You’re Probably Underinvested in Gold

Date Posted: November 1, 2019

Read time: 56 min

The U.S. was founded 243 years ago, and in that time it's amassed some $23 trillion in debt and counting. As massive as this number is, it's still less than half what Elizabeth Warren says her government-run "Medicare-for-all" program would cost... over only 10 years.

Press Release: U.S. Global Investors Announces Quarterly Results Webcast

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

The U.S. was founded 243 years ago, and in that time it’s amassed some $23 trillion in debt and counting. As massive as this number is, it’s still less than half what Elizabeth Warren says her government-run “Medicare-for-all” program would cost… over only 10 years.

The Massachusetts senator and presidential contender made the announcement this morning, responding to critics who’ve demanded to see some details on her proposal. According to her campaign, the price tag to provide Medicare-style health care to every American would be “just under $52 trillion.”

To put things in perspective, that’s close to one-fifth of the total wealth in the entire world, which Credit Suisse estimated to stand at $280 trillion in 2017.

The $52 trillion is just the nominal price tag. It doesn’t take into account incidental costs, such as what to do about the estimated 2 million Americans who would lose their jobs should private insurance be eliminated. And because the plan would be covered in part by tax hikes on employers, the ultra-wealthy and financial transactions, companies may be less inclined to hire, and people may be less inclined to invest.

The 2020 election is only 12 months away. Early signs point to another term for Donald Trump, according to Moody’s Analytics presidential election model, which has a near-perfect record at predicting outcomes. But impeachment risks are mounting, and Warren is leading the Democratic polls.

I urge investors to prepare for market volatility and currency devaluation. Gold and gold stocks have historically been excellent diversifiers in such times, but new research from the World Gold Council (WGC) shows that most investors are radically underexposed to the yellow metal, even when they believe otherwise.

Gold: Efficient, Effective and Under-Represented

I talked briefly about the WGC’s research about a month ago. The gist of the study is that investors may assume they have adequate exposure to gold because they’re invested in a fund that tracks a broad-based commodity index. The problem with this assumption is that most major commodity indices have a relatively small weighting in gold, and so their gold exposure is much smaller than they realized.

| S&P GSCI | Bloomberg Commodity Index | ||

|---|---|---|---|

| Energy | 63% | Energy | 34% |

| Agriculture | 15% | Grains | 20% |

| Livestock | 7% | Industrial Metals | 18% |

| Industrial Metals | 11% | Precious Metals | 16% |

| Precious Metals | 4% | Gold | 12% |

| Gold | 3.37% | Softs | 6% |

| Livestock | 6% | ||

|

Weights as of January 2019. Gold weighting is a sub weight of precious metals |

Weights as of June 2019. Gold weighting is a sub weight of precious metals |

||

Take a look at the tables above. The S&P GSCI, which tracks 24 commodities, has only a 3.37 percent weighting in gold. The Bloomberg Commodity Index is slightly better, with a weighting of 12 percent. These percentages shrink even more when you consider that commodities in general represent a small portion of most investors’ portfolios.

“If you are buy-and-hold investor, if you are trying to create long-term strategies, the evidence overwhelmingly shows that gold is a more effective strategic asset than commodities alone,” explains the WGC’s director of investment research, Juan Carlos Artigas, who I had the opportunity to chat with recently.

To illustrate Juan Carlos’ point, look at the following chart. In the 20-year, 10-year and five-year periods through June 2019, gold outperformed all other commodities, including energy, industrial metals and precious metals. Despite this, gold may still be under-represented in some investors’ portfolios.

“The optimal weight for gold, or the amount of gold that can help investors get better risk-adjusted returns, is between 2 percent and 10 percent,” Juan Carlos says.

Loyal readers know this is mostly in line with my own recommendation of a 10 percent weighting in gold, with 5 percent in bullion, the other 5 percent in high-quality gold mining stocks.

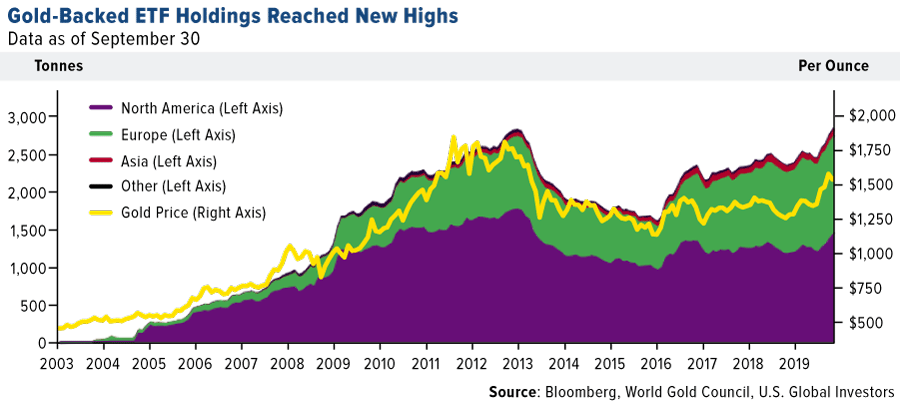

Gold-Backed ETFs at All-Time Highs

At the same time that gold is largely under-represented in many investors’ portfolios, those “in the know” have been buying at a healthy clip. In fact, since the start of the most recent gold price rally, holdings in gold-backed ETFs have climbed to an all-time high. Holdings as of September stood at more than 2,855 tonnes, surpassing the previous high of 2,839 tonnes in November 2012.

With bond yields at historic lows at the moment, “gold may become an attractive and more effective diversifier than bonds, justifying a higher portfolio allocation than historical performance suggests,” the WGC writes in its latest report, “It may be time to replace bonds with gold.”

