

| May-27 | Durable Goods Orders | 0.8% | -1.3% | 1.3% |

| May-27 | GDP Annualized QoQ | 6.5% | 6.4% | 6.4% |

| May-27 | Initial Jobless Claims | 425k | 406k | 444k |

| May-31 | Germany CPI YoY | 2.3% | — | 2.0% |

| May-31 | Caixin China PMI Mfg | 51.9 | — | 51.9 |

| Jun-1 | Eurozone CPI Core YoY | 0.9% | — | 0.7% |

| Jun-1 | ISM Manufacturing | 61.0 | — | 60.7 |

| Jun-3 | ADP Employment Change | 690k | — | 742k |

| Jun-3 | Initial Jobless Claims | 410k | — | 406k |

| Jun-4 | Change in Nonfarm Payrolls | 678k | — | 266k |

| Jun-4 | Durable Goods Orders | — | — | -1.3% |

Strengths

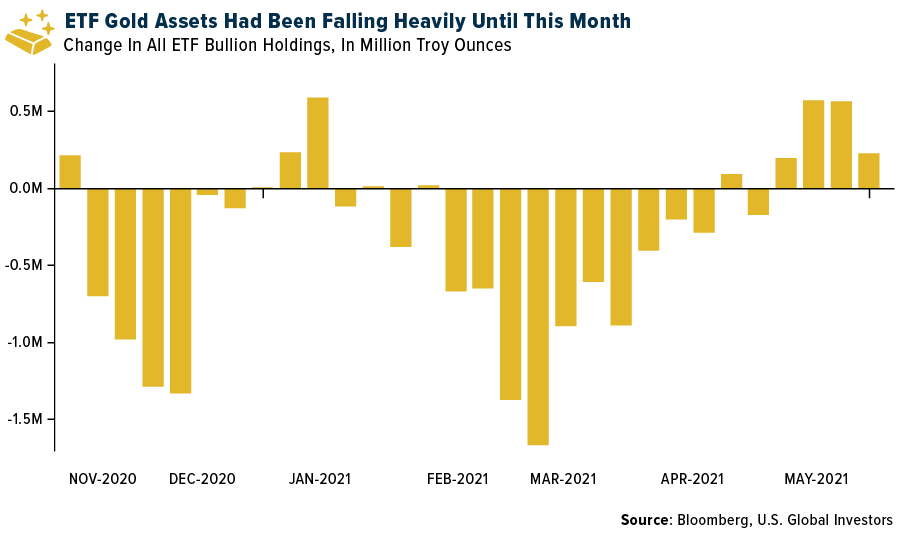

- The best performing precious metal for the week was palladium, up 1.45% on curtailed supply news. Gold continues to do well, as hedge funds raised their net long position to the highest level since January. ETFs have had inflows throughout May, following three months of sales. The recent weakness in Bitcoin is helping the price of gold, as well as a weak dollar. There is also belief that Russia will resume buying of gold for its central bank. The central banks in India and Thailand also have been buying gold recently. Gold stored at the Bank of England has been selling for premiums recently, implying that there is active central bank buying. The Bank of England stores and sells gold on behalf of other central banks.

- Barrick Gold held an investor day discussing its Nevada Mines operation. There are 200 possible exploration targets that could bolster the production profile and extend production visibility to 15 years. Current guidance for the mine is a 200,000-ounce decline in 2022. The company also highlighted that it cut G&A by half after its deal with Newmont at the Nevada Mines operation.

- Wesdome Gold will restart its gold mine at the Kiena siter in Val d’Or, Quebec. The mine is anticipated to have a seven-year life, producing an average of 84,000 ounces at US$380 per ounce cash costs.

Weaknesses

- The worst performing precious metal for the week was platinum, but still had a positive gain of 1.04%. Gold miner Dacian Gold is seeking early support for an equity raising that could see it raise about $40 million. The news comes only days after Dacian Gold released drilling results at Mt. Marven, which is located at its 100 per cent owned Mt. Morgans Gold Operation in Western Australia. It also comes about 12 months after Dacian Gold last tapped shareholders for fresh funds. On that occasion, Dacian Gold raised $98 million in a placement and non-renounceable rights issue.

- AngloGold has reported that following a ground incident last week at the Obuasi Mine in Ghana (where one miner remains missing) that it will need to undertake an in-depth assessment of mine design, mine schedule, and ground management plans before progressively restarting the mining operations. The early indications are that this was caused by the failure of a horizontal or sill pillar, in one of the smaller mining stopes. This will see AngloGold suspend its 2021 production guidance of 300,000-350,000 ounces at a total cash cost of $660-$710 per ounce.

- Bloomberg wrote a report indicating that Barrick Gold’s earnings lack strong momentum in 2021. Output will fall this year 3% as non-core assets are disposed of. Gold production expansion may be difficult until 2030.

Opportunities

- Montage Gold reported good results at its Kone silver mine. Consensus was for a 200,000-ounce operation with a mine life of 10+ years. A recent preliminary economic assessment guides to 249,000 ounces per year of silver with a mine life of 15 years. The payback period on exploration is 2.8 years.

- MMC Norilsk Nickel PJSC, the world’s largest producer of palladium, expects a significant shortfall of the metal this year after flooding at its Arctic mines upended its December projection for an almost balanced market. Increased demand combined with flooding at Nornickel’s Oktyabrsky and Taimyrsky mines, along with incidents at the company’s concentrator, will produce a palladium deficit of 900,000 ounces.

- Gold and precious metals along with and many mined commodities have hit record prices this year as the global economy bounces back from Covid-19 but business are finding materials and general supplies limited. For instance, the price of copper—used in construction and to conduct electricity—has nearly doubled over the past 12 months to a record of $10,762 a metric ton earlier in the month. Miners, however, have been cautious towards deploying new capital. Executives seem to be more focused on delivering financial performance, that discipline is now raising the specter of supply restraint which should keep prices firm.

Threats

- An attempted coup in Mali, Africa’s third-largest gold producer, threatens to derail presidential elections planned for February that are meant to return the nation to civilian rule. The move comes after an Aug. 18 coup saw the ouster of former President Ibrahim Boubacar Keita and adds to the chaos in the West African country. Mali produced 66.5 tons of gold in 2020, making it the third-largest producer of the metal in Africa, according to the Mali Mining and Petroleum Conference and Exhibition. Companies including B2Gold, Barrick Gold and AngloGold Ashanti operate in the West African nation.

- B2Gold provided an update confirming that the evolving political situation in Mali has not impacted operations at the Fekola Mine. This comes after Mali’s interim President Bha Ndaw and Prime Minister Moctar Ouane were arrested by the military on May 24th.

- Gold has done well over the past two months, but with several FOMC meetings between now and year-end, the risk of “taper talk” may be a headwind to the price of gold because yields may increase.

Leaders and Laggards

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (03/31/2021):

United Airlines

Azul SA

Singapore Airlines Ltd.

Qantas Airways Ltd.

Anglo American Plc

Ivanhoe Mines Ltd.

Barrick Gold Corp.

Wesdome Gold Mines Ltd.

Newmont Corp.

AngloAshanti Ltd.

Montage Gold Corp.

MMC Norilsk Nickel PJSC

B2Gold Corp.

BHP Group Ltd.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

Personal consumption expenditures (PCE) is the value of the goods and services purchased by, or on the behalf of, “persons” who reside in the United States.