This Economic Indicator Is Proving the Naysayers Wrong

Date Posted: November 22, 2019

Read time: 53 min

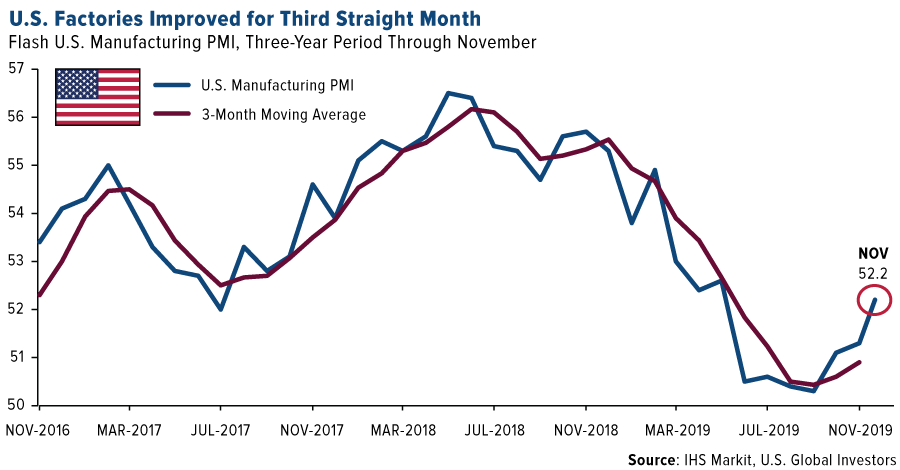

Flying in the face of negative economic news, U.S. factories picked up steam for the third straight month in November. The preliminary PMI, a leading indicator we closely track here at U.S. Global Investors, pulled further away from its August low with a reading of 52.2 this month.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

Flying in the face of negative economic news, U.S. factories picked up steam for the third straight month in November. The preliminary manufacturing purchasing manager’s index (PMI), a leading indicator we closely track here at U.S. Global Investors, pulled further away from its August low with a reading of 52.2 this month. That’s up from 51.3 in October and marks a seven-month high.

Remember, investors are better served when they follow the trend lines, not the headlines.

A raft of economic reports on Friday welcomed the turnaround:

Chris Williamson, chief economist at IHS Markit—which releases the monthly PMI—wrote that the November reading “adds to evidence that the worst of the economy’s recent soft patch may be behind us.”

Responding to the manufacturing uptrend, Renaissance Macro’s head of economics, Neil Dutta, urged investors to “look for construction activity to rise.”

“Today’s improvement,” wrote Cornerstone Macro’s Nancy Lazar, “shows U.S. manufacturing is recovering as trade uncertainty recedes.”

Finally, Stan Shipley at Evercore ISI said that today’s improved PMI and consumer sentiment releases “suggest solid employment and consumer spending will pull the manufacturing sector higher rather than the manufacturing sector dragging the overall economy lower.”

Taken together, this is all very constructive not just for manufacturers but also exporters, container shipping companies and cargo airlines, not to mention the energy, materials and financial sectors.

The Boeing Co., for instance, announced a bump in orders for its still-grounded 737 MAX aircraft. Following this year’s Dubai Airshow, the world’s largest aerospace event, Boeing reported that Kazakhstan’s Air Astana had committed itself to as many as 30 MAX jets, while an undisclosed buyer ordered 20. This comes after SunExpress, a Turkish leisure carrier, purchased 10, bringing the total value of MAX sales to $7.5 billion.

Negative headlines may get the clicks, but savvy investors who can look past those headlines and follow the money often get the rewards.

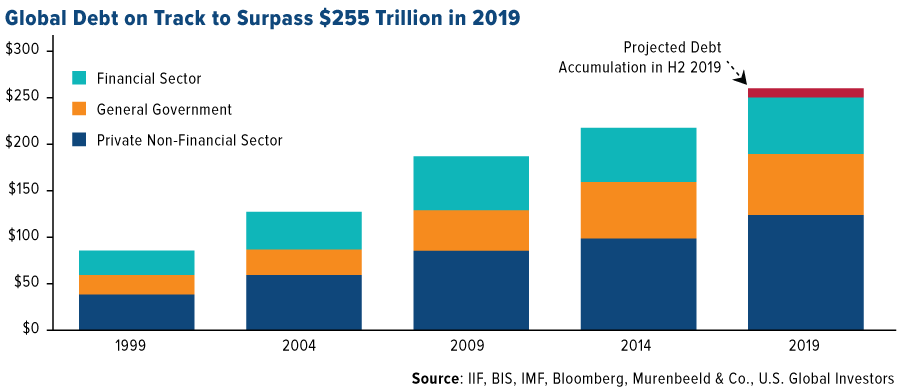

Global Debt Expected to Hit a New Record Amount

Although the PMI report is encouraging, there’s still reason to remain somewhat cautious long-term. The latest accounting of global debt levels was just released, and the news might be so bad that it’s good—for gold prices, at least.

After climbing above $250 trillion in the first half of 2019, the amount of debt that’s owed by governments, the financial sector and non-financial sector is now forecast to touch a record $255 trillion by year’s end, according to the Washington, D.C.-based Institute of International Finance (IIF).

Says IIF economists, this mind-boggling sum is the equivalent of 320 percent of total global economic activity—the highest level ever.

To put it another way, for every $1 that’s produced today, an additional $3.20 in debt is created and thrown atop the heap. I shouldn’t need to say it, but I will anyway: This is unsustainable.

As economist Martin Murenbeeld writes in his most recent Gold Monitor newsletter, “rising global debt levels is one of our most important medium/long-term factors in the gold outlook.”

That’s because debt “inhibits growth,” Murenbeeld says, “and high debt levels will, when central banks are committed to targeting maximum employment and stable inflation, limit central banks’ policy options to ‘loose’ or ‘very loose.’”

“All this will be very positive for gold, of course!” he adds.

$7 Trillion in Unfunded U.S. Pension Liabilities

Here in the U.S., national debt hit an unimaginable $23 trillion on October 31—Halloween Day, of all days. That’s roughly 107 percent of U.S. gross domestic product (GDP), or nearly double its share of the economy from 2000.

This data comes from U.S. National Debt Clock, which I highly recommend you visit if you haven’t already done so. It’s an invaluable tool.

