When Will Business Travel Recover? Sooner Than You Might Think

Date Posted: June 18, 2021

Read time: 50 min

Two million people boarded scheduled flights in the U.S. yesterday, a more than 150% improvement from where we were at the beginning of the year. Leisure travel is mostly back as California and New York reopen their economies and as the European Union (EU) formally adds the U.S. to its list of countries approved for entry.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

Two million people boarded scheduled flights in the U.S. yesterday, a more than 150% improvement from where we were at the beginning of the year. Leisure travel is mostly back as California and New York reopen their economies and as the European Union (EU) formally adds the U.S. to its list of countries approved for entry.

It’s appropriate, then, that the U.S. Global Jets UCITS ETF (JETS) launched this week on the London Stock Exchange (LSE), giving U.K. and European investors access to the global airlines industry. I’m excited to say that this marks the second time this year that U.S. Global Investors has expanded its product line to international markets, the first case being in April when our airlines ETF debuted on the Mexican Stock Exchange (BMV).

The offering comes thanks to our partnership with HANetf, Europe’s first independent full-service provider of UCITS, or Undertakings for Collective Investment in Transferable Securities. UCITS can be registered in Europe and offered to investors throughout the EU. Once approved, they become exempt from regulation in individual countries.

I’m confident the UCITS ETF will meet overseas investors’ demand for a product that seeks to track the global economic reopening.

Cautiously Optimistic on Business Travel

In terms of reopening, the two big holdouts continue to be Canada (more on that later) and business travel. The difference between the two is that we’re seeing steady improvement with the latter—domestically, anyway.

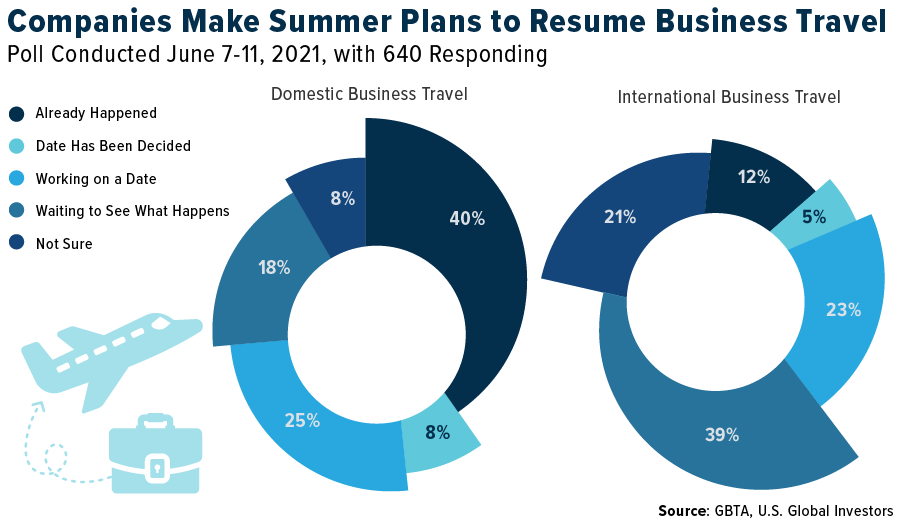

A poll conducted this month among members of the Global Business Travel Association (GBTA) showed that domestic business travel is well on its way to recovery. Forty percent of respondents said that business travel within the country where their firm is based has already resumed, while a third said that their company has either decided on a start date or is working toward a date. Only 18% said that their company was “waiting to see what happens.”

International business travel is another story. Only 12% of respondents said business travel outside of the country where their company is based has resumed, a sign that we still have a long way to go yet.

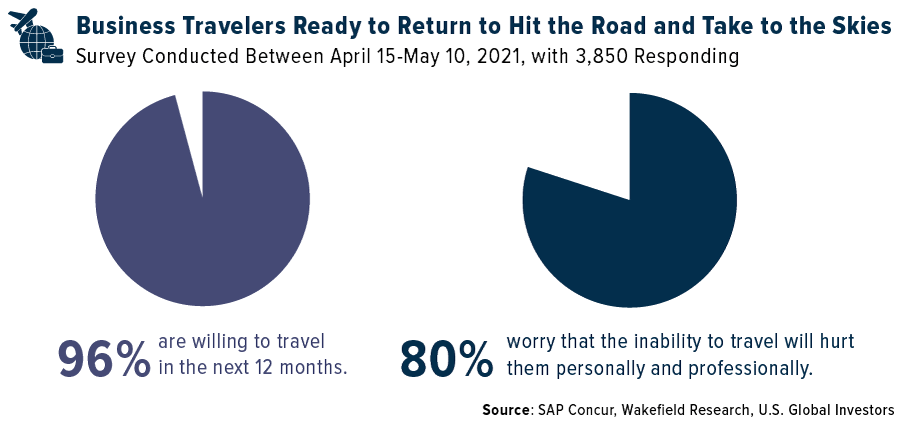

Some companies’ hesitancy to resume business travel, though—particularly on the domestic side—is not in alignment with the results of another survey, which show that a vast majority of workers are more than ready to hit the road and take to the skies again.

According to SAP Concur’s Global Business Travel Report 2021, released this week, a whopping 96% of global business travelers said they were willing to start traveling again in the next 12 months. And with good reason: 80% said they were worried that the inability to travel could hurt them not just professionally but also personally.

As many of you reading this know, there’s no replacement to meeting clients and colleagues in person and attending live professional meetings and events (PMEs). Zoom fatigue is real, for women more so than men. Companies from Google to WeWork are working on introducing accessible holographic technology to be used in the office, but right now it’s expensive, and I suspect the “creepy” factor will lead to strong resistance.