Follow the Smart Money

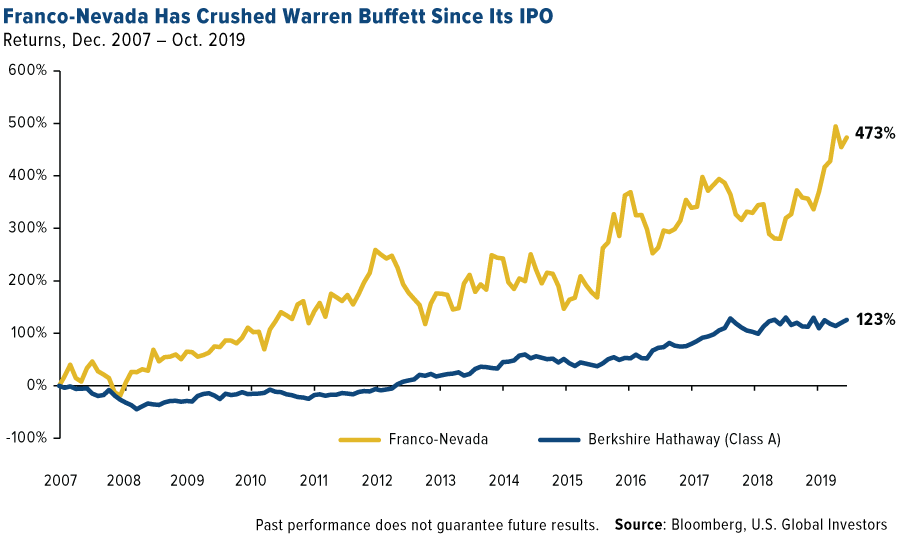

Speaking of gold ETFs, our webcast with my longtime friend and mentor, Pierre Lassonde, was held this week, and by all measures, it was a huge success. I’ve participated in a number of webcasts over the years, but never one with so many registrants and attendees.

I expected no less from the cofounder of gold royalty company Franco-Nevada, whose stock is up more than 473 percent since its IPO in December 2007. That’s enough to beat Warren Buffett’s Berkshire Hathaway by a multiple of nearly four.

Buffett, as you probably know, is famously not a fan of gold, saying at one point that “it doesn’t do anything but sit there and look at you.”

His low opinion on the yellow metal is in stark contrast to other big-name investors, including Ray Dalio, Stanley Druckenmiller, Jeffrey Gundlach, Paul Tudor Jones, Bill Gross, Sam Zell, Mark Mobius and many other billionaires who have embraced the yellow metal.

With all due respect to Buffett, maybe he should reconsider gold. After all, he changed his mind about airlines. Years after quipping that a “farsighted capitalist” should have shot down Orville Wright at Kitty Hawk and “done his successors a huge favor,” the Oracle of Omaha now owns millions of shares in all four of the major domestic airlines.

“Warren Buffett loves franchises,” Pierre said during the webcast, “and there’s no greater franchise in the world than Franco-Nevada.”

Franco-Nevada investors would no doubt agree. In the past 10 years, the company’s average dividends per share (DPS) growth rate was nearly 20 percent per year.

As Pierre put it, “We could send everyone at Franco-Nevada to Hawaii for 30 years and still be able to afford to continue raising our dividends.”

If you weren’t able to listen in, you can still get the replay by emailing us at info@usfunds.com!

October 31, 20193 Emerging Europe Stocks We’re Bullish On Right Now |

October 29, 2019The Opportunities Go to Those Who Can See… |

October 25, 2019Gold at $10,000 Isn’t Crazy |

|||

Gold Market

This week spot gold closed at $1,514.40, up $9.85 per ounce, or 0.65 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 1.03 percent. The S&P/TSX Venture Index came in off just 0.91 percent. The U.S. Trade-Weighted Dollar fell 0.61 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Oct-29 | Conf. Board Consumer Confidence | 128.0 | 125.9 | 126.3 |

| Oct-30 | ADP Employment Change | 110k | 125k | 93k |

| Oct-30 | GDP Annualized QoQ | 1.6% | 1.9% | 2.0% |

| Oct-30 | Germany CPI YoY | 1.0% | 1.1% | 1.2% |

| Oct-30 | FOMC Rate Decision (Upper Bound) | 1.75% | 1.75% | 2.00% |

| Oct-31 | Eurozone CPI Core YoY | 1.0% | 1.1% | 1.0% |

| Oct-31 | Initial Jobless Claims | 215k | 218k | 213k |

| Oct-31 | Caixin China PMI Mfg | 51.0 | 51.7 | 51.4 |

| Nov-1 | Change in Nonfarm Payrolls | 85k | 128k | 180k |

| Nov-1 | ISM Manufacturing | 48.9 | 48.3 | 47.8 |

| Nov-4 | Durable Goods Orders | -1.1% | — | -1.1% |

| Nov-7 | Initial Jobless Claims | 215k | — | 218k |

Strengths

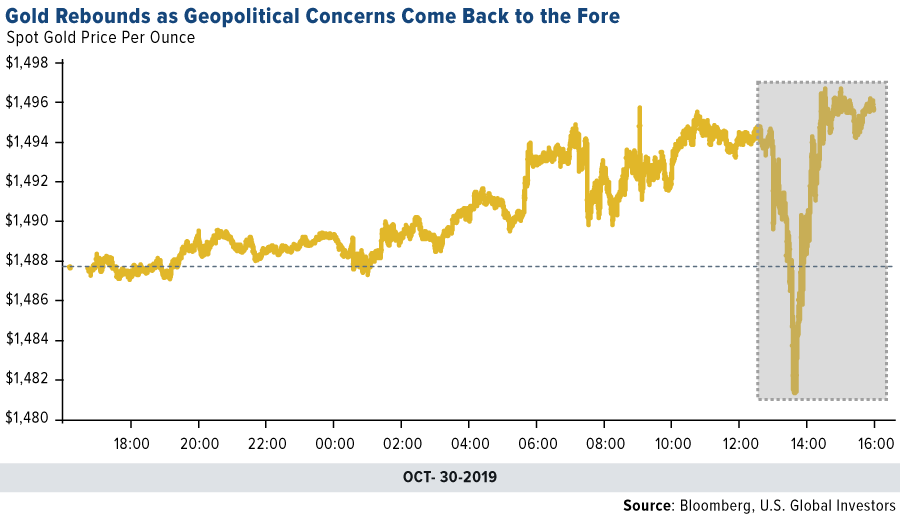

- The best performing metal this week was platinum, up 2.61 percent, followed closely by palladium, up 2.39 percent. Both platinum and palladium experienced strong demand as hedge funds pushed their net-long positions to five and three-week highs, respectively. Gold traders and analysts were mostly bullish in the weekly Bloomberg survey due to renewed concerns over a trade deal between the U.S. and China. The latest rate cut by the Fed helped remove a negative characteristic of gold – that it doesn’t pay any interest. With real yields now negative, the yellow metal is comparatively attractive.