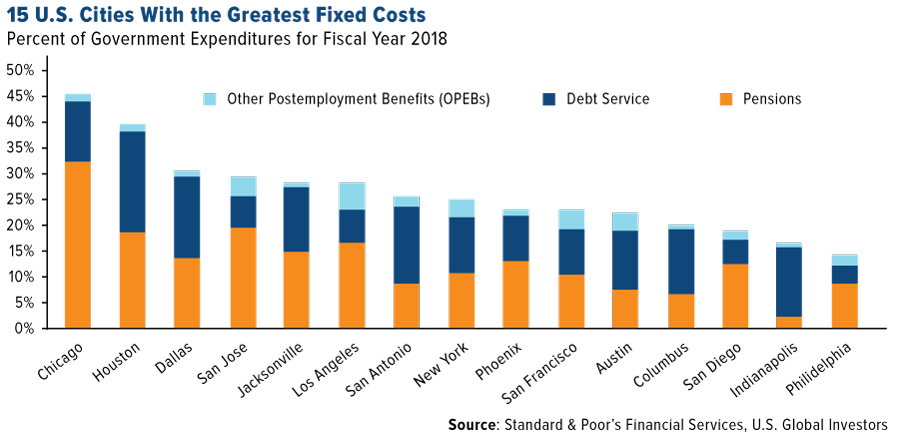

What I find particularly eye-opening is the amount of unfunded public pension liabilities. They’re currently closing in on $7 trillion—the equivalent of $20,700 per U.S. citizen. An unfunded pension is any retirement plan for which sufficient assets have not been set aside, and as Murenbeeld points out, such obligations inhibit economic growth. The greater they become, the more tax revenues must go not toward infrastructure, education and other public benefits but to fixed costs.

It should come as no surprise to you that the U.S. city facing the biggest shortfall at the moment is Chicago, Illinois. About a third of the Windy City’s budget is earmarked for pension payments alone, and when you combine other obligations such as debt service and “other postemployment benefits” (OPEBs), fixed costs amount to 45 percent of expenditures.

Time to Replace Bonds? WGC Says: “Maybe”

My reason for sharing this with you is that, again, higher debt levels have put tremendous pressure on the Federal Reserve (and central banks in general) to keep monetary policy “loose” or “very loose.” In turn, bond yields have been unremarkable lately, to say the least.

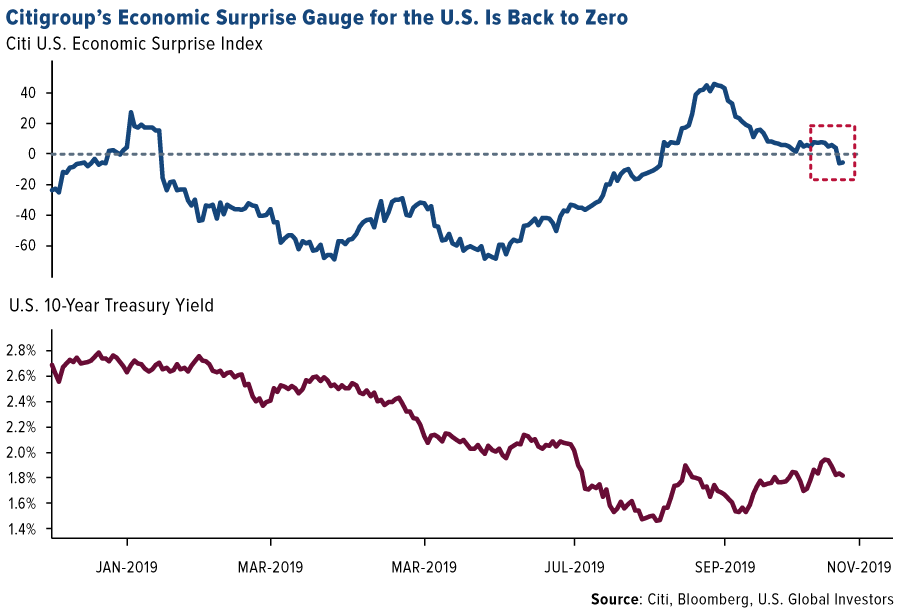

Case in point: The nominal 10-year Treasury yield was trading at just under 1.8 percent today—which, coincidentally, is the annual rate of U.S. inflation, according to the Department of Labor’s October report.

What this means is that the real yield on the 10-year T-note is a big fat 0 percent.

And when this happens, according to the World Gold Council (WGC), “it may be time to replace bonds with gold.”

“Re-optimizing portfolio structures for lower future expected bond returns suggests investors should consider an additional 1 percent to 1.5 percent gold exposure in diversified portfolios,” the WGC writes in a report dated October 30. The London-based group adds that “extremely low or negative yielding bonds could weigh on the overall performance” of investors’ portfolios,” which favors “additional gold exposure.”

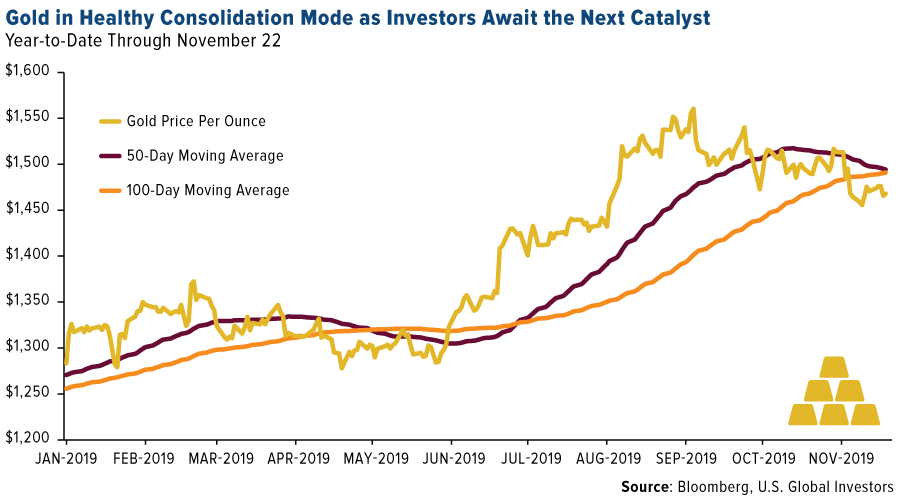

Gold Is on Sale, “Creating Room for Further Gains”

This week gold continued to trade below its 50-day and 100-day moving averages as investors seem to be waiting for the next catalyst, whether that’s Fed policy, movements in the U.S. dollar or developments in the U.S.-China trade war.