Ohio State University: Little Risk in Meetings and Events

Besides, more and more research continues to come out that meeting people in person and attending live events poses little risk if common sense precautions are observed. A new paper by a team of health care scientists with the Ohio State University makes the case that a return to PMEs is “inherently possible in the current environment.” The team studied a number of PMEs that took place during the pandemic and found that, as long as safety precautions were observed, they ended up not being so-called super-spreader events.

“By setting standards to balance public health measures with meeting face to face, PMEs can help in a return to social interactions and networking,” the researchers write, adding: “As more of the population is fully vaccinated, these risks are further reduced.”

A good case study is the recent Bitcoin 2021 conference in Miami. An estimated 12,000 people from all over the world were in attendance. Some attendees reportedly tested positive for the virus, but the conference did not become the super-spreader event many people feared it would be.

Will Canada Finally Open Its Borders?

Again, California and New York—the number one and number three largest states by GDP—lifted nearly all restrictions this week as the share of residents who have received at least one vaccine dose surpassed 70%.

This is hugely positive, as both states were among the earliest and hardest to be hit by the virus.

It’s now time for the U.S.-Canada border to reopen to non-essential travel. The border is the longest in the world at 5,525 miles, and for every month that it remains closed, the U.S. economy loses $1.5 billion in potential travel exports, according to the U.S. Travel Association. That’s enough to support many thousands of American jobs.

The current restrictions, which have been in place since March 2020, were originally set to expire this coming Monday, but today they were extended for at least another month, all but guaranteeing another lost summer to travel and tourism.

This decision is not consistent with the science. Supposedly, Canada has rocketed past Israel in terms of the share of people who have received at least one dose. If things are going so well, why has the border not been reopened?

It’s against this backdrop that the Canadian Parliament continues to debate the controversial C-10 bill, which many worry would give the government the power to regulate the content that Canadians post on social media.

Register Today

I’ll have much more to say about travel trends next week during a webcast with Connor O’Brien, CEO of O’Shares ETFs. Connor and I will discuss the reopening of global economies, and what that means for airlines and e-commerce. I’m looking forward to it, and I hope you’ll join us!

Register for the webcast, to be held at 11:00am EST on Thursday, June 24, by clicking here.

Index Summary

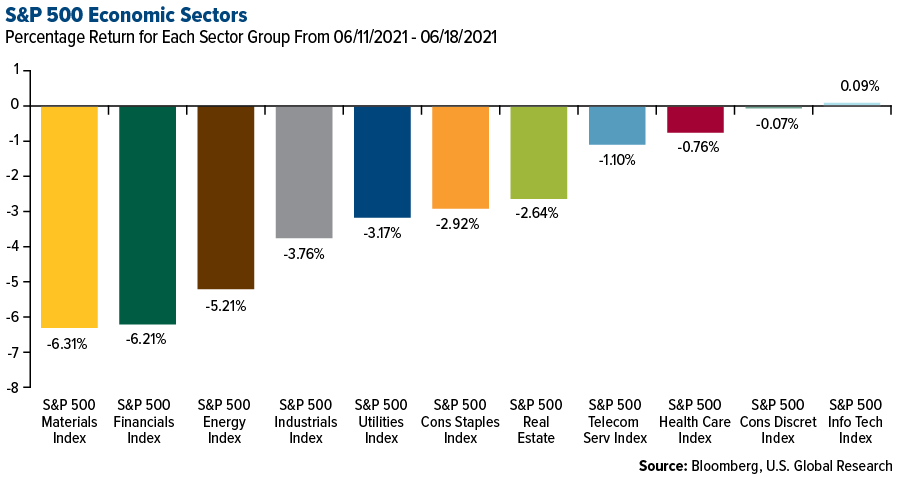

- The major market indices finished down this week. The Dow Jones Industrial Average lost 3.45%. The S&P 500 Stock Index fell 1.91%, while the Nasdaq Composite fell 0.28%. The Russell 2000 small capitalization index lost 4.20% this week.

- The Hang Seng Composite lost 0.85% this week; while Taiwan was up 0.61% and the KOSPI rose 0.57%.

- The 10-year Treasury bond yield fell 1 basis point to 1.44%.

Airline Sector

Strengths

- The best performing airline stock for the week was Bangkok Airways, up 19.3%. According to Bank of America, daily website visits for European airlines increased significantly in the week ending June 8, up by 7% to around 36% of 2019 levels. Air France, Iberia Airlines and Turkish Air are close to 2019 levels. Web traffic for U.S. carriers is now down only 5% compared to 2019 levels, according to ISI.

- According to Credit Suisse, Swiss voters voted down a trio of environmental proposals on Sunday, including the CO2 law. Although the vote is unfortunate in the sense that this makes it very difficult for Switzerland to meet its 2030 goal of cutting emissions, it should come as a relief to airlines most exposed to negative demand impacts coming from this region. A Reuters article notes that 51.6% of voters rejected the motion.

- According to Raymond James, airline fares are up 5% over the past week. Spirit Airlines (up 18%) and JetBlue (up 16%) are showing the best gains so far. Fare increases are likely to continue in the future as passenger counts continue to climb.

Weaknesses

- The worst performing airline stock for the week was Air Berlin, down 26.9%. Air Canada announced a 30-day extension to its COVID-19 refund policy. This allows eligible customers who purchased a non-refundable ticket before April 13, 2021, for travel on or after February 1, 2020, but did not fly for any reason, to receive a full cash refund. With the announcement, the deadline has been extended to July 12, 2021. Air Canada also noted that 40% of eligible customers have requested a refund, implying that the remaining 60% are undecided. Refunds have a significant impact on an airline’s cash flow and cash levels.