- Gold saw its fifth monthly gain in October after benefitting from haven buying amid increased geopolitical tensions. Turkey’s official gold reserves rose $72 million from the previous week to now total $26.5 billion. According to central bank data, Turkish gold reserves are up 42 percent year-over-year. American Eagle gold-coin sales from the U.S. Mint more than doubled in October, versus September and were the highest since March, with total sales of 11,500 ounces.

- The yellow metal initially fell after the Fed cut rates for the third time on Wednesday, but then quickly regained those loses despite policy makers hinting they might put further cuts on hold. Bloomberg reports that the Fed looks prepared to stop cuts in order to assess the impact on the economy of their reductions over the past three meetings. Dan Pavilonis, senior market strategist at RJ O’Brien & Associates LLC, said “there’s a lot of moving parts now that are creating a theme to be bullish on gold.”

Weaknesses

- The worst performing metal this week was silver, with a slight gain of 0.44 percent, despite setting a five-week high on futures net long positions. The ISM Index rose in October by lower than estimates and signals a third straight month of contraction for U.S. manufacturing. The index rose to 48.3 from a 10-year low of 47.8 in September, compared with median projections of 48.9. Bloomberg reports that the low reading highlights challenges for manufacturers such as the ongoing trade war, slowing global growth and a strong dollar.

- The Chicago PMI reading also missed estimates, posting the lowest reading since 2015 at 43.2 for the month of October. Bloomberg analysis shows that the index has never dipped this low out of a recessionary period except for the 2015-2016 oil and China growth scare. Market reactions to the reading were very negative, which makes sense given its recessionary prediction history.

- The Perth Mint reported that gold coin and bar sales totaled 32,469 ounces in October, down from 46,837 ounces the month prior. Silver sales did increase at 1.39 million ounces, versus 1.35 in September. Gold consumption in China fell 9.6 year-over-year in the first nine months of 2019 at 768.31 tons, according to the China Gold Association. Demand in the world’s largest consuming country was hit by higher prices and downward pressure on the economy.

Opportunities

- Bloomberg’s Eddie van der Walt says that gold’s bullish performance even as the S&P 500 continues to hit record highs suggest that gold has “unfinished business” at $1,550 an ounce. “While U.S. GDP has so far held up in the face of slowing manufacturing, there’s still plenty of bears out there wary of stocks near record highs – they will probably be pivotal in pushing the metal back to the highs for a re-test.”

- Torex Gold reported strong third quarter earnings. The company had revenue of $198.2 million on sales of 132,535 ounces of gold and produced 138,145 ounces during the quarter. Torex will be appointing Jody Kuzenko as its new CEO at the annual general meeting in June 2020, which is a huge step for gender diversity in the mining world. Evolution Mining’s Executive Chairman Jake Klein cautioned companies to practice responsible capital spending and not rush into acquisitions. Klein says “fundamentally, I don’t see it as our business, or our position, to buy assets on the basis that the gold price is going to go up.”

- Zimbabwe is hoping that a platinum mining boom will help revive its economy. Platinum projects valued at more than $8 billion have been announced by Cypriot and Russian investors, but the country still remains politically and economically instable. Zimbabwe is home to the world’s third largest platinum-group metal deposits and has announced 2.79 million ounces in output by 2024, almost triple current output levels.

Threats

- The market for bulletproof vehicles is skyrocketing and demand in the U.S. is higher than ever, according to a Bloomberg news story. Philip Nadjafov, whose family founded Isotrex, says business has risen in the last three years to fulfill UN and government contracts and that “people are investing in their security.” This is a troubling sign of the times and highlights the wealth gap of more consumers able to afford six-figure bullet proof personal vehicles. ArmorMax CEO Mark Burton says “people are worried about random acts of violence.”

- Well-known hedge fund manager Paul Tudor Jones says that the S&P 500 will fall 25 percent if Democrat Elizabeth Warren wins the 2020 presidential election – one of many on Wall Street who are predicting doom if there’s a shakeup in the White House. However, just a few years ago strategists were predicting a big drop if Donald Trump was elected, which did not happen. Point being there will be many political risks from now until the 2020 election and no one can say for sure how the stock market will respond to anyone becoming elected, or re-elected.

- The U.S.-China trade deal still seems unlikely after China is said to doubt that any long-term deal with President Trump will be possible. Another turn is that Chile cancelled an economic summit in a few weeks where the U.S. and China were meant to meet and sign phase 1 of a deal.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 1.44 percent. The S&P 500 Stock Index rose 1.47 percent, while the Nasdaq Composite climbed 1.74 percent. The Russell 2000 small capitalization index gained 1.96 percent this week.

- The Hang Seng Composite gained 1.53 percent this week; while Taiwan was up 0.92 and the KOSPI rose 0.59 percent.

- The 10-year Treasury bond yield fell 7 basis points to 1.72 percent.

Domestic Equity Market

Strengths

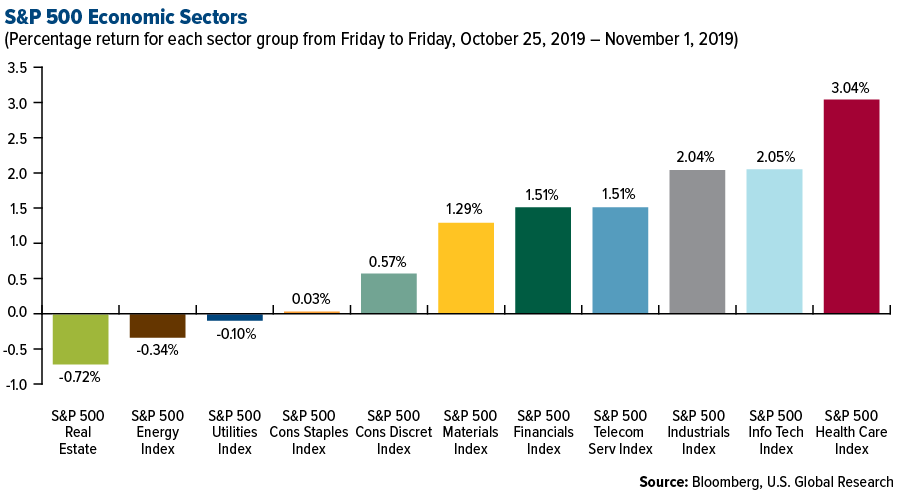

- Health care was the best performing sector of the week, increasing 3.04 percent compared to an overall increase of 1.47 percent for the S&P 500 500.