In a note to investors this week, UBS strategist Joni Teves says she sees the pause in gold prices as an opportunity for investors.

“We think the ongoing consolidation in the market is healthy, creating room for further gains, and likely also easing some of the persistent concerns on positioning,” Joni writes. “We would view this as an opportunity to gradually re-engage at better levels, especially as investors look to the year ahead, with uncertainty likely to persist and rates likely to stay low.”

She concludes by saying that gold could trade at $1,600 an ounce next year, with a “pit stop at $1,550 over the next three months.”

I believe crypto mining is another interesting space as we head into the new year. To watch my introduction of HIVE Blockchain Technologies, the world’s first and so far only cryptocurrency mining company, click the banner below!

Gold Market

This week spot gold closed at $1,461.60, down $6.70 per ounce, or 0.46 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 0.40 percent. The S&P/TSX Venture Index came in up 0.27 percent. The U.S. Trade-Weighted Dollar rose 0.28 percent

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Nov-19 | Housing Starts | 1320k | 1314k | 1266k |

| Nov-21 | Initial Jobless Claims | 218k | 227k | 227k |

| Nov-26 | Hong Kong Exports YoY | -8.4% | — | -7.3% |

| Nov-26 | New Home Sales | 707k | — | 701k |

| Nov-26 | Conf. Board Consumer Confidence | 126.5 | — | 125.9 |

| Nov-27 | GDP Annualized QoQ | 1.9% | — | 1.9% |

| Nov-27 | Durable Goods Orders | -0.6% | — | -1.2% |

| Nov-27 | Initial Jobless Claims | 220k | — | 227k |

| Nov-28 | Germany CPI YoY | 1.2% | — | 1.1% |

| Nov-29 | Eurozone CPI Core YoY | 1.2% | — | 1.1% |

Strengths

- The best performing precious metal this week was palladium, up 3.85 percent. Shipments of palladium from Switzerland to Hong Kong rose to a five-year high in October. In the weekly Bloomberg survey of gold traders and analysts, most respondents were surprisingly bullish on the yellow metal for next week, expecting further tension between the U.S. and China over Hong Kong. President of Serbia Aleksandar Vucic told reporters this week that it has the largest amount of gold in Serbia’s history and that it will continue to buy gold based on the direction the crisis in the world is moving.

- The Federal Reserve Bank of Atlanta’s GDPNow tracking estimate for the fourth quarter was cut to an annualized 0.3 percent gain, which could breathe new life into gold, writes Bloomberg’s Joseph Richter. Gold can often move in the opposite direction of the market.

- Alacer Gold reported a 28 percent increase in its resource estimate for the Ardich project after an exploration-drilling program. CEO Rod Antal said the resource of 816,000 ounces at Ardich “has grown into a significant discovery” and that they expect “the deposit will continue to grow with additional drilling.”

Weaknesses

- The worst performing precious metal this week was gold, down 0.46 percent. Turkey’s gold reserves fell 941,000 ounces to 17.3 million in the week of November 15 – the largest drop in 14 months. AngloGold Ashanti Ltd. is working to resume operations at its Siguiri mine in Guinea after protests forced operations to close for three days, reports Bloomberg. A company spokesman for AngloGold says that talks with community leaders who are demanding a tar road be extended to their village have been productive.

- Citigroup cut its three-month gold price target to $1,485 from $1,575 an ounce. According to the note, they are still bullish saying, that they “remain bullish bullion in the medium-term and still project fresh cyclical highs being breached by 2021.” South African gold miner Heaven-Sent Gold Group Co. has cancelled its Hong Kong IPO due to unfavorable market conditions, according to Reuters TFR. The company, which owns two mines in South Africa, would have been the first gold miner to be listed in Hong Kong in more than a year.

- Sibanye Gold announced that it has ended its membership in the World Platinum Investment Council – a big move as Sibanye is one of the largest platinum producers. The council’s focus is on stimulating demand; however, Sibanye says that it should consider a basket of platinum-group metals, not just one.

Opportunities

- UBS says that gold will outperform cyclical commodities in 2020 and that political uncertainty could send safe haven flows into the metal. In a report led by Mark Haefele, UBS says “muted economic growth and now lower interest rates reduce the opportunity cost of holding gold.” The report adds that since gold is priced in U.S. dollars, a weaker dollar could push gold prices higher, reports Bloomberg. A report from Norilsk Nickel says that global palladium demand is expected to increase 4 percent next year compared with 1 percent in 2019. According to the Union of Gold Producers in Russia, Russian gold production is expected to increase 6 percent to 350 tons in 2019.

- Silver’s gains are surpassing those of gold for a second straight week. The gold-to-silver ratio is still historically high, but is down from the 26-year record high in July, according to Bloomberg data. Commerzbank AG analyst Daniel Briesmann says that “from this point of view, silver seems to be too cheap and undervalued.” Barrick Gold announced that it has agreed to sell its entire stake in Australia’s Kalgoorlie Mine for $750 million – a big move toward selling non-core assets to raise more than $1.5 billion by the end of 2020. The stake was purchased by Saracen Mineral, which already owns two operations in the same region. CEO Mark Bristow of Barrick says that “the sale allows us to further focus our portfolio on core operations.”

- K92 announced strong drill results from its Kainantu gold mine in Papua New Guinea. The company recorded a drill hole of 288.73 grams per ton of gold and another hole of 107.55 grams per ton of gold. TriStar Gold also reported strong drilling results from its Castelo de Sonhos gold project in Brazil, including 24 meters at 1.1 grams per ton from 95 to 119 meters.

Threats

- Ray Dalio’s Bridgewater Associations has bet more than $1 billion that stock markets will fall by March, according to people familiar with the matter. The Wall Street Journal reports that there has been a surge in put options outstanding tied to the S&P 500 index, hitting the highest level in more than four years. This is a sign that more investors are becoming increasingly bearish on the market, especially ahead of the 2020 presidential elections.

- The world’s wealthiest investors are becoming more rattled and are looking for traditional security in the form of highly secured vaults. IBV International Vaults is opening its sixth location, this one in London, where the company will offer apartment-sized spaces for securing valuables. Swiss Gold Safe says it has seen extraordinary demand for safe-deposit boxes since it started offering them in 2015. Sincona Trading AG, a precious metals dealer in Zurich, said it had many empty safety deposit boxes three years ago, but now they are renting about five a day and will soon be full.