- Chinese air traffic demand appears to be slowing. The weekly volume index fell 42% versus 2019 levels, which is worse than the -34% in the previous week. Domestic volume fell 18% versus 2019 levels, as opposed to a 14% drop in the previous week. The Chinese economy has been slowing in recent months, with declining credit growth.

- International Airlines Group (parent to British Airways) and easyJet stocks fell during the week as the U.K. elected to delay its economic reopening by one month due to the COVID Indian variant. The decision will be reassessed in one month.

Opportunities

- Bookings through online ticket agencies are up 5% versus 2019 levels this week, which is an increase of 8.4% from the previous week. The strength appears to be concentrated in leisure markets. International tickets are also improving, down 44% versus 2019 levels, which is an improvement from down 51% the week before.

- According to Bank of America, during the G7 summit, the U.K. and the U.S. set up a new taskforce that will assess how to safely re-open transatlantic travel between the two countries. The Biden administration is also setting up an expert group with the European Union (EU) to reduce travel restrictions, although airlines do not expect any changes before July 4. Meanwhile, France and Spain launched their digital COVID certificates last week which should allow frictionless travel within the EU, joining seven other EU countries.

- According to Morgan Stanley, the CDC moved 61 countries down from its highest "Level 4" rating (which discourages all travel) and moved an additional 50 countries and territories down to "Level 2" and "Level 1." These changes occurred after the CDC revised its criteria for travel health notices, which included a revised rating for the U.S. to "Level 3" from "Level 4." While testing and quarantine requirements are still in place for some of these destinations, the easing in travel restrictions offers hope that there is light at the end of the tunnel for international travel.

Threats

- According to Goldman, corporate travel may return to pre-COVID levels in two years. Southwest Airlines has said that corporate travel is down 77% in its most recent data. This trend has been witnessed by all major carriers worldwide.

- Global restrictions remain high, at 85% of total routes, according to UBS. G20 travel restrictions continue to affect 94% of routes. These restrictions are preventing international demand from returning to pre-COVID levels.

- Lufthansa is planning an equity raise (3-4 billion Euro for a company with a 6 billion Euro market cap) and asset disposals to reduce leverage. While reducing leverage is a positive for the airline, as balance sheets have been stretched in recent years, the equity raise has the potential to be dilutive to existing shareholders.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Romania gaining 0.76%. The best performing country in Asia this week was Taiwan, gaining 0.61%.

- The Brazilian real was the best performing currency this week, gaining 0.70%.

- Industrial production continues to improve in Europe. It strengthened by 39.3% in April year-over-year and 0.80% month-over-month. Looking at the individual economies’ available data, industrial output expanded in 12 countries, while it contracted in five countries.

Weaknesses

- The worst relative performing country in emerging Europe for the week was Turkey, losing 4.78%. The worst performing country in Asia this week was Pakistan, losing 0.14%.

- The Hungarian forint was the worst performing currency this week, losing 4.07%.

- China released weaker activity data than previously predicted: May industrial production was up 8.8% year-over-year versus consensus of an increase of 9.2% (and 9.8% in the prior month), retails sales increased 12.4% versus consensus of a 14.0% increase (and 17.7% in the prior month), fixed asset investment rose 15.4% year-to-date versus consensus 17.0% (and 19.9% in the prior month).

Opportunities

- President Biden and European Union leaders reached a deal Tuesday to put to rest a 17-year-old trade dispute about subsidies for aircraft manufacturers. The U.S. imposed $7.5 billion in tariffs on European exports in 2019 after the World Trade Organization ruled that the EU had not complied with its rulings on subsidies for Airbus. This year, there appears to be less threat of further tariffs and more possibility of working toward a common goal of creating peace and prosperity.

- More than half the money that flowed into European funds last year went into sustainable products, according to the Association of the Luxemburg Fund Industry, which represents the region’s biggest fund market. European ESG (Environmental, Social and Governance) funds hit a record high of $1.4 trillion in assets last year, more than doubled since 2018. Companies are focusing on ESG credentials as Europe is rolling out a historic package of new regulations designed to divert financing away from businesses that hurt the environment.

- Europe is opening to Americans and other visitors after more than a year of COVID-19 travel restrictions. This will bring back tourists and their money to the EU’s 27 member states, effectively driving the service sector higher. But travelers will need to be patient in the process of figuring out who is allowed into which country, how, and when.

Threats

- Resurgent concerns about the health of the China Evergreen Group have pushed its stock price to the lowest level since March of 2020. Evergreen is a Chinese private real estate company with 1.95 trillion yuan ($305 billion) of liabilities, the world’s most indebted real estate company and one of the most systematically important borrowers in China; the company recently missed payments at the developer’s affiliates. Is it too big to fail? The fate of this company may depend on whether Chinese authorities allow banks to keep funding it.

- Meetings between U.S. President Biden, Turkish President Erdogan, and Russian President Putin failed to produce a breakthrough that would ease political tensions. The Turkish lira once again declined against the dollar as Erdogan indicated that he won’t change his stance on its purchase of Russian S-400 missile systems.

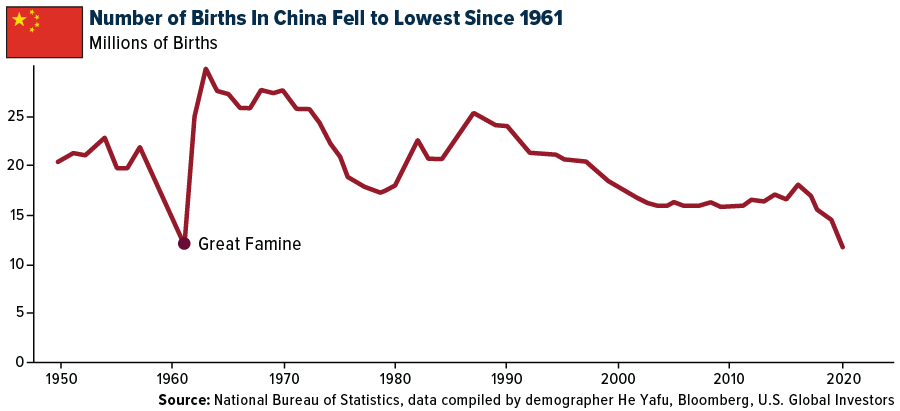

- Number of births in China fell to lowest since 1961; the Chinese government’s recent change with respect to child policy allowing families to have three children will have a short-lived effect. China also faces the dilemma of an aging population. To slow the decline in workforce, China had announced plans to gradually raise the national retirement age in the next few years.