- Tiffany & Co. was the best performing stock for the week, increasing 28.87 percent.

- Apple beat fourth-quarter sales and profit targets as a wearables surge overshadowed the ongoing iPhone funk. The tech giant posted revenue of $64 billion for its fiscal fourth quarter, beating analysts’ expectations. Apple’s $24 billion wearables segment is now almost as big as its Mac business. Apple’s wearables and accessories products accounted for nearly as much revenue in the company’s just-completed fiscal year as its Mac computers.

Weaknesses

- Real estate was the worst performing sector for the week, decreasing 0.72 percent compared to an overall increase of 1.47 percent for the S&P 500.

- Arista Networks was the worst performing stock for the week, falling 24.17 percent.

- Deutsche Bank tumbled on a disappointing quarterly loss after the “necessary evil” spending on a massive overhaul. The bank is spending more to axe 18,000 jobs and as part of a major restructuring.

Opportunities

- Dunkin’ Brands reported a better-than-expected quarterly profit on lower costs on Thursday and raised its forecast for 2019, betting on investments to improve delivery and add new menu items to boost growth. The company has been pushing into premium coffees that are sold at affordable prices compared with Starbucks Corp. as it steps up to gain market share in an extremely competitive breakfast segment.

- Lyft lost less money than Wall Street expected in the third-quarter as the company keeps adding new riders. The ridesharing firm said last week that it expects to turn a profit a full year ahead of when Wall Street analysts had expected it to.

- Spotify revenue beats estimates on higher paid subscriber addition. The music streaming company reported a better-than-expected 113 million in total paid subscribers for its premium service.

Threats

- Volkswagen lowered its 2019 outlook for vehicle deliveries as demand cools. VW said a slowdown in global demand would result in Volkswagen Group vehicle deliveries in 2019 to be in line with year-earlier figures, adjusting its earlier forecast which had expected a slight increase.

- Netflix competitor HBO Max is set to launch in May for $15 per month. According to Vox, HBO Max will feature all of HBO’s programming as well as original shows.

- Beyond Meat’s shares are sinking as locked-in investors see “the time to cash out.” The stock sank 9 percent in premarket trading. The lockup period — or time when investors who bought into the stock pre-IPO are unable to sell it — expired on Tuesday.

The Economy and Bond Market

Strengths

- The U.S. labor market is showing resilience. Nonfarm payrolls climbed 128,000 in October, exceeding forecasts, despite a six-week long strike at General Motors Co. and 20,000 temporary census workers leaving their jobs, according to a Labor Department report Friday. The unemployment rate edged up from a half-century low, matching projections.

- U.S. gross domestic product (GDP) grew faster than expected in the third quarter, but slowed slightly as business investment continued to decline. The Commerce Department said Wednesday that economic activity grew at an annualized rate of 1.9 percent in the third quarter, down slightly from the 2 percent pace in the second quarter. Economists polled by Dow Jones had expected the first look at third-quarter economic growth to come in at 1.6 percent. The better-than-expected data was the result of continued consumer spending as well as government expenditures, the department said

- Federal Reserve officials reduced interest rates by a quarter of a percent for the third time this year and signaled a pause in further cuts unless the economic outlook changes materially. The Federal Open Market Committee (FOMC) altered language in its statement following the two-day meeting Wednesday, dropping its pledge to “act as appropriate to sustain the expansion,” while adding a promise to monitor data as it “assesses the appropriate path of the target range for the federal funds rate.” “We believe monetary policy is in a good place,” Fed Chairman Jerome Powell said at a news conference following the decision. “We see the current stance of policy as likely to remain appropriate as long as incoming information about the economy remains broadly consistent with our outlook.”

Weaknesses

- A gauge of U.S. manufacturing showed the sector continued to contract in October, the third straight month of slowdown amid global trade uncertainties. The manufacturing purchasing manager’s index (PMI) came in at 48.3 last month, compared with a 47.8 reading in September. But it was below economists’ expectations of 49.1. A number below 50.0 represents a contraction in the industry.

- U.S. consumer confidence unexpectedly fell in October amid household concerns about the short-term outlook for business conditions and job prospects. The Conference Board said its consumer confidence index slipped to a reading of 125.9 this month from an upwardly revised 126.3 in September. Economists polled by Reuters had forecast it rising to 128.0 in October.

- China’s factory output slipped to its lowest level in eight months as Trump’s trade-war malaise sets in. New export orders led the fall — a sign that Trump’s trade war has further damaged China’s export economy. Additionally, Hong Kong slid into recession for the first time since the global financial crisis in the third quarter, advance estimates showed on Thursday. The economy has been weighed down by increasingly violent anti-government protests and the protracted U.S.-China trade war.

Opportunities

- The U.S. will have a relatively slow week with the only major release being the ISM non-manufacturing PMI on Tuesday. The ISM’s non-manufacturing composite is forecast to edge up to 53.2 in October from 52.6 in September when it plunged to a three-year low. If the PMI does recover in October, it would go some way in easing recession fears and reinforce the Fed’s decision to put its easing cycle on hold.

- The preliminary reading of the University of Michigan’s Consumer Sentiment Index on Friday is forecast to remain steady. Such an outcome would reassure investors of the consumer’s resilience.

- China will eliminate all restrictions on foreign investments not included in its self-styled "negative lists," a vice commerce minister said on Tuesday. It will also "neither explicitly nor implicitly" force foreign investors and foreign companies to transfer technologies, Wang Shouwen told a news conference in Beijing.

Threats

- U.S. factory orders for September come out on Monday. Following this week’s weak manufacturing data, next week’s forecast for a continued slowdown seems like the path of least resistance.

- House Speaker Nancy Pelosi said Friday she expects the Democratic-led impeachment inquiry of President Donald Trump to begin public hearings this month. Pelosi spoke a day after the House voted to set up a formal process for public hearings in an investigation of whether Trump used his office to pressure Ukraine to open a politically motivated investigation in exchange for releasing military aid. Pelosi also said that Congress should pursue an impeachment inquiry regardless of its impact on financial markets.

- Chinese officials reportedly cast doubt on any long-term trade deal with Trump — and his impulsive nature is part of the problem. "Chinese officials have warned they won’t budge on the thorniest issues," Bloomberg reported. And they’re also worried "he may back out" of a deal.