- According to Research Affiliates, value stocks are trailing growth at a rate that falls within the worst decile in history. The disparity between the two has only been larger twice before – during the global financial crisis and for more than a year at the peak of the dot-com bubble. Rob Arnott, co-founder of the firm, says that although value stocks have been frustrating investors for a decade, now is the wrong time to bail on them. Most gold stocks would be considered value stocks at current prices, while exploration and development companies border on deep value.

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 0.46 percent. The S&P 500 Stock Index fell 0.33 percent, while the Nasdaq Composite fell 0.25 percent. The Russell 2000 small capitalization index lost 0.47 percent this week.

- The Hang Seng Composite gained 0.95 percent this week; while Taiwan was up 0.36 percent and the KOSPI fell 2.79 percent.

- The 10-year Treasury bond yield fell 6 basis points to 1.773 percent.

Domestic Equity Market

Strengths

- Health care was the best performing sector of the week, increasing by 0.81 percent versus an overall decrease of 0.33 percent for the S&P 500.

- Target Corp was the best performing S&P 500 stock for the week, increasing 12.20 percent.

- The Buckle’s shares surged Friday after the clothing and accessories retailer’s fiscal-third quarter results beat expectations, driven by strong comparable-store sales growth. Buckle said revenue in the quarter ended November 2 rose to $224.1 million from $215.1 million in the prior year period. Shares of Buckle rose more than 17 percent in Friday trading, heading to the highest level since August of last year.

Weaknesses

- Materials was the worst performing sector for the week, decreasing by 1.69 percent versus an overall decrease of 0.33 percent for the S&P 500.

- Kohls Corp was the worst performing S&P 500 stock for the week, falling 20.45 percent.

- Pure Storage shares tumbled on Friday after the cloud-computing company gave a revenue outlook that was weaker than expected, with the results “pressured by pricing, again,” in the words of Morgan Stanley. Shares sank 20 percent and erased much of a recent gain. The sell-off represented the second time in the past three quarters when shares have greeted an earnings release with a pronounced decline.

Opportunities

- The launch of Apple TV+, coupled with Apple’s foray into digital services, could help the company increase its income from advertising by more than fivefold to $11 billion annually within the next six years. Analysts at JP Morgan say the company had the potential to raise revenue by a third every year, from an estimated $2 billion currently to $11 billion in 2025.

- Hibbett Sports shares surged in Friday trading after boosting its full-year forecast following better-than-expected third-quarter results. The company increased their full-year earnings per share range from $2.15 – $2.32 to $2.30 – $2.50.

- Cloud-based communications specialist Ooma reported earnings on Thursday night, covering the third quarter of fiscal year 2020. The company exceeded analyst expectations across the board and reported a small profit where Wall Street was expecting a loss. Investors loved these strong figures, sending share prices 24 percent higher by the end of Thursday’s extended trading session.

Threats

- Foot Locker cut its full-year comparable sales view on its quarterly earnings call. The company now sees comps up in low-single digits versus mid-single digit growth in August. The stock fell as much as 6.9 percent as the market opened.

- Marcus Corp. and Cinemark Holdings were cut at B. Riley FBR Friday as analyst Eric Wold projected “flattish” fourth quarter box office results and said he sees valuation for the movie theater operators pressured by box office trends until mid-2020.

- Venator Materials dropped as much as 8.1 percent, the most since October, after UBS analyst Joshua Spector cut the stock to neutral from buy, with a price target of $3.75, seeing a more balanced risk/reward.

The Economy and Bond Market

Strengths

- Consumer sentiment unexpectedly rose in November, according to data released Friday by the University of Michigan. The university’s index of consumer sentiment climbed to 96.8 from 95.5 last month. Economists polled by Dow Jones expected consumer sentiment to dip to 94.9 for November.

- IHS Markit said its U.S. flash manufacturing purchasing managers index (PMI) rose to 52.2 in November from 51.3 in October. This is the fastest rate since April. Meanwhile the U.S. flash services PMI in November rose to 51.6 from 50.6. This is the quickest expansion since July. “A welcome upturn in the headline index from the flash PMI adds to evidence that the worst of the economy’s recent soft patch may be behind us,” said Chris Williamson, chief business economist at IHS Markit.

- U.S. home sales increased more than expected in October and house prices rose at the fastest pace in more than two years amid lower mortgage rates and a shortage of properties for sale. The National Association of Realtors said on Thursday that existing home sales rose 1.9 percent to a seasonally adjusted annual rate of 5.46 million units last month.

Weaknesses

- A mixed bag of retail sales figures and weak factory numbers in the U.S. helped push a closely-watched gauge of economic surprises back into negative territory. The index from Citigroup Inc. — which falls when data prove worse than forecast – dropped below zero on Friday for the first time since early September. Renewed caution over the resilience of the U.S. economy has weighed on benchmark Treasury yields, which retreated to 1.83 percent last week after an early November surge brought them close to 2 percent.

- The Conference Board Leading Economic Index (LEI) for the U.S. declined 0.1 percent in October to 111.7, following a 0.2 percent decline in both September and August. "The U.S. LEI declined for a third consecutive month, and its six-month growth rate turned negative for the first time since May 2016. The decline was driven by weaknesses in new orders for manufacturing, average weekly hours, and unemployment insurance claims," said Ataman Ozyildirim, Senior Director of Economic Research at The Conference Board.

- The number of people who applied for jobless benefits clung to a five-month high in mid-November, likely reflecting seasonal swings in employment just before the start of the holiday season.

Opportunities

- The monthly home price index and the S&P CoreLogic Case-Shiller 20-City Composite are both out next Tuesday along with new home sales. Pending home sales will follow on Wednesday. With some signs of a pickup in the housing market, better-than-expected numbers next week would signal that the Federal Reserve’s three rate cuts are starting to lift the sector, taking some of the pressure off policymakers to lower rates further.

- The Conference Board’s consumer confidence gauge is due on Tuesday and the Personal Income and Outlays report is out on Wednesday. The consumer confidence index is forecast to edge up 0.9 points to 126.8 in November, holding within its recent range.

- On Monday the Ifo Business Climate index will be out of Germany. Recent business surveys for Germany and the Eurozone have provided some indication that the worst of the downturn may be over in the euro bloc, though they also suggest that a convincing rebound is far from near. Still, any further signs that growth is bottoming out could bolster sentiment.