Energy and Natural Resources Market

Strengths

- The best performing commodity for the week was iron ore, up 1.19%. Iron ore rebounded this week as China’s record steel output overshadowed the nation’s campaign to crackdown on commodity prices.

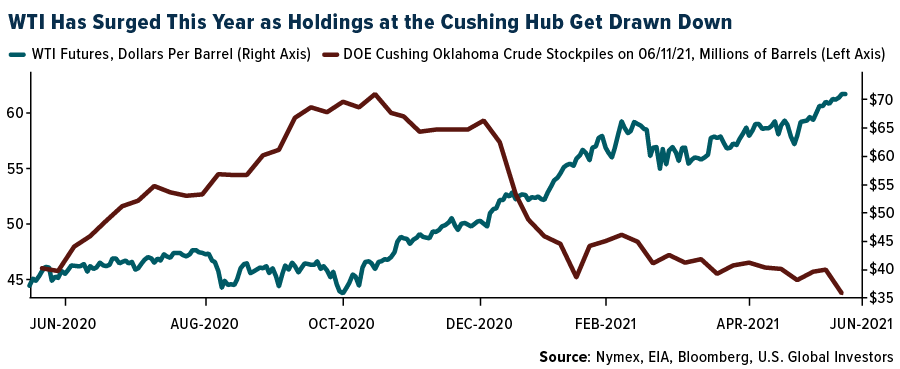

- West Texas Intermediate (WTI) crude traded near $72 a barrel, before paring gains and settling around $71.65, while Brent crude settled around $73.40 after rallying to $74.96 per barrel. This week, the U.S. Federal Reserve announced that it would begin talks on tapering asset purchases and expects to see two rate hikes by the end of 2023, aiding a rally in the U.S. dollar which hurt the appeal of commodities priced in the currency. Additionally, the U.S. government reported that domestic crude stockpiles have been sinking as refinery demand picks up. Citigroup Inc. noted that the outlook for the oil markets remain positive and expects Brent to top $80 a barrel soon on the back of pent-up leisure demand, which is being enabled by vaccine rollouts. The chart below shows the rising price of WTI against the drop in U.S. crude stockpiles over the past year.

- The U.S. shale industry is expected to generate more than $30 billion of free cash this year, which will be a record amount according to Bloomberg Intelligence. Although it is just a tiny blip compared to the $300 billion the sector has spent over the last decade, as estimated by Deloitte LLP, it could indicate a turning point in an industry that was largely written off by investors when the pandemic hit. This record amount is not only attributed to the 50% gain in global oil prices, but the ability of the industry to hold back on new supply, avoid drilling more marginal wells, and cutting costs across the board. The record amount of free cash will allow the industry to reduce its debt levels and still have enough cash to reward the shareholders.

Weaknesses

- The worst performing commodity for the week was lumber, down 16.92%. The selloff in lumber is seen as a seasonal dip as traders expect weakness until mid-to-late July.

- Some commodities have seen their year-to-date gains wiped out, while several more are close to doing so. Soybean futures are down more than 20% from an eight-year high reached in May, corn and wheat futures have also tumbled from multiyear highs, while copper, nickel, sugar and even lumber have pared their 2021 gains. The Bloomberg Commodity Index is set for its worst week since the start of the pandemic, with the decline being attributed to China’s efforts to slow inflation and curb the commodities rally, and the U.S. Federal Reserve’s signal for two interest-rate increases by 2023. Additionally, the U.S. dollar extended its gain this week, making commodities less appealing to investors that hold other currencies, and a big backwardation in many commodities and seasonality accounted for some of the recent slump as future contracts rolled over.

- Gazprom PJSC, which is the world’s largest producer of natural gas, is under scrutiny as the geo-analytics firm Kayrros SAS identified an enormous methane leak at its pipeline in Russia’s Tatarstan region. Gazprom reported that its pipeline repairs on June 4 released 1,830 metric tons of methane, which has roughly the same short-term planet-warming impact as 40,000 internal-combustion cars driving for a year. Kayrros added that its analysis estimates an emission rate of 395 metric tons per hour, making Gazprom responsible for the most severe release of methane from the oil and gas sector since September 2019.

Opportunities

- The global head of carbon trading at Trafigura Group, Hannah Hauman, believes that the carbon market has the potential to be 10 times the size of the global crude oil market, while at the FT Commodities Global Summit this week. This bullish outlook is also shared by commodities traders around the world as global leaders take stronger actions to limit climate change. This year alone, the European Union’s (EUs) carbon market, the world’s largest, has seen the price of one metric ton of carbon rise by 60%. Ulf Ek, the founder, and chief investment officer at Northlander Commodity Advisors LLP, said that the current price of carbon is still seen as too low by the EU regulators and that a higher price is needed for the bloc to realize its goal of reaching net zero emissions by the middle of the century.