Energy and Natural Resources Market

Strengths

- The best performing major commodity for the week was natural gas, which gained 17.57 percent as widespread cold weather brought chills to the Midwest and Northeastern U.S. Palm oil futures saw the biggest monthly advance since September 2015 due to supply concerns, strong Chinese demand and expectations for a jump in its use as a biofuel. Bloomberg reports that the most actively traded contract gained more than 16 percent in October.

- The Caixin China Manufacturing PMI in October unexpectedly rose to 51.7, up from 51.4 in September, which is positive for commodity demand outlooks. Miners, steelmakers and base metals rose on the news. The Stoxx Europe 600 Basic Resources Index rose as much as 1 percent Friday morning while several miners and steelmakers also had advances. Base metals saw a second monthly advance, as the strong Chinese PMI data comes as a contrast to the largely gloomy world manufacturing news.

- Total SA reported third-quarter earnings that beat estimates. The French energy giant offset lower oil and gas prices by boosting production and cutting costs, reports Bloomberg. RBC analyst Biraj Borkhataria says “in the midst of the sector seeing material earnings downgrades, Total stands out as having a relatively resilient portfolio, visibility on earnings and a shareholder-friendly-remuneration plan.”

Weaknesses

- The worst performing major commodity for the week was iron ore, which fell 4.02 percent largely on growth fears. Oil had its biggest weekly loss in a month due to growing U.S. stockpiles and renewed doubts that a long-term U.S.-China trade deal will happen, which hurts demand for the fuel. Concerns grew again over the supply and demand imbalance when Saudi Arabia announced that it has added more than 1 million barrels a day of production. Oil futures fell as much as 2.5 percent on Thursday, then rose on Friday morning, but are still down around 4 percent for the week. Royal Dutch Shell Plc said that the worsening economy could slow the pace of returns to shareholders and that the 2020 outlook is weakening.

- The U.S.-China trade dispute continues to take a big toll on American farmers. A report by the American Farm Bureau Federation shows that farm bankruptcies rose 24 percent in September to the highest since 2011. Farmers are increasingly dependent on trade aid and federal programs for income, with $33 billion of a projected $88 billion in income set to come from aid.

- Iron saw a monthly loss in October amid difficulties in China’s steel industry. Bloomberg reports that iron is struggling to hold around $80 and could risk falling into the $70s. Rio Tinto Group said that iron ore shipments could increase up to 5 percent in 2020, sparking oversupply fears. China, the world’s top buyer of natural gas, saw its imports fall for the first time in more than three years due to oversupply and an outage at a key terminal. Last piece of China news: the nation is behind on its solar installation targets. The country estimated earlier this year that capacity would grow to 45 gigawatts, but estimates now show that it could total less than 30 gigawatts by the end of 2019.

Opportunities

- Lundin Petroleum AB announced that it plans to invest $60 million in a Norwegian hydropower plant. CEO Alex Schneiter said in a Bloomberg interview that its mission “is to be one of the most efficient offshore producers on this planet” and “we recognize that we are a large consumer of electricity, so we want to go one step further and also replace what we’re using.” Lundin said that it might plant trees to offset the use of gas turbines to power production at some of its offshore Norway drilling sites.

- Tsingshan Holding Group, a private Chinese company that produces one fifth of the world’s stainless steel, is transforming the nickel market. Tsingshan pioneered the use of nickel pig-iron, a lost-cost alternative to pure iron, to make stainless steel and is driving costs down. In the span of two months, more than half of nickel stockpiles in the London Metal Exchange network have been drained, with Tsingshan said to be a key driver, reports Bloomberg. Inventories of the metal are the lowest in 11 years and ore prices are up a whopping 56 percent so far in 2019.

- Cornerstone Macro published a note about ESG and renewable energy saying “organization is what matters, not production.” The group said that the energy industry exists to organize energy and get it to the right places at the right times. Although bullish on the growth in renewables, Cornerstone points out the grave need for storage and grids to organize power supplies from wind and solar. ESG-minded investing has grown in popularity, with Harvard Business Review reporting that “in the beginning of 2018, $11.6 trillion of all professionally managed assets – one $1 of every $4 invested in the U.S. – were under ESG investment strategies.”

Threats

- An independent study led by the Church of England Pensions Board and the Council of Ethics of the Swedish National Pension Funds found that about 10 percent of the world’s 1,635 tailings damns have had stability issues at some stage, reports Bloomberg. The study contacted miners globally to get more information on dams, following the Brazil dam failure disaster early this year. The investors behind the study control around $13.5 trillion in assets.

- Australia’s pro-coal Prime Minister Scott Morison announced that he will fight back strongly against green activists who “threaten the livelihoods of fellow Australians.” The nation, a top global miner, still derives most of its energy from burning fossil fuels and is at a cross roads with green movements picking up steam. Southeast Asia is also clinging to coal. The International Energy Agency estimates that demand will double to 400 million tons a year by 2040.

- California is still “under fire” from strong winds that can spark fires after knocking down live-wire electricity poles. Utility companies deliberately blackout customers in an effort to keep fallen lines from sparking blazes. The threat of wildfires will remain a challenge for California as fire can cause widespread damage and require vast sums to rebuild and repair.

Emerging Europe

Strengths

- Russia was the best performing country this week, gaining 2 percent. Gazprom shares gained 6.8 percent after Denmark approved the Nord Stream 2 pipeline construction in its waters. Shares of Norilsk Nickel gained 5.2 percent on news that Indonesia will ban exports of nickel ore immediately, not at the beginning of next year as previously planned.

- The Polish zloty was the best performing currency this week, gaining 1.5 percent against the U.S. dollar. All emerging European currencies gained in the past five days, as the dollar corrected and the U.K. avoided exiting the eurozone on October 31 without a deal.

- Health care was the best performing sector among eastern European markets this week. Richter, a Hungarian pharmaceutical company, and the only stock in the health care sector, gained 5.5 percent over the past five days.

Weaknesses

- Turkey was the worst performing country this week, losing 1.8 percent. The U.S. House passed a sanction bill against Turkey with heavy majority, despite that the White House previously assured Turkey that there would be no sanctions per a recent agreement on Northern Syria. The bill still needs to pass through the Senate, but it definitely added to already high geopolitical pressure between the two nations.

- The Russian ruble was the worst relative performing currency in the region this week, gaining just 50 basis points. Historically, the ruble has been highly correlated with the price of Brent crude oil, which lost 70 basis points in the past five days.