Threats

- The second estimate of U.S. GDP growth in the third quarter is scheduled for release on Wednesday. A relatively weak preliminary reading of 1.9 percent annualized growth is expected.

- October durable goods orders will be released Wednesday and are forecast to show a deceleration of -0.7 percent.

- What may jolt investors more than data are new developments on the trade front. The latest press reports suggest U.S. and Chinese negotiators have hit a stumbling block on the issue of rolling back existing tariffs but that an agreement is still within reach. Resistance by the Trump administration to give ground on removing some of the tariffs already in place could spoil a deal and throw markets into fresh turmoil so investors will remain highly sensitive to the flashing headlines.

Energy and Natural Resources Market

Strengths

- The best performing major commodity for the week was coffee, which gained 5.47 percent on expectations of the market tightening, maybe shifting to a deficit, due to shrinking supplies from Brazil.

- Crude oil climbed to a nine-week high on Thursday after China signaled a renewed desire to resolve the trade war with the U.S. Although oil prices then fell on Friday morning, it still had a third straight weekly gain. The weekly Bloomberg survey found that analysts and traders were overall neutral on WTI crude futures for next week.

- Nickel prices have steadied after falling into a bear market, according to Citigroup analysts, as prices could climb in 2020 amid expectations of a deficit in the refined market. Major nickel producer Norilsk Nickel says it expects global demand to rise 5 percent in 2020, compared to 4 percent this year. However, the supply-demand deficit is set to shrink to 28,000 tons next year compared with 67,000 tons in 2019.

Weaknesses

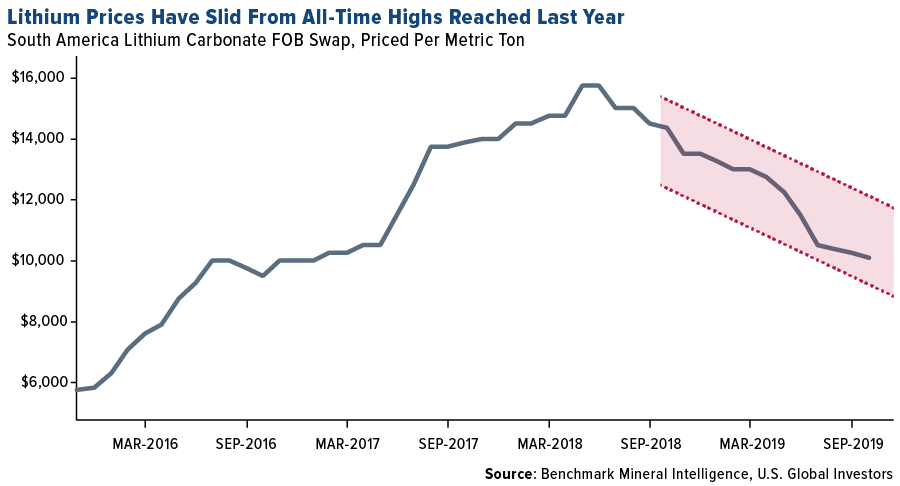

- The worst performing major commodity for the week was zinc, which fell 3.84 percent alongside other base and industrial metals. Chilean-based SQM, the world’s second largest lithium producer, expects prices for the metal to continue falling this quarter and through 2020. Bloomberg reports it is a big reversal from the company saying just two months ago that it was optimistic on lithium prices. SQM missed the lowest estimates for net income and revenue in the third quarter due to falling metal prices and lower sales volume.

- Copper production in China is hitting record highs even as the trade war drags on. Smelters produced 868,000 tons in October, topping the high set in December 2017 and up 17.9 percent on a daily basis from a year earlier, reports Bloomberg. China’s copper smelting fees have fallen to their lowest since 2011 and could indicate tighter supply. The weekly Bloomberg survey of copper traders and analysts found that they were split on outlook for prices due to conflicting signals on the prospects of a trade war deal. Bloomberg’s Eddie van der Walt writes that copper prices display more skepticism about the fate of the global trade war than equities do. Copper rallied more than 13 percent early this year on hopes of a deal, but then talk of a phase one trade deal only saw the metal rise by half as much.

- The long-awaited Saudi Aramco IPO was meant to attract billions of foreign capital to Saudi Arabia, but now it looks as if most of the investment will come from ultra-wealthy Saudis. The company is shunning New York and other international exchanges and won’t even market its IPO to American, Canadian, European or Japanese investors, reports Bloomberg. This means that major banks including Goldman Sachs and Morgan Stanley will miss out on fees from the share sale.

Opportunities

- The world’s largest lithium-ion battery power station, the Hornsdale site in South Australia operated by French company Neoen SA, will become even bigger due to an investment by Tesla. Neoen announced that the system will be expanded by 50 percent to 150 megawatts. Since installation in 2017, the battery has helped stabilize the area’s grid and prevent outages, reports Bloomberg. According to new research, average wind speeds rose 7 percent since 2010 in northern mid-latitude regions, which is excellent news for the wind power industry.

- Talk of a Rio Tinto takeover of Glencore arose again after top Glencore executives visited Australia last week. The Financial Review reports that a merger between the two mining giants would create huge opportunities for synergies and could help Glencore rise to the strong operational record of Rio. Glencore’s CEO Ivan Glasenberg has advocated that there would be a positive trade off from Rio cutting its annual iron ore production by 30 million tonnes because it would boost prices significantly.

- Bloomberg Law reports that, starting next year, builders in California’s Marin County will have to use concrete with low greenhouse gas emissions when developing public and private structures. This is the nation’s first such ordinance to tackle the reduction of pollution from concrete, as many building standards have tackled other issues such as greener wiring, lighting and power. According to Chatham House, the manufacturing of cement accounts for 8 percent of worldwide man-made carbon dioxide emissions.

Threats

- The $146 billion lubricants industry is at risk of becoming obsolete due to the rise of electric vehicles. Carmakers are switching to battery-powered vehicles that use less grease than combustion vehicles. Bloomberg reports that demand is expected to decline from 2025 and lubricant makers are wary of Eastman Kodak’s demise when it failed to grasp the potential of digital cameras.