- Russian metals giant MMC Norilsk Nickel PJSC (Nornickel) is set to begin offering exchange-traded commodities (ETCs) for nickel and copper on the London Stock Exchange (LSE) amidst a growing interest in ETCs, which offer investors exposure to the underlying commodity without investing directly in the spot or derivatives markets. Nornickel’s sales chief, Anton Berlin, said this week that new digital instruments provide great opportunities to investors to benefit from rising demand for base metals, and noted that the ETCs would be the first physically backed nickel and copper exchange-traded products. Issued through Nornickel’s Global Palladium Fund, the ETCs would be the first ever to utilize blockchain distributed-ledger technology to record purchasing information.

- Jeff Currie, Goldman Sachs’ head of commodities research, sees the latest selloff in commodities as a buying opportunity. The Bloomberg Commodity Spot Index slid 3.6% this Thursday, its biggest one-day drop in almost 14 months, with soybeans and platinum losing their year-to-date gains. This latest drop came on the back of the U.S. Federal Reserve’s signal of interest rate increase, a gain in the U.S. dollar, China’s intervention to cool down the commodities rally, and a better weather forecast for U.S. crops. Currie added that the recent move in spot prices is based on interest rate speculation and not on the expectations of future supply and demand, and that scarcity and strong physical demand will dictate prices in the long-term.

Threats

- The Chinese government is stepping up its intervention in the commodities market and reduce speculation as it tries to ease the threat of soaring raw material costs to its economic rebound from the pandemic. The State-owned Assets Supervision and Administration Commission (SASAC) ordered state-owned enterprises (SOEs) to control risks and limit their exposure to overseas commodities markets, while asking them to report their futures positions for SASAC review. China’s National Food and Strategic Reserves Administration also announced that it will release state stockpiles of metals including copper, aluminum, and zinc. These announcements led to metals prices and mining stocks falling across the board before paring losses.

- Countries across the globe are facing a power crunch due to extreme heat and longer droughts, surging post-pandemic power demand, rising fossil fuel prices and a bumpy transition into renewables, and higher energy costs are expected to add to the inflationary pressure coursing through the global economy. The result of the power crunch is that California is at a risk of blackouts due to a sprawling heat wave in the western U.S., cities in China’s industrial heartland are rationing electricity, and prices for electricity in Europe are far higher than usual for this time of the year. Furthermore, the operator of the Texas power grid asked customers to cut back on electricity usage as the state is facing a heat wave, while some of the power generators are offline for maintenance.

- The price of solar panel modules has risen almost 15% this quarter, representing only the seventh quarter out of the past 45 when prices have failed to decline. The recent surge is being attributed to the increase in price of polysilicon, the semi-metallic substance used to make solar panels and computer chips, which has risen from $10.57 per kilogram, at the end of 2020, to $29.41 per kilogram now, marking a 178% increase. Although there is additional polysilicon capacity expected to hit the market over the coming years, about one-third of it will be in Xinjiang, China, the region that has been under severe scrutiny across the globe because of the alleged treatment of minority groups and reports of forced labor. China will have to credibly separate its supply chain from such claims as 45% of the world’s solar-grade polysilicon comes from just four Xinjiang-based manufacturers.

Domestic Economy and Equities

Strengths

- May’s retail sales were down 1.3% month-over-month, steeping lower than consensus for a 0.5% monthly drop, but sales are up strongly on a year-over-year basis by 28.1%. Also, April’s sales were improved by 0.9% month-over-month from an initial flat reading.

- Europe opened its borders to tourists from the United States and Canada after restrictions were put in place due to the pandemic. Bank of America announced that all vaccinated staff will return to the office in September. BlackRock will allow vaccinated staff to return in July.

- Marathon Oil Corp was the best performing S&P 500 stock for the week, up 88.46%. Morgan Stanley lifted the stock from underweight to equal weight, with a price target of $15. Also, RBC Capital Markets raised its recommendation on the stock to outperform, with a price target of $18.

Weaknesses

- Initial jobless claims increased from 376,000 to 412,000. Most Bloomberg economists expected the number to drop to 360,000. Continuing jobless claims for regular state programs, also unexpectedly increased, but these claims have still come down sharply from the more than 5 million reported back in January.

- Inflation continues to pick up. May headline producer price index data (PPI) was reported higher by 0.8% month-over-month versus consensus for a 0.5% gain. Inflation increased 6.6% year-over-year. Core May PPI was up 0.7% month-over-month, above 0.5% consensus.

- Viatris Inc., was the worst performing S&P 500 stock for the week, down 23.91%. After rallying in May, the stock saw a selloff as Citigroup Inc. initiated coverage of the stock, giving it a neutral rating.

Opportunities

- President Biden’s eight-day trip to Europe has ended. The G7 voiced support for a 15% minimum global tax on corporations. The U.S. and European Union (EU) reached a deal to end a 17-year-long Airbus/Boeing trade dispute. The U.S. imposed $7.5 billion in tariffs on European exports in 2019 after the World Trade Organization ruled that the EU had not complied with its rulings on subsidies for Airbus, which is based in France. Biden’s first trip to Europe made the U.S./Europe relationship warmer and opened a door to tighter cooperation between both continents.

- Money supply growth spiked and is already reversing. This correction in money supply will cause inflation to fall and will prove that the spike in inflation is transitory, says the Cornerstone Macro Team. They believe that monetary and fiscal stimulus will fade, and income/savings will slow, translating into lower prices. Cornerstone expects a 2022 slowdown, but the economy will still expand by 4%, following this year’s growth of 9%.

- Treasury Secretary Janet Yellen said the U.S. is “well on the way” to a strong recovery from the COVID-19 pandemic. The country still faces some challenges that will require substantial public investment, and she urges lawmakers to back President Joe Biden’s proposal for a multi-year, $4 trillion spending plan on childcare, infrastructure, and green investments.