- Financials was the worst performing sector among eastern European markets this week. Alior Bank, a Polish bank, was the worst preforming equity, losing more than 10 percent in the past five days.

Opportunities

- Great Britain avoided exiting the eurozone without a deal on October 31. Prime Minister Boris Johnson secured a new Brexit deal recently and was able to call for a snap election after the EU extended the Brexit deadline to January 31, 2020. Latest polls show that his Conservative party is leading, and if he wins the December 12 election, he could have majority in the parliament. His job to push Brexit negotiations through the parliament could be an easier task going forward.

- The Polish zloty and Hungarian forint are among the strongest emerging market performers in October. The two currencies have been sensitive to Brexit worries, given the importance of EU budget transfers and remittances from foreign workers in the U.K. But with a no-deal option for the U.K. to leave the EU off the table, central emerging currencies may now move higher.

- S&P upgraded Greece’s credit rating by one notch to BB- with a positive outlook. Revised ratings on Greece reflect the improving economic outlook, strong budgetary performance and a favorable government debt structure, S&P said in a statement. Greece has turned the corner, and continued government efforts to push the reforms should bring the country back to the investment grade rating. The investment grade rating is only two notches away.

Threats

- Emerging market equites headed for a fourth week of gains on Friday as strong Chinese data and hopes for a trade deal lifted investor appetite for risker assets. In addition, a Federal Reserve rate cut prompted money flow into emerging markets, the biggest inflows in 37 weeks according to Bloomberg’s article “Flow to Stocks and Bonds Buoyed by Fed, Trade Talk.” Given the strong emerging market performance, souring trade talks and weaker data out of the United States might spark a correction in the risker assets.

- On Friday, Russia assumed the power to disconnect the country from the global Internet as a controversial law signed by President Putin went into effect. The government intends to create infrastructure for a sovereign Internet to protect against cyberattacks from abroad, but critics see the measure as a step toward increased government control. For the first time ever, the Russian state has full technical control over the Internet.

- Euro-area growth came in slightly above expectations, but remains a long way below trend. The economy expanded by 20 basis points in the third quarter, slightly above both the median estimate of economists surveyed by Bloomberg News. Eurozone inflation was reported lower. Christine Lagarde took over Mario Draghi’s post on November 1 and she will continue his efforts to revive the euro-area economy.

China Region

Strengths

- The best performing indices in the region were India’s Nifty and Sensex Indices, which jumped 2.65 and 2.84 percent, respectively. Within East and Southeast Asia, Hong Kong, Singapore and Malaysia all closed up better than 1 percent on the week.

- Industrials constituted the best-performing sector in the Hang Seng Composite for the week, rising 2.67 percent, ahead of Properties & Construction as well as Information Technology up at the top.

- This is an odd strength, one must admit, but perhaps appropriate, given the most curious global phenomenon famously (or infamously?) known as “Baby Shark.” The viral (accursed?) song has now, according to a recent Bloomberg News story, racked up some 3.8 billion views on YouTube globally and featured in places like this country’s recent World Series (Congratulations, Nationals, and tough loss, H-town…) as well as in the recent protests in Lebanon. But behind it all is a closely-held South Korean company called SmartStudy Co., and its children’s educational brand Pinkfong. Behind that company is the Kim family, whose stakes in the rising fortune are now running at roughly $125 million and counting, thanks in large part to “Baby Shark.” (That’s a lot of doo-doo doo-doo doo-doos.) Kim Min-seok founded SmartStudy Co. in 2010.

Weaknesses

- The poorest-performing index in the region was the Jakarta Composite in Indonesia, which was closed Friday but finished down 38 basis points on the week.

- Energy and Materials were the weakest sectors in Hong Kong’s Hang Seng Composite Index this week, falling 2.00 and 1.15 percent, respectively.

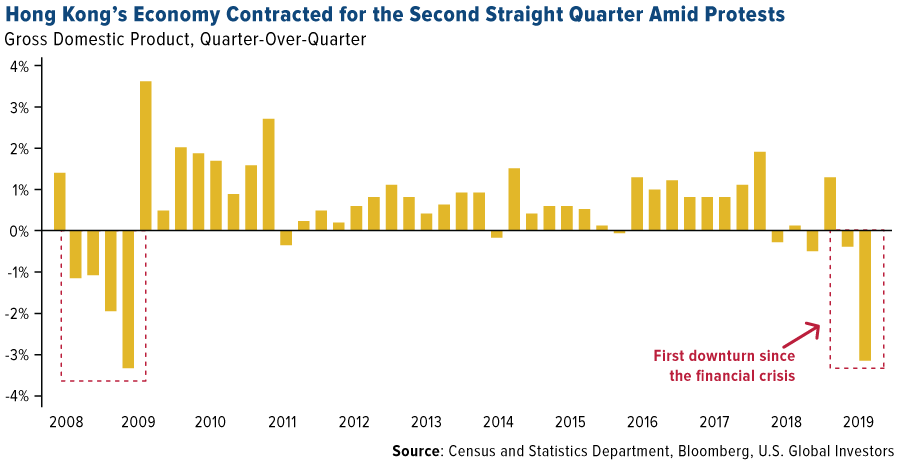

- Hong Kong’s quarter-over-quarter GDP growth has now contracted for a second straight quarter, with the third quarter GDP print for the Special Administrative Region showing quarter-over-quarter contraction by 3.2 percent, below estimates for only a 0.6 percent drop and following the prior QoQ decline of 0.4 percent. The financial hub’s troubles of late have clearly weighed on the region’s economic growth.

Opportunities

- U.S.-China trade talks continue, with Chinese sources telling media late this week that the U.S. and China have more or less reached a “consensus in principle” around core Phase One issues without providing much detail, and chief economic advisor Larry Kudlow stated that the U.S.-China calls this week were productive and making good progress. Both sides have called the week’s talks constructive. Indeed, the relatively positive note on which the week closed out seems perhaps a bit coincidental given the cancellation of the APEC meetings in Chile as well as firm Chinese indications that the Chinese do not intend to budge on the thornier issues (at least any time soon). Still, continued talks are a positive, and while Phase One could conceivably be as substantial as it gets until the 2020 U.S. elections are behind us, it may well represent a positive springboard or base from which to work going forward post-2020 election. Of course, how exactly this all plays out remains anyone’s guess in a trade war that’s dragged on over multiple calendar years already, but given the relatively slow pace so far and the word from the Trump team that simply because the APEC meeting may be off is not any indication of a breakdown in talks—and that sometimes these things just take more time—it sure seems possible that even a “Phase One” or “Skinny” deal may well not come until early 2020, at which point it is equally conceivable that more domestic items on the agenda will likely preoccupy Mr. Trump as he moves forward toward November while the Chinese stand by to see which way the wind is blowing. (Again, all this is simply a hypothetical, but hardly one requiring much imagination.) In the meantime, progress toward a slow Phase One is meaningful for markets and corporate sentiment; any resolution or certainty will likely be even more so.

- Despite the recent bump up in Hong Kong’s market, the blue chip Hang Seng Index in Hong Kong remains as of Friday at a price-to-earnings (P/E) ratio of 10.55, certainly up off its lows but hardly scraping the sky in some IFC2-like fashion. The S&P 500 here in the U.S., for rough comparison, trades at a P/E of 20.23. What’s your time horizon?

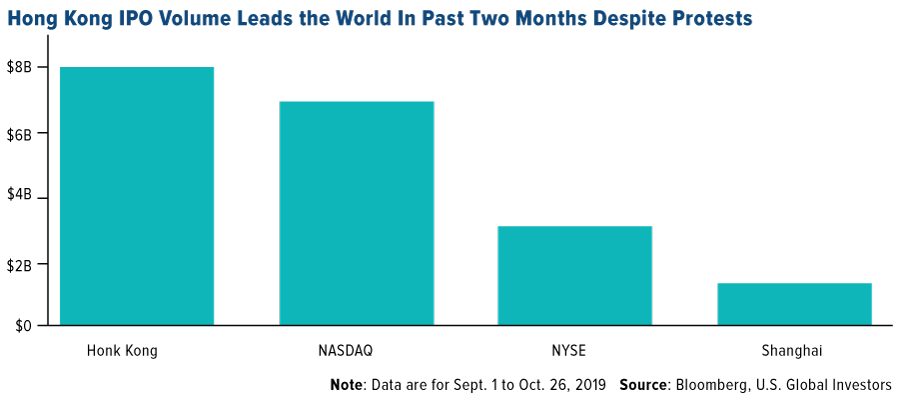

- Now, here’s a fun fact despite all the recent doom and gloom about the Hong Kong SAR (and even as U.S.-listed Chinese ecommerce giant Alibaba considers a decision soon about a listing in HK): over the last couple of months—and again, in spite of all the hullabaloo—HKEX has pulled in more money than its major global competitors, including the NYSE, the Nasdaq and Shanghai.

Threats

- In keeping with this section’s views, we once again reiterate that trade war escalation must remain a threat until it isn’t. The base case increasingly seems to be, for many analysts, that some sort of continued delay to implementation of new tariffs is possible in the nearer term while working toward some sort of Phase One agreement in more detail, but China has made relatively clear—especially this week—that the country is (ostensibly, at least) not interested in budging on the thornier issues between the two sides any time soon. The Trump administration reiterated that some things simply take more time to achieve, and certainly does not seem pressured—yet, at least—for any sort of immediate deal. Stay tuned.

- In Hong Kong, we continue to see conflicting data in media about the future of once-favored Beijing supporter HK CEO Carrie Lam. Late reports this week confirmed that the Chinese authorities seek a more active “role” in HK on everything from education to selection of leadership. While hardly either the tone or substance that most protestors seem inclined to favor, one wonders whether this may be a forceful if face-saving statement from Beijing indicating that yes, indeed, leadership change may be deemed more acceptable, so long as the replacement is deemed acceptable to Beijing? Clearly, this will not resolve protestors’ perceived long-term threats from Beijing to the city’s autonomy, but it could present a way forward, at least at face value, for another of the protestors’ demands: the resignation of Ms. Lam. Of course, who knows what comes next if indeed we do see a move toward new leadership? And therein lays the threat…

- The Markit Indonesia PMI declined to 47.7 from 49.1, still languishing down in contractionary territory and making new lows ahead of next week’s third-quarter GDP print.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended November 1 was carVertical, up 1,377.22 percent.

- On Thursday, the bitcoin blockchain reached $1 billion in cumulative transaction fees, reports CoinDesk. “This milestone is a really cool one just because it shows how much people value block space,” said Bryan Aulds, founder of bitcoin wallet Billfodl. While the cumulative amount of transaction fees converted to U.S. dollar amounts to roughly $1billion, the article continues, the amount is actually much larger if you consider the market value of bitcoin today.

- Bitcoin gained nearly $2,500 at its peak this week, writes Bloomberg, following positive comments regarding blockchain technology from Chinese officials. The largest digital currency hit a ceiling at $10,000 however, indicating it will need to meaningfully breach that level for confirmation the rally could continue, the article explains.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended November 1 was Howdoo, down 74.97 percent.

- On Tuesday, billionaire founder of Bitmain Technologies, Wu Jihan, announced the resignation of his co-founder Micree Zhan Ketuan, reports Bloomberg. The news was a surprise ouster that appeared to resolve a struggle for control of the world’s largest crypto-mining startup.

- Initial coin offerings are way down, although a few brave promoters are still using the SEC’s Form D exempt offering process to gain access to accredited investors with no pre-review by the SEC, writes MarketWatch. However, there’s been a steep drop-off since the SEC started suing, and settling, with some early promoters.

Opportunities

- Bitmain is said to have confidentially filed for an initial public offering (IPO) with the U.S. Securities and Exchange Commission, reports CoinDesk, following a failed attempt to go public on the Hong Kong Stock Exchange in 2018. The offering was filed earlier this week and is being sponsored by Deutsche Bank. The mining giant will now undergo questioning by the securities regulator before – if allowed – submitting an F1, a certification required for foreign companies before listing in the U.S. securities markets, the article explains.

- Bruce Fenton, a longtime bitcoin advocate, has started a new broker-dealer for digital asset firms and financial advisors, reports CoinDesk. The firm is called Watchdog Capital and is capable of securities underwriting, investment banking, crowdfunding, Reg A+ offerings, starting real estate investment trusts and doing over-the-counter trading for retail and institutional business, the article continues.

- Halloween 2019 marks the eleventh anniversary of the release of bitcoin’s white paper, outlining the first fully decentralized, peer-to-peer electronic cash system by the anonymous creator Satoshi Nakomoto, reports CoinDesk. Bitcoin’s code was rolled out the following January, making its first year inauspicious at best. Eleven years later, however, many metrics point toward a bright future for the digital asset.

Threats

- The laws of finance still apply in cryptocurrency’s parallel universe, writes one Bloomberg article this week. A group of former Wall Street traders who are now seeking riches in digital assets say that crypto credit has expanded too quickly and is headed for a blow-up. The volume of loans outstanding is too small to shake the wider world, the article goes on to explain, but the worries still serve as a cautionary reminder of how new technologies can’t do away with finance’s boom and bust cycles.

- While some see China’s recent embrace of blockchain technology as helpful validation, others worry that crypto is diverging further from its anti-authoritarian roots, writes CoinDesk. The world’s most populous country is making significant progress with plans for a national cryptocurrency that could increase the government’s surveillance powers over the economy.

- This week Belgium’s financial sector regulator, the Financial Services and Markets Authority, issued a new warning over suspected cryptocurrency scam websites, reports CoinDesk. It added nine new domains to its list, bringing its running total to 131 domains.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| 10-Yr Treasury Bond | 1.72 | -0.08 | -4.34% |

| Oil Futures | 56.06 | -0.60 | -1.06% |

| Hang Seng Composite Index | 3,657.85 | +55.18 | +1.53% |

| S&P Basic Materials | 370.03 | +4.70 | +1.29% |

| Korean KOSPI Index | 2,100.20 | +12.31 | +0.59% |

| S&P Energy | 437.36 | -1.51 | -0.34% |

| Nasdaq | 8,386.40 | +143.28 | +1.74% |

| DJIA | 27,347.36 | +389.30 | +1.44% |

| Russell 2000 | 1,589.33 | +30.62 | +1.96% |

| S&P 500 | 3,066.91 | +44.36 | +1.47% |

| Gold Futures | 1,515.10 | +9.80 | +0.65% |

| XAU | 95.94 | +2.40 | +2.57% |

| S&P/TSX VENTURE COMP IDX | 541.49 | -5.00 | -0.91% |

| S&P/TSX Global Gold Index | 246.99 | +3.70 | +1.52% |

| Natural Gas Futures | 2.70 | +0.40 | +17.52% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Korean KOSPI Index | 2,100.20 | +68.29 | +3.36% |

| 10-Yr Treasury Bond | 1.72 | +0.12 | +7.38% |

| Gold Futures | 1,515.10 | +7.20 | +0.48% |

| S&P Basic Materials | 370.03 | +20.43 | +5.84% |

| S&P 500 | 3,066.91 | +179.30 | +6.21% |

| DJIA | 27,347.36 | +1,268.74 | +4.87% |

| Nasdaq | 8,386.40 | +601.15 | +7.72% |

| Oil Futures | 56.06 | +3.42 | +6.50% |

| Hang Seng Composite Index | 3,657.85 | +156.02 | +4.46% |

| S&P/TSX Global Gold Index | 246.99 | +5.81 | +2.41% |

| XAU | 95.94 | +6.32 | +7.05% |

| Russell 2000 | 1,589.33 | +109.70 | +7.41% |

| S&P Energy | 437.36 | +21.43 | +5.15% |

| S&P/TSX VENTURE COMP IDX | 541.49 | -13.35 | -2.41% |

| Natural Gas Futures | 2.70 | +0.46 | +20.29% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| XAU | 95.94 | +4.12 | +4.49% |

| S&P/TSX Global Gold Index | 246.99 | +9.08 | +3.82% |

| Gold Futures | 1,515.10 | +82.70 | +5.77% |

| DJIA | 27,347.36 | +763.94 | +2.87% |

| S&P 500 | 3,066.91 | +113.35 | +3.84% |

| Nasdaq | 8,386.40 | +275.28 | +3.39% |

| Korean KOSPI Index | 2,100.20 | +82.86 | +4.11% |

| Natural Gas Futures | 2.70 | +0.50 | +22.75% |

| S&P Basic Materials | 370.03 | +6.56 | +1.80% |

| Russell 2000 | 1,589.33 | +38.57 | +2.49% |

| Oil Futures | 56.06 | +2.11 | +3.91% |

| Hang Seng Composite Index | 3,657.85 | -31.83 | -0.86% |

| S&P/TSX VENTURE COMP IDX | 541.49 | -49.84 | -8.43% |

| S&P Energy | 437.36 | -14.57 | -3.22% |

| 10-Yr Treasury Bond | 1.72 | -0.18 | -9.29% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (09/30/2019):

Gazprom PJSC

MMC Norilsk Nickel PJSC

Torex Gold Resources Inc

Royal Dutch Shell Plc

Franco-Nevada Corp

Starbucks Corp

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The STOXX Europe 600 Index is derived from the STOXX Europe Total Market Index (TMI) and is a subset of the STOXX Global 1800 Index. With a fixed number of 600 components, the STOXX Europe 600 Index represents large, mid and small capitalization companies across 18 countries of the European region: Austria, Belgium, Czech Republic, Denmark, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, the Netherlands, Norway, Portugal, Spain, Sweden, Switzerland and the United Kingdom. The S&P GSCI Total Return Index in USD is widely recognized as the leading measure of general commodity price movements and inflation in the world economy. Index is calculated primarily on a world production weighted basis, comprised of the principal physical commodities futures contracts. The Bloomberg Commodity Index is made up of 22 exchange-traded futures on physical commodities. The index represents 20 commodities, which are weighted to account for economic significance and market liquidity. The University of Michigan Confidence Index is a survey of consumer confidence conducted by the University of Michigan. The report, released on the tenth of each month, gives a snapshot of whether or not consumers are willing to spend money. The NIFTY 50 index National Stock Exchange of India’s benchmark broad based stock market index for the Indian equity market. The BSE SENSEX is a free-float market-weighted stock market index of 30 well-established and financially sound companies listed on Bombay Stock Exchange. The IDX Composite index lists and measures the performance of all stocks listed on the Indonesia Stock Exchange (IDX). It is also known as the JSX Composite – the Jakarta Stock Exchange index. The price-earnings ratio, also known as P/E ratio, P/E, or PER, is the ratio of a company’s share price to the company’s earnings per share. The ratio is used for valuing companies and to find out whether they are overvalued or undervalued.