- According to the Production Gap Report backed by the U.N., natural gas, oil and coal supplies in 2030 are set to be more than double the levels consistent with limiting global warning to 1.5 degrees Celsius as set in the Paris Agreement. Michael Lazarus, lead author of the report, says that “this report shows, for the first time, just how big the disconnect is between Paris temperature goals and countries’ plans and policies for coal, oil and gas production.” According to Global Energy Monitor, China has almost 148 gigawatts of coal-fired capacity under active construction or likely to be resumed – almost equivalent to the 150 gigawatts of existing coal fleet capacity in the entire EU.

- The outlook for American shale producers continues to worsen. Bloomberg Reports that Laredo Petroleum Inc. and Oasis Petroleum Inc. are among at least six producers whose ability to secure short-term loans against their oil and natural gas reserves have dropped by 10 percent or more. At least 15 producers have filed for bankruptcy this year and market values are down at least 21 percent so far in 2019.

Emerging Europe

Strengths

- Hungary was the best performing country this week, gaining 1.5 percent. The central bank kept its rates unchanged at a record low level despite the Hungarian forint weakening and core inflation moving higher. Hungary is the fastest growing economy in central Europe with GDP growing at 5 percent.

- The Turkish lira was the best performing currency this week, gaining 60 basis points. Stronger economic data supported the lira in the past five days. Consumer confidence improved in the month of November and foreigners’ net bond and stock investments are on the rise.

- Health care was the best performing sector among eastern European markets this week.

Weaknesses

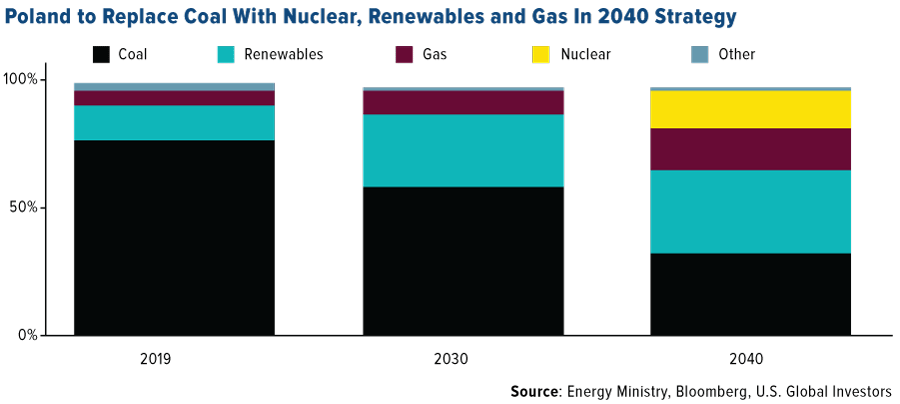

- Poland was the worst performing country this week, losing 1.5 percent. Some polish state-controlled equites trading on the Warsaw exchange were under pressure this week after the government confirmed its move to go ahead with the long planned $60 billion nuclear power plant project. The scale of the project may be a burden for utilities and some companies might be asked to help finance the project. The financing details will be set over next few months.

- The Polish zloty was the worst performing currency in the region this week, losing 80 basis points. Domestic political noise put pressure on the currency. There is some reshuffling in the government after last month’s parliamentary elections.

- Consumer staples was the worst performing sector among eastern European markets this week.

Opportunities

- Minutes from the last ECB’s meeting under Mario Draghi revealed that he called for more unity among members and signaled readiness to use full sets of instruments to support the euro economy. Activity data released since the October meeting has been improving. GDP growth was 0.2 percent for the EU in the third quarter, above the ECB forecast of 0.1 percent, largely driven by expansion in Germany. Preliminary November manufacturing PMI data released on Friday came out stronger as well, indicating a possible turnaround.

- According to the central bank’s chief forecaster in Poland, Piotr Szpunar, the nation’s economy will not be derailed by a global slowdown or smaller inflows of cash from the European Union. Growth in Poland will slow down from 4.3 percent to 3.3 percent next year; however, it will remain one of the strongest in central Europe supported by an increase in social spending and a minimum wage hike boosting consumption. Moreover, despite the record low unemployment, Poland still has the EU’s fifth’s cheapest hourly costs.

- The Cornerstone Macro research team predicts Germany GDP to increase to 1 percent year-over-year by the fourth quarter of 2020. They also believe that the sentiment is too depressed and will improve as auto production is stabilizing, the inventory drag is ending, a U.S.-China trade truce is approach and Brexit is likely to be soft.

Threats

- Morgan Stanley in “Moscow talks” wrote that the number of delinquencies of loans among Russian consumers increased year-to-date by 4 percent. According to the study conducted by the professional collector association, one in four borrowers of Russian banks has delinquencies of their loans that exceed three months.

- Moody’s cuts its German banking outlook to negative from stable amid weaker profitability. It expects banks’ profitability and overall creditworthiness to weaken over the next 12 to 18 months amid the low interest rate environment. It sees traditional commercial banks, and in particular deposit-funding institutions, to struggle to out-earn their costs, even though loan-loss provisions are unsustainably low. On the positive side, it noted that debt repayment capacity of borrowers will remain high amid low rates, a strong labor market and buoyant domestic demand.

- Equites trading on the Istanbul exchanged moved higher, supported by stronger economic data. However, domestic political noise increased in the past few days. Turkey’s pro-Kurdish opposition party (HDP) called on Wednesday for an early election, but ruled out withdrawing from the parliament to protest the government dismissal of HDP’s majors mainly due to links to terrorism. HDP is the only party in the parliament which opposed Turkish incursion into northern Syria on October 9.

China Region

Strengths

- The best performing index in the region was Hong Kong’s Hang Seng Composite Index, which bounced up by 95 basis points following a tough week last week.

- Information Technology was the top performer the Hang Seng Composite on the week, climbing 2.74 percent.

- China’s October reading on year-over-year FDI rose to 7.4 percent, up from the prior reading of 3.8 percent.

Weaknesses

- The worst performing indices in the region were Vietnam’s Ho Chi Minh Stock Index, which fell by 3.18 percent, and China’s Shanghai Composite, which declined by 2.79 percent.

- Energy was the worst performing sector in the HSCI on the week, falling 34 basis points in that time.

- Thailand’s year-over-year third quarter GDP reading came in at 2.4 percent, shy of expectations for a 2.7 percent reading, but still up mildly from the prior reading of 2.3 percent.