Threats

- The National Federation of Independent Business Index dipped in May due to a labor shortage, with a record high of 48% of owners reporting unfilled job openings. Enhanced federal unemployment benefits have been blamed for keeping potential workers on the sidelines. Twenty-five states have ended the program, trying to encourage more people to re-enter the workforce.

- This week’s Federal Reserve (the Fed) meeting revealed that the massive stimulus provided to fight the pandemic may be cut down sometime in 2023. Members of the Fed have previously predicted the stimulus until 2023. A minority of the Fed members expect they will need to begin raising interest rates in 2022.

- Three large companies sought Chapter 11 bankruptcy in the U.S. last week, marking a second straight week with a relatively elevated number of fillings, Bloomberg reports. A fourth was filed on Sunday. These numbers, however, don’t suggest a broad pickup in restructuring activity.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was XinFin Network, rising 50.30%.

- An alliance of 15 banks – 10 private-sector banks, four public-sector banks, and one foreign bank – have announced the formation of the Indian Banks’ Blockchain Infrastructure Company (IBBIC), a new company that will build blockchain technology solutions to process letters of credit for domestic transactions in India. The company’s blockchain solution will aim to verify data for invoices on goods and services tax and e-way bills, which track the movement of goods and services electronically to ensure compliance with tax laws, to eliminate paperwork and reduce transaction times.

- The Chinese government is pacing ahead with the adoption of its central bank digital currency (CBDC), the digital yuan, as it announced that the CBDC is available for deposit and withdrawal at over 3,000 ATMs across Beijing. The Beijing branch of the Industrial and Commercial Bank of China and the Agricultural Bank of China (ABC) have set up these ATMs and were the two most notable banks involved in the People’s Bank of China’s (PBOC) CBDC tests. The PBOC and the Chinese government have been actively promoting the digital yuan in Beijing and are expected to distribute 40 million digital yuan (~$6.2 million) to Beijing residents as part of its “red envelope” campaign.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performer for the week was Kusama, down 29.21%.

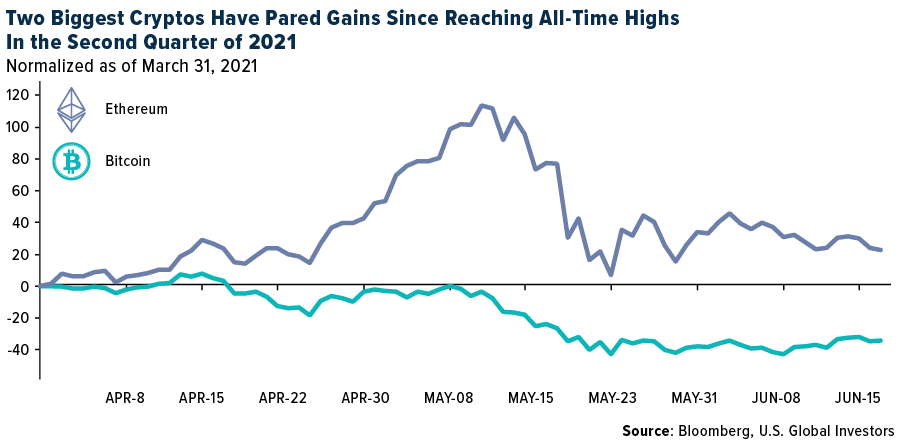

- The U.S. Securities and Exchange Commission (SEC) delayed its decision on whether it will allow New York-based VanEck to launch a Bitcoin exchange-traded fund (ETF). The SEC must render a decision on prospective applications within 45 days of the filing and can take up to 240 days to make the final decision. The SEC, in response to VanEck’s filing, is asking for public comments regarding the application and wants to know from interested parties whether the ETF would be susceptible to market manipulation, a concern that the SEC has continually stated. Market participants believe that the SEC is unsure whether it has proper surveillance over cryptocurrency exchanges and is unable to ensure adequate investor protection. Meanwhile, both Bitcoin and Ethereum are experiencing a bearish second quarter after reaching all-time highs in April and May, respectively. The chart below shows the performance of the two biggest cryptocurrencies since April 2021.

- The World Bank has denied El Salvador’s request to assist the Central American nation in implementing Bitcoin as a legal tender into its national economy, alongside the U.S. dollar. The World Bank said that it is committed to helping El Salvador regarding issues of currency transparency and regulatory process, but it cannot support Bitcoin’s adoption as a legal tender due to the environmental and transparency shortcomings.

Opportunities

- Switzerland-based digital asset bank Sygnum announced that it is offering Ethereum 2.0 staking to its customers, a few months after allowing its asset management, hedge fund, and family office clients to stake on the Tezos blockchain. The bank’s head of business units, Thomas Eichenberger, noted that the Ethereum (ETH) staking service will involve locking up multiples of 32 ETH for an undefined period and is expected to generate a yield of between 6.5% and 8% per annum. He also added that Sygnum’s institutional staking is “bank-grade” and that they are using hardware security firm Securosys to handle the ETH withdrawal keys, as ETH 2.0 staking involves both a validatory key and a withdrawal key. Furthermore, Sygnum’s competitor SEBA Bank is also launching its ETH 2.0 staking service.

- Paxos Settlement Service, a blockchain-based post-trade settlement platform for U.S. securities, announced that Wedbush Securities will join its program. Wedbush, a Los Angeles-based investment firm with $2.4 billion under management, is set to join Credit Suisse, Instinet, and Societe Generale in the Paxos program. The service is built using a permissioned Ethereum fork and allows two parties to bilaterally settle securities trades with each other on the same day. Paxos is also applying with the U.S. Securities and Exchange Commission (SEC) to become a clearing agency alongside the Depository Trust & Clearing Corporation (DTCC), which is currently the only clearing agency in the U.S.