Opportunities

- A Phase One U.S.-China trade deal remains an opportunity, with the latest updates on the week being that the U.S. and China are reportedly “close,” according to President Trump, and that China would “like” to make a deal, but that Hong Kong appears to be increasingly problematic. Markets still appear to remain reasonably optimistic that a deal of some kind is more likely than not, and given that the two sides remain in close conversation with invitations for further talks on the table and a December 15 deadline incentivizing serious discussion, perhaps no “big” news is good news for the moment.

- After nearly 10 years of talks, the European Union and Singapore have formally completed their free trade agreement this week. Bloomberg News reports that the EU is Singapore’s third-largest goods trading partner, while Singapore is the EU’s largest goods trading partner within ASEAN.

- Alibaba raised some $11 billion from its new Hong Kong listing, despite the hullabaloo around the troubled city and amid ongoing protests. The Chinese ecommerce and tech juggernaut, flush with cash, may well be the first of several U.S.-listed ADRs from China that could seek an eventual listing in HK, especially if U.S. political pressure and rhetoric develops into actual economic restrictions or threats of such on portfolio flows into said ADRs. Alibaba’s listing also, of course, gives it a larger war chest and edge in assessing other opportunities and supporting its existing ventures.

Threats

- In keeping with this section’s views, we once again reiterate that trade war escalation must remain a threat until it isn’t. While there remains a degree of optimism in the U.S.-China trade tiff at the moment and while the two sides are engaged in reportedly constructive talks, there remain a number of sturdy sticking points, even for what is supposedly on the table around “Phase One.” Agricultural purchases and their speed and scope seem to loom as large as ever, and while supposedly the two sides are going “retro” and reaching back toward the near-agreement of May when there was reportedly some sort of consensus, the thorny issues of whether and how tariffs can be rolled back—whether roll-backs might be “earned” according to progress, etc., or whether a deal might simply hold off new tariffs—still complicate matters (so far as we know). And of course, there is the matter of Hong Kong…

- The situation in Hong Kong continues to remain a thorny one as well, with elections in the special administrative region looming tomorrow amid ongoing threats of protests or possible disruptions. Carrie Lam’s government is attempting to reinstitute the ban on masks heading into the elections. U.S. President Donald Trump has come out and said that China would like to roll in to Hong Kong, and Congress did pass S. 1838 this week, sending the bill to President Trump’s desk and ramping up pressure all around. President Trump has said he “stands” with Hong Kong, and U.S. Secretary of State Mike Pompeo called on Carrie Lam to permit an independent probe into the protest incidents, saying the U.S. is “gravely concerned” with the rising violence in the city. Protestors holed up in Hong Kong Polytechnic University remain in a stand-off situation heading into the weekend, and riot police are expected to guard poll booths at the upcoming elections.

- The U.S. dollar strengthened again on Friday, taking back much of last week’s decline. A rising dollar could pressure emerging market assets, and although the dollar remains off its highs, still at this point nonetheless remains worth watching carefully.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended November 22 was MMOCoin, up over 9,000 percent.

- Grayscale Investments is filing to register its Bitcoin Trust as a Securities and Exchange Commission (SEC) reporting company, writes CoinDesk. If the Form 10 filing is deemed effective by the U.S. regulator, the trust’s shares would be registered under the Exchange Act of 1934, the article explains, potentially making it the first cryptocurrency investment vehicle to become a reporting company.

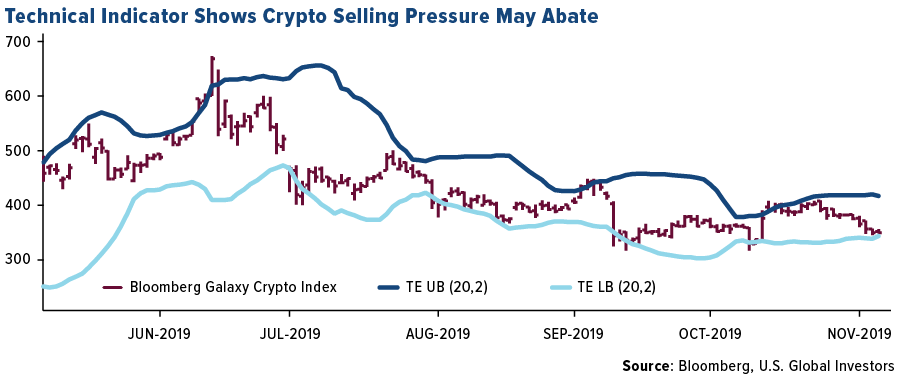

- Despite a sell-off in cryptocurrencies, Bloomberg reports that at least one technical indicator is “painting a brighter picture.” The Bloomberg Galaxy Crypto Index, which tracks a basket of the largest digital assets, is nearing its lower limit, the article explains, potentially signaling that selling pressure may dissipate and a short-term rally could ensue.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended November 22 was ETHplode, down 48.89 percent. CNBC reported that a bipartisan team of senators introdocued a bill that would make Facebook’s libra a security under the law. Facebook has insisted that the libra is a digital payments system. Being classified as a security will likely draw increased regulation and scrutinity to the project.

- A handful of technical indicators are pointing to further pain ahead for bitcoin, reports Bloomberg, as the coin’s recent sell-off accelerates. On Monday, the price tested the key level of $8,000 as the price dropped as much as 5 percent. In addition, bitcoin bounced off its 200-day moving average line, the article continues, a drop below it could trigger a sell signal.

- Top crypto exchange Binance has made a move into India’s huge cryptocurrency market (although slightly troubled), with the acquisition of the WazirX exchange platform, reports CoinDesk. To get around the banking issues, Binance launched Indian rupees on its Binance Fiat Gateway in recent weeks. “The acquisition of WazirX shows our commitment and dedication to the Indian people and strengthen the blockchain ecoysystem in India as well as another step forward in achieving the freedom of money,” said CEO Changpeng Zhao.

Opportunities

- Michael Novogratz’s Galaxy Digital Holding Ltd. is starting two bitcoin funds for accredited and institutional investors, writes Bloomberg, with a demographic profile that hits close to home. In a phone interview, Novogratz explained that the funds will target the “wealth of America,” or more specifically, people between 50 and 80 who may have stayed largely on the sidelines of cryptocurrency investing.