- Nornickel, one of the biggest metal producers in the world, reported that it will provide its customers with blockchain-based tokens alongside the traditional certificates when the customers buy exchange-traded commodities (ETCs) based on the company’s metals. The Global Palladium Fund (GPF), Nornickel’s subsidiary, will launch ETCs on nickel and copper, and the blockchain tokens proving their authenticity, on the London Stock Exchange (LSE) and Borsa Italiana. Atomize, which is Nornickel’s Switzerland-based tokenization platform, will issue the tokens using the Hyperledger Fabric, an open source blockchain overseen by The Linux Foundation.

Threats

- Bitcoin’s hashrate, which is the total computational power used to secure and process transactions on the blockchain, dropped to the lowest level since November 2020 after China’s recent crackdown on cryptocurrency mining, fueled by concerns over the network’s energy consumption. Data compiled by Glassnode showed that the seven-day average Bitcoin hashrate fell to 129.1 million exahashes per second this week, a 28.5% drop from the all-time high of 180.6 million exahashes per second in mid-May. China’s 1THash, which is one of the world’s 15 largest mining pools, lost around 70% of its hashrate last week.

- The central bank governor of Indonesia, Perry Warjiyo, reiterated the country’s ban on financial institutions using cryptocurrencies as a means of payment and is mobilizing official supervisors to enforce the ban. He also emphasized that cryptocurrencies are not legitimate payment instruments under the constitution, Bank Indonesia Law, and Currency Law. This reiteration of the ban comes a few weeks after Bank Indonesia announced that it is working on a central bank digital currency (CBDC) as the nation saw an increase of 60.3% year-over-year in the use of digital payments as of April 2021.

- Chinese authorities continued their crackdown on cryptocurrency mining this week as miners in Ya’an City, in the Sichuan province, were ordered to shut down their operations for examination. The report was unclear when or whether miners would be allowed to restart operations. Sichuan province, which is China’s biggest hydropower producer, also issued orders to power generation companies to immediately stop supplying power to any cryptocurrency mining operation. The order identified 26 large mining projects that will be required to shut down, following similar orders to cryptocurrency miners in Yunnan, Xinjiang, Inner Mongolia, and Qinghai provinces.

Gold Market

This week spot gold closed at $1,764.16, down $113.37 per ounce, or 6.04%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 10.73%. The S&P/TSX Venture Index came in off 3.36%. The U.S. Trade-Weighted Dollar rose 1.97%.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Jun-15 | Germany CPI YoY | 2.5% | 2.5% | 2.5% |

| Jun-15 | PPI Final Demand YoY | 6.2% | 6.6% | 6.2% |

| Jun-16 | China Retail Sales YoY | 14.0% | 12.4% | 17.7% |

| Jun-16 | Housing Starts | 1,630k | 1,572k | 1,517k |

| Jun-16 | FOMC Rate Decision (Upper Bound) | 0.25% | 0.25% | 0.25% |

| Jun-17 | Eurozone CPI YoY | 0.9% | 1.0% | 0.9% |

| Jun-17 | Initial Jobless Claims | 360k | 412k | 375k |

| Jun-23 | New Home Sales | 875k | — | 863k |

| Jun-24 | Durable Goods Orders | 3.0% | — | -1.3% |

| Jun-24 | GDP Annualized QoQ | 6.4% | — | 6.4% |

| Jun-24 | Initial Jobless Claims | 380k | — | 412k |

Strengths

- The best performing precious metal for the week was gold, but still off 6.04%. U.S consumer prices rose in May by more than consensus expectations. CPI jumped 5% from the prior year, with many price jumps reflecting shorter term price gains from pandemic-induced supply shortages. The Federal Reserve believes most of these price changes will prove to be transitory. Economists Sarah House and Shannon Seery, at Well Fargo & Co., believe that inflationary pressure will broaden out rather than sinking back to pre-pandemic levels.

- Alamos Gold reported one of its best drilling results at the Island Gold mine, which will allow it to expand to both the east and west. Reserves at this location have increased by 1 million ounces over the past year. According to Raymond James, Torex Gold announced an updated mineral resource estimate for its Media Luna project, which now consists of a gold-equivalent indicated resource of 3.54 million ounces at an average grade of 5.27 grams per ton, reflecting a 58% increase in contained AuEq metal compared to the previously reported estimate. Of the indicated resource, 61% of the contained value is attributable to gold.

- Debswana Diamond Co., a unit of De Beers Plc, unearthed a 1,098-carat stone in Botswana on June 1, the largest since the company began operations five decades ago. Preliminary analysis suggests the stone is the world’s third-largest gem-quality diamond ever, after the Cullinan Diamond that was discovered in South Africa in 1905 and the Lesedi la Rona that was found in Botswana in 2015, according to Debswana acting Managing Director Lynette Armstrong.

Weaknesses

- The worst performing precious metal for the week was palladium, down 10.86%. According to Bloomberg, Burkina Faso’s government has ordered that artisanal mining activities in the two gold-rich localities of Oudalan and Yagha areas should cease after jihadists killed more than 130 people.

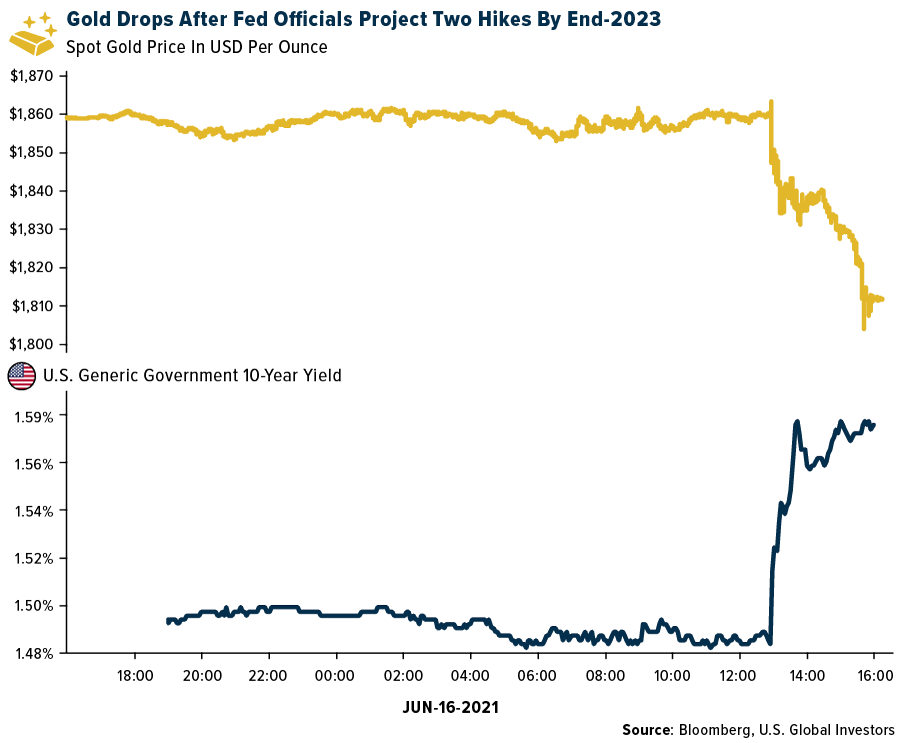

- Gold extended its decline as a U.S. bond rally lost steam ahead of this week’s Federal Reserve meeting. Bullion retreated on Monday as Treasury yields ticked higher, making the non-interest-bearing metal seem less attractive to some investors. At the Fed meeting, the timeline for interest rate increases was pulled forward, implying that stimulus that buoyed the metal will be decreased. They also indicated that there may be two increases by the end of 2023.

- Gold demand seems to be dropping. Swiss gold exports fell 37% in May. Sales to India fell 96% to 2 tons. Shipments to China fell 19% to 32.8 tons and exports to Hong Kong dropped to 3.8 tons. Swiss gold imports declined 11% month-to-month as well, to 164 tons.

Opportunities

- Fiore Gold announced it is acquiring the Illipah property from Waterton for $200,000 in cash plus 1.3 million shares. This past producing property is just 20 miles from the company’s Gold Rock project and has very similar geology. Fiore’s geology team will be able to apply their knowledge of this geology and quickly generate first pass drill targets at the newly acquired property. The company will be reviewing the existing geologic data, doing surface mapping and sampling while permitting is underway before launching a drill program early next year.

- Yamana Gold announced Friday that it is acquiring Globex Mining’s Francoeur, Arntfield and Lac Fortune Gold properties for a total consideration of C$15 million. The properties, two of which are past producing, are adjacent to the west of the Wasamac project, thus adding potential exploration upside. Yamana believes that mineralization at these properties is like that of Wasamac, based on historical production records, drilling and recent exploration efforts.

- E79 Resources share price gained slightly more that 300% over the past week on released drill results for its Happy Valley Gold Prospect in Vitoria, Australia. Drill hole HVD002 intersected 0.70 meters at 99.00 g/t Au at 94.90 meters downhole. Drill hole HVD003 intersected 0.6 meter at 147 g/t Au from 165.2m downhole and 11.10 meters of 160.45 g/t Au from 190.4m downhole. E79 Resources was testing the down-dip extensions of previously mined high-grade structures in the 1870s.

Threats

- COVID-19 continues to plague remote international mining. Mining companies are throwing their weight behind vaccination efforts as the pandemic continues to ravage much of the developing world. Miners are offering vaccines and bolstering healthcare services to employees and surrounding communities. The effort is focused on poorer nations, where healthcare systems are weak, vaccines are scarce and inoculation campaigns lag far behind those in the West. Anglo American PLC has said it is spending as much as $30 million to support the global rollout of COVID-19 vaccines across its footprint. Other miners, from Glencore to Rio Tinto, have been offering support to local governments during the pandemic, from conducting screening and mobile testing to donating extra beds for hospitals and clinics.

- Kinross Gold announced that mill operations at Tasiast in Mauritania have been temporarily suspended due to a fire that broke out on June 15. No injuries were reported on site. The company is currently assessing the damage and potential impact to the mine. Tasiast represents about 13% of Kinross’ 2021 production.

- Crypto assets such as Bitcoin continue to present a challenge to gold. Paul Tudor Jones, the head of Tudor Investments, believes that 5% of a portfolio should be in crypto assets. It serves as a diversifier, much like gold or commodities. However, the Bank of International Settlements recently issued guidance that banks should apply $1,250% risk weight for bitcoin. This factor along with minimal capital requirements of 8% results in the bank having to hold at least the same amount in offsetting assets to counter the volatility of Bitcoin. This will make it less capital efficient for the banks to hold crypto assets and reject their adoption.

Leaders and Laggards

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (03/31/2021):

Spirit Airlines

JetBlue Airways Corp

Air Canada

Southwest Airlines

Lufthansa

VanEck Vectors Short Muni ETF

Torex Gold Resources

Fiore Gold

AngloAmerican PLC

Gazprom PJSC

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The Producer Price Index (PPI) program measures the average change over time in the selling prices received by domestic producers for their output. The National Federation of Independent Business’s (NFIB) Index of business optimism is based on responses from 1221 member firms. The Bloomberg Commodity Index is made up of 22 exchange-traded futures on physical commodities. The index represents 20 commodities, which are weighted to account for economic significance and market liquidity.