- The first blockchain-based airline tickets were issued this week. German airline Hahn Air flew passengers with blockchain-powered tickets on a routine flight between Dusseldoft and Luzemborg, reports Retuers. The airline partnered with Winding Tree, an open-source travel distribution platform, to issue the tickets. Hahn Air head of corporate strategy and government and industry affairs Jorg Troester said “it is important to look into the future to understand how can we make distribution faster.”

- According to CCN.com, Singapore’s central bank could soon authorize the trading of derivatives referencing cryptocurrency assets such as bitcoin. The move to license crypto derivatives stems from a demand for well-regulated crypto derivative products, per the central bank.

Threats

- According to CoinDesk, the Internal Revenue Service (IRS) is focusing on potential illicit activities facilitated by bitcoin ATMs and cryptocurrency kiosks, specifically their potential for tax evasion or money laundering. John Fort, the IRS’ criminal investigation chief, commented that generally, U.S. operators provide know-your-customer and anti-money laundering verifications of users as required by law. However, “we believe some have varying levels of adherence to those regulations,” Fort said.

- Maksim Zaslavskiy’s two fraudulent investment schemes, primarily taking place during the 2017 ICO boom, has landed the Brooklyn businessman in federal prison for 18 months for conspiring to commit securities fraud, reports CoinDesk. Zaslavskiy sold investors asset-backed tokens for two companies, however the underlying assets of the tokens did not exist.

- On Wednesday, well-known statistician and analyst Willy Woo delivered his latest analysis on what’s next for the price of bitcoin. The price of BTC has almost reached its bottom for 2019, Woo explained, but the threat still remains for markets to hit $4,500. As reported by CoinTelegraph, Woo and trader Tone Vays say this cycle could see a drop of around 71 precent versus the highs of $12,800 seen several months ago – putting bitcoin at $4,500 before next May’s block reward halving event.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| 10-Yr Treasury Bond | 1.77 | -0.06 | -3.22% |

| Oil Futures | 58.02 | +0.30 | +0.52% |

| Hang Seng Composite Index | 3,607.94 | +33.79 | +0.95% |

| S&P Basic Materials | 371.93 | -6.39 | -1.69% |

| Korean KOSPI Index | 2,101.96 | -60.22 | -2.79% |

| S&P Energy | 438.15 | -2.28 | -0.52% |

| Nasdaq | 8,519.89 | -20.94 | -0.25% |

| DJIA | 27,875.62 | -129.27 | -0.46% |

| Russell 2000 | 1,588.94 | -7.51 | -0.47% |

| S&P 500 | 3,110.29 | -10.17 | -0.33% |

| Gold Futures | 1,468.80 | -6.60 | -0.45% |

| XAU | 93.66 | +0.05 | +0.05% |

| S&P/TSX VENTURE COMP IDX | 530.02 | +1.44 | +0.27% |

| S&P/TSX Global Gold Index | 241.01 | +1.44 | +0.60% |

| Natural Gas Futures | 2.66 | -0.02 | -0.93% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Korean KOSPI Index | 2,101.96 | +21.34 | +1.03% |

| 10-Yr Treasury Bond | 1.77 | +0.01 | +0.45% |

| Gold Futures | 1,468.80 | -33.90 | -2.26% |

| S&P Basic Materials | 371.93 | +11.69 | +3.25% |

| S&P 500 | 3,110.29 | +105.77 | +3.52% |

| DJIA | 27,875.62 | +1,041.67 | +3.88% |

| Nasdaq | 8,519.89 | +400.09 | +4.93% |

| Oil Futures | 58.02 | +2.05 | +3.66% |

| Hang Seng Composite Index | 3,607.94 | +25.84 | +0.72% |

| S&P/TSX Global Gold Index | 241.01 | +6.18 | +2.63% |

| XAU | 93.66 | +3.66 | +4.07% |

| Russell 2000 | 1,588.94 | +36.09 | +2.32% |

| S&P Energy | 438.15 | +0.79 | +0.18% |

| S&P/TSX VENTURE COMP IDX | 530.02 | -13.02 | -2.40% |

| Natural Gas Futures | 2.66 | +0.38 | +16.70% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| XAU | 93.66 | -0.34 | -0.36% |

| S&P/TSX Global Gold Index | 241.01 | -10.94 | -4.34% |

| Gold Futures | 1,468.80 | -45.50 | -3.00% |

| DJIA | 27,875.62 | +1,623.38 | +6.18% |

| S&P 500 | 3,110.29 | +187.34 | +6.41% |

| Nasdaq | 8,519.89 | +528.50 | +6.61% |

| Korean KOSPI Index | 2,101.96 | +137.31 | +6.99% |

| Natural Gas Futures | 2.66 | +0.50 | +23.34% |

| S&P Basic Materials | 371.93 | +19.81 | +5.63% |

| Russell 2000 | 1,588.94 | +82.94 | +5.51% |

| Oil Futures | 58.02 | +2.67 | +4.82% |

| Hang Seng Composite Index | 3,607.94 | +109.98 | +3.14% |

| S&P/TSX VENTURE COMP IDX | 530.02 | -48.08 | -8.32% |

| S&P Energy | 438.15 | +13.13 | +3.09% |

| 10-Yr Treasury Bond | 1.77 | +0.16 | +9.78% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (09/30/2019):

MMC Norilsk Nickel PJSC

Alacer Gold Corp

AngloGold Ashanti Ltd

Barrick Gold Corp

K92 Mining Inc

TriStar Gold Inc

The Boeing Co.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

Bloomberg and Galaxy Digital Capital Management launched the Bloomberg Galaxy Crypto Index (BGCI). The index is designed to measure the performance of the largest cryptocurrencies traded in USD. The BGCI is market capitalization-weighted and includes cryptocurrencies such as Bitcoin, Ethereum, Monero, Ripple and Zcash. The Consumer Confidence Survey reflects prevailing business conditions and likely developments for the months ahead. The Conference Board Leading Economic Index is a composite economic index constructed to summarize and reveal common turning point patterns in economic data. The Ifo Business Climate Index is a closely followed leading indicator for economic activity in Germany prepared by the Ifo Institute for Economic Research in Munich, Germany. S&P/Case-Shiller U.S. National Home Price Index tracks the value of single-family housing within the United States. The index is a composite of single-family home price indices for the nine U.S. Census divisions. The Vietnam Stock Index or VN-Index is a capitalization-weighted index of all the companies listed on the Ho Chi Minh City Stock Exchange. The Shanghai Stock Exchange Composite Index is a capitalization-weighted index. The index tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